Judging from the economic data released by the United States in August, the US economy - this galloping locomotive - has finally shown some signs of slowing down.

The U.S. CPI rose 3.2% year-on-year in July, ending the previous 12-month decline. The forecast was 3.3%, and the previous value was 3.0%. The U.S. core CPI rose 4.7% year-on-year in July, and the forecast was 4.8%, and the previous value was 4.8%. The CPI has risen, but it is still lower than market expectations. The Fed's interest rate hike has been effective.

From the employment perspective, the U.S. labor market has also shown a certain degree of slowdown. In July, the number of new jobs in the U.S. non-agricultural sector was 187,000, lower than market expectations. In terms of hourly wages, the average hourly wage in the second quarter increased by 4.5% year-on-year, a slight slowdown from 4.8% in the previous quarter. The latest salary tracking data from the job search website Indeed shows that the annual salary growth rate in the job advertisements on the website is 4.7%, lower than 5.8% in April and 8% in July last year. The labor market has always been an important reference for the Federal Reserve to raise interest rates, because wages and prices tend to rise synchronously. The current reduction in wage expectations has undoubtedly put the labor market on the side of the Federal Reserve.

Similarly, the initial value of the US Markit Services PMI in August was 51 (expected 52.2, previous value 52.3); the initial value of the Markit Manufacturing PMI in August was 47 (expected 49.3, previous value 49). The manufacturing industry fell into contraction, and the expansion of the service industry was also lower than expected.

Numerous economic data indicate that the US economy has slowed down this month, but the economic data of a single month is not enough to determine the medium- and long-term economic trend, and the strength of the US economy is still at a high level. Powell also made a hawkish speech at the Jackson Hole meeting, saying that given the strength of the US economy, interest rates may continue to rise in the future.

Institutions are "deadlocked": the Atlanta GDP model predicts that the US economy will grow by 5.8%, but Fitch downgraded the US credit rating.

The Atlanta Fed's GDPNow model predicts that the third quarter GDP growth rate of the United States is 5.9% based on currently available data. However, the market believes that the data used in the model forecast (July retail sales, auto sales, new home starts, etc.) only reflects short-term conditions, and as future data is released and adjusted, the model forecast results will follow.

On the one hand, the model gave an extremely optimistic forecast, but on the other hand, Fitch downgraded the rating of municipal bonds related to the US sovereign rating to "AA+", which was the first time Fitch downgraded the US credit rating since it issued the rating in 1994. Blackstone Group's Stephen Schwarzman also echoed that Fitch's downgrade was "in line with the data." Fitch not only downgraded municipal bonds, but also said it might downgrade the ratings of dozens of US banks, including JPMorgan Chase. Institutions generally have complaints about the federal government's long-standing fiscal and debt problems, and Fitch's rating downgrade may be a concentrated reflection of this dissatisfaction.

The soaring U.S. Treasury yields in August have become a "beautiful landscape" in the global financial market, with both short-term and long-term Treasury bonds soaring. The yields on 10-year and 30-year U.S. Treasury bonds hit their highest levels since 2007 and 2011, respectively; the interest rates on short-term Treasury bonds such as 1-year, 2-year and 5-year bonds remain high and have been trading sideways at high levels for several months.

In fact, it is not just U.S. Treasury bonds, but also bond yields in countries such as Japan and Germany that remain high.

Why did the US Treasury yields soar so rapidly? The current wave of interest rate increases in Treasury bonds is most likely a quick response to the interest rate hike. The US economy continues to be strong, and many scholars no longer expect a recession in the US this year, which in turn fuels the market's expectations of another rate hike by the Federal Reserve, causing interest rates to continue to rise. In addition, Fitch believes that the government's fiscal risks continue to deteriorate, which also reduces the market's confidence in US Treasury bonds, which will inevitably lead to an increase in the financing cost of US Treasury bonds.

The result of the surge in U.S. bond yields is that risky assets are under great pressure. This month, the three major U.S. stock indexes closed down across the board. The risks of crypto assets such as Bitcoin were also released on August 18, but they have not recovered the decline so far. Although Nvidia, the "global AI leader", continued to trade sideways at a high level and set a new high, other technology heavyweights showed a continued downward trend. This month, Nvidia released its second quarter report, in which revenue doubled year-on-year, 22% higher than expected, and EPS earnings increased more than four times year-on-year, nearly 30% higher than expected. The third quarter revenue guidance is 160±2% US dollars, a year-on-year increase of 170%, 28% higher than expected, far exceeding market expectations. Subsequently, Nvidia continued to announce that it would spend 25 billion US dollars to repurchase the company's shares. This behavior shocked the market and brought endless imagination to investors. Various institutions have raised their expectations for Nvidia's stock price, and the most optimistic bulls have raised their stock price expectations to US$1,100 (Rosenblatt).

As the "largest arms dealer in the AI era", Nvidia is in the limelight. Indeed, AI is still the new track with the most certainty and a very broad market. Generally speaking, it is an important signal that giant companies have exceeded market expectations for two consecutive quarters, indicating that there is good synergy between the upstream and downstream of the industry, that is, the formation of an industrial chain. AI may be the most certain track in the U.S. stock market under the pressure of U.S. debt, and it may usher in institutional groups.

