Many crypto market experts believe that the familiar 4-year cycle of Bitcoin (BTC) is no longer as accurate as before. They point to several reasons such as: 95% of Bitcoin has been mined, about 1 million BTC currently sits in reserves of corporations, and macroeconomic factors along with increasingly influential regulatory policies are strongly driving prices.

This means that while the halving cycle has not completely disappeared, Bitcoin is no longer separate from the world. Instead, it moves in tandem with the traditional financial sector, where liquidity, refinancing, and long-term valuation are the key factors shaping the trend.

Understanding this rhythm may be as important for Bitcoin's future as its halving cycle.

Refinancing challenge: The 2026 debt wall

According to the Institute of International Finance (IIF), total global debt reached about $315 trillion in Q1 2024, with an average maturity of 7 years. This means approximately $50 trillion in debt needs to be refinanced each year.

The Financial Times notes that by 2026, the 'maturity wall' will increase by nearly 20%, reaching over $33 trillion, nearly three times the total annual capital investment spending of developed economies.

The need to refinance this massive debt load in the context of high interest rates will be a heavy burden for both governments and businesses, especially for those with weak financial health.

This will be a real test for risk assets such as stocks, high-yield bonds, emerging market debt, and even digital currencies. Market liquidity will be heavily drawn into refinancing needs, causing capital flows into risk assets to diminish.

Along with tightened borrowing conditions (even if the Fed starts to lower interest rates at the end of this year, the rates will still be much higher than during the 2010–2021 period), this could create pressure leading to increased capital costs, wider credit spreads, and investors demanding higher risk premiums.

When liquidity tightens, risk assets that rely on abundant cash flow will face valuation pressures, leading to reduced capital inflows and greater volatility.

For Bitcoin, this period coincides with the end of the 4-year cycle – a time that often falls into a bear market. If global liquidity does not grow strongly (experts estimate it needs to increase by 8%–10% annually for the system to remain stable), this wall of debt could create a significant shock.

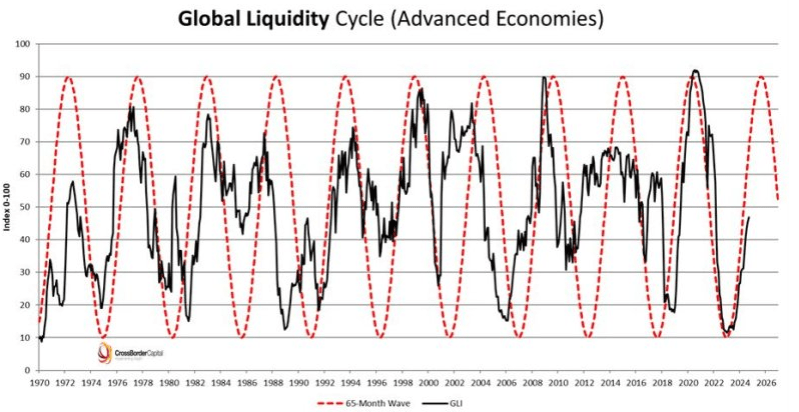

Will the liquidity cycle tighten in 2026?

Currently, global liquidity is still on the rise. As of June 2025, the M2 money supply of the four largest central banks has increased by 7% since the beginning of the year, reaching $95 trillion.

According to economist Michael Howell, including short-term debt and cash of households and businesses, this figure has reached $182.8 trillion in Q2 2025, an increase of $11.4 trillion since the end of 2024, approximately 1.6 times global GDP.

However, liquidity is also cyclical. Howell's global liquidity index hit a low at the end of 2022 and is now heading towards a peak by the end of 2025. In the past, when liquidity peaked, markets often faced significant volatility: short-term interest rates surged, and investors ramped up selling of risk assets.

U.S. liquidity also shows similar signals. According to the Federal Reserve Bank of New York, bank reserves are currently at $3.2 trillion – still considered 'ample', but the long-term goal is to reduce it to a 'sufficient' level.

From this perspective, if liquidity begins to contract in 2026, Bitcoin is almost certain to be affected, potentially exacerbating the bear market cycle. Conversely, if debt pressures force central banks to resume money pumping, this trend could bring a new lease of life for Bitcoin.

