Last week, late at night, my phone kept vibrating— messages from fan A Qiang were filled with panic, sending 3 voice messages in a row: 'Bro! I can't open my ICBC card! The 150,000 I just sold BTC is still in there, and the bank said it was frozen by the Shandong police; will this money be lost? My mom is still waiting for this money to pay for her surgery!'

Opening the screenshot he sent, the bank card status clearly states 'judicial freezing', with a freezing period of 6 months. This is already the 7th fan this week who asked me about 'withdrawal card freeze': some converted USDT into RMB, but before they could transfer it to pay for a mortgage, the card was locked; some privately traded with strangers for a 2,000 profit, only to receive scam money, leading to police calling them to take a statement, nearly getting involved in a criminal case.

Today, let's not beat around the bush and thoroughly expose the 'withdrawal card freeze'— from the 'dirty money logic' of public security freezing cards to the 'risk control red line' of banks locking cards, from real-life stepping on mines cases to feasible unfreezing steps, this will help you avoid 90% of the pitfalls.

First, understand a painful premise: every penny you earn from selling coins is under the regulatory 'magnifying glass'.

Many people's first reaction after their cards are frozen is 'I didn’t commit a crime!'— but you may have forgotten that the central bank had already drawn a red line in September 2021: (Notice on Further Preventing and Handling Risks of Virtual Currency Trading and Speculation) clearly states that activities such as virtual currency trading and exchange are considered illegal financial activities, and related transactions are not protected by law.

What does this mean? When you convert BTC and USDT into RMB, the essence of your 'withdrawal' is essentially a 'risk behavior that regulators focus on'. Banks and public security are like two security checkpoints: as long as your fund flow has a hint of 'dirty money' (such as upstream being scam funds or gambling money), an alarm is triggered immediately, and the card is frozen without discussion.

Public security freezing cards: it’s not targeting you, but focusing on 'blood-stained money'— 3 real stepping on mines cases.

Public security card freezing is officially called 'judicial freezing', and the core is not to arrest you, but to trace 'dirty money'. Last year, a fan named Old Wang had a particularly typical experience: he sold USDT on a certain C2C platform, and the other party transferred 100,000 using a personal account. He transferred the money the same day to buy a financial product, and 3 days later his card was frozen—later he found out that the other party's money was the pension money of a scammed elderly woman, and Old Wang became a 'victim in the chain of funds'.

I have compiled 3 of the most common 'innocent scenarios', and after reading, you might break out in a cold sweat:

1. Upstream funds are scam money: the 'withdrawal' you received may be someone else's life-saving money.

Last month, a fan named Xiao Li sold 50,000 USDT on the platform. The buyer was a 'quick person', transferring the money immediately without haggling. As a result, a week later, his Construction Bank card was frozen by the Henan police— it turned out that buyer was part of a telecom fraud gang, who defrauded a college student of tuition, then turned around and used that money to buy USDT to 'clean it', and Xiao Li just happened to receive this 'dirty money'.

When public security investigates, they will trace the flow of funds 'to the end': from the victim → the scammer → the coin buying account → your account. As long as you are on this chain, your card will be frozen. What’s more troublesome is that even if you are completely unaware, you must cooperate with the investigation to prove 'you didn't know this money was dirty money'.

2. Funds linked to online gambling: hundreds of yuan in gambling funds split into multiple transactions, and you just happened to receive one.

Another fan, Old Chen, liked to 'withdraw small amounts multiple times' on small platforms, selling only 10,000 to 20,000 USDT each time. As a result, once he received 20,000 from a 'personal account in Foshan, Guangdong', and 3 days later his card was frozen— later the officer told him that account was a 'receiving account' for an online gambling platform, the platform split the gambling funds into hundreds of transactions, and Old Chen just happened to receive one, becoming a link in the 'gambling fund transfer chain'.

This situation is the most unjust: you think it’s a 'normal transaction', but you've already been caught up in a gambling case, with an unfreeze period of at least 6 months, or even longer.

3. Helping others 'withdraw money' for a fee: seems easy, but actually steps on the 'aiding crime' red line.

The most dangerous is 'acting as a withdrawal agent'. Last year, there was a case in Shenzhen: a fan named Xiao Lin was asked by a friend to 'help', using her bank card to receive coin payments, and then transferring it to her friend for a 3% handling fee. Xiao Lin thought 'since the money just passes through my hands, there’s no risk', so she helped and transferred 300,000 back and forth. As a result, a month later, the police showed up— the friend's money was 'cut from online gambling', and Xiao Lin was sentenced to 1.5 years for 'aiding information network crime' (aiding crime), and had to return the 300,000 dirty money.

Remember: as long as your card helps others 'process dirty money', regardless of whether you collect a handling fee, you may violate the law.

Bank card freeze: it's not about catching you, but triggering the 'anti-money laundering alarm'— 3 most easily stepped on pitfalls.

