Micron's earnings report can't just be called 'better than expected' anymore.

It's more like it's signaling something to the market:

The valuation logic in the memory sector is being rewritten by AI.

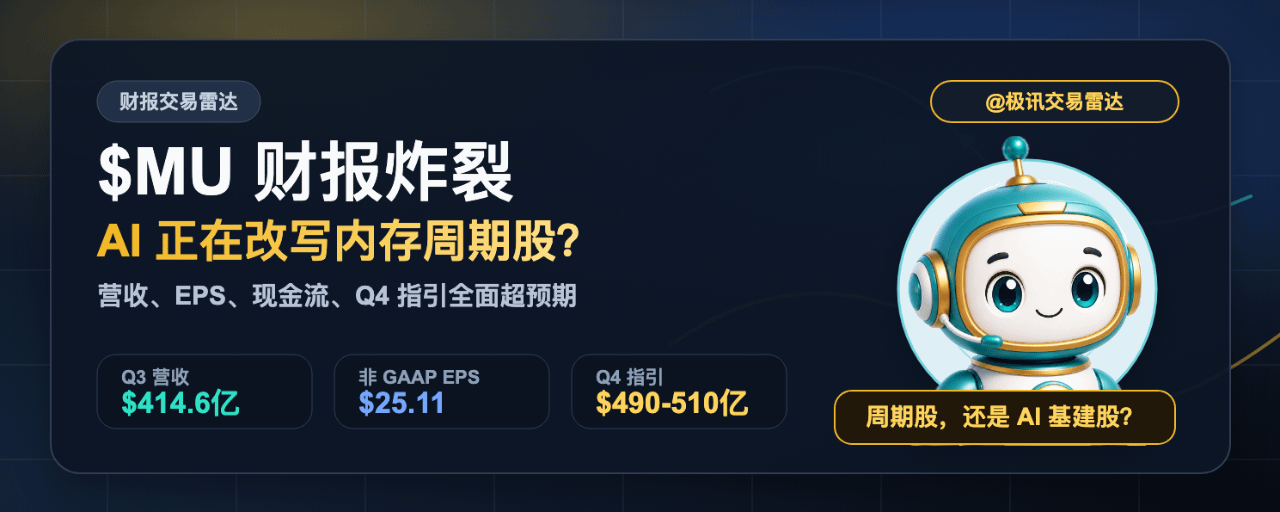

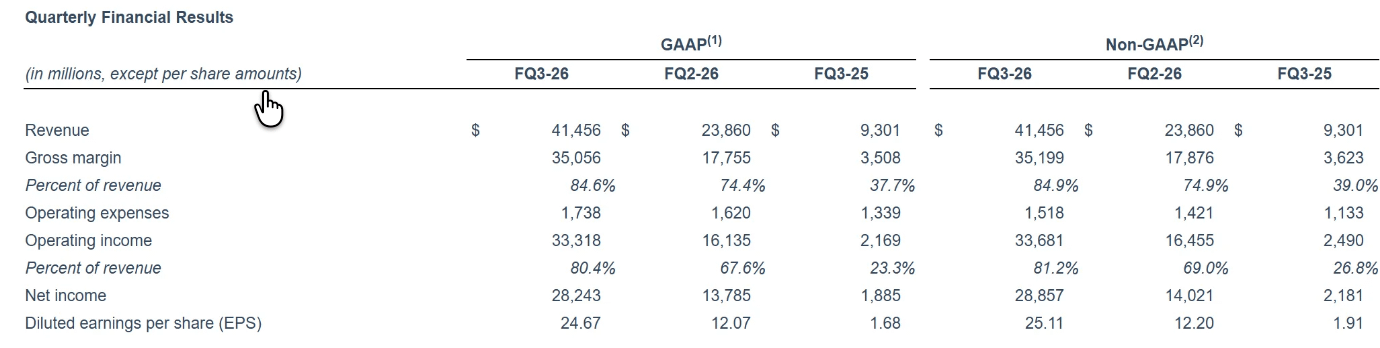

In Q3, Micron's revenue hit $41.46 billion, compared to just $9.3 billion last year.

GAAP net profit was $28.24 billion, with diluted EPS at $24.67;

Non-GAAP net profit was $28.86 billion, with diluted EPS at $25.11.

What's really off the charts is the cash flow.

Operating cash flow stood at $25.39 billion, up from $11.9 billion last quarter, and only $4.61 billion a year ago.

After deducting $7.1 billion in capital expenditures, the adjusted free cash flow is still a solid $18.3 billion.

At the end of the quarter, Micron’s cash, marketable securities, and restricted cash totaled $30.2 billion.

This is no longer the normal rebound of a traditional cyclical stock during an upcycle; it’s a concentrated pull from AI demand across the memory supply chain.

Micron CEO Sanjay Mehrotra put it very plainly:

Memory technology has strategic value in the AI era. The company is investing record amounts in technology, products, and its supply chain to meet customers’ rapidly growing needs. Long-term strategic customer agreements will also improve the durability and predictability of performance.

This sentence is crucial.

Because the market’s biggest concern about Micron in the past was that the cycle is too strong:

profits explode in good times, but in bad times, inventory and prices crush profits together.

But if HBM, AI server memory, high-performance SSDs, and long-term customer agreements can make demand more stable, then Micron is not just a cyclical stock—it looks more like a key supplier to AI infrastructure.

The product side is also validating this.

HBM4 has already shipped in large volumes to major customer platforms, and certified samples have been delivered to multiple end customers.

HBM4E is progressing smoothly and is expected to reach mass production in 2027.

At the same time, products such as 256GB DDR5 RDIMM, LP5X SOCAMM2, PCIe Gen6 high-performance SSDs, 245TB QLC SSDs, automotive-grade NAND, and more are also moving forward.

In other words, Micron is not relying on only one HBM narrative; it benefits simultaneously from AI servers, data center storage, end-user devices, and automotive scenarios.

Most importantly, the Q4 guidance.

The company expects adjusted revenue of $49.0–$51.0 billion in the fourth fiscal quarter, adjusted gross margin of about **86%**, and adjusted EPS of $30–$32.

The third fiscal quarter was already record-breaking, and the fourth fiscal quarter is set to be even stronger.

So the real question behind this earnings report isn’t whether Micron’s results are good or not.

The answer is already clear.

The real question is:

Does the market still need to value Micron as a traditional cyclical stock?

If AI demand and HBM supply-demand tightness are only a short-term mismatch, Micron may be near the cyclical peak right now.

However, if multi-year customer agreements, AI data center expansions, and bottlenecks in high-end memory supply can remain in place, Micron’s valuation framework may be repriced.

Previously, Micron was a memory-cycle stock.

Now, Micron is increasingly like a memory infrastructure company in the AI era.

Do you think this cycle for Micron is at the peak, or is the valuation re-rating just beginning?