$XRP A heated debate about the future of XRP has reignited following comments from Tom Zschach, Chief Innovation Officer at SWIFT. In a widely shared LinkedIn exchange, Zschach argued that banks are unlikely to adopt XRP as a settlement asset, insisting they will prefer tokenized deposits or regulated stablecoins that remain under their direct control.

The discussion, highlighted in a post by $589 on X, quickly became ammunition for XRP skeptics who view it as confirmation that the asset has no role in global banking.

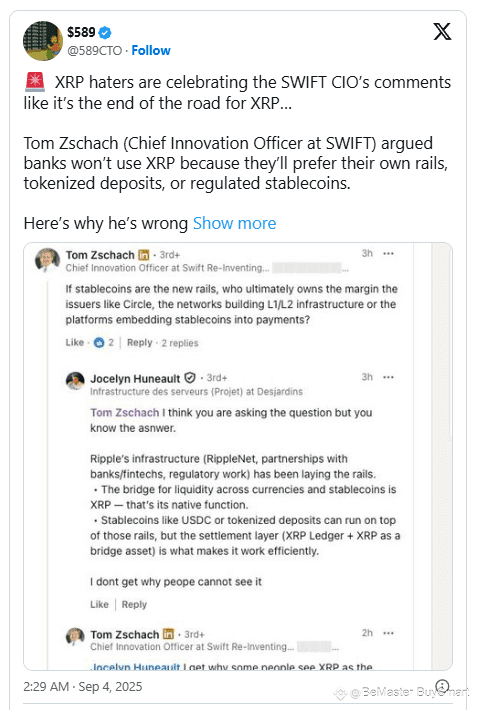

✨The LinkedIn Debate: XRP vs. Bank-Controlled Assets

The conversation began when Zschach asked who ultimately owns the margin in a financial system increasingly built on stablecoin rails. Jocelyn Huneault, an infrastructure expert at Desjardins, responded by stressing that Ripple’s ecosystem is already laying those rails.

Huneault explained:

“Ripple’s infrastructure (RippleNet, partnerships with banks/fintechs, regulatory work) has been laying the rails. The bridge for liquidity across currencies and stablecoins is XRP — that’s its native function. Stablecoins like USDC or tokenized deposits can run on top of those rails, but the settlement layer (XRP Ledger + XRP as a bridge asset) is what makes it work efficiently.”

Zschach pushed back, saying that while XRP might appear to be a natural bridge, banks would hesitate to rely on a token that doesn’t sit on their balance sheets. “Liquidity is one thing; legal enforceability is another,” he wrote, adding that banks may ask why they should pay a “toll” to an external asset when they can settle directly with instruments they already control.

✨Why That Argument Falls Short

Zschach’s concerns highlight real issues of trust and regulation, but they overlook the structural inefficiencies in the current global payments system. The reliance on nostro/vostro accounts, where banks pre-fund accounts worldwide to facilitate cross-border transfers, traps trillions of dollars in idle liquidity.

Internal rails or tokenized deposits do not solve this global-scale problem. XRP, by contrast, was designed specifically to unlock that liquidity by enabling settlement without pre-funding.

✨SWIFT’s Limitations in Settlement

Another point of contention is the role of SWIFT itself. The network facilitates messaging between banks but does not move money or provide settlement finality. Funds still travel through correspondent banks, perpetuating inefficiencies. Even if stablecoins are layered onto this system, the fundamental bottleneck of trapped capital remains.

✨XRP as a Neutral, Always-On Bridge

Unlike bank-issued tokens, XRP is neutral in its nature. It doesn’t reside on a single balance sheet, allowing for unique scalability that benefits institutions that need to conduct transactions beyond their own systems.

The XRP Ledger processes transactions in seconds, operates 24/7/365, and requires no reliance on a particular issuer’s balance sheet. This gives it an edge over tokenized deposits or stablecoins that remain constrained by their issuers’ systems.

✨Ripple’s Regulatory Strategy

Zschach correctly noted that legal enforceability is critical. That is precisely why Ripple has spent over a decade working with regulators and securing licenses in major jurisdictions. The launch of Ripple USD (RLUSD), a regulated stablecoin, provides banks with a compliant on-ramp that connects seamlessly with XRP and the XRP Ledger.

This hybrid approach reflects Ripple’s recognition that multiple forms of digital value will coexist, with XRP serving as the bridge.

✨The Direction of Travel

Even SWIFT acknowledges the shift. The organization is piloting systems to connect CBDCs and tokenized assets, a clear signal that the future is multi-rail and that interoperability will be indispensable. In such an environment, a neutral bridge like XRP has a role no single bank-issued token can fully replace.

✨The Road Ahead

Zschach’s skepticism reflects the caution of established financial institutions, but it does not erase XRP’s value proposition. Stablecoins and tokenized deposits will play important roles, but they remain siloed solutions.

XRP addresses the challenge of freeing trapped liquidity across borders and systems. As $589 emphasized, the facts remain clear: XRP is neutral, liquid, always available, and designed for the trillion-dollar inefficiencies that persist in global finance.

Far from signaling the end of the road, SWIFT’s doubts only highlight why XRP’s unique role may become indispensable once regulation and adoption converge.

🚀🚀🚀 FOLLOW BE_MASTER BUY_SMART 💰💰💰

Appreciate the work. 😍 Thank You. 👍 FOLLOW BeMaster BuySmart 🚀 TO FIND OUT MORE $$$$$ 🤩 BE MASTER BUY SMART 💰🤩

🚀🚀🚀 PLEASE CLICK FOLLOW BE MASTER BUY SMART - Thank You.