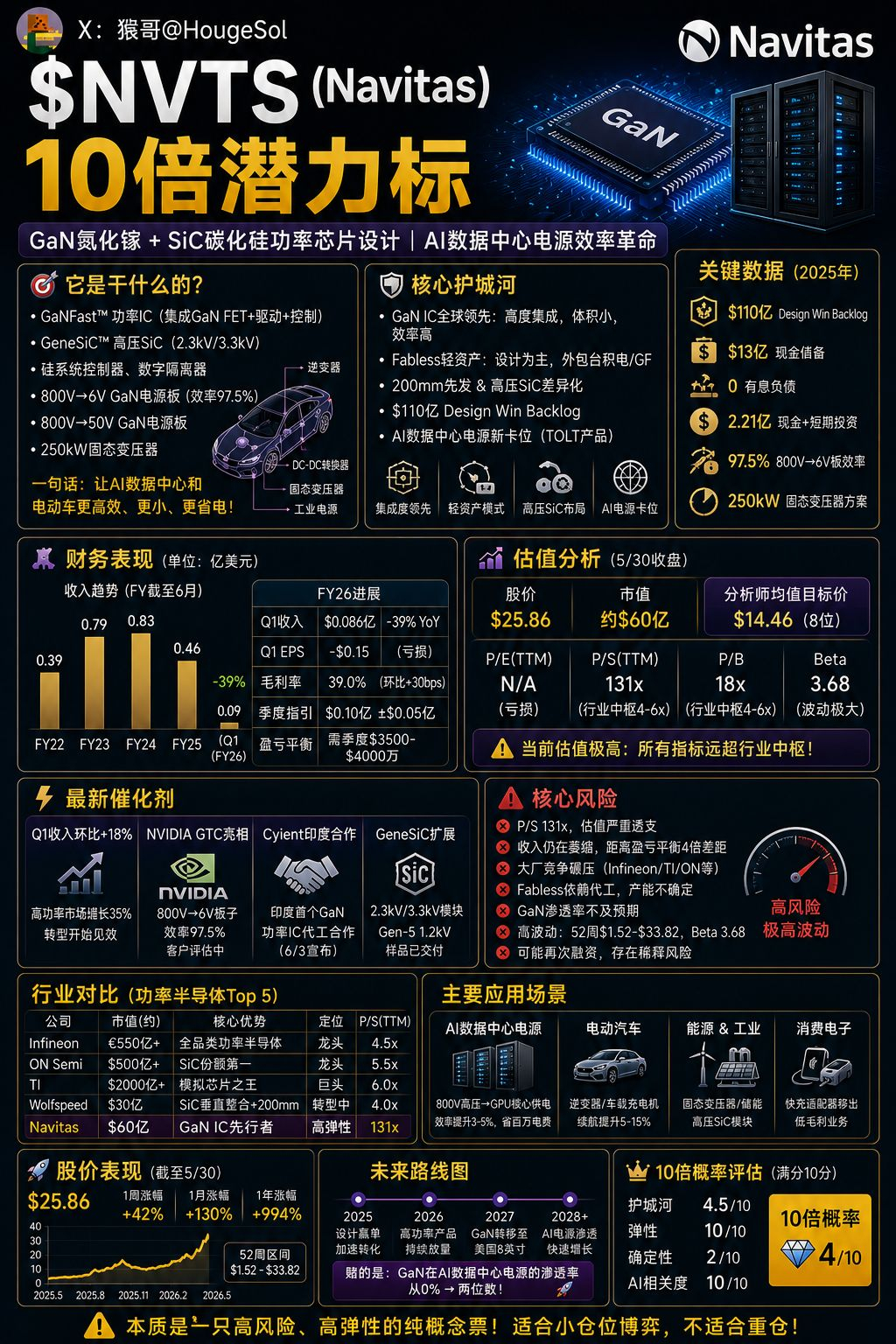

This company NVTS, let's drop a jaw-dropping figure: annual revenue of $45.9 million, market cap of $6 billion, P/S ratio of 131x. In the power semiconductor sector, the norm is 4 to 6x, and this one is over 25x that. This might be the most absurdly valued power chip company I've analyzed.

But why did it pump 10x in a year? Because it hit the right direction: AI data centers are freaking energy hogs.