Bank card freezing is more like 'temporary control', but it's still troublesome. Last week, a typical experience was shared by a fan named Xiao Zhang: he withdrew 50,000, received it in 3 transactions (from 3 different accounts), and transferred the money to his salary card that day. As a result, China Merchants Bank directly restricted him from 'non-counter transactions' (unable to transfer, unable to withdraw cash, only able to deposit money at the counter).

He went to the bank asking, and the teller pointed to the transaction flow saying: 'Your card usually has a monthly flow of only 3,000; suddenly there’s 50,000 coming from 3 unfamiliar accounts, and then transferred out the same day, the system directly flagged it as 'suspicious transaction'— the anti-money laundering risk control was triggered.'

Banks focus on three types of 'abnormal operations' that you might be doing every day:

1. Quick in and out: shuffling money like 'money laundering'.

Receiving a withdrawal of 100,000 at 10 am, transferring to another card at 2 pm, and transferring back the next day— this kind of operation in the banking system has the same characteristics as 'splitting funds and evading regulation' for money laundering. The bank doesn't care if you're selling coins; as long as the flow is 'quick in and out, with no reasonable purpose', the card will be locked.

2. Large transactions without a 'reasonable explanation'.

Someone withdrew 500,000, and when the bank called asking 'where did the funds come from?', he said 'it was transferred by a friend', then they asked 'who is your friend? Why did they transfer you money?' He couldn't answer— this kind of vague explanation will only make the bank more vigilant. What the bank wants is a 'traceable source', like 'part-time job payment' or 'goods payment' (must have proof), not 'money from a friend'.

3. Note stating 'virtual currency': directly crosses the regulatory red line.

The dumbest operation is to 'note the real hammer'— writing 'BTC withdrawal' or 'money from selling USDT' during the transfer. The bank's backend will see this clearly and directly lock the card without negotiation. For banks, 'virtual currency' is a regulatory red line; they'd rather mistakenly freeze 100 than let 1 go, after all, no one wants to bear the responsibility of 'providing services for illegal financial activities'.

Bank card freezing is relatively easier to resolve, usually in 3-7 days, but if you honestly say 'this is money from selling coins', the chances of being denied unfreezing are high— banks won't risk violating regulations for your money.

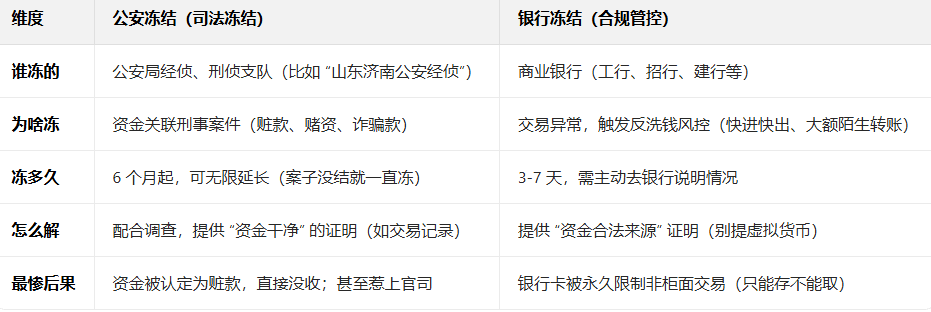

Public security card freezing vs bank card freezing: a table to clarify, don’t panic in the wrong direction.

Many people, after having their cards frozen, run around for help, sometimes looking for the bank and sometimes the public security. The key is to first clarify 'who froze it'.

Correct operation after the card is frozen: 3 steps, miss one step and you could lose everything.

Many people panic after their cards are frozen, either confronting the bank hard saying 'my money is legal', or looking for 'brokers' to pay for unfreezing, and end up making matters worse. Remember, the correct operation has only 3 steps:

Step one: first clarify 'who froze it'— don’t contact the wrong person.

Check APP information: Open mobile banking to see the status notes on the bank card— if it says 'XX Public Security Bureau frozen', it was frozen by public security; if it says 'internal bank risk control restriction', it was frozen by the bank.

Call bank customer service: directly ask 'Why was my card frozen? Who froze it? Is there a way to contact them?'— for example, customer service might say 'It was frozen by the Economic Investigation Team of the Public Security Bureau in Qingdao, Shandong, and the contact number is XXX'.

Request (freeze notice): If it was frozen by public security, ask the bank to send you a (freeze notice) (electronic or paper version) with the name, phone number, and unit of the case officer, which is key for subsequent communication.

Step two: respond appropriately, don’t speak carelessly.

👉 If it was frozen by public security: proactively contact them, don’t hide.

Tip for contacting the officer: don’t come up asking 'when can I get my money back', first politely say 'Hello, I am the holder of the XX bank card (after reporting the last 4 digits), I see my card has been frozen by your side, and I'd like to explain the situation and provide some materials'.

