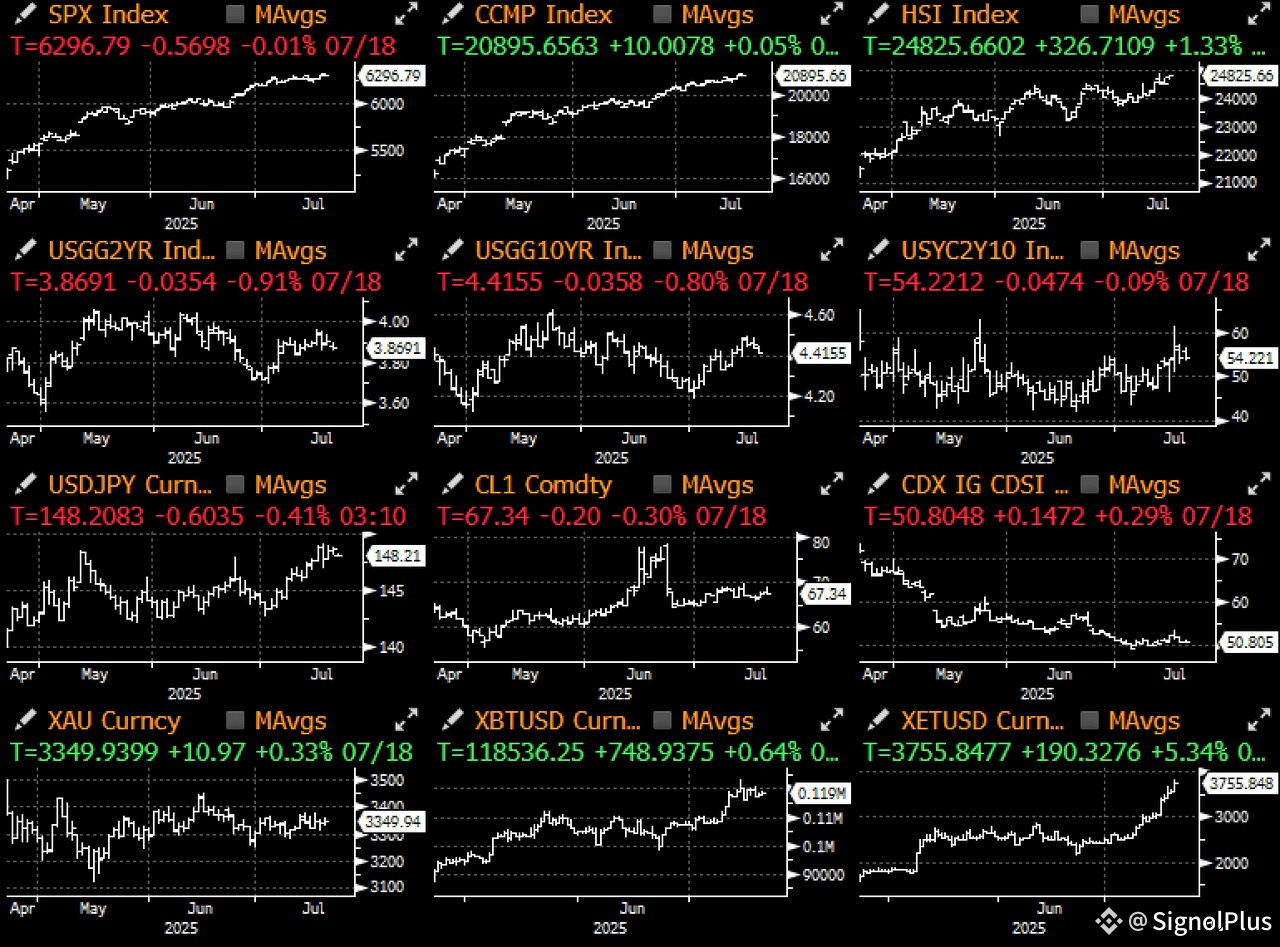

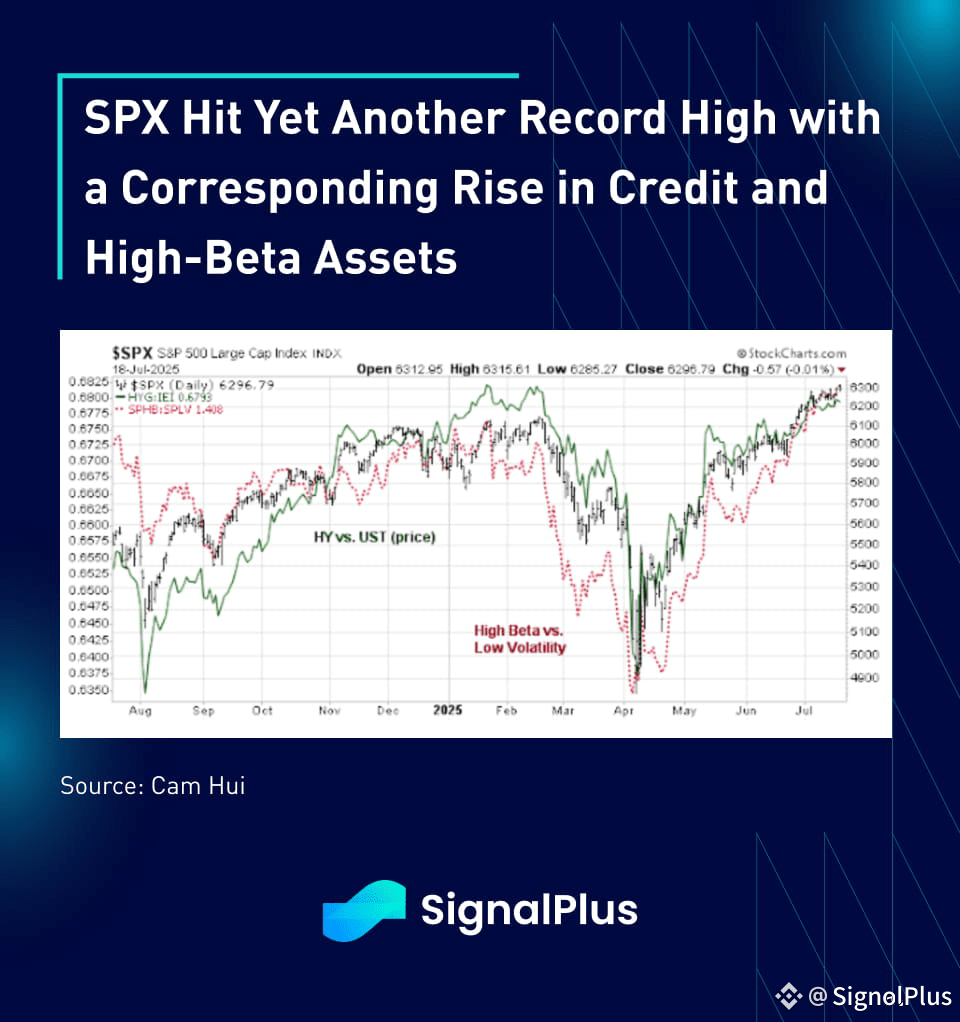

Another week, another record high. The SPX hit another ATH on Friday, the 3rd fresh record for the week and the 6th in July. The market continued to ignore ongoing tariff escalations (30% on Mexico & EU), nascent price-pressure passthroughs in the latest CPI, and the latest drama to terminate Fed Chair Powell ‘for cause’.

