Take you into this silent revolution, analyzing the rise logic and industry impact of proprietary AMM.

In the Solana ecosystem, known for its high speed and low cost, we observe a brand new trend accelerating: a group of 'invisible' giants without official websites or promotions—Proprietary Automated Market Makers (referred to as 'Proprietary AMM') are rapidly emerging. They are reshaping the trading landscape in a more professional and efficient way, becoming a new engine driving on-chain capital flow. The Bitget Wallet Research Institute will take you into this silent revolution in this article, analyzing the rise logic and industry impact of proprietary AMM.

Invisible Giants: The Operating Logic of Proprietary AMM

Image Source: Helius

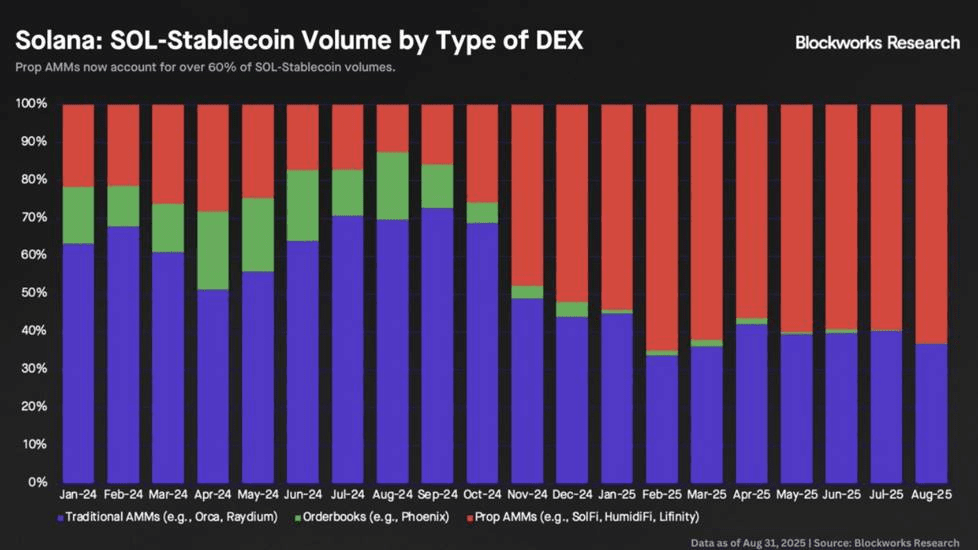

According to Blockworks' statistics, in August 2025 alone, proprietary AMMs processed approximately $47 billion in spot trading on Solana, accounting for 31% of the total trading volume on Solana's on-chain DEX. In high liquidity trading pairs like SOL-stablecoin, this trend is even more astonishing—since May 2025, proprietary AMMs have consistently captured over 60% of the market share in SOL-stablecoin trading pairs each month, and the proportion can even be higher in trading pairs between stablecoins.

