A turning of the calendar has been used as a moment to set direction, and the contours of that direction have been drawn by BounceBit with unusual clarity. A year of convergence has been anticipated, in which the momentum of traditional markets and the cadence of decentralized finance are expected to meet more coherently than before. The language of this convergence has been framed as CeDeFi paired with Real-World Assets, and the perspective has been offered that 2025 will reward infrastructure that treats trust and efficiency as complements rather than trade-offs. In that frame, a roadmap has been shared and a philosophy has been revealed.

It has been suggested that 2024 should be remembered as a threshold year for CeDeFi. Mechanisms that once lived behind the glass walls of institutions were reimagined as on-chain products accessible to ordinary users. Basis arbitrage, long a professional’s instrument, was re-packaged through advances in fund segregation and exchange mirroring so that capital could be mobilized without surrendering custody. Confidence in this approach was reinforced by the maturation of connectivity between custodial venues and centralized exchanges, where frameworks such as MirrorX and ClearLoop were cited as proof that capital efficiency can be delivered alongside verifiable control. Against that backdrop, a pair of archetypes was held up: one that pushed stablecoin adoption through base-layer arbitrage and another that recast basis strategies as modular, token-denominated yields across multiple large-cap assets. In the telling, BounceBit was placed inside the second archetype, and the distinctiveness of that placement was used to explain growth that arrived without the crutches of emissions or points.

Evidence of that growth has been pointed to in the behavior of total value locked and in the fees actually paid to the protocol. A surge from a lower base to more than threefold during the final months of 2024 has been presented not as a promotional stunt but as an outcome generated by product-market fit. Monthly fee records that eclipsed prior periods have been described as confirmation that usage was not being purchased; it was being chosen. A further signal has been emphasized through institutional adoption, where a public company in Asia with deep Bitcoin reserves stepped forward with capital and a strategic alliance. In that act, a bridge between centralized, regulated balance sheets and agile on-chain engines was made more tangible. Partnerships across ecosystems were also invoked, not as ornaments but as on-ramps along which liquidity and credibility can move in both directions.

A cultural geography has been woven through this narrative. A base in Singapore has been described, through which access to Asian liquidity venues has been cultivated, while simultaneous outreach to Western institutions has been pursued. A month spent in New York has been mentioned not as a travel diary but as a signal that the conversation with issuers of tokenized assets and established financial houses has been elevated from abstract curiosity to practical evaluation. In this geography, the thesis has been articulated that the most resilient structures in the next cycle will be built where Eastern liquidity meets Western issuance, and where regulated disclosures can be reconciled with permissionless market access.