NVIDIA's GB200 rack consumes 120kW; this juice has to be converted from high-voltage AC from the grid to low-voltage DC for the GPUs. If they lose just 1% efficiency in the conversion, the whole data center burns through millions more in electricity costs.

NVTS’s GaN chips can push conversion efficiency to 97.5%, outperforming traditional silicon solutions by 3 to 5 percentage points. In a data center worth billions, those few percentage points translate to real dollars.

What sets it apart from Wolfspeed?

The approach is completely different; Wolfspeed is heavily asset-based and vertically integrated, handling everything from substrates to components in-house, with factories costing billions. They just crawled out of bankruptcy.

NVTS is fabless and light on assets, only designing chips while outsourcing manufacturing to TSMC and GlobalFoundries. They don't build factories or maintain production lines, like an architect who only draws blueprints without constructing the buildings.

Their core product is called GaNFast, the world’s first chip that integrates GaN power FETs and driver control protection circuits all in one.

Most competitors are still using discrete solutions. The benefits of integration are smaller, faster, more efficient, and fewer external components, like the 800V to 6V power board showcased at NVIDIA's GTC, delivering 20kW with 97.5% efficiency, samples have already been sent out to most power supply vendors for evaluation.

The SiC direction is also being worked on, with GeneSiC's high-voltage silicon carbide modules hitting 2.3kV and 3.3kV. This voltage range is an area that Wolfspeed and ON Semi haven’t really tapped into, applied in solid-state transformers and grid infrastructure.

But the problem is, the revenue is just too low.

First-quarter revenue was $8.6 million, down 39% year-over-year, with a GAAP net loss of $33.8 million. The loss is four times the revenue – earning $8.6 million in a quarter but losing $33.8 million; it's like running a bubble tea shop raking in $10,000 a month, but rent, utilities, and labor add up to $40,000.

Why is revenue declining?

They're actively cutting their low-margin mobile fast-charging business and pivoting to AI data center power, but they've chopped the old business and the new one hasn’t ramped up yet.

Management says breakeven requires quarterly revenue to hit $35 million to $40 million. Right now, it's at $8.6 million, falling short by four times. Even at the current quarterly growth rate of 16%, it would take nearly two years to reach breakeven.

The good news is they have a light balance sheet, with $221 million in cash and zero debt. Assuming they burn $15 million a quarter, they can last for three and a half years. The fabless model means they won’t go bust, but they’re not making money either, stuck in a 'won't starve but can’t get full' situation.

How does it compare to peers in terms of scale?

Infineon invests over $5 billion annually in R&D, TI over $4 billion, while NVTS spends $30 million, a difference of more than a hundred times. It’s like trying to claim territory with a water gun against a bunch of guys with rocket launchers; technically you might be more agile, but they have the resources to crush you.

What do analysts think?

Eight analysts have a consensus price target of $14.46, while it’s currently at $25.86, nearly double. All analysts’ targets are below the current price, which is a very dangerous signal.

It’s shot up 42% in the past week, 130% in a month, and 994% over the year, driven purely by narrative and momentum, completely disconnected from fundamentals.

Let me throw out some risks to keep you grounded.

A P/S of 131 isn’t just 'high'; it’s completely out of touch with reality. Any negative news could trigger a 30% to 50% crash.

Revenue is still shrinking, dropping from $83.3 million to $45.9 million and continuing downward, still four times away from breakeven.

If Infineon and TI decide to go all-in on GaN, NVTS might get sidelined quickly.

Being fabless means relying on foundry partners for capacity and yield, which aren’t in their hands. They've diluted shares multiple times in the past, and it's likely to happen again in the future. Beta of 3.68 is among the highest I've analyzed.

Moat score: 4.5, elasticity: 10, certainty: 2, 10x probability: 4.

Power semiconductor rankings: Infineon > ON Semi > TI > Wolfspeed > NVTS; coming in last due to too little revenue, too high a valuation, and too strong competition.

It's essentially a gamble on two things:

Can GaN replace silicon-based solutions in AI data center power, and can NVTS survive and thrive under the pressure from giants?

If both bets pay off, $6 billion could turn into over $50 billion; if either one goes wrong, it could drop back to below $3 billion.

A P/S of 131 means you’re paying today’s price for revenue expected in 2030. Just a heads-up, the current price is $30, which carries significant risk, suitable only for tiny positions and pure speculation, not for anyone heavy on the bag or unable to stomach a 30% drop in a single day!