The crypto market is currently showing bottoming characteristics.

First, the sudden plunge in the price of Bitcoin in August led to long liquidation and intensified speculation in the market. On the 18th, there was an "earthquake" in the currency market: major mainstream currencies crashed, Bitcoin fell to a minimum of 24220USDT, and ETH fell to a minimum of 1470.53USDT, and has not recovered the decline so far. We also mentioned above that this plunge was mainly due to the concentrated release of risk aversion sentiment, not caused by certain news. This plunge caused a 24-hour liquidation of US$990 million across the network, an increase of 737.87% over the previous trading day, and long liquidation increased significantly.

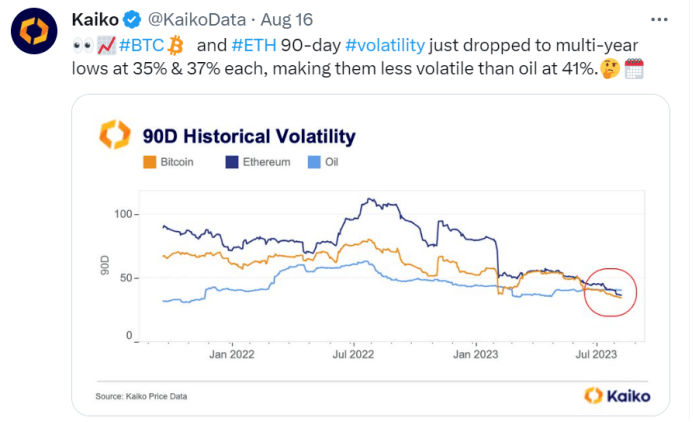

Secondly, Bitcoin's volatility and trading volume are at historical lows, and its price performance is sluggish. This month, Jacobi Asset Management launched Jacobi FT Wilshire Bitcoin Spot ETF, which was launched on Euronext Amsterdam on August 15, but the market had little reaction to the news, and instead experienced a stampede and plunge. This has already reflected that market sentiment is relatively sensitive and confidence is insufficient. One of the characteristics of the bottom of the secondary market is that it is not sensitive to positive news, but very sensitive to negative news, and is prone to pessimistic stampede and plunge. At present, whether from the market or sentiment perspective, the crypto market is likely to have a bottom.

In addition, the DeFi TVL locked volume has continued to decline this month, hitting its lowest point since February 2021, currently at about $38.134 billion. This is a drop of more than 70% from the peak of over $170 billion during the Defi Summer in 2021.

But on the other hand, from a global perspective, the Web3 industry has continued to benefit. Since the beginning of this year, nearly 10 large financial institutions, including BlackRock, have submitted Bitcoin spot ETF applications to the US SEC. On August 30, it was reported that a US federal court approved the cryptocurrency fund Grayscale Investments to launch the first Bitcoin ETF in the United States, and the US court overturned the SEC's decision to block the ETF, paving the way for the first Bitcoin ETF.

At the same time, encryption laws in various places are becoming more and more perfect, especially the encryption market in Hong Kong is accelerating. From the vice president of HKUST who once again suggested that the government speed up the support of Hong Kong dollar stablecoin, to Li Jiachao publicly stating that "we are fully exploring the issue of stablecoin regulation", to HashKey Exchange supporting compliant "Hong Kong drifters" to open accounts for trading, Hong Kong's "encryption-friendly" pace is getting faster and faster. At present, the first batch of "licensed" cryptocurrency exchanges in Hong Kong have landed. HashKey Exchange and OSL Digital Securities announced in August that they have obtained approval from the Hong Kong Securities and Futures Commission to provide virtual asset trading services to retail users. As one of the world's three major financial centers, Hong Kong can set an example in the compliance construction of digital asset transactions, which also gives us hope for the future of encrypted assets.

The Chinese and American economies are experiencing a "dislocation". The resilience of the US economy and the temporary pressure on the Chinese economy are intertwined, casting a shadow of uncertainty on global investors. Risk aversion has dominated the global secondary market trend this month. Both US stocks and Chinese A-shares have performed poorly, and the crypto market has experienced a plunge that has caused many people to blow up their positions.

However, the crypto market has obvious bottom characteristics, and the sentiment is also experiencing the most difficult "dark night before dawn". From the first batch of "licensed" cryptocurrency exchanges in Hong Kong to the upcoming release of Bitcoin spot ETFs, all of these indicate that the development of Web3 is in the ascendant. From the market perspective, the bottom of this round of the currency market has also been showing a fluctuating upward trend. In the future, there may be events that stimulate the currency price to break through the pressure level of $30,000, and then there may be a new wave of increases.

Copyright Statement: If you need to reprint, please add our assistant on WeChat for communication. We reserve the right to pursue legal liability for any unauthorized reprint or plagiarism.

Disclaimer: The market is risky and investment should be cautious. Please strictly abide by the local laws and regulations when considering any opinions, views or conclusions in this article. The above content does not constitute any investment advice.