In the world of DeFi, we have seen too many 'Lego' stitching games, but very few can seamlessly integrate the rigor of traditional finance with the efficiency of the on-chain world.

First of all, it must be made clear that Huma Institutional is not a simple lending pool; its underlying logic originates from a very core area in mature financial markets—structured finance. This means that from its inception, it has been thinking about how to precisely slice and reorganize the risks and returns of a basic asset (such as accounts receivable) to meet the needs of institutions with different risk appetites.

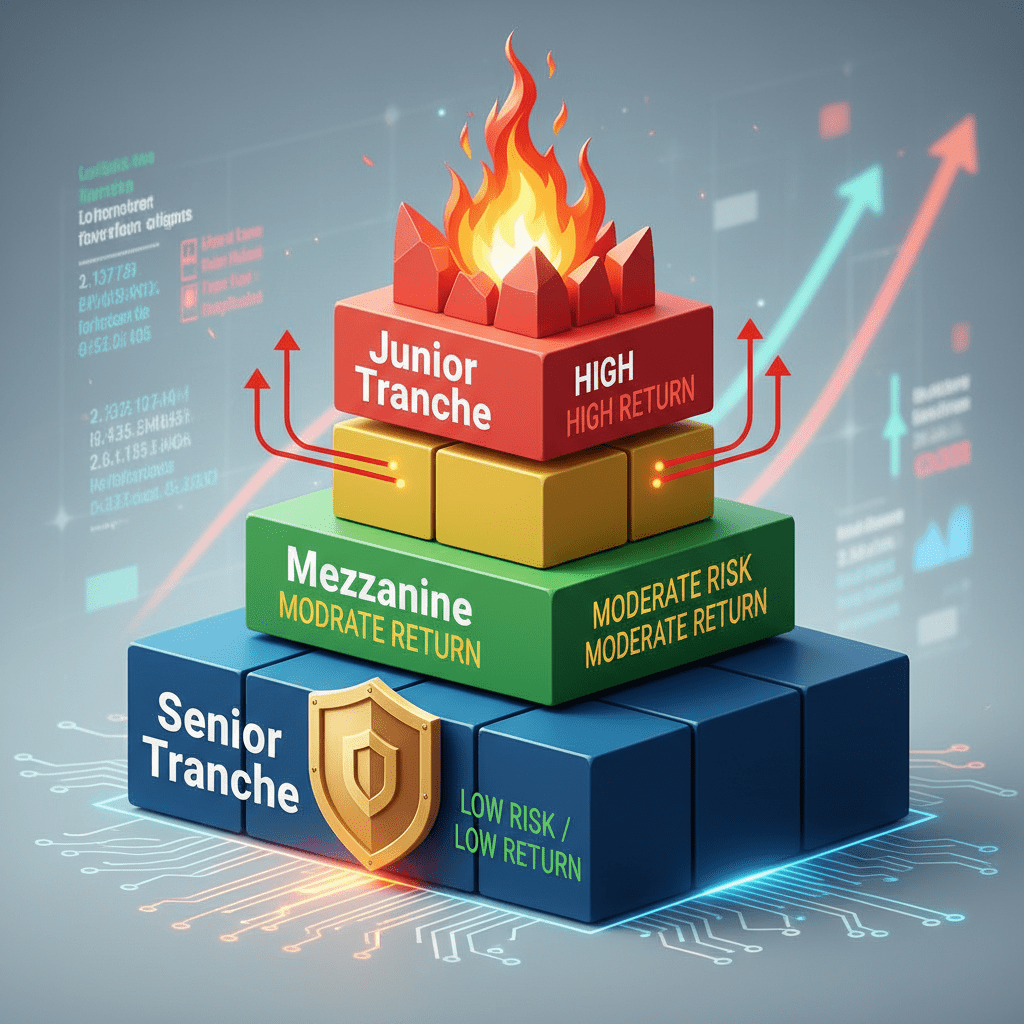

The most intuitive manifestation of this slicing is the 'Tranches' design. You can think of it as a 'safety cushion' system. Senior tranche investors enjoy the lowest risk and stable returns, while junior tranche investors use their potential 'First Loss' to provide protection for the senior tranche, and of course, they also have the opportunity to achieve higher potential returns.

The brilliance of the Huma protocol lies in its modularization of this process. [It has built-in first loss capital structures of up to 16 layers, allowing asset providers and capital providers to flexibly configure risk buffer capital from borrowers, insurance, or different investors, thereby tailoring a precise risk-return ratio for every layer of funding.

