Under the trend of compliance, the crypto industry may usher in a golden age.

Entering 2025, the crypto industry welcomes a true turning point.

In fact, over the past decade, the market has been exploring in a regulatory vacuum and gray experimental zone. Although it has given rise to a massive trading scale, it has never entered the compliant mainstream.

Now, as the regulatory framework gradually clarifies, the industry has finally entered a new phase.

In the US, the (Financial Innovation and Technology Act) (FIT21) passed by Congress establishes a framework for the regulation of crypto assets, clarifying the division of responsibilities between the SEC and CFTC; meanwhile, the (Clarity for Payment Stablecoins Act) has become one of the most watched pieces of legislation, requiring that stablecoin issuance must have 1:1 reserves and qualified custody, which is currently under review.

The EU's (Regulation on Markets in Crypto Assets) (MiCA) will come into full effect in 2025, unifying the regulation of stablecoins, crypto service providers, and token issuances, providing institutional protection for the European market for the first time.

Financial centers in Asia such as Singapore, Hong Kong, and Japan are also advancing compliance pathways for stablecoins and virtual assets, while traditional banks and financial institutions are beginning to pilot projects.

The clarity of policies is reshaping market expectations.

We see that after experiencing a contraction in 2022-2023, the market value of stablecoins rebounded to over $150 billion in early 2025, with compliant stablecoins gradually becoming the main force in cross-border settlements.

At the same time, institutional funds are rapidly entering the market:

BlackRock's spot Bitcoin ETF is set to be approved by the end of 2024, attracting billions of dollars in capital; Visa and PayPal are also beginning to directly embed USDC and PYUSD into cross-border settlement and e-commerce payment networks.

These signals collectively indicate that the crypto industry is shifting from 'speculative narrative' to 'institutional dividend-driven', with long-standing uncertainties troubling the market, including concerns about whether users can comply with usage, whether institutions can comply with investment, and whether financial giants can comply with access, gradually being resolved.

