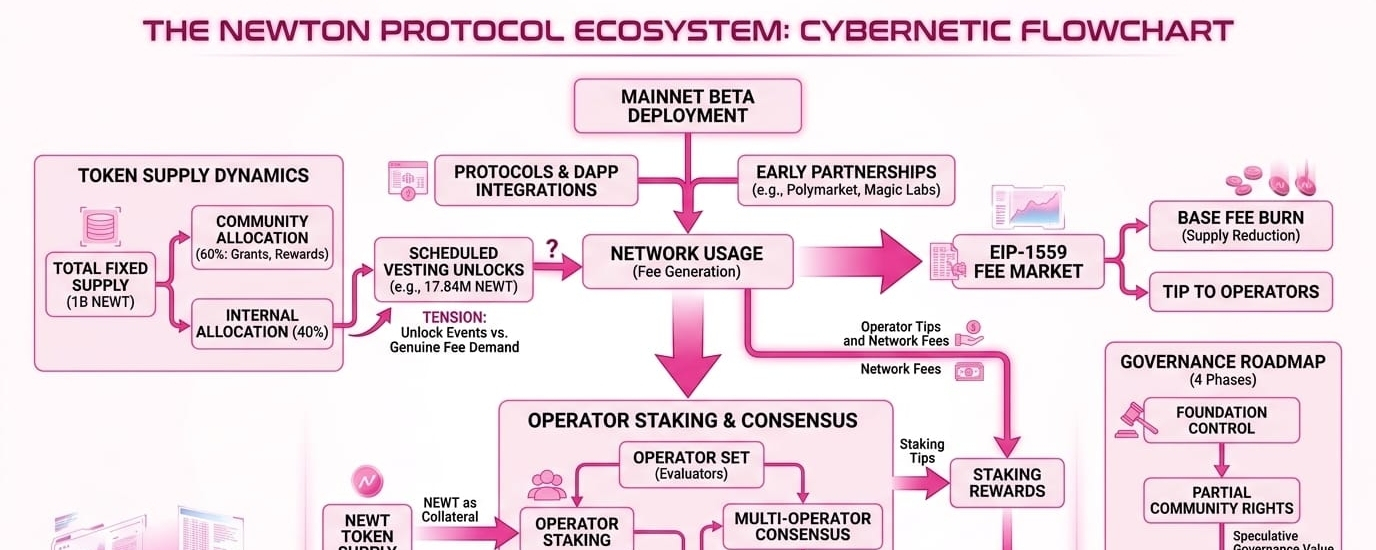

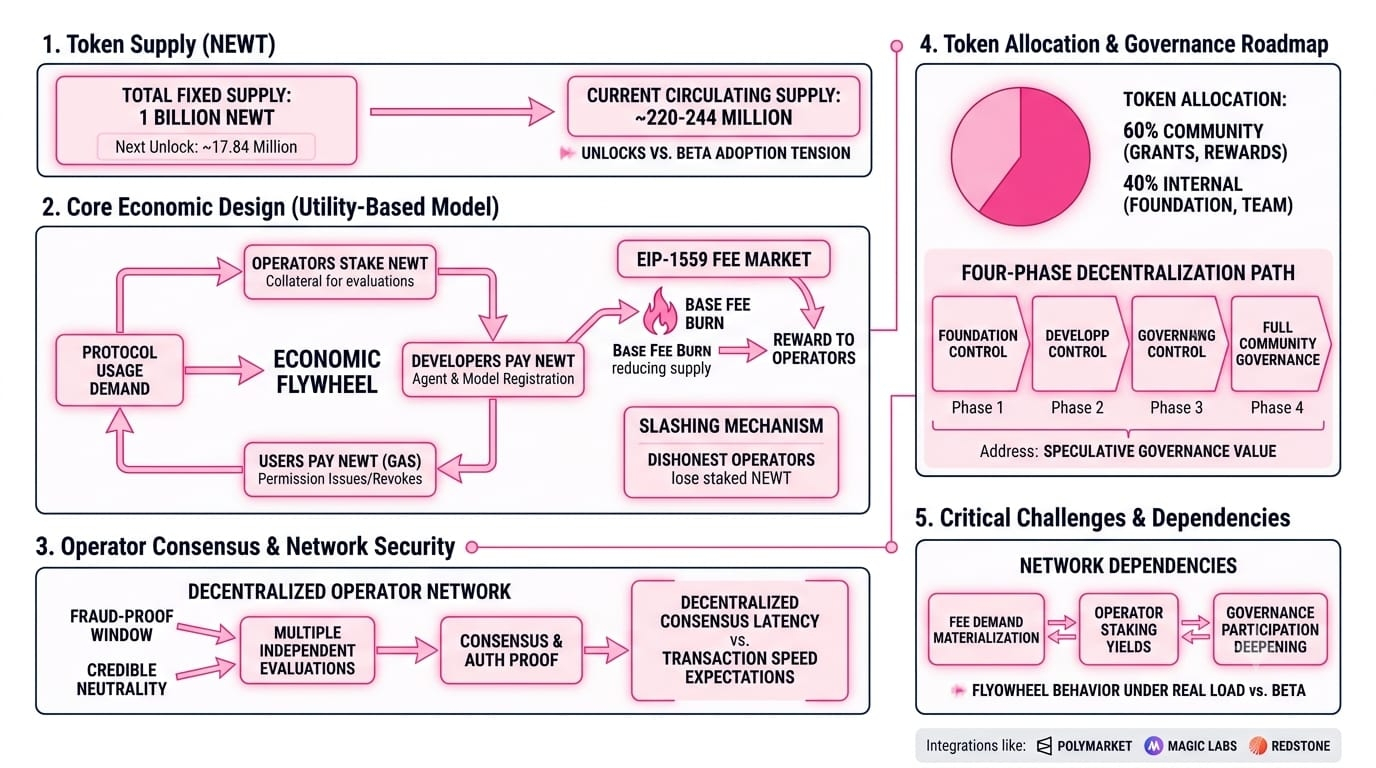

I was sitting with the Newton Protocol token documentation the other night, not for any particular reason, just one of those late sessions where you pull a thread and end up three hours deep into foundation disclosures and vesting schedules. What started as a quick look at circulating supply turned into something more complicated. The total fixed supply is one billion NEWT with no inflation built in, which sounds clean on paper, but when I started mapping the unlock timeline against the stage the protocol is actually at right now, mainnet beta, early integrations, a handful of live partners, I started noticing a tension that doesn't get talked about much. The next scheduled unlock is sitting just weeks out, releasing roughly 17.84 million tokens. That's not enormous relative to total supply, but when you look at the current circulating figure of around 220 to 244 million tokens and a market cap still finding its footing, even moderate unlock events carry more weight than they would at a later stage of adoption. I sometimes wonder whether the timing of supply events relative to actual protocol usage is the thing most people should be studying here, and whether the current phase of beta deployment is generating enough genuine fee demand to absorb what's coming out of vesting over the next few quarters.

What seems interesting to me about the economic design is that Newton isn't trying to sustain token value through inflation rewards or liquidity mining. The model is built around real utility demand: operators stake NEWT as collateral to run policy evaluations, developers pay NEWT to register agents and models in the marketplace, and users pay NEWT as a gas fee whenever they issue or revoke permissions. The fee market is modeled after EIP-1559, which means there's a base fee that adjusts with demand and a burn mechanism embedded into the structure. On paper this is elegant. The protocol absorbs token supply from the market through genuine usage, and dishonest operators face slashing, losing a portion of their restaked collateral if they sign off on incorrect policy evaluations. The economic incentives point in the right direction. But the question that comes to mind is whether enough transactions are flowing through the policy layer right now to make those incentives meaningful. A staking and slashing model only creates real security if operators have enough at stake to make dishonesty costly, and that requires a certain volume threshold that I can't easily verify from the outside.

The part I keep returning to is the operator consensus mechanism specifically. Once the protocol moves fully out of beta, multiple independent operators evaluate the same transaction proposal, reach agreement, and the network issues a single compact authorization proof. No single operator decides the outcome, and the fraud-proof window means any incorrect approval can be challenged and penalized retroactively. Looking from the outside, this is a genuinely robust design for credible neutrality. But it also introduces a latency and coordination layer that doesn't exist in simpler centralized compliance checks. The question that comes to mind is whether the protocols most likely to adopt Newton early, teams without large compliance budgets, smaller stablecoin issuers, newer RWA platforms, are actually equipped to reason about the tradeoff between decentralized consensus latency and the speed their users expect. I'm not completely sure the friction is prohibitive, but I also haven't seen a clear benchmark published for how long the evaluation cycle actually takes at current operator counts during beta. That gap in public information makes it harder to assess whether the user experience is competitive with what a centralized compliance vendor could offer.