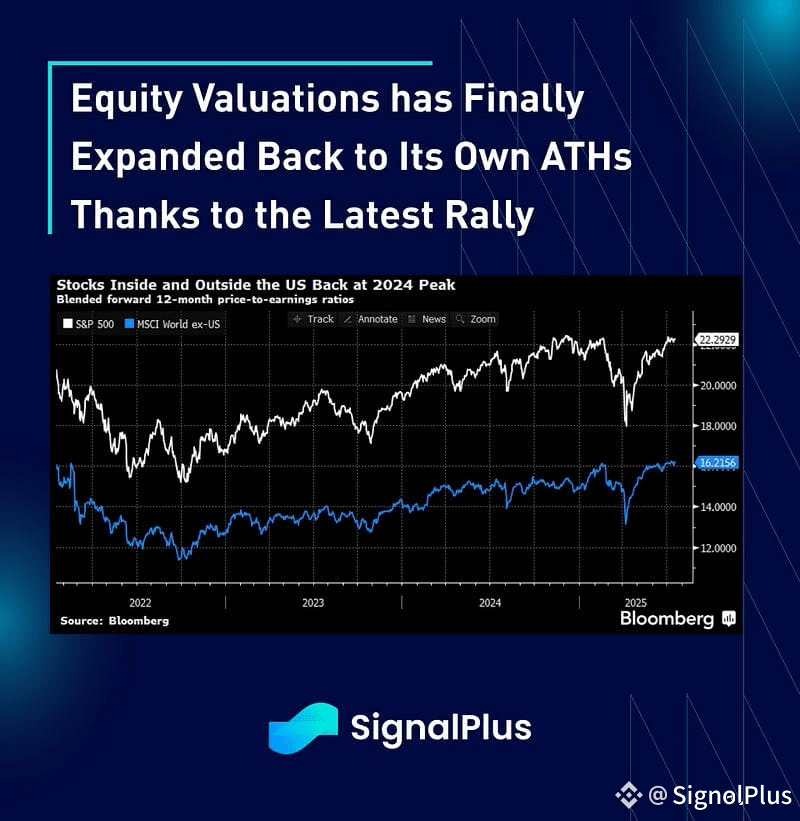

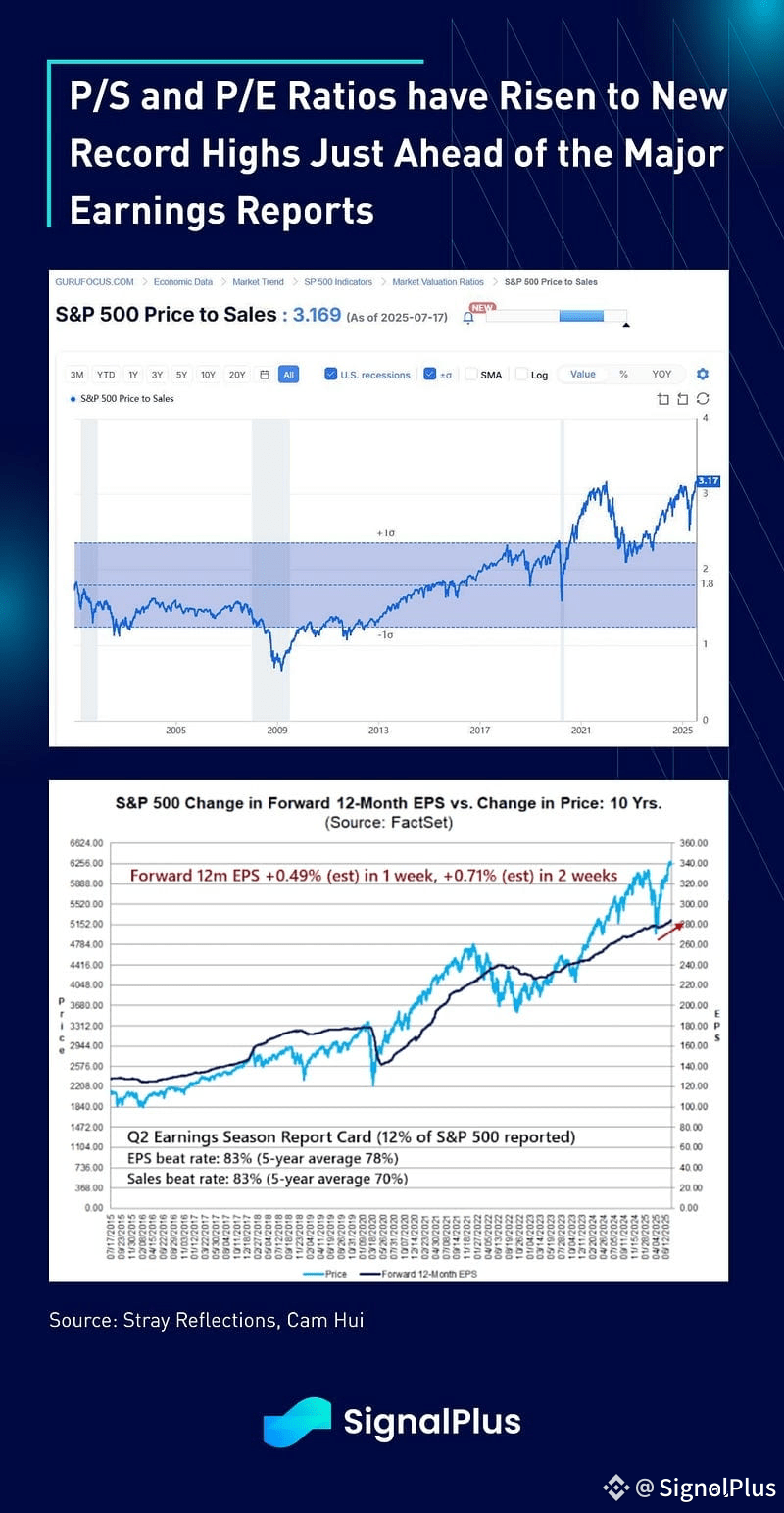

The latest rally has expanded the S&P 500’s price-to-earnings ratio close to its own all time highs, just ahead of the Q2 earnings season as investors pay up for any sort of equity exposure.

