Macro markets have settled down into a sleepy range market, with sentiment trending back into the familiar ‘goldilocks’ mode with both equity and bond prices grinding higher on lukewarm economic data and falling volatility.

The Trump administration has continued with their latest tariff ruminations, though the impact on markets appear to be fading as the bark appears to be worse than the bite. The latest reciprocal tariffs have been pushed back to April 1st, with Canada, Mexico, India, and China being named as the main counterparties being placed under scrutiny.

Net net, despite the high initial speculations, Trump 2.0 trades have performed poorly YTD, with the consensus ‘Trump-basket’ trades underperforming the main index substantially, with the USD and oil moving substantially lower, while EM equity and FX outperforming drastically.

Most notably, Chinese equities have done remarkably well, driven initially by Deepseek optimism and more recently by an apparently warming relationship between policy leaders and onshore tech companies. The HSI appears to be on the verge of breaking higher from a multi-year downtrend, with stalwarts such as Alibaba getting the attention of top US fund managers and allocators.

US economic data has been lukewarm, with CPI coming higher than expected last week, against weak retail sales on Friday. Rate cut odds have increased back to ~60% by June, with Chairman Powell trying his best to explicitly talk down inflation concerns in his latest House Financial Services Committee hearing:

“The CPI readings are almost above all forecasts, but I want to remind you of two points. First, we will not get excited over one or two good readings, nor will we get excited over one or two bad readings. Second, our inflation target focuses on the Personal Consumption Expenditures (PCE) price index because we believe it is a better measure of inflation. “ — Powell, February 13, 2024

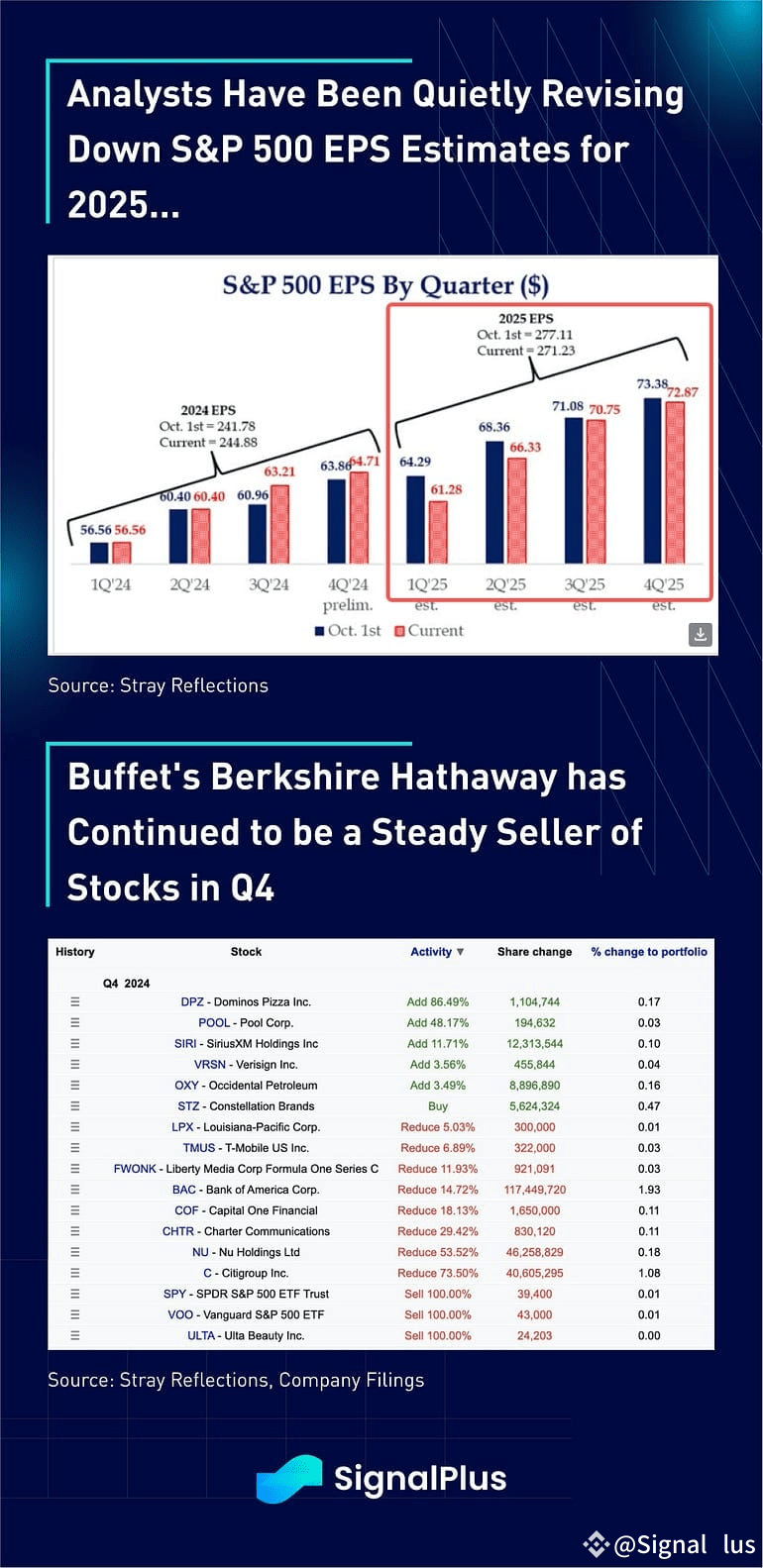

However, against the muted backdrop, equity EPS estimates for 2025 have fallen materially as analysts have been quietly lowering their quarterly projections. Furthermore, Warren Buffet has also been steadily taking down his equity exposure, and actually sold 100% of his SPX ETF exposures last quarter, including substantial de-risking in his bank holdings.

While YTD returns for equities has been a small positive, gold prices have been on a tear as there has been heavy demand for spot gold deliveries across various trading exchanges. Bloomberg reports that large shipments of bullion have been leaving the UK for US settlement as financial firms have been moving 70%+ more gold into COMEX-approved vaults, with ~300–400 metric tones of shipment being made from London to NY over the past 8 months.

Concerns for rising import prices from Trump’s tariffs have caused traders to stockpile gold more than usual, while the Fed’s cavalier approach towards inflation has also created a persistent demand curve for the foreseeable future.

Over in crypto, while gold has been outperforming handily against low realized, the embattled Ethereum has struggled on the other side of the spectrum, with prices falling 20% YTD against a ~60–70% realized vol, by far the worst performing vol-adjusted asset class across the major altcoin spectrum and against major equity indices.

The only saving grace that is that the trading sentiment is so universally negative against the #2 token, and that Trump’s Liberty Financial foundation has been expressly accumulating ETH in this downturn. Are we due for a dead cat bounce soon?

On the more positive side, cumulative inflows into BTC ETF have remained steady despite prices stagnating around 100k, while Tudor’s 13F filing also showed that IBIT was the fund’s largest single equity position ($12B AUM) as of the end of 2024.

Finally, in other news, FTX repayments will finally be made as of this week (initially to smaller accounts), and it’ll be interesting if the capital will be redeployed to crypto use as they start filling wallets throughout this quarter.