Source: Blockworks Research

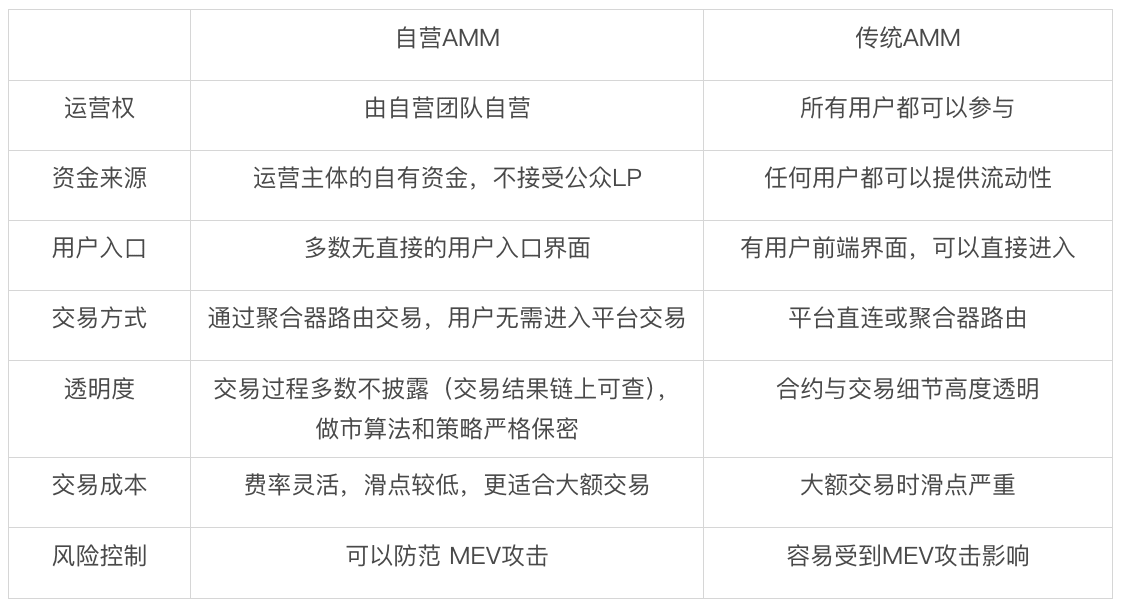

To understand this transformation, it is essential first to clarify the definition of proprietary AMM. Simply put, it is a type of on-chain market maker operated by a few professional teams using their own funds and does not open liquidity entry to ordinary users. This sharply contrasts with traditional AMMs like Uniswap, which allow anyone to become a liquidity provider (LP) and earn transaction fees, achieving 'crowdsourced' liquidity; while proprietary AMM returns the power of market making to professional teams, focusing entirely on extreme efficiency and risk control, with the following characteristics in specific operational models:

Invisible Entry: Most proprietary AMMs do not have user-facing website entries, and ordinary users cannot interact with them directly.

Algorithm Confidentiality: Market-making algorithms and parameters are kept strictly confidential, and transparency is significantly lower than that of traditional AMMs.

Reliance on Aggregators: The way to obtain trading orders is to directly access aggregators (such as Jupiter) to match user trading requests to the platform with the best quotes.

Comparison Table of Proprietary AMM and Traditional AMM Operating Models

Note: A few proprietary AMMs (such as Lifinity) open the user front end, but their liquidity is still primarily based on the team's own funds, and the realization of transactions is still completed through routing to aggregators.

This business model is based purely on execution efficiency rather than brand or community. Traditional DeFi projects need to invest heavily in marketing and community building to attract users and liquidity. In contrast, proprietary AMM converts all 'marketing budgets' into small price advantages for users during trading, ultimately capturing huge trading volumes. This also indirectly confirms that the DeFi market is maturing, with market participants increasingly resembling rational economic agents—following the principle of 'optimal price wins'—rather than merely idealists of 'decentralization first'.

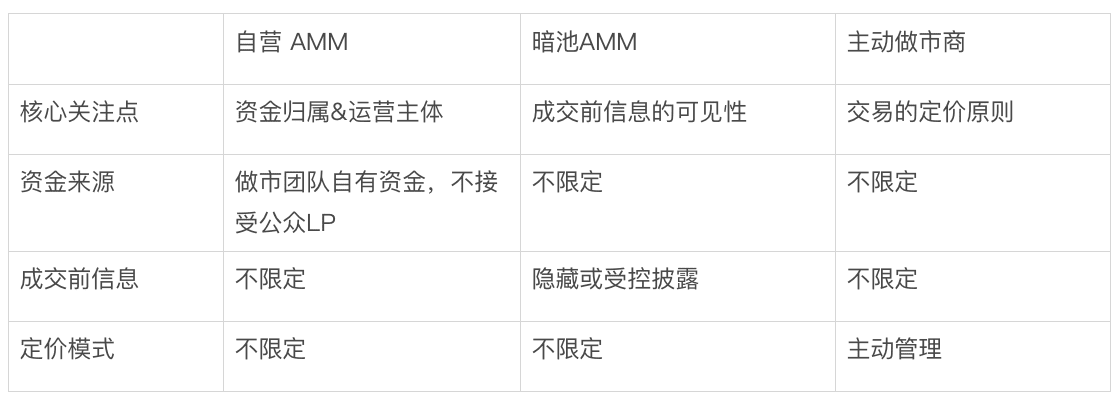

Concept Clarification: Is it a 'Dark Pool' or an 'Active Market Maker'?

With the rise of proprietary AMMs, some related terms like 'Dark Pool AMM' and 'Proactive Market Maker (PMM)' have also frequently appeared, making it crucial to clarify their differences. In fact, these three concepts are not mutually exclusive but differ in their emphasis on definitions.

Dark Pool AMM: The core lies in information concealment. It describes a trading method that hides order intentions during the matching phase, aiming to reduce information leakage and price impact.

