The central bank warns of the risks of US dollar stablecoins, impacting the stability of the New Taiwan dollar exchange rate

With the booming development of the cryptocurrency market, the circulation scale of US dollar stablecoins has been expanding, drawing close attention from Taiwan's financial regulatory authorities.

According to reports from (Central News Agency), Taiwan's central bank recently pointed out that if US dollar stablecoins are widely used, they may become a tool to evade Taiwan's current foreign exchange regulations, which not only weakens the central bank's monitoring of cross-border capital movements but may further affect the stability of the New Taiwan dollar exchange rate.

The central bank emphasized that in the future, in addition to strengthening monitoring measures, it does not rule out formally incorporating information related to stablecoins into the observation indicators of monetary policy management to ensure the order of the financial market.

How do US dollar stablecoins bypass existing currency exchange regulations?

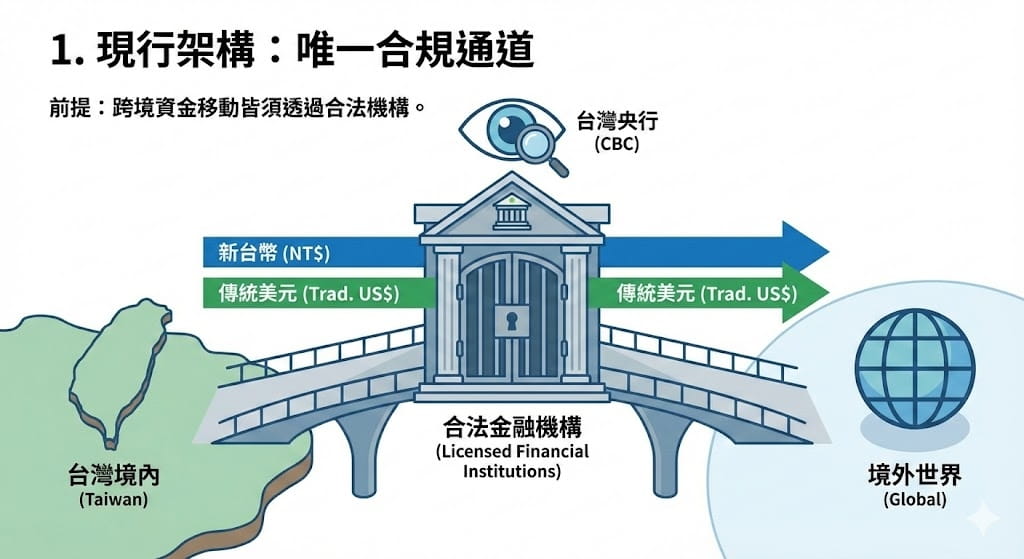

Why has the US Dollar stablecoin become a shadow foreign exchange market? The central bank first explains from Taiwan's current foreign exchange management framework, as the existing regulations are based on the premise that all cross-border capital movements must go through legitimate financial institutions.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

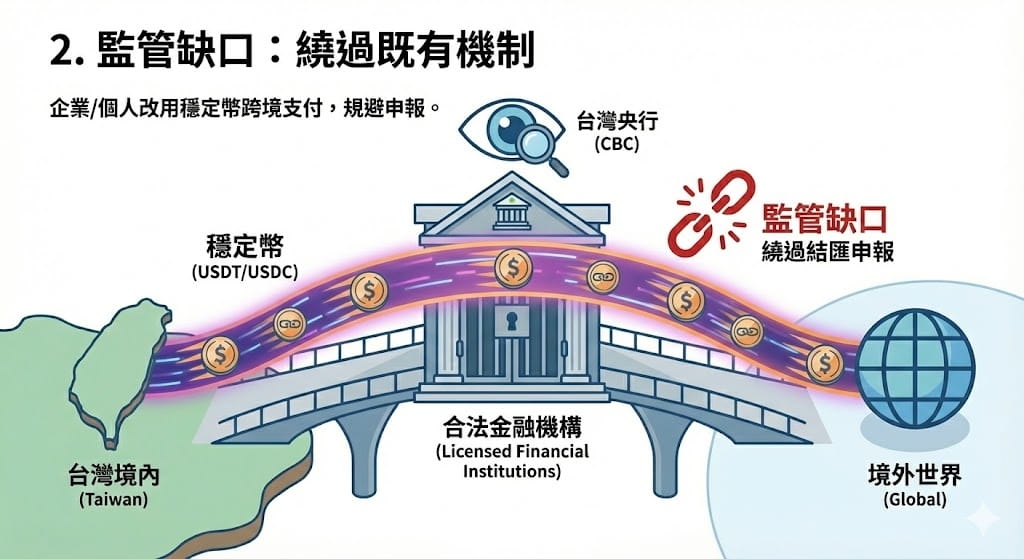

However, if in the future companies or individuals extensively use stablecoins for cross-border payments and transactions to bypass existing foreign exchange declaration mechanisms, it will lead to severe regulatory gaps in the current foreign exchange management system.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

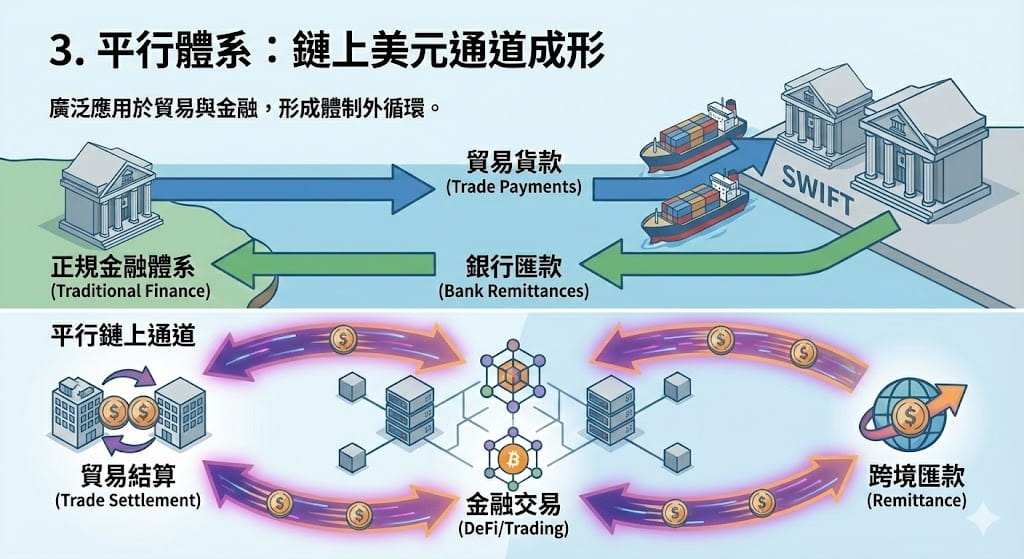

When companies widely apply US dollar stablecoins for trade payment settlements, financial transactions, or cross-border remittances, it may create a parallel channel for the inflow and outflow of dollars on-chain outside of the formal financial system.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

To avoid shadow foreign exchange, the central bank will timely adjust definitions.

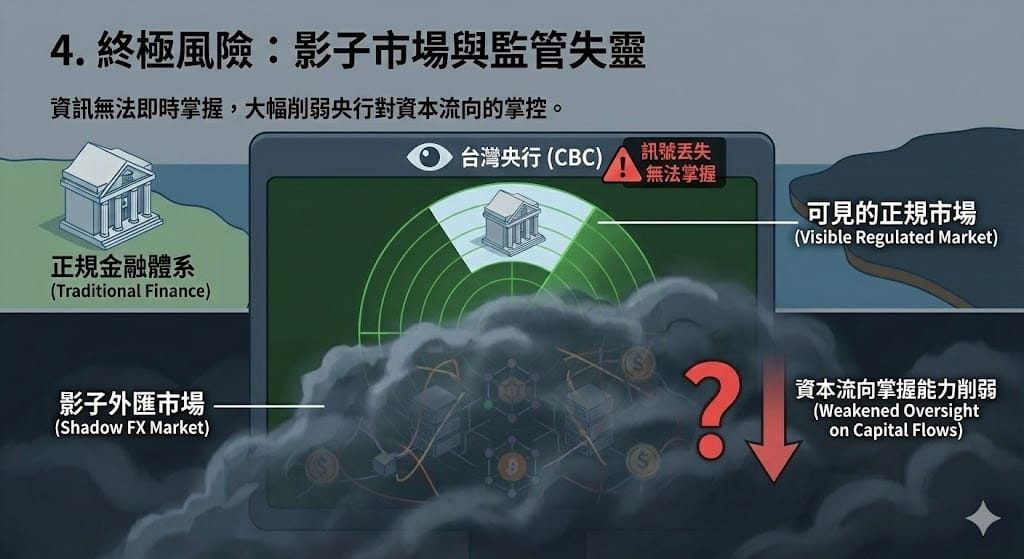

If the regulatory authorities cannot promptly grasp these on-chain information, some cross-border transactions will completely escape regulation, evolving into what is known as the 'shadow foreign exchange market', which will significantly weaken the central bank's ability to control capital flows.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

According to the central bank's explanation, images generated using Nano Banana Pro are for reference only.

In response, the central bank stated that it will closely monitor the development of the stablecoin ecosystem and reassess the definitions of monetary-related aggregates. In the future, as needed, it will follow the latest guidelines from the International Monetary Fund (IMF) and timely revise relevant monetary statistics and definitions.

Further Reading:

The International Monetary Fund warns: Stablecoins may accelerate currency substitution, weakening central bank capital controls.

The central bank has likened wildcat banking, stating that the advantages of TWD stablecoins are limited.

Regarding the nature and risks of stablecoins, Central Bank President Yang Jinlong recently quoted scholars in a speech, likening it to a modern version of 'wildcat banking', implying its private issuance, regulatory arbitrage, and potential instability.

Regarding whether a TWD stablecoin should be promoted, the central bank analyzed in the reference materials after the board meeting that the planned TWD stablecoin is similar to electronic payment tokenization and belongs to the 'Pay Before' model, where consumers must preload funds before spending.

The central bank further pointed out that there is no significant advantage compared to the current real-time debit of financial cards (Pay Now) or the deferred payment of credit cards (Pay After).

Considering that Taiwan's existing payment system is already quite complete, convenient, and low-cost, the actual demand for TWD stablecoins from the consumer end remains to be discussed.

The central bank believes that the current impact of TWD stablecoins on monetary credit creation and policy transmission mechanisms is not significant; the degree of future impact will depend on the number of practical application scenarios and the design of the regulatory framework.

Scholars call for setting up firewalls to prevent systemic crises.

In the face of the increasing connection between traditional finance and virtual assets, academia has also proposed specific risk management recommendations.

According to reports from (Commercial Times), former Central Bank Vice President and current National Taiwan University Economics Professor Chen Nanguang suggested that regulatory authorities should establish a clear 'firewall' between stablecoin issuers and traditional deposit institutions, such as appropriately limiting banks' exposure ratios to stablecoin businesses to prevent risk transmission.

In addition, to prevent liquidity crises that may arise from large-scale redemptions, temporary redemption restrictions or the design of liquidity cost mechanisms may be implemented in the future to strengthen market resilience and reduce potential risks.

International news related to stablecoins:

(GENIUS Act) First wave of rules released, FDIC paves the way for banks to issue stablecoins.

Is a 1:1 peg to the US dollar stable? Moody's proposes a brand-new rating framework to assess the quality of stablecoin reserves.

The article "Central Bank: US Dollar Stablecoins May Become Shadow Foreign Exchange Markets! They Could Evade Currency Exchange Regulations, Impacting TWD Exchange Rate" was first published in "Crypto City".