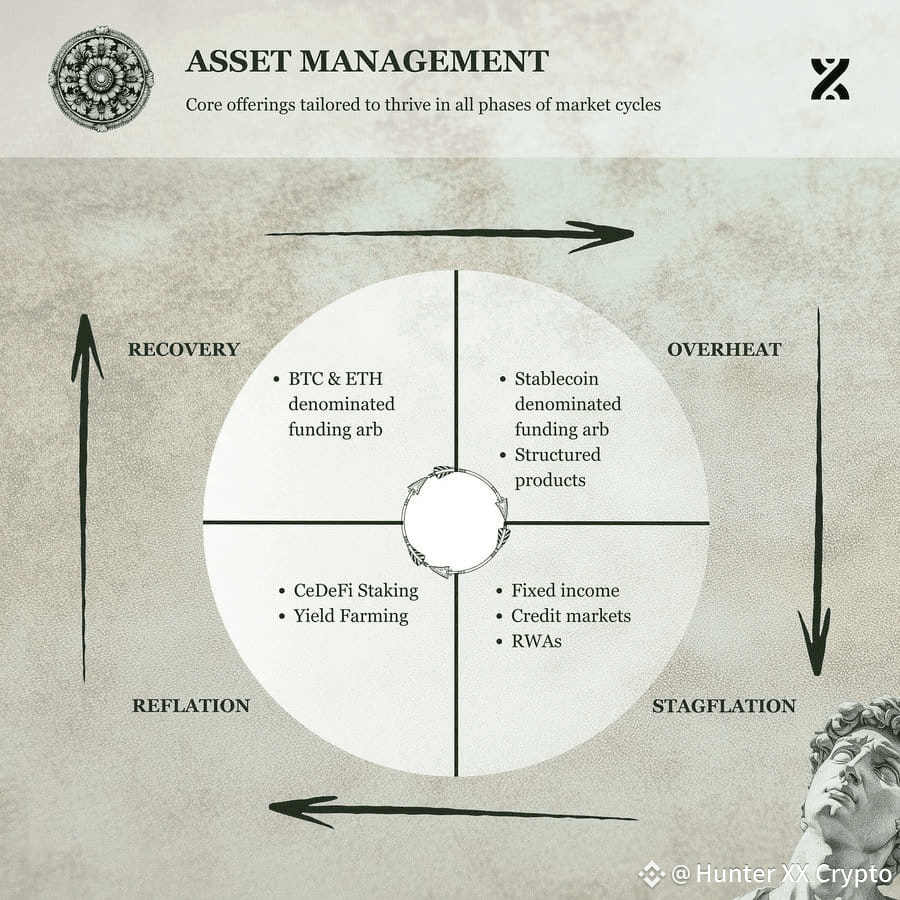

Into that set of convictions, an all-weather product posture has been placed. Rather than a single bet, a sequence of stances has been proposed, aligned with the rhythm of cycles. During the more exuberant portion of the last cycle, BTC-denominated real yields were emphasized so that directional conviction could be expressed with structured prudence. As the cycle matures, a rotation toward dollar-denominated yield has been forecast, with the late-stage appetite for stability acknowledged and the need for professionally managed profit-taking respected. Through this chord progression, a promise has been made that the same engine can be tuned for different tempos, and that composable instruments will be provided so portfolios can be re-weighted without leaving the rails that gave them their initial advantage.

Within 2025, that posture has been organized into a sequence of releases. An institutional flagship has been slated to open the year, with CeDeFi methods married to RWA rails and bundled under a single product concept. It has been called BounceBit Prime, and its purpose has been cast as transformation of tokenized treasuries and money-market units into settlement assets that actually do work. Later, an expansion of credit markets backed by RWAs has been planned on the BounceBit chain so that dollar-like instruments and tokenized credit can be used as collateral with fewer frictions. After that, a clearing and settlement layer for RWAs has been proposed so that fungibility among similar underlying assets can be widened and so that minting, burning, and swapping can be conducted without a labyrinth of wrappers. Finally, a turn toward regulatory-aligned yield has been forecast, with additional institutional partnerships expected to be layered as guardrails are finalized. Although dates have been grouped by quarter, the emphasis has remained on sequence rather than spectacle; the claim has been that each layer equips the next.

The macro lens has not been neglected. It has been observed that in Western markets, the most sophisticated asset bases are being tokenized first: Treasury bills, money-market exposures, private credit. The critique has been voiced that yield alone is not utility, and that tokenized wrappers must be given functions beyond passive carry if adoption is to deepen. In Asia, it has been noted that the muscle memory of onboarding large cohorts of users has persisted, with liquidity venues evolving UI, UX, and access funnels at a relentless pace. The result has been depicted as an asymmetry that can be harnessed: Western tokenized instruments have been seen as raw materials, while Asian market infrastructure has been seen as production capacity. If the two are brought into phase through verifiable settlement and credit primitives, it has been suggested that meaningful growth can be unlocked without the brittleness that accompanied prior cycles.

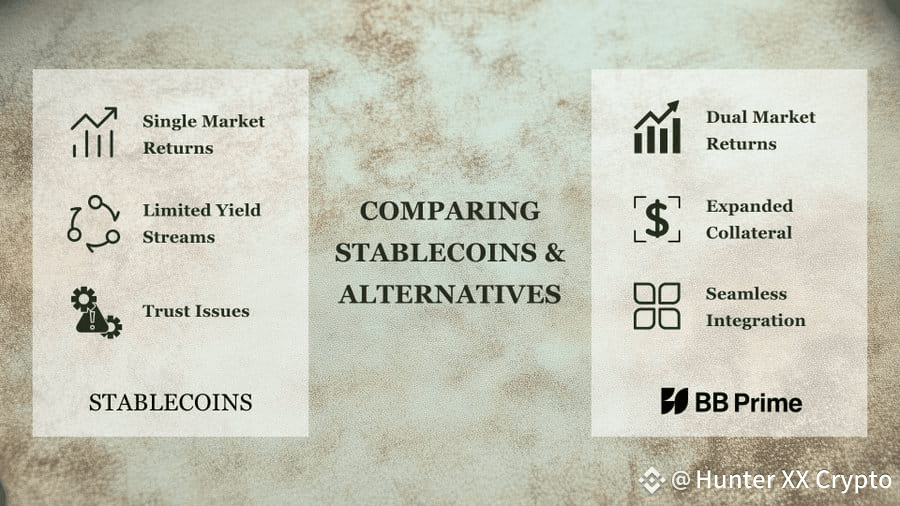

A closer focus on stablecoins has been offered to illustrate micro-level frictions. Trust questions around reserves and issuers have been acknowledged; distribution bottlenecks via centralized exchanges have been highlighted; and the habit of extracting underlying yield for the issuer has been identified as a structural tax on holders. Rather than rejecting stablecoins outright, an alternative path has been put forward in which tokenized Treasuries and fund units can be threaded into CeDeFi and exchange venues directly. In that configuration, settlement and collateral functions can be carried by instruments that already clear within the core of traditional finance, while the basis yields of crypto markets can be harvested without relying on stablecoin wrappers as intermediaries. A parity of yield has been promised in that arrangement, where the risk-free rate can be combined with basis returns rather than being traded off. The concept has not been presented as a demolition of stablecoins but as a pragmatic circumvention of their specific limitations when institutional comfort is being courted.