Active Market Maker: The core lies in active pricing. It refers to dynamically adjusting quotes through introducing oracles, actively managing inventory, etc., to pursue higher capital efficiency.

Proprietary AMM: The core lies in the ownership of funds and operating entities. It defines a model where the operating team uses its own funds for market making.

Definition Sorting Table for Three AMM Concepts

After clarifying the definitions, it is not difficult to find that these three concepts are not mutually exclusive but describe different dimensions of the same financial entity. In fact, a typical proprietary AMM, in pursuit of extreme efficiency and security, usually operates in a 'dark pool' mode, and its pricing strategy (though not public) is likely also 'active'.

Therefore, although mainstream media sometimes mix these terms, the term 'proprietary AMM' directly points to the root of the problem from a fundamental logic perspective: who controls the funds, and who bears the risk. Compared to the 'Dark Pool AMM' or 'Active Market Maker' that describes technical characteristics, 'Proprietary AMM' more accurately reveals the essence of this new force from the perspective of business model and operational entities.

Efficiency Revolution: Why Has Solana Become the Ultimate Testing Ground?

The rise of proprietary AMM stems from its precise targeting of the core pain points of traditional AMM. The passive design of traditional liquidity pools inevitably leads to high slippage when facing large transactions, and long-term suffering from impermanent loss and MEV attacks (such as sandwich attacks). Proprietary AMM almost perfectly solves these problems through refined management by professional teams and active quoting strategies. They can offer users narrower spreads, lower slippage, and more stable trading outcomes, especially in large exchanges, where the experience is now extremely close to that of top centralized exchanges.

All of this is inseparable from Solana's unique blockchain architecture. Firstly, Solana's high throughput and extremely low transaction fees make this 'active' model, which requires frequent updates of quotes, economically feasible. Secondly, the dominant position of aggregators (especially Jupiter) in the Solana ecosystem creates a 'one-stop distribution channel' for these market makers. They do not need to establish their own brand, website, or user community, allowing all resources to focus on their unique core competencies—execution and pricing—this extreme specialization greatly simplifies their business model and reduces operational costs.

It can be said that proprietary AMM is not simply a choice of Solana; it is itself a symbiotic and native market structure with Solana, a perfect example of the co-evolution between the high-performance architecture of underlying public chains and the business models of upper-layer financial applications.

Future Landscape: The Wave of Specialization and the Specter of 'Centralization'

The rise of proprietary AMM indicates that on-chain markets are moving towards a more professional and polarized direction, and a clear 'dual-track market' will gradually take shape.

Mature Asset Market: High liquidity trading pairs like SOL-stablecoin will increasingly be dominated by proprietary AMM that can provide extreme spreads.

Long Tail Asset Market: Trading pairs like newly launched meme coins on foreign exchanges will continue to rely on traditional AMMs like Raydium, which do not require permission, for early price discovery and liquidity guidance.

This trend is a victory of mechanism efficiency, marking that on-chain market making is undergoing a profound wave of specialization. The market structure is shifting from open liquidity crowdsourcing to specialized market making by a few teams, greatly improving the execution efficiency and security of on-chain trading and setting new benchmarks for the industry.

But the other side of the coin is the renewed concern about the specter of 'centralization'. While users enjoy better execution quality, they inadvertently make a trade-off and sacrifice: they exchange DeFi's core principles of high transparency, permissionless access, and decentralization for extreme efficiency. When most order flows are directed towards a few anonymous 'black boxes', although transactions are still settled on-chain, the opacity in the process undoubtedly introduces new trust risks and undermines the auditability foundation upon which DeFi is built.

From a more macro perspective, the dominant position of proprietary AMM is reshaping and consolidating Solana's ecological positioning. It further strengthens Solana's image as the 'blockchain Nasdaq'—a venue tailored for high-performance, institutional-grade financial applications, with execution speed and capital efficiency as the highest principles. This gives Solana a differentiated advantage in the public chain competition, making it the preferred deployment platform for innovative protocols eager to combine CEX-like performance with DeFi core.

Conclusion

The rapid rise of proprietary AMM on Solana is not accidental but a logical and even inevitable evolution in the DeFi market's pursuit of extreme capital efficiency. Although it has sparked important discussions about the decentralized future, this proactive and efficient liquidity provision model has already elevated industry performance to new heights. Regardless of how the final landscape evolves, this silent revolution has already penned the preface for the next chapter of on-chain finance.