Materials to prepare: ① Exchange order screenshot (showing transaction time, amount, buyer account); ② Your real-name authentication information (ID photo); ③ Chat records with the buyer (if it’s a platform transaction, screenshot the platform's chat records); ④ Bank statement (indicating which transaction is the withdrawal).

Key reminder: if the officer asks you to 'return the dirty money', don’t rush to refuse, first ask 'how much to return? Will it be unblocked after returning? Can we sign a (unfreeze agreement)?'— to avoid returning money without unfreezing, ending up with empty joy.

👉 If it's a bank freeze: don't mention 'virtual currency', find a 'compliance reason'.

When speaking at the counter: don't foolishly say 'this is money from selling coins', instead say 'this is a friend's repayment' (prepare chat records with your friend, such as 'I borrowed 50,000 from you before, can you return it to me now?'), or 'this is my part-time job payment' (prepare the settlement records from the part-time platform).

Keep a soft attitude: don't confront the teller hard with 'this money is legal, why did you freeze my card'— the teller has no authority to judge 'legality'; they only see if you can provide 'compliance proof'. The more you cooperate, the faster the unfreezing.

Step three: be wary of 'unfreeze scammers'— don’t just get frozen and then get scammed.

Many people, after having their cards frozen, receive 'strange text messages': 'Your card is frozen? I’m an insider at the bank, pay 20,000 to help you unfreeze in 3 days, refund if it’s unsuccessful.' Remember: unfreezing from public security and banks follows official procedures; there’s no such thing as 'paying to find connections'.

Last year, a fan had 80,000 frozen and found a 'broker', giving them 30,000. However, the broker took the money and blocked him, and the card wasn't unfrozen— in the end, not only did he not get back the 80,000, but he was also scammed out of 30,000, making matters worse.

4 tips to avoid pitfalls: keep your withdrawal safe by 90% (all from fans' hard lessons).

Compared to unfreezing after a freeze, what's more important is 'avoiding pitfalls in advance'. These 4 tips are summarized from the experiences of dozens of fans with frozen cards; following them can save you a lot of detours.

1. Only conduct transactions through large platforms, don’t be greedy for small private benefits.

Fan Old Zhou, in order to save 200 yuan on handling fees, privately added a 'buyer' on WeChat for trading. After the other party transferred 50,000, Old Zhou transferred the USDT over, and 3 days later his card was frozen— it turned out the other party's money was scam funds. Although large platforms have higher fees (generally 0.1%-0.5%), they will review the buyer's fund source, at least filtering out some 'dirty money', making private trading 10 times safer.

2. Withdraw using a 'dedicated card', do not use salary cards / mortgage cards.

Specifically obtain a second-class card (with a daily transfer limit of 10,000 - 50,000) for withdrawals, and usually don’t keep too much money in it, nor use it for salary payments, mortgage payments, or linking to Alipay/WeChat. Even if it gets frozen, the loss will only be within this card, not affecting your life.

3. Transaction records 'triple backup', don’t wait until frozen to find them.

You need to have these three documents simultaneously: ① Exchange order screenshots; ② Transfer receipts; ③ Chat records with the buyer: ① in your phone's album; ② on a cloud drive (such as Baidu Cloud); ③ on a USB drive. Last year, a fan lost his phone, and all records were gone. After public security froze the card, he couldn't prove his innocence, losing 120,000 which he still hasn't recovered.

4. Small amounts withdrawn multiple times, don’t go all in at once.

If you have 100,000 to withdraw, don’t sell it all at once; split it into 5 transactions of 20,000 each, with an interval of more than 3 days, and don’t transfer to the same card. Large amounts of concentrated withdrawals are like 'setting off fireworks' in the risk control system; if they don't freeze you, who will they freeze? Additionally, after the withdrawal arrives, don’t transfer it out the same day; wait 1-2 days before transferring to avoid the suspicion of 'quick in and out'.

Lastly, let me say a hard truth: what you're gambling is not 'luck', but 'your livelihood'.

A fan told me he froze 80,000, which was his mother's surgery fee. He went to the police station every day and after three months, it was finally unfrozen. By then, his mother's surgery had been postponed. You think selling coins for withdrawal is 'making a bit of difference', but in fact, it's gambling— betting that the upstream funds are clean, betting that the bank won't trigger risk control, and betting that public security won't come knocking.

But the cost of losing a gamble could be something you can't bear: money is gone, the card is useless, and you might even get into legal trouble. Instead of figuring out 'how to unfreeze', it's better to first think clearly: is this kind of transaction, which is not protected by law, really worth the risk of 'losing both money and card'?

If you've also had experiences with frozen cards or have questions, follow Ming Ge— avoiding more people stepping into pitfalls is more important than anything.#机构筹资布局SOL #BNB创新高