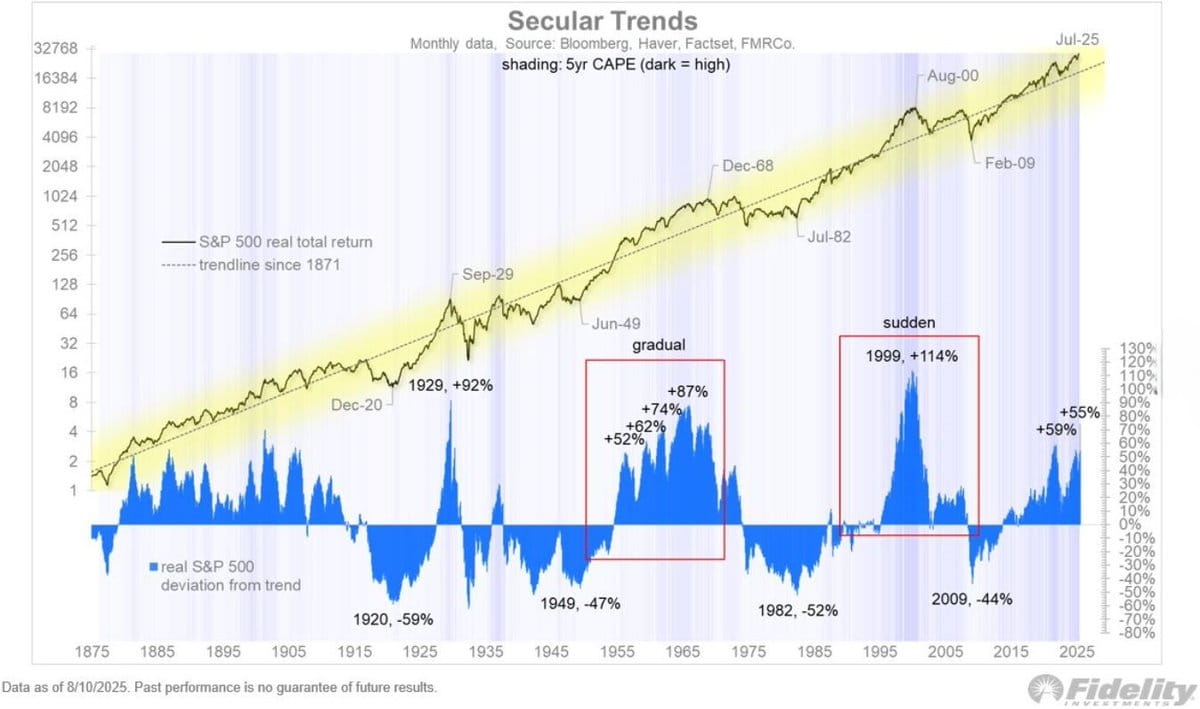

The long-term trend could peak in 2028.

In addition to liquidity and debt needing refinancing, long-term economic cycles also play an important role. According to The Kobeissi Letter and data from Fidelity, based on the CAPE model (cyclically adjusted P/E ratio), the current bull market began in 2009 and has lasted for 16 years.

In the past, the period from 1982 to 2000 saw a 114% increase before collapsing with the dot-com bubble, while the period from 1949 to 1968 ended with deeper corrections near the end of the cycle.

Many analyses suggest that the current market resembles the 1960s more than the late 1990s bubble. If history repeats itself, the current growth cycle could extend until around 2028, meaning an additional 2–3 years before it ends.

"This rally is extremely strong," analysts say.

This opens up the possibility that Bitcoin will experience a bear market that is not too severe in 2026, followed by a strong recovery in 2027–2028, coinciding with the next halving.

Overall, there is no single measure that can predict the future. The burden of debt, liquidity cycles, policy changes – innovation, and investor sentiment can all pull the economy in different directions.

The market's ups and downs depend on the interaction of these factors, and Bitcoin is no exception. The path ahead will be shaped not only by the halving event or liquidity peak but also by all the other dynamics.