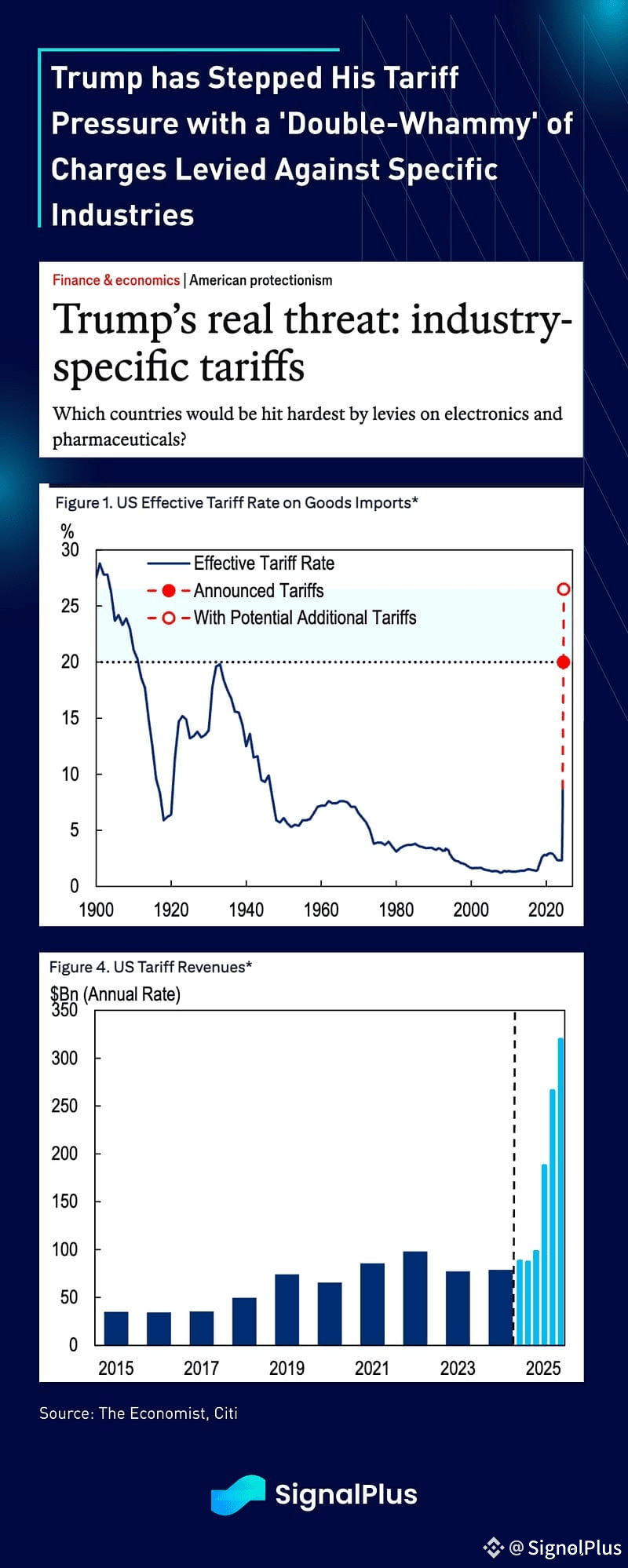

Meanwhile, embolded by the stock market’s performance, President Trump has revigorated his tariff escalation and is readying plans for industry-specific tariffs to kick in alongside the current country-specific tariffs, supposedly to take place in 2 weeks’ time. The initial targeted sectors will be on pharmaceuticals and semiconductors, which is intended to supplement and over the US’s entire sphere of imports.