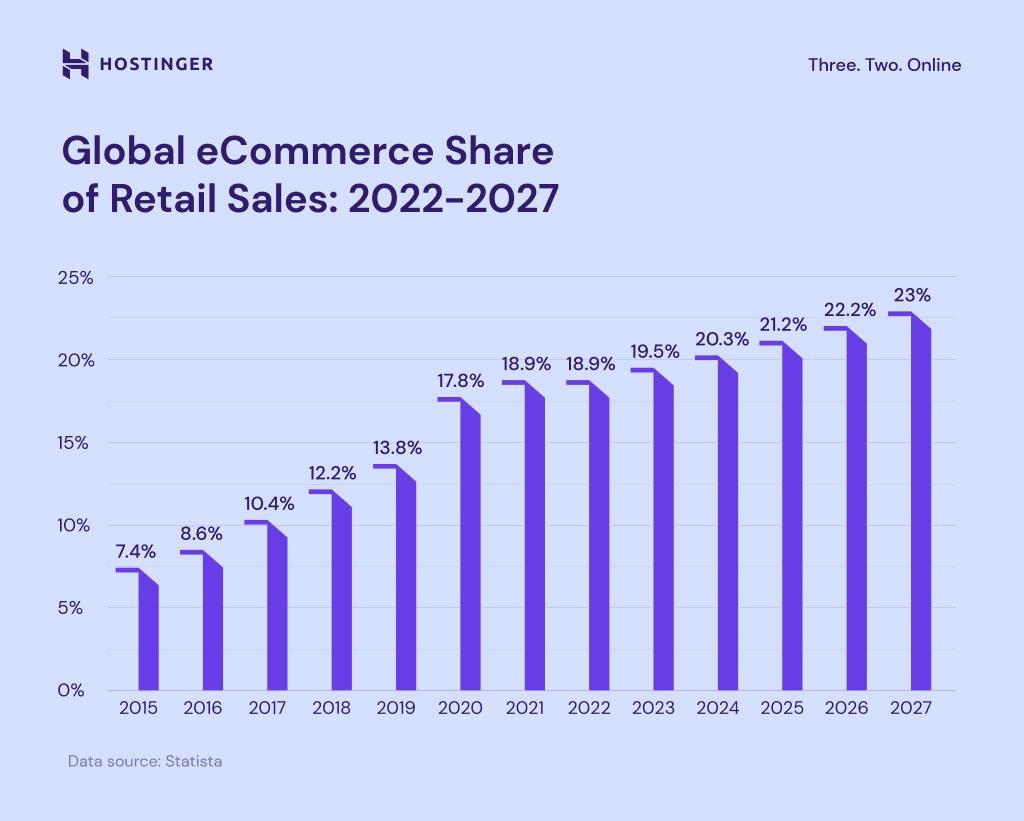

Changes in the share of global e-commerce sales in the retail market from 2015 to 2027

In this context, the development logic of Web3 is also transforming: from relying on speculative and liquidity narratives to applications that can support real consumption and payment scenarios. As institutional opportunities and trillion-dollar consumption markets overlap, the narrative of the consumption economy may become the starting point of a new round of golden age.

The consumption narrative will become the new 'traffic hub'.

On the other hand, although exchanges and public chains are still the primary entry points for current Web3 users, with the former facilitating asset buying and selling flows and the latter providing the infrastructure for applications and development, the entry point that can truly touch high-frequency consumer payments remains blank. In other words, while users can easily buy cryptocurrency assets on exchanges today, it is still challenging to use these assets directly for payments in daily life.

This gap is particularly evident in data.

The annual scale of global retail payments has exceeded trillions of dollars, covering various scenarios from daily retail to cross-border e-commerce. In contrast, although on-chain payments and stablecoin settlements have grown rapidly in recent years, their penetration rate is still below 5%. The blockchain has accumulated a massive stock on the asset side, but there remains a significant gap between it and the most critical interface of consumption payments with the real economy.

Expected growth in e-commerce market sales.

It is precisely this gap that has become the biggest bottleneck in the industry's development.

On one hand, on-chain assets lack high-frequency circulation scenarios, making it difficult to truly realize their use value.

On the other hand, the traditional consumption system is firmly locked by traditional financial networks and regulatory systems, leaving users always lacking a bridge between 'on-chain wealth' and 'daily life'.

The regulatory shift since 2025 has opened up dual spaces of policy and capital for payment-related Web3 applications. Compliant stablecoins are gradually gaining institutional recognition, traditional financial giants are beginning to explore on-chain settlements, and institutional capital is actively seeking infrastructure that can accommodate real payment flows. This means that migrating real consumption scenarios onto the chain will become the most promising narrative direction in this round of the market.

In this landscape, consumption payments will become a strategic gap, and the ecosystem that first establishes user habits and network effects at this high-frequency entry point is likely to become the true 'traffic hub' in the golden age of Web3.

In this context, PSP, as an on-chain infrastructure aimed at the consumption economy, is expected to align with new industry trends and open the next phase of trends.

PSP: Building an integrated consumption network on-chain and off-chain

PSP (Pre-Spending Power) is an on-chain infrastructure aimed at the consumption economy. Its design goal is to systematically integrate consumption behavior, credit accumulation, and asset flow into the same chain, building a consumption-driven ecosystem that supports long-term growth.

In traditional systems, elements such as payment, points, credit, financing, and supply chain fulfillment are often fragmented, with different institutions controlling different data and value capture points.

PSP attempts to break this disconnection and recombine them on-chain. Through the transparency and immutability of blockchain, the rights confirmation mechanism of real-world assets (RWA), the distributed node network of DePIN, and the data optimization capabilities of AI, PSP enables isolated links to operate within the same framework. This way, every consumption behavior can become a traceable data record and asset certificate, which can be reused in subsequent scenarios.

Focusing on the PSP system, its overall structure includes five core components:

Payment networks and debit cards: This is the most intuitive entry point for users to access the ecosystem. Users can make payments using stablecoins and digital assets, both in e-commerce and retail, as well as seamlessly settle in cross-border transactions. Physical and virtual debit cards further lower the operational threshold for users, allowing on-chain assets to truly enter daily consumption.