The governance roadmap adds another layer of complexity worth sitting with. The foundation has outlined a four-phase decentralization path, moving from foundation control toward full community governance over staking rewards, fee structures, budget approvals, and ecosystem priorities. That's a reasonable structure for a protocol that needs to ship fast early on while eventually handing control to stakeholders. But I sometimes wonder about the period between where Newton is now and where full decentralization lands. During that transition, NEWT holders have partial governance rights that progressively expand, which means the token carries governance value that is partly speculative, priced on where the protocol will be eventually rather than what holders can actually influence today. It makes me think about how markets historically price governance tokens during intermediate phases, and whether the gap between current utility and future governance weight gets reflected rationally or whether it creates volatility as each new phase unlocks new rights. The 60-40 community-to-internal token allocation is another thing I find myself chewing on. Sixty percent directed toward ecosystem grants, network rewards, and community initiatives signals intent toward decentralization, but the actual pace at which that community allocation reaches active participants and generates real behavioral engagement is something only time and transparency reports will reveal.

The thing I keep coming back to at the end of all this is that Newton Protocol is trying to solve a genuinely hard coordination problem. It's building economic infrastructure, a fee-paying operator network with slashing and staking, underneath a compliance product that most of its target users have never needed to think about at the transaction layer before. For that infrastructure to work the way it's designed, usage has to scale fast enough to make staking economically attractive for operators, fees have to flow consistently enough to validate the EIP-1559 model, and governance participation has to deepen meaningfully as each phase of decentralization unlocks. Each of those conditions depends on the others in ways that create a compounding dependency. If operator counts stay thin during beta, evaluation consensus gets fragile. If fee demand doesn't materialize quickly enough, staking yields compress and operator participation weakens. I'm not saying any of this is inevitable, and the existing integrations, the Polymarket deployment, the Magic Labs developer network, the RedStone data partnership, suggest the foundation is more solid than many early-stage infrastructure plays. But I hold the conviction loosely, because what's genuinely hard to know from the outside is how the economic flywheel between fee generation, operator incentives, and token demand actually behaves under real load rather than beta conditions. The real character of this system probably only reveals itself once the guardrails of beta come off and the network has to sustain itself on usage alone, anyway, time will tell

#BitcoinFalls44%FromJanuaryPeak #SouthKoreanStocksRise5% #DowHitsRecordHigh #PhiladelphiaSemiconductorIndexFalls4%