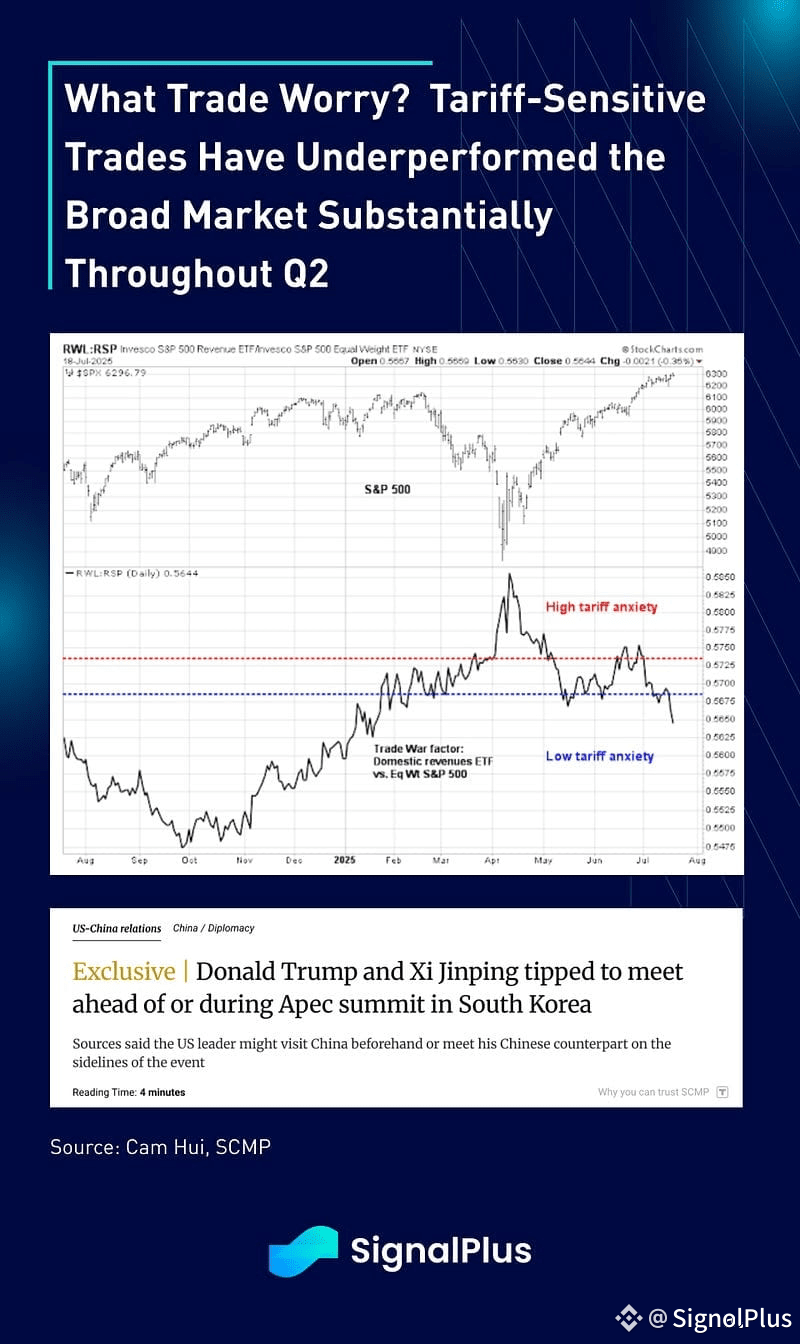

Even with the renewed threat, the market has all but brushed off this current round of tariff escalation, with ‘tariff-sensitive’ themes continuing to underperform benchmark indices. Whether it’s due to expectations of an eventual ‘TACO’ moment, a lessening of pointed-aggression against the major trading partner (Xi-Trump meeting expected to take place in Korea), or confidence that the private sector will cope with the fallout, the market will likely remain tone-deaf to trade conflicts until further notice.

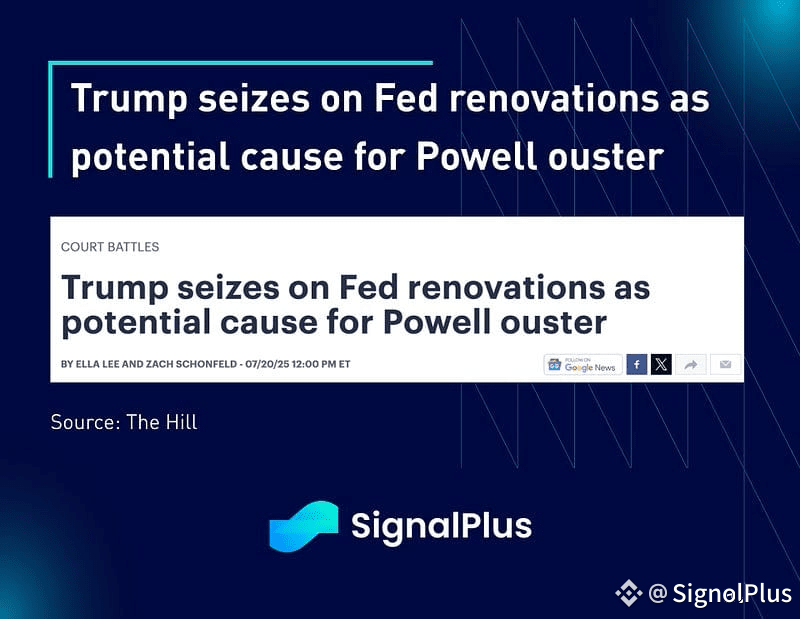

Speaking of policy, the Trump administration has whipped up the latest Fed drama with media stories surfacing on how Fed Chair Powell might be ousted over issues of building budget overruns. Yes, you read right.

Some $2.5 billion in renovations to the central bank’s headquarters in Washington have put Powell in the hot seat over management of the project, which has cost about $600 million more than initially expected. Asked Tuesday if the pricey updates are a fireable offense, Trump said, “I think it sort of is.” — The Hill

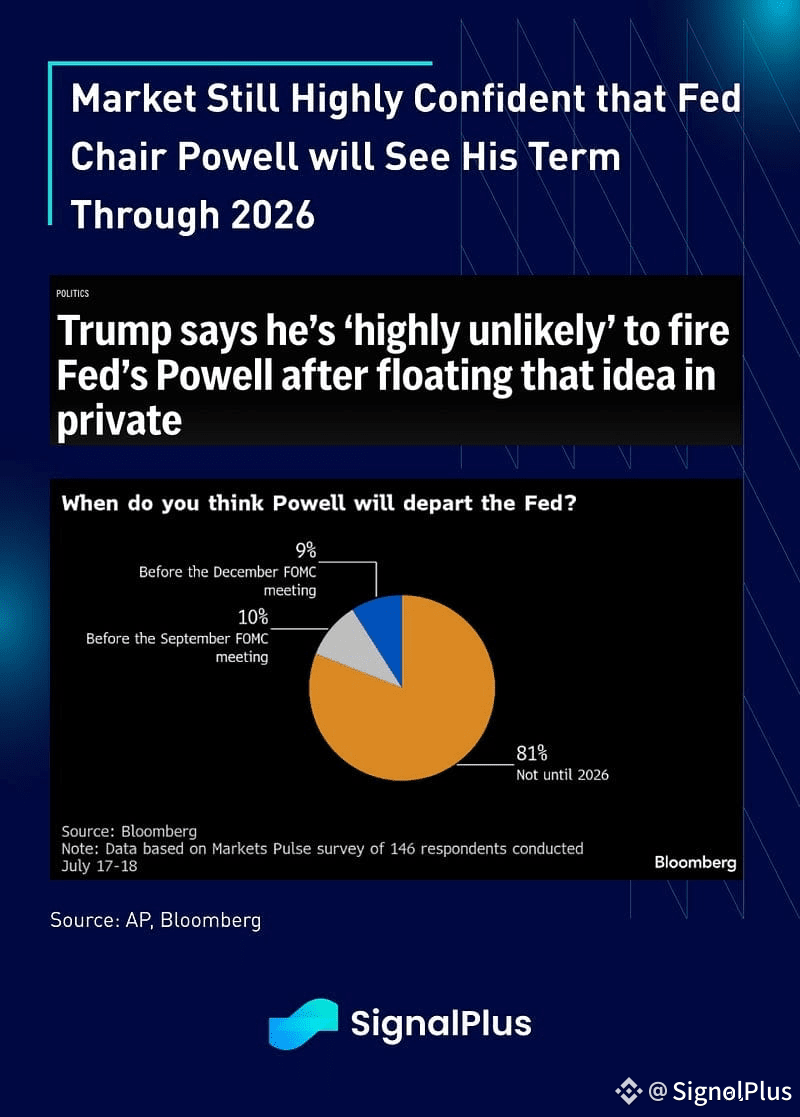

After leaking that ludicrous statement, Trump quickly walked back on that threat with the market also in overwhelming consensus that Powell will see his term through 2026.