Loyalty and points systems: Traditional points systems are often closed and have poor liquidity. PSP introduces PowerPennies, transforming consumption records into verifiable digital assets that can not only be used for consumption but also traded, collateralized, or even linked with financial products. Points thus shift from being ancillary rights to becoming real asset units for users.

Credit and financial modules: In the PSP ecosystem, users' consumption and interaction behaviors will accumulate into on-chain credit profiles. This allows the platform to support richer consumer finance services, such as BNPL (buy now, pay later), NFT pre-sale contracts, and collateral financing. For users, this means more financing options; for merchants, it means more efficient risk management and credit support.

DePIN fulfillment network: Payment involves not only the flow of funds but also the fulfillment of goods and services. PSP incorporates warehousing, logistics, and distribution nodes into a decentralized incentive system, allowing the fulfillment process to be tracked and verified on-chain. This improves transparency and reduces costs associated with intermediaries and information asymmetry. In cross-border transactions, this mechanism can particularly enhance efficiency and trust.

AI smart engine: PSP utilizes artificial intelligence to achieve a higher level of optimization. AI can provide personalized recommendations based on user profiles and transaction data, assist in credit assessments and risk control on the financial level, and offer dynamic advice on spending and saving at the asset management level. This capability allows consumption to no longer be a passive behavior but a dynamic process that adapts to user needs and market conditions.

Based on this system, PSP can generate practical application effects across multiple dimensions.

For users, it provides a channel to extend on-chain assets into daily life.

Whether in e-commerce shopping, offline retail, or payments and settlements during cross-border travel, stablecoins and digital assets can be smoothly used through debit card systems, simplifying the user’s operational process while providing clearer consumption purposes for on-chain assets. At the same time, the combination of points and credit systems means that consumption behavior is no longer limited to one-time expenditures but will continuously generate verifiable rights, which will accumulate in the form of digital assets over the long term, thus enhancing the value of consumption behavior in personal asset allocation.

For merchants and service providers, the role of PSP is reflected in both data and financial tools.

The accumulation of transaction data on the chain provides a more objective basis for credit assessment and risk control, enabling merchants to formulate financing and marketing strategies based on users' real behaviors. The introduction of modules such as BNPL or NFT pre-sale also gives merchants greater flexibility in capital turnover and sales methods. Meanwhile, the application of the DePIN fulfillment network provides transparent tracking and incentive mechanisms for warehousing, logistics, and distribution, thereby enhancing the efficiency of the supply chain and reducing risks and extra costs due to information asymmetry in cross-border transactions.

On a broader ecological level, the architecture of PSP creates entry opportunities for various types of participants.

Logistics nodes, small service providers, content creators, etc., can access the network by providing services, fulfilling contracts, or contributing content, and receive corresponding incentives. This mechanism enhances the participation and diversity of the ecosystem, allowing value creation to no longer be limited to the platform itself but to be collaboratively completed by multiple parties. As the number and types of participants increase, the overall utility of the ecosystem continues to enhance, and the network effect will gradually amplify.

Therefore, from the perspective of the fundamentals of PSP, it not only addresses the execution issues of consumer payments but also integrates consumption behavior, credit systems, and asset management through an integrated architecture, forming a complete consumption economy closed loop that encompasses users, merchants, service providers, and institutions. This brings higher consumption added value to users, provides more reliable collaboration tools for merchants and service providers, and creates paths for wider participants to enter and benefit.

The new transformation brought by PSP

In fact, looking back at the past rounds of industrial evolution, every new technology narrative ultimately needs to find a way to accommodate high-frequency and universal economic variables. The industrial revolution reshaped social division of labor through productivity improvements, while the internet drove new business models by connecting information and people.

In recent years, the development of Web3 has undergone multi-layered evolution. The earliest wave focused on the financial level, where DeFi explored asset liquidity and transparency through trading, lending, and derivatives experiments, while the narrative in the cultural and social layer transitioned to NFTs, DAOs, and decentralized social interactions, attempting to assetize identity, organization, and symbolic assets. Meanwhile, infrastructure continuously improved, with public chains expanding, cross-chain communication, privacy computing, oracles, etc., providing possibilities for more complex application scenarios. It can be seen that the commonality behind these narratives is the expectation to migrate activities such as finance, culture, organization, and collaboration that already exist in human society into a new institutional and technological framework.