Within this architectural sketch, restaking of RWAs has been positioned as a cornerstone. By permitting regulated money-market exposures to be used for network security on the BounceBit chain, a dual-yield effect has been claimed: steady Treasury-linked returns on the one hand and CeDeFi basis yields on the other. In that move, a broader point has been advanced, namely that idle, safe capital can be given a second job without violating the risk boundaries imposed by institutions. Alongside restaking, a clearinghouse model for RWAs has been introduced in concept, intended to make near-substitutable assets more fungible and to reduce the fragmentation caused by wrapper proliferation. Through such a clearinghouse, smoother switching among Treasury-backed instruments has been envisioned, with fewer manual steps and less liquidity trapped in the margins.

Attention has also been directed to an ecosystem layer. New protocols have been encouraged to use the CeDeFi stack and the emerging RWA credit markets as building blocks. An example has been cited in a mobile-first trading venue slated for an early 2025 debut, where alignment with BounceBit’s staking community has been embedded in token economics. The expectation has been expressed that more such applications will arrive, each using the underlying pipes to hide complexity while exposing simpler user flows. In parallel, an initiative called CeDeFi Liquidity Mining has been described as entering its late implementation stages. In that design, trading that occurs on centralized exchanges would be rewarded through on-chain incentives, allowing exchange flow to be brought into the same incentive fabric that has traditionally been confined to decentralized venues. Negotiations with major exchanges have been alluded to, and a launch during 2025 has been forecast as likely.

Across all of this, tone has mattered. An argument has been made that sustainable adoption is less about fireworks and more about habits that can survive the unglamorous hours of a market. For that reason, the absence of emissions and points during the late-2024 growth spurt has been underscored, and the accumulation of protocol revenue has been used as a counterweight to hype cycles. Institutional courtiers have been named, not to claim virtue by association, but to indicate that counterparty diligence on both sides has been completed to a degree that supports ongoing work. Likewise, the geographic straddle has been framed less as a branding exercise than as a logistical advantage in bringing regulated assets to where liquidity is most elastic.

As the year turns, a community has been addressed with a promise that the bridge being assembled will carry two-way traffic. Builders have been invited to treat the CeDeFi stack as a service layer that can be reused without being rebuilt. Institutions that are testing RWA programs have been encouraged to consider settlement flows that do not strand their units in static wrappers. Users who survived prior cycles have been reassured that differing appetites can be served at different moments, with BTC-centric yield when risk is welcomed and dollar-centric carry when risk is being trimmed. Confidence has not been asked for as charity; it has been requested as a response to operational proofs that have already been logged.

Through all of this, the language of synchronicity has been chosen deliberately. A calendar in the West has been seen closing its first month as an astrological marker in the East arrives, and into that coincidence a plan has been placed. It has been argued that the next era of market structure will be written where custody and capital efficiency are reconciled, where tokens represent registries that legacy finance already understands, and where interfaces are simplified so the pipes do not become the product. In that era, the role for a platform like BounceBit has been defined not as a dispenser of speculative novelty but as a fabric through which capital can be re-deployed, redeemed, and restaked with fewer frictions and clearer receipts.

If that fabric is woven as promised, a different kind of composability will be felt. It will be felt when a Treasury unit can be moved into a CeDeFi basis trade without a detour through a stablecoin; when a restaked money-market position secures a chain while still paying its base yield; when a clearinghouse can translate across wrappers so that bid-ask spreads stop multiplying with each new product. It will be felt when a mobile-first venue can turn complicated paths into a single, legible tap; when centralized volumes can be acknowledged by on-chain incentive systems; when the distance between East and West is measured not in time zones but in messaging latency.

A community that has been asked to accompany this journey has not been promised immunity from volatility or perfection in execution. Instead, an architecture has been proposed that treats volatility as a given, that positions capital to benefit from rotation rather than be scattered by it, and that invites regulation into the loop without conceding the advantages of open settlement. If those commitments are kept, the year called 2025 will not be remembered as a month of announcements; it will be remembered as the period when the foundation for a new financial choreography was poured and when the step between old balance sheets and new rails became steady enough to be used without spectacle.