As governments and financial institutions explore digital money, two models dominate the conversation: Central Bank Digital Currencies (CBDCs) and stablecoins. While both aim to modernize payments and settlement, their design philosophies, trade-offs, and long-term implications are fundamentally different. From Plasma perspective, understanding these differences is critical to shaping a scalable, neutral, and globally usable financial system.

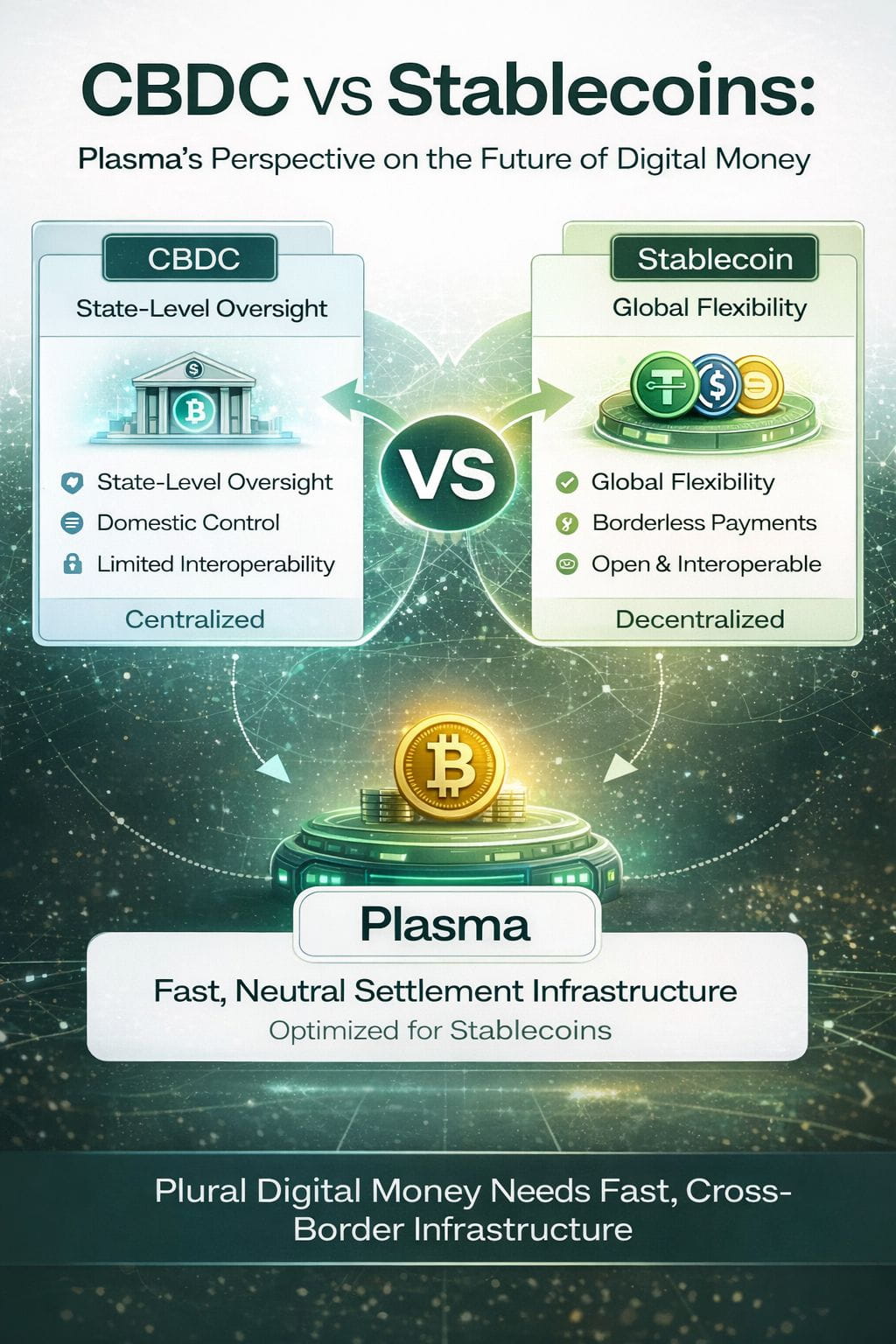

CBDCs are digital versions of national currencies issued and controlled directly by central banks. Their primary strength lies in state-level oversight and integration with existing monetary systems. Governments see CBDCs as tools to improve payment efficiency, reduce cash usage, and enhance regulatory visibility. However, this control comes with trade-offs. CBDCs are inherently permissioned, often limited by geographic borders, and tightly coupled to domestic policy decisions. For users, this can mean reduced privacy, potential programmability of money, and limited interoperability across borders.

Stablecoins, on the other hand, are typically issued by private entities and operate on public blockchains. Their key advantage is flexibility. Stablecoins move globally, settle instantly, and operate 24/7 without relying on traditional banking hours. They are already widely used for cross-border payments, remittances, on-chain settlement, and digital savings. While regulation and issuer risk remain important considerations, stablecoins have proven their ability to function as internet-native money.

Plasma architecture is built around this reality. Plasma does not compete with CBDCs as a government instrument. Instead, it provides neutral, high-performance infrastructure where stablecoins can operate reliably at scale. By focusing on stablecoin settlement rather than speculative activity, Plasma enables fast finality, predictable costs, and continuous payment flow, qualities essential for real-world financial usage.

One of the most important distinctions Plasma highlights is interoperability. CBDCs are likely to remain siloed within national systems, while stablecoins already operate across borders and platforms. Plasma amplifies this advantage by acting as a payment rail optimized for stablecoins, allowing them to move efficiently between users, institutions, and applications without friction.

Privacy and neutrality also play a role. CBDCs prioritize oversight, which may be suitable for domestic policy goals but less appealing for global commerce. Plasma, by anchoring security to Bitcoin and supporting permissionless stablecoin transfers, offers a more censorship-resistant and neutral settlement layer, while still remaining compatible with regulatory frameworks at the application level.

Plasma views the future of digital money as plural, not exclusive. CBDCs may serve domestic monetary systems, while stablecoins power global, borderless finance. Plasma role is to ensure that when stablecoins are used, for payments, savings, or settlement, they operate on infrastructure designed for reliability, scale, and trust. In that future, stablecoins are not just alternatives to CBDCs; they are complementary tools, and Plasma is the bridge that helps them move efficiently in a global financial system.