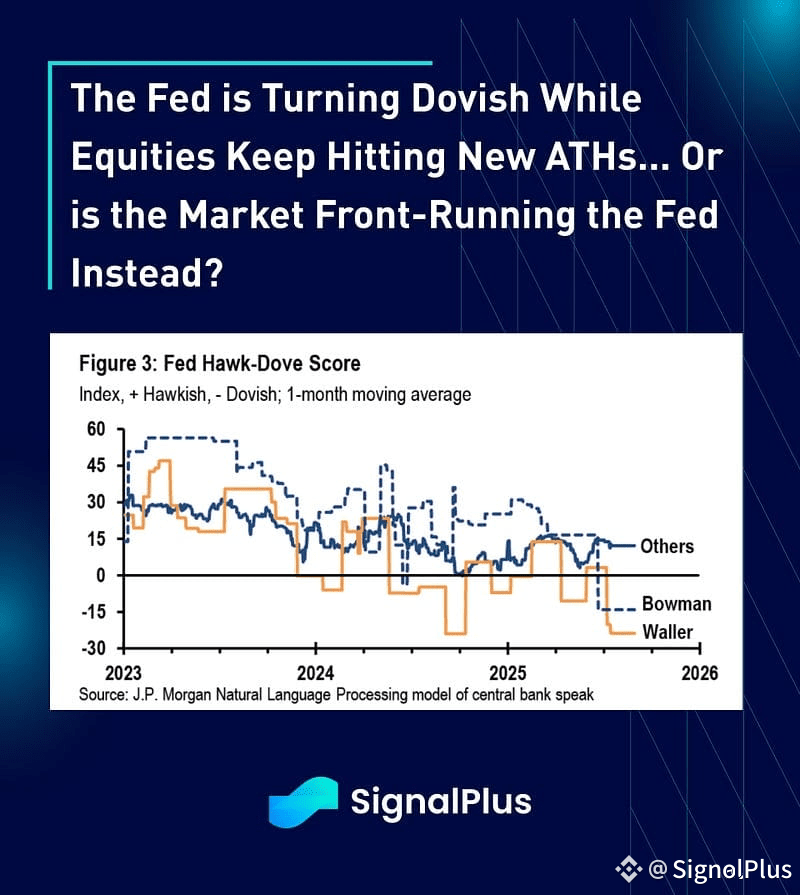

Meanwhile, in a somewhat unconventional move, Fed Governor Waller gave an early ‘dissent’ by publicly stating that he would prefer to see rates lowered in the July meeting, stating that “the private sector is not doing as well as everybody thinks it is”, with the US labour market also “on the edge” as most of the employment is concentrated in the public sector.

With the Fed-speak turning dovish while markets keep hitting ATHs, is there any wonder that the market is currently in as much of a risk-on mode as it has been over the past 2 months? Or are markets forward pricing a dovish-Fed, hence front-running the incoming rate cuts and leading to the Golidlocks narrative?