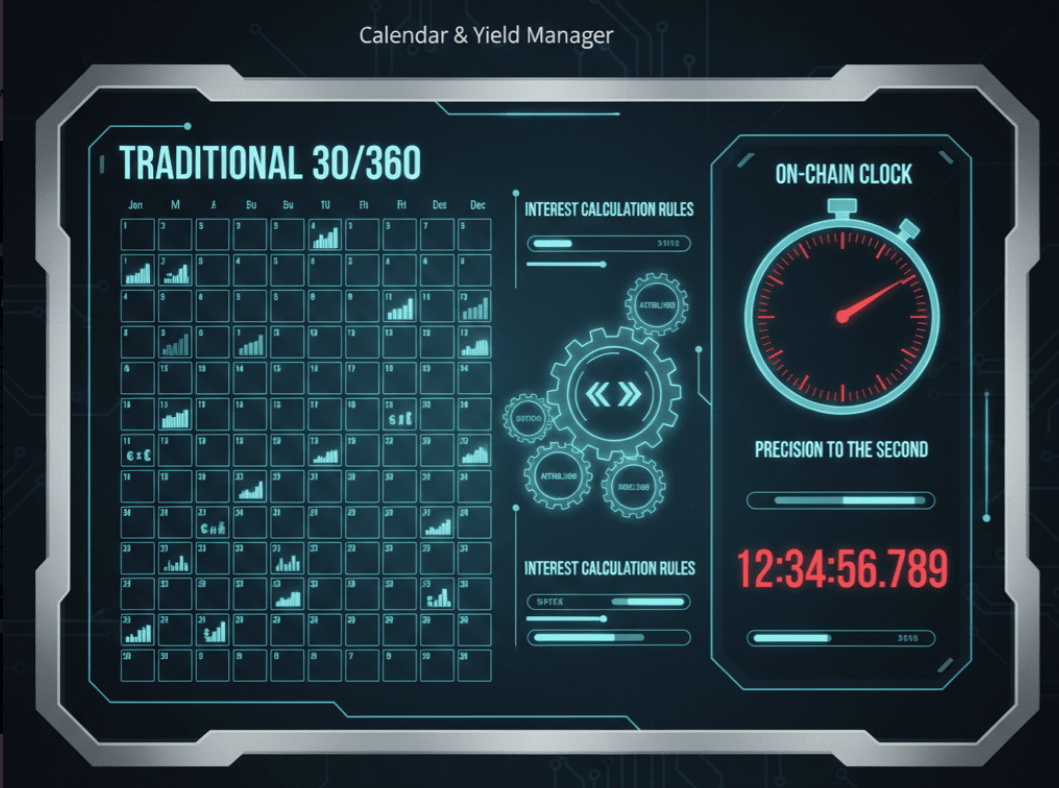

Secondly, Huma Institutional's design fully respects and accommodates the 'linguistic habits' of traditional finance. For example, it introduces configurable 'Calendar' and 'Yield Manager' modules.

We know that in the traditional financial world, many fixed income products use a '30/360' interest calculation method, meaning that regardless of whether it is a long month or a short month, interest is calculated as if every month has 30 days and a year has 360 days. This is completely different from the precise second-based interest calculation method in the DeFi world. Huma's modular design allows an asset pool to freely choose the applicable interest calculation rules, whether following traditional practices or embracing efficient on-chain calculations; the protocol can seamlessly support both. This greatly reduces the friction costs for traditional institutions entering the on-chain world.

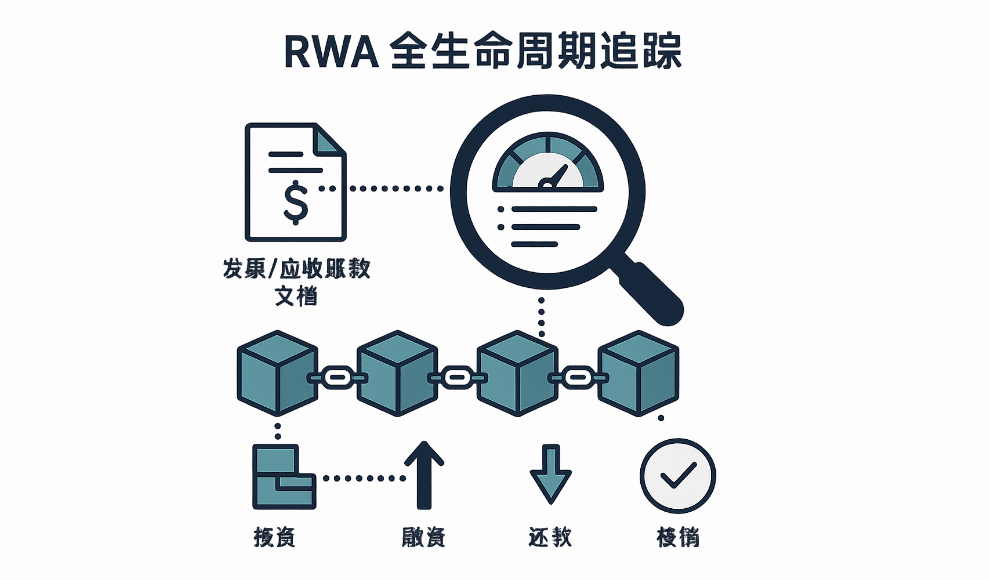

Of course, all these complex and precise structures ultimately need to be presented through the language of blockchain. One of the core values of Huma Institutional is to clearly and transparently map real-world assets (RWA) onto the chain through tokenization. It is not just about issuing a token that represents asset ownership; more importantly, it records the entire lifecycle of an accounts receivable—from generation, financing, repayment to write-off—in an immutable manner. This means that investors can easily and in real-time monitor the performance of the underlying assets; risk is no longer a black box but a quantifiable, traceable, and manageable on-chain data stream.

The true charm of Huma Institutional lies not in creating a brand new asset, but in building a sufficiently professional, flexible, and transparent 'translation' and 'assembly' system. It re-implements the time-tested risk control logic and product structure from the traditional structured finance sector in a modular way using blockchain, thereby finding an excellent balance between institutional-level security compliance and the high efficiency of DeFi. It is not about using DeFi to disrupt traditional finance, but about empowering the core business of traditional finance with DeFi, opening up a broader and more efficient credit market.