Once upon a time, stablecoins were merely used as 'casino chips' for hedging and trading within the cryptocurrency circle. Now, it has transformed into a behemoth with a market value exceeding $300 billion, shaking the foundations of global financial infrastructure. From payment giants like PayPal and Stripe to Wall Street financial behemoths like JPMorgan and Charles Schwab, even traditional card organizations like Visa are all diving into this space.

This raises two core questions: how much investment is actually needed to issue a seemingly simple stablecoin? And why is the traditional banking industry willing to take on the dual challenges of regulation and technology, scrambling to enter a field seemingly already monopolized by Tether (USDT) and Circle (USDC)? This article will delve into the true costs behind stablecoin issuance and reveal the deeper strategic motivations of the banking industry in this area.

A tough battle between capital and compliance

Many mistakenly believe that issuing stablecoins is as simple as deploying a smart contract. However, to legally and compliantly launch a globally-oriented stablecoin, the costs and complexities involved are comparable to establishing a medium-sized bank.

1. Traditional path: The million-dollar entry ticket

For issuers wanting to take matters into their own hands, costs mainly lie in three foundational engineering areas:

Compliance and legal systems: This is the most expensive 'entry fee.' Issuers need to navigate regulations across multiple jurisdictions and obtain key licenses, including the MSB (Money Services Business) in the U.S., Bit License in New York, MiCA in the EU, and VASP in Singapore. Behind each license are detailed financial disclosures, strict anti-money laundering (AML) mechanisms, and ongoing monitoring report obligations. Market analysis indicates that just applying for the VASP license in Hong Kong could incur costs totaling tens of millions of Hong Kong dollars. Overall, a stablecoin issuer with global operational qualifications can easily reach annual compliance and legal expenditures in the millions of dollars.

Reserve management and liquidity: The cornerstone of stablecoin credibility lies in its reserves. Issuers need to invest user-deposited funds in high-quality liquid assets (such as U.S. Treasury bonds). When reserves reach billions or even tens of billions of dollars, operational costs can soar. Just the custodial fees alone could reach millions of dollars a year. Additionally, to ensure that users can 'redeem and exchange instantly,' issuers must maintain sufficient liquidity positions to cope with large redemptions during extreme market conditions, which is very close to the risk preparation mechanisms of traditional money market funds.

Technical systems and security maintenance: This is not just about deploying an ERC-20 contract. Issuers must establish a highly stable and auditable technical system, covering smart contract deployment, multi-chain minting and burning, cross-chain bridge configuration, wallet whitelisting, on-chain transaction monitoring, security risk control, and API integration, among others. This system, which serves as the 'public settlement layer,' has technical and maintenance costs that typically remain in the millions of dollars a year.

2. Emerging models: 'Stablecoin as a service' lowers the barriers to entry

Just when people thought stablecoins were exclusive to the giants, new models are emerging. Take payment giant Stripe's acquisition of Bridge and M0 as an example; their goal is not to issue their own stablecoins but to become 'arms dealers for stablecoins.'

Stripe has packaged the complex financial processes of stablecoin issuance (such as licensing, reserve management, compliance) into an API, allowing businesses to issue their own branded stablecoins within weeks, just as they would integrate online card payment functionalities. The mUSD launched by the world's largest crypto wallet Meta Mask is the first representative case under this model. This means that issuing stablecoins is moving from a highly specialized financial issue to an engineering problem. It also suggests that the market will soon welcome an era of flourishing stablecoins.

An inevitable choice for banks

Given the high issuance costs and the presence of the two giants, USDT and USDC, why do banks and other financial institutions continue to rush to enter the market? The answer is far more complex than simply 'interest rate arbitrage.'

1. Direct incentives: The undeniable 'risk-free' profits

The business model of stablecoin issuers is extremely tempting. They use the dollars deposited by users (without paying interest) to purchase U.S. Treasury bonds, earning a stable 4% to 5% interest rate spread in the current high-interest environment. Tether's quarterly financial report shows profits reaching tens of billions of dollars, proving the incredible profitability of this model. For banks holding large amounts of customer deposits, this is a massive income source with almost no credit risk.

More importantly, a new 'yield generation era' has arrived. Emerging stablecoins like Ethena's USDe are starting to distribute the earnings of underlying assets to token holders, directly challenging the traditional model of banks 'attracting cheap deposits and earning high spreads.' When users can earn over 4% annualized yield by holding stablecoins, the meager 0.07% interest on bank accounts seems extremely ironic. This competitive pressure forces banks to confront stablecoins; otherwise, they risk massive outflows of deposits.

2. Strategic layout: Deep considerations beyond profits

However, for institutions like Charles Schwab or JPMorgan, the strategic significance far outweighs short-term profits. Issuing proprietary stablecoins is a key layout concerning survival and leadership in the next decade.

Branding, narrative, and leadership: Amid the wave of financial technology, issuing stablecoins has become the most direct way for institutions to showcase their 'innovation capabilities' and 'keeping up with the times.' This is not just a payment tool; it is also a powerful brand declaration, announcing that they are the definers of the future of digital finance, not passive followers.