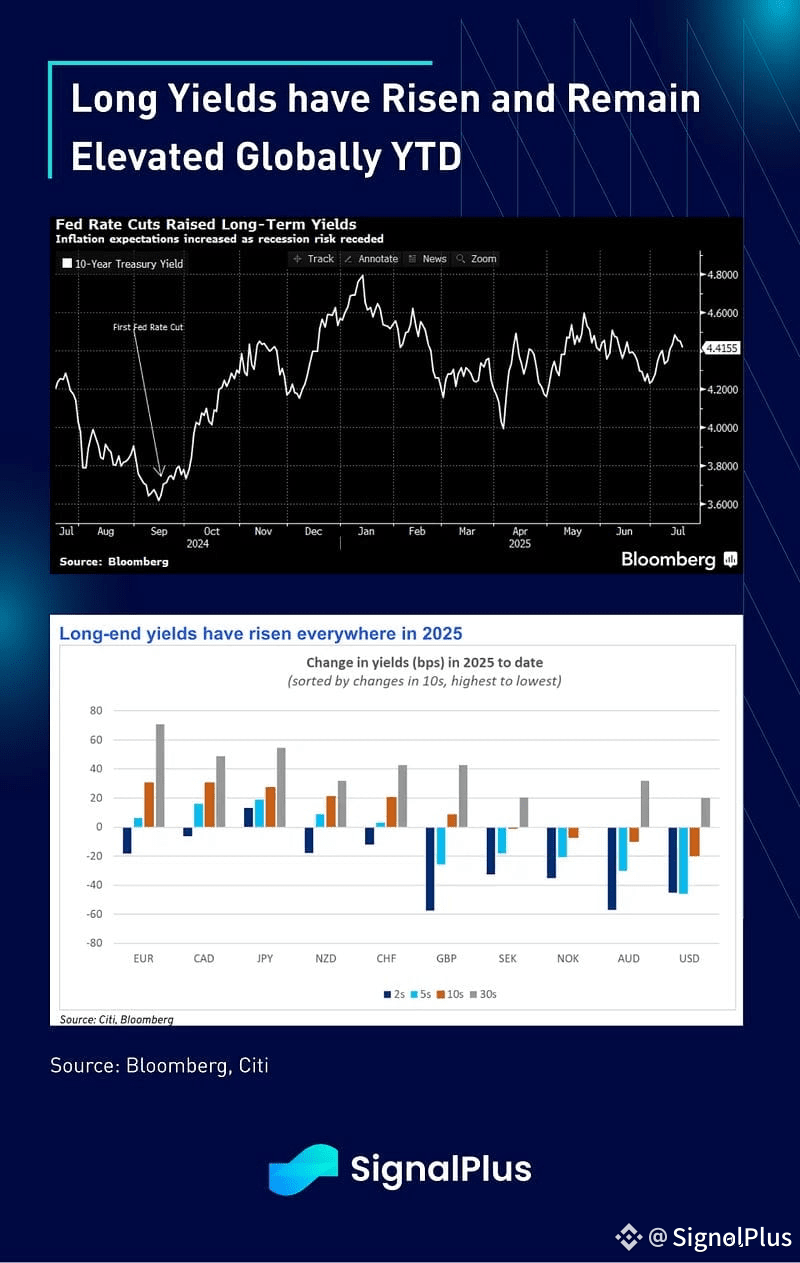

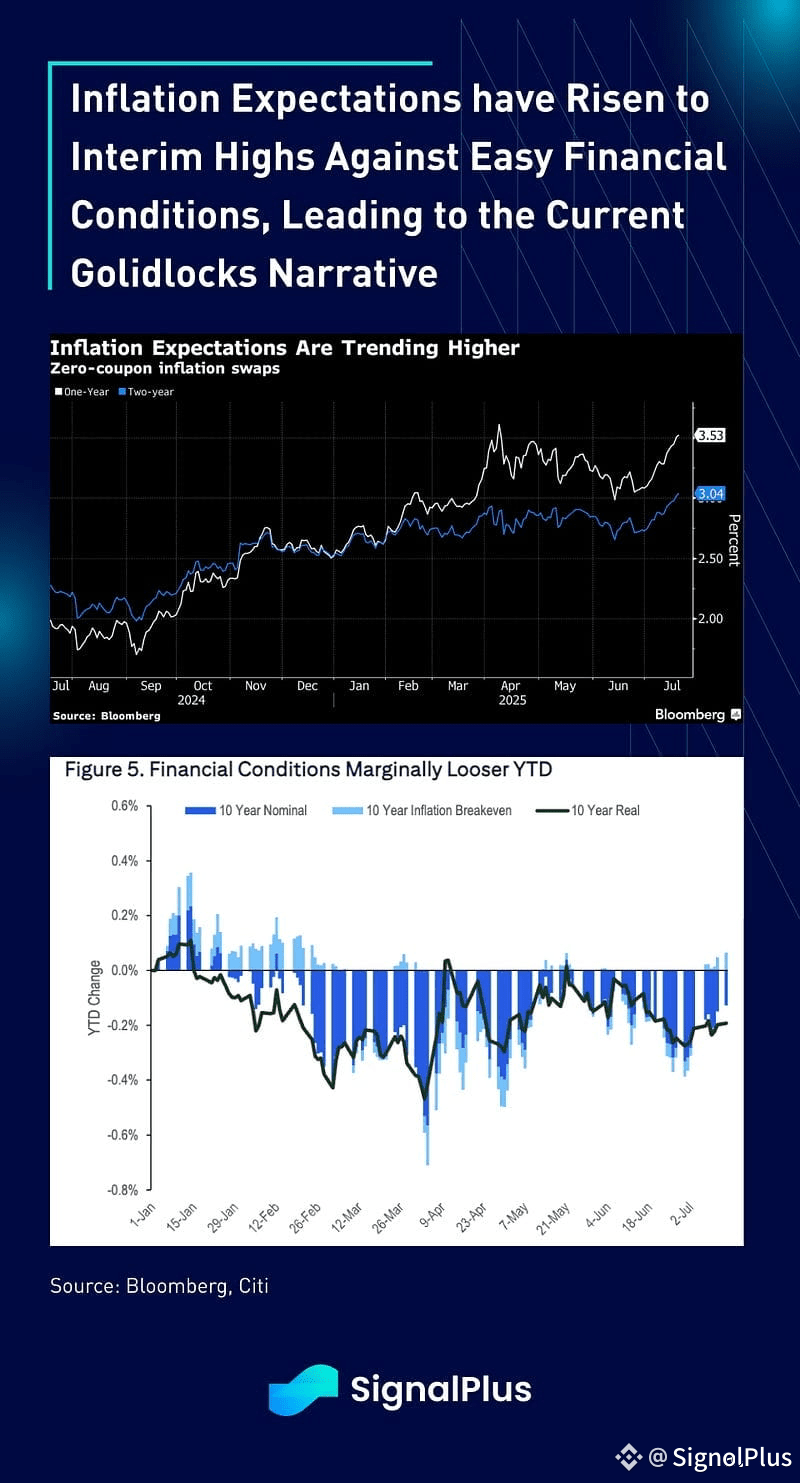

Regardless, inflation expectations have creeped back in with long-dated yields staying elevated globally, while inflation breakevens have climbed back to the highest level in years as financial conditions stay loose.

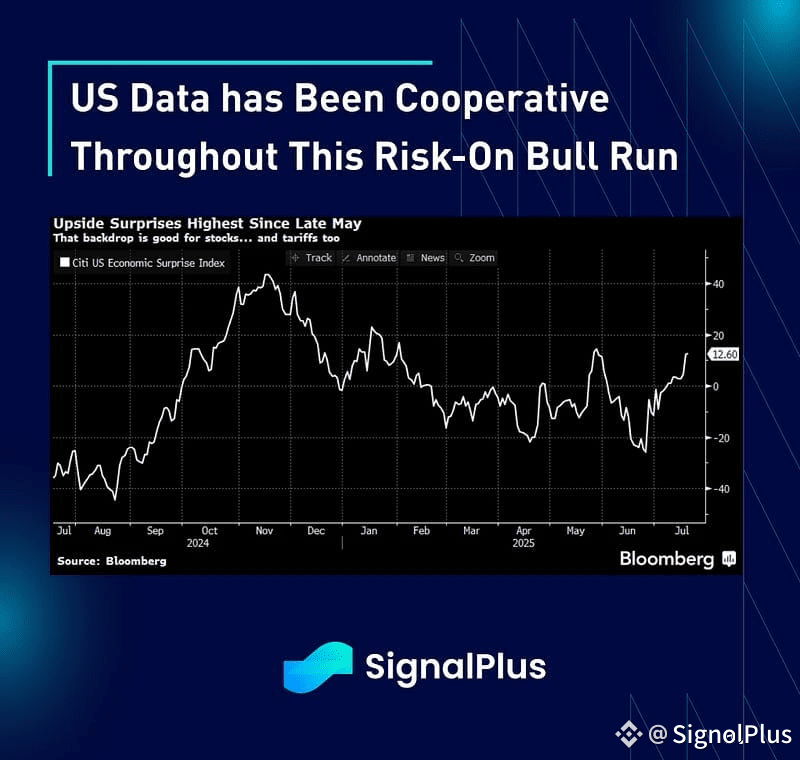

Data was also cooperative over the past week, with the UMich report showing a modest improvement in consumer sentiment across both current conditions and future expectations, while 1yr inflation expectations have dropped to pre-tariff levels at 4.4% vs 5.0% prior.

This week will see earnings reports kicking into high gear with Tesla and Alphabet due to report on Wednesday. According to Bloomberg, we have seen 58 out of 498 stocks reporting in the S&P 500, with earnings surprising on the upside by 7.8%. Even against the rising earnings, price-to-sales and price-to-earnings ratios have risen to or above record highs across both US & global stocks, with investors paying ‘full price’ for tacking on risk-exposure at this juncture.