From this more macro perspective, the next variable becomes evident: consumption.

It is the largest and most universal behavior in the economy, as well as a hub connecting finance, culture, and collaboration. Making consumption, this fundamental economic variable, on-chain may be the key step in driving Web3 from early experiments to large-scale applications.

From a macro perspective, consumption has three characteristics that give it unique potential for on-chain migration.

Global retail consumption occupies a large part of GDP, far exceeding the scale of financial derivatives.

Unlike sporadic asset transactions, consumption is a daily behavior that naturally brings network effects.

Consumption is not just a one-time expenditure; it also generates points, credit, contracts, and data, all of which can be further verified and utilized on-chain.

These attributes determine that once consumption migrates on-chain, it will not only bring traffic but also generate combinable financial and data assets.

Similarly, as mentioned above, macro market trends are also providing conditions for this transformation.

Institutional level: The US, Europe, and Asia are clarifying the regulatory framework for stablecoins and payments.

Digital level: E-commerce, cross-border retail, and online content have become important engines for global growth, with user payment and consumption data highly concentrated.

Financial level: BNPL, points financialization, and pre-sale models have been validated in the Web2 environment, indicating a stable demand for consumer finance and user incentives.

These three forces combined make 'assetization of consumption behavior' a more logical evolution direction for the era.

Looking back at the development experience of Web2, transformation often occurs when existing paths are optimized and reconstructed.

The success of Alipay and WeChat Pay lies in gradually migrating payment habits to mobile through points, red envelopes, and social interactions in familiar scenarios; Amazon Prime relies on points rebates and logistics experiences to firmly lock users into its e-commerce closed loop. These cases illustrate that users will not change their habits for unfamiliar narratives, but if the added value and convenience are sufficiently large, they will quickly complete the migration.

Based on this experience, the path of PSP is to work simultaneously on lowering thresholds and enhancing returns:

The front end provides card and wallet interfaces, allowing users to complete payments in existing scenarios; the back end transforms payment behavior into points, credit, and combinable assets, making consumption no longer the 'end point of expenditure' on the user side, but rather a starting point that can continuously bring rights. As the frequency of use on the user side increases and credit data improves, merchants' financial services and risk control capabilities will also be enhanced; as merchants and service providers are onboarded, the richness of goods and services increases, further enhancing user retention. This cycle amplifies the network effect, allowing every participant in the consumption chain to gain positive incentives.

Macro-wise, the significance of consumption migration lies in that PSP is the first to shift Web3 from asset speculation to mass economy.

In recent years, industry narratives have focused more on a few investors and speculative behaviors, but when consumption—this most universal variable—is integrated into the on-chain system, Web3 truly holds the potential to reach a large-scale user base. In other words, the migration of consumer payments is not just a new business model but may become a watershed that distinguishes the past 'speculative narrative' from the future 'application narrative'.

Therefore, PSP is redefining the role of consumption in the on-chain economy. By integrating payment, credit, points, fulfillment, and asset management into the same architecture, PSP allows consumption behavior to possess characteristics of traceability, accumulation, and reusability for the first time.

It not only solves the problem of 'how to pay' but also opens up a new path of 'consumption as asset, consumption as credit'. This mechanism transforms consumption from a single expenditure event into a foundational engine that can drive financial services, supply chain collaboration, and ecosystem growth. In other words, the new transformation brought by PSP makes consumption a variable in the infrastructure of Web3, allowing the industry to move from relying on speculative narratives to a long-term application era supported by real economic behavior.

From a macro perspective, PSP is backed by the largest economic scale of the global consumption market.