Control and ecological closed loop: What banks fear the most is customers converting their funds into USDC or USDT, thereby detaching from their financial system. Issuing proprietary branded stablecoins can firmly lock customer funds and transaction behaviors within their own ecosystem, preventing value leakage. This not only preserves interest income but also allows control over key user data and transaction flows.

Paving the way for future tokenization: The future of traditional finance is asset tokenization (RWA). Whether it is stocks, bonds, or real estate, the future may see these assets issued and traded on the blockchain. Stablecoins are the underlying settlement tools of this future trading market. Banks investing in stablecoins is akin to building toll booths before the highway is completed, preparing infrastructure for a much larger tokenization market in the future.

Opportunities arising from regulatory clarity: With the advancement of regulations such as the U.S. (GENIUS Act), the regulatory pathways for stablecoins are gradually becoming clearer. This provides traditional financial institutions with a compliant entry framework. Under clear rules, banks can leverage their deep compliance experience and brand reputation to issue products that are more trusted than existing crypto-native stablecoins, turning regulation from a barrier into a moat.

New financial order

The evolution of stablecoins seems like a history where a decentralized ideal has been co-opted by reality and ultimately integrated into mainstream finance. It has gradually transformed from a revolutionary tool aimed at bypassing traditional systems into a financial infrastructure dominated by regulators and traditional giants.

So we may be witnessing a turning point of an era:

The barriers to entry for issuance are polarizing: on one hand, the compliance-heavy asset-intensive model is costly; on the other hand, 'stablecoin as a service' is giving rise to a plethora of customized, functional stablecoins.

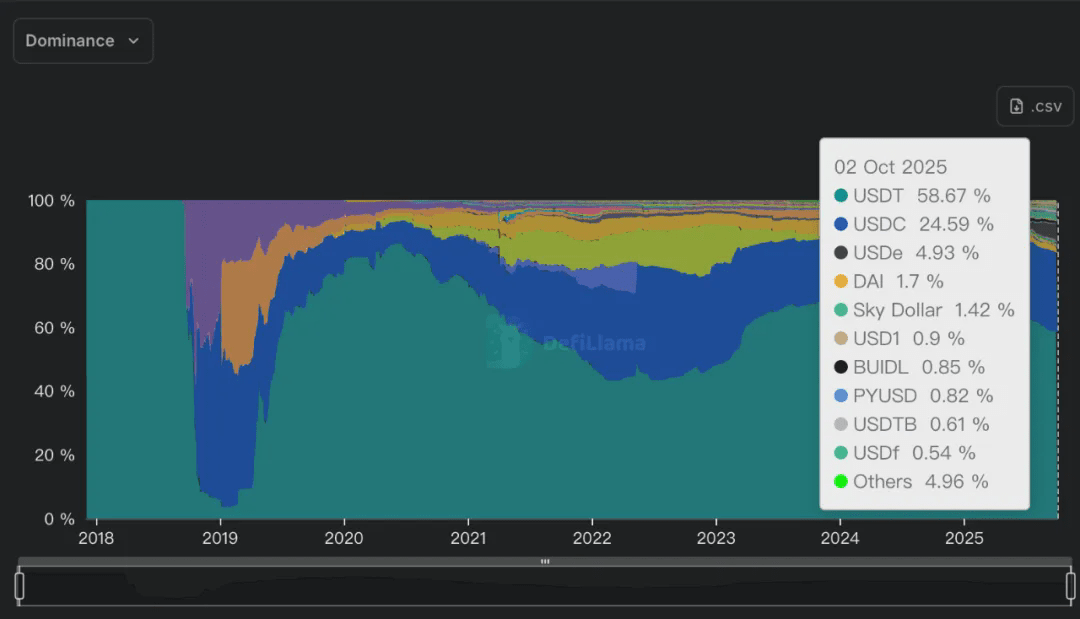

The market landscape is shifting from a duopoly to a multipolar model: The monopoly position of Tether and Circle is being eroded by various stablecoins issued by exchanges, wallets, fintech companies, and even banks. The maturity of cross-chain technology has made the cost of switching stablecoins nearly zero, and the network effects are weakening.

The ultimate form of stablecoins may be 'programmable currency': its true revolutionary aspect lies not in transfer speed or cost, but in its programmability. From real-time settlement of wages and automated B2B payments to insurance claims without human intervention, stablecoins are redefining the meaning of money. This is also why payment giants like Visa are actively exploring using stablecoins for cross-border settlements.

Returning to the initial question: Banks entering the stablecoin space are not only to take a share of the pie but also to avoid being eliminated in the next generation of financial revolution. What they are issuing is not just a token but their own place in the future financial order. The outcome of this competition will no longer be solely determined by the size of the balance sheet but rather by who can better embed trust, technology, and narrative into the underlying code of global finance. And this grand history has just begun.