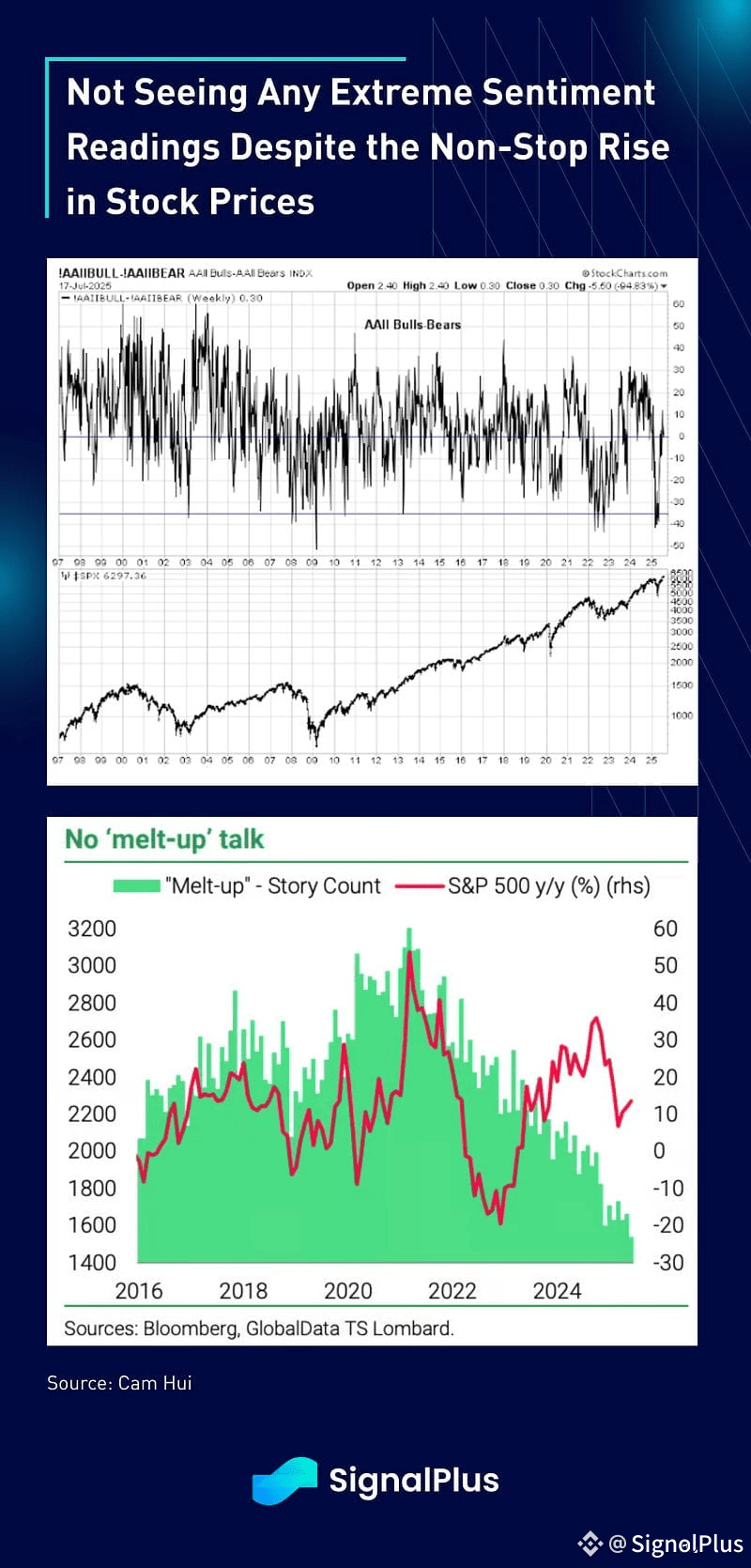

Surprisingly, despite the incessant rise, we have yet to see extreme sentiment readings across conventional momentum measures, with AAII Bull-Bears ratio stuck at around the middle of the range, and search engine queries for ‘melt-up’ stories remain at record lows.

Has the macro doom-bears finally gone extinct for good, and everyone embracing the ‘stock-only-go-up’ mantra? Don’t fade the rally…