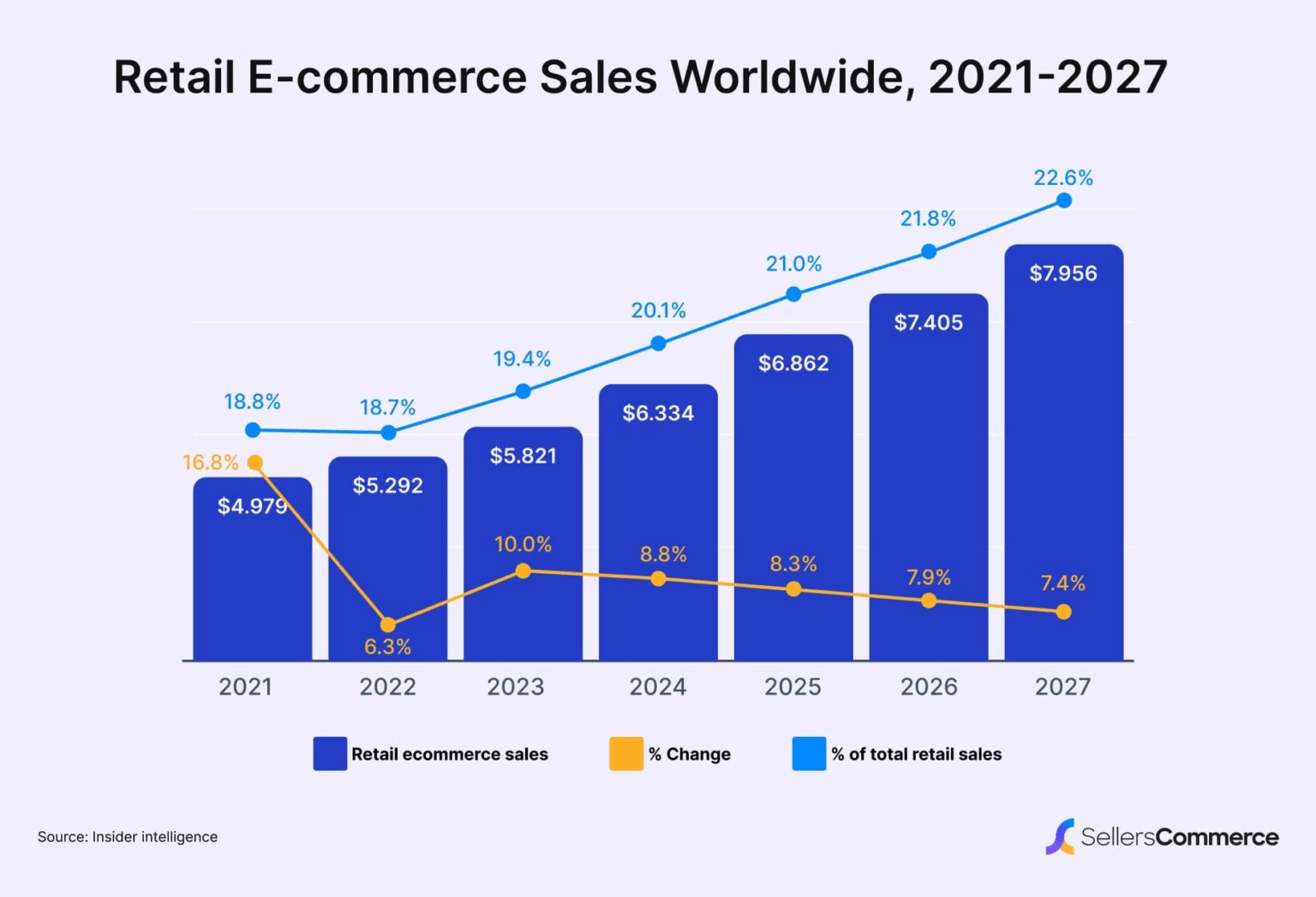

Retail consumption has long accounted for over 60% of global GDP. Just in 2023, global retail sales have exceeded $30 trillion, with the share of cross-border e-commerce and digital retail continuing to grow. It is expected that by 2030, the scale of the cross-border e-commerce market will reach $7-8 trillion. This means that consumption is not only the core engine of the global economy but also the most universal and high-frequency behavioral variable.

In such a multi-trillion dollar market, even if only a very small proportion is digitized, assetized, and migrated on-chain, the released increment is enough to reshape the industry landscape.

Unlike previous market stories driven by speculation, the value space of PSP comes from its direct anchoring of the most widespread economic activity, which is consumption. This is precisely why it undertakes the long-term migration demands of a macro market.