On August 7, President Donald Trump signed an order allowing cryptocurrency to be included in 401(k) retirement programs. The cryptocurrency industry sees this as a significant step forward in promoting acceptance; however, investment experts warn that this comes with significant risks.

The executive order titled 'Democratizing Access to Alternative Assets for 401(k) Investors' has directed U.S. financial regulators to expand access to cryptocurrency and private companies within 401(k) plans.

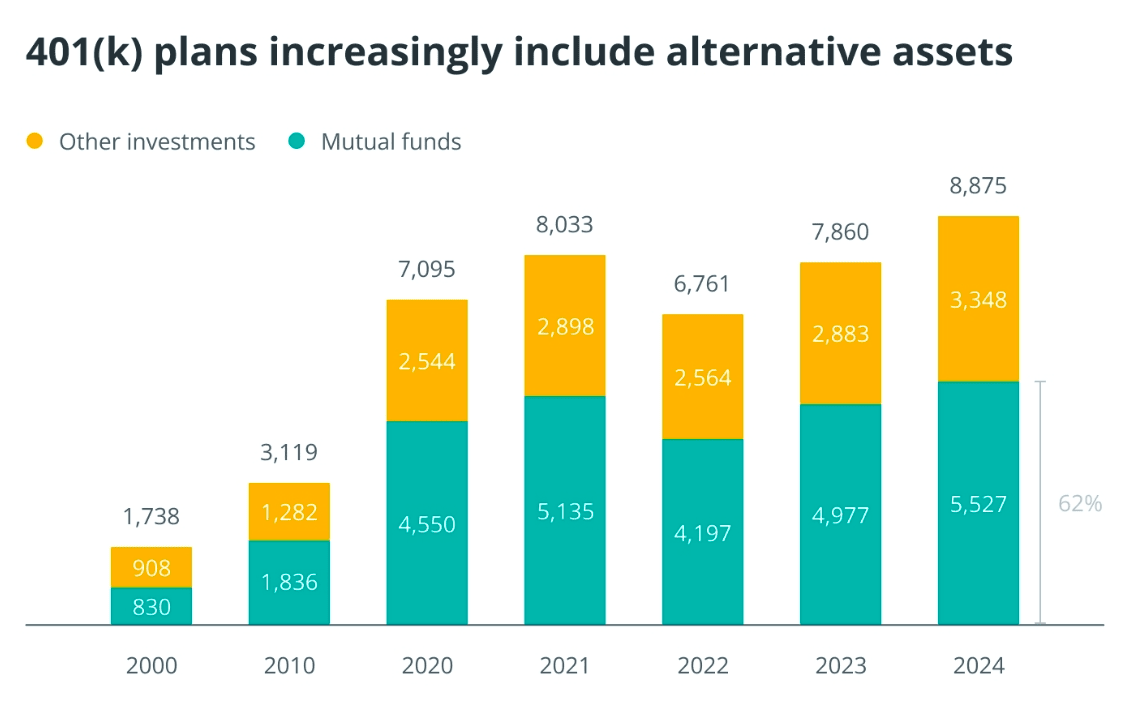

The 401(k) investment plan, a form of employer-sponsored retirement savings, is one of the most popular programs in the U.S. As of 2024, total assets in 401(k) plans reached $8.9 trillion, which could create a significant demand for cryptocurrency and potentially increase their value.

Although cryptocurrency traders may view this move as a positive signal for subsequent bull runs, financial experts and market observers emphasize that there are many concerning risks.

What risks does Bitcoin pose for 401(k) investors?

Trump's order opened up previously restricted investment opportunities in the most popular retirement plan in the U.S., requiring the U.S. Department of Labor to reassess restrictions on six different asset classes:

Private equity

Real estate (including debt instruments secured by real estate)

Actively managed cryptocurrency investment products

Commodities

Infrastructure development funding projects

Funds sharing longevity risk.

Industry experts suggest that increasing investