Good afternoon, friends. I am Azu. Let me put it bluntly: the most dangerous thing in BTCFi is not the decline in returns, but the ambiguity of the 'return logic'—you don't know what exactly is making money, and who the risk is being placed on. Lorenzo put Babylon at the bottom layer because it re-establishes the 'BTC earning' process back onto a verifiable track: the staking and unbonding periods of BTC, as well as the core penalty boundaries, can all be clearly defined by rules. For example, with the official parameters of Babylon Phase 2, the unbonding time for BTC staking is 1008 Bitcoin blocks (about a week), the maximum penalty limit is 0.1%, and the penalized BTC will be dealt with by burning, to prevent the question of 'who receives the penalized funds' from becoming a new trust black hole.

But now let's do the "extreme situation simulation" you asked for: If Babylon does not expand as quickly as the market expects, or if the narrative around BSN/multi-staking slows down, what would be the most direct result? In one sentence - the yield will revert to a state that is "more like macro parameters, rather than project marketing." For example, in Babylon's mechanism, one source of rewards for BTC stakers is the inflation distribution of BABY (common terminology in documentation and ecological interpretation states that part of the annual inflation will be used as BTC staking reward). Once ecological expansion slows down, the demand for new network security decreases, and competition for rewards diminishes, the yield curve may switch from a "growth narrative" back to "stock allocation." At this time, the most common market reaction is not "everyone leaves," but rather the secondary market will price in expectations earlier: the premium of stBTC disappears, discounts appear, and asset fluctuations like YAT increase, with sentiment leading and data following.

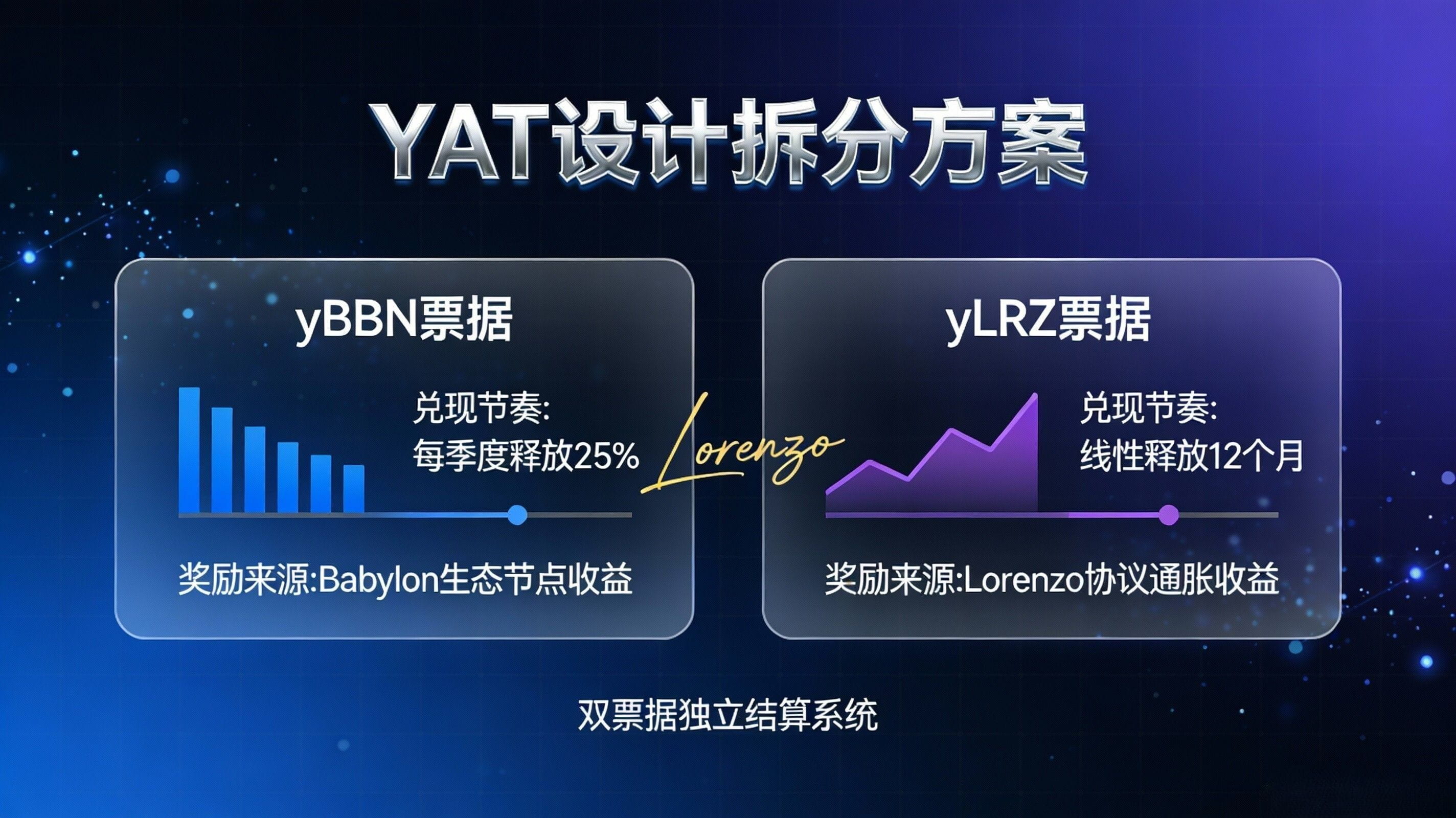

What truly tests Lorenzo is not whether the yield is high or low, but whether he can turn this "weakening yield" into manageable, modular, and switchable risks, rather than having one bomb blow everyone up on the same line. One critical thing I observed that Lorenzo did: when the rules of Babylon's first phase were complex and required adjustments in technology and distribution during the process, Lorenzo directly拆开了原本“一张 YAT 代表一切”的设计,改成了yBBN(对应 Babylon 奖励份额)与yLRZ(对应协议侧激励/权益)两张票据,并明确告知哪些奖励可先领取、哪些需要等待更长周期。这件事很重要,因为它等于告诉市场:底层如果变了,我不会靠一句“相信我”糊过去,我会把收益来源拆开、把兑现节奏拆开、把等待成本显性化——你可以选择承担哪一段不确定性,而不是被打包带走。

So where might Lorenzo’s Plan B be when "Babylon’s expansion falls short of expectations"? I prefer to look from the architecture rather than slogans. Lorenzo defines the Financial Abstraction Layer (FAL) in his own documentation as an infrastructure that "abstracts complex strategies into modular components"; it can support products like OTF (On-chain Traded Fund) and standardizes the routing of funds, NAV calculation, settlement, and yield distribution. This means that even if the ideal "BTC native staking grid" expands slowly, the protocol does not necessarily have to stick to one source of yield: it can function more like an asset management layer, transforming "yields" from a single narrative into a multi-strategy, long-term, multi-risk portfolio expression. Of course, this does not guarantee any yield; rather, it states: from the perspective of product engineering, the FAL/OTF structure is designed to allow for switchable engines at the top when the underlying yields do not go smoothly, rather than just increasing leverage to force through.

The changes in rules are actually very clear here: When you place the yield of BTC in a native staking system like Babylon, you are not accepting "eternal growth," but rather a "parameterized exit mechanism" - for example, a 1008 block exit wait and a 0.1% upper limit penalty boundary. The impact on users is also direct: your yield expectations need to switch from "story-driven" to "mechanism-driven," more like making a constrained configuration rather than chasing an eternal machine race; at the same time, you need to start treating "liquidity discounts/premiums, cashing rhythm, and reward source splitting" as core observation indicators, rather than just focusing on APR.

Finally, here’s an Azur-style action guide; I would write it in three sentences and stick it to my memo: First, I will treat the liquidity cost of "waiting a week for the worst exit" as a premise, planning this BTC as funds that cannot be used for emergency purposes at any time, rather than fantasizing about a one-click escape while staking. Second, I will look at the yields separately: which part comes from Babylon's rule distribution, and which part comes from protocol-side incentives, prioritizing the portion that offers "clear explanatory, verifiable, and cashable paths" when encountering rule adjustments, rather than placing all uncertainties on the same ticket. Third, if I find that the underlying expansion is not smooth and yields enter a stock phase, my first reaction will not be to leverage up to recover yields, but rather I would prefer to split my positions into "underlying exit-capable stBTC/staking position + upper layer replaceable strategy position," ensuring I always have choices - because in BTCFi, those who survive are never the ones chasing yields the hardest, but the ones who clearly outline the exit paths first.