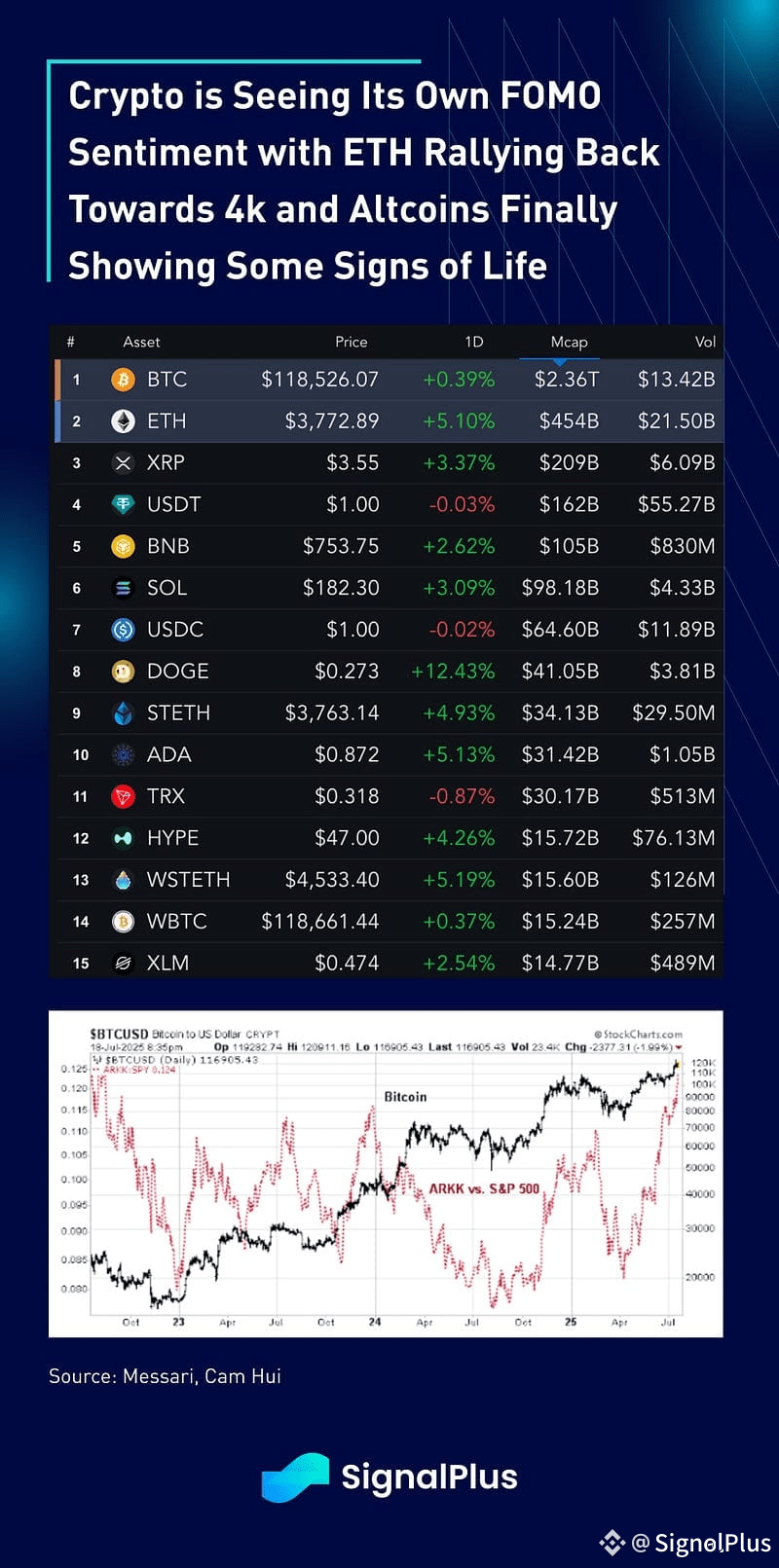

Crypto has certainly not shied away from our own FOMO moment, with Ethereum having a fantastic week as we approach the $4k area (+22% over 5 trading days), and a number of major altcoins seeing double digit gains for the week. BTC has also reached its own record highs at above $118k, albeit with more restrained excitement, as it certainly feels like that the good days are back until further notice.

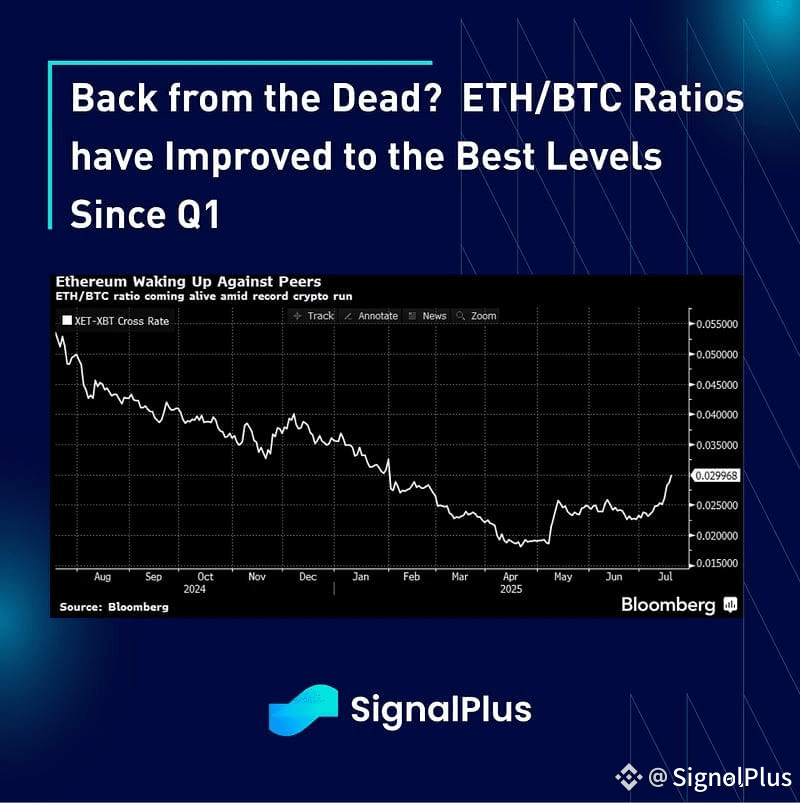

The ETH/BTC ratio has temporarily revived from its grave, and has improved to the best levels since Q1. Some will credit the stablecoin / RWA focus being beneficial for the proof-of-stake network, while others will point to the new ETH-based treasury plays as catalyst for the rally. We personally think it’s just a good old-fashioned risk-on spill over with most of mainstream TradFi having been fully positioned on BTC over the past 7 months.

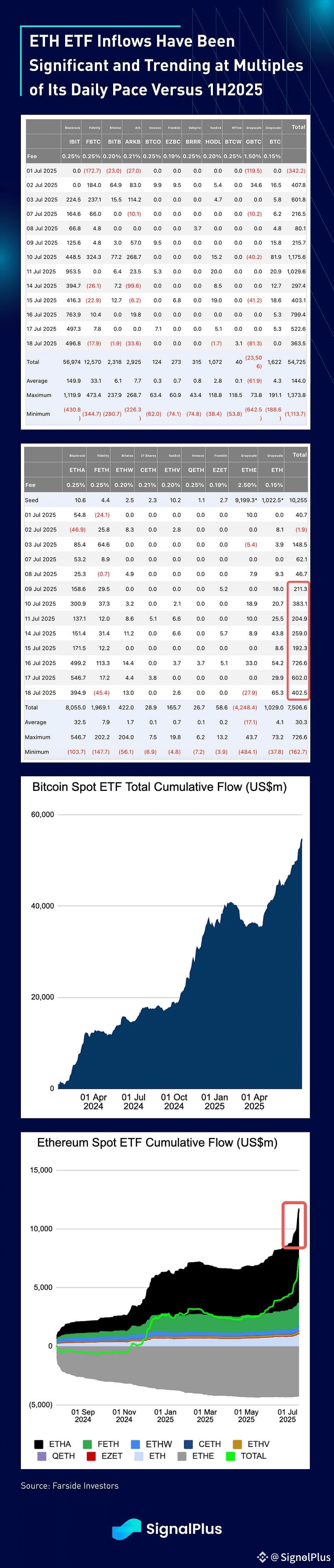

As a positive milestone, Congress did finally pass its landmark stablecoin legislation over the past week, trading tighter federal and state regulations for more venues for stablecoin payments. This has probably spurred on some structural tailwind with ETH ETFs seeing record inflows in the past 2 weeks, totalling over 3bln in July with daily figures (300–500M) trending at 5–10x the amounts seen in the 1H of the year.

At the risk of echoing the same concluding thoughts as we have for the better part of the past 8 weeks… Never short a boring market and enjoy the good times as they roll. Good luck and good trading to all our friends as we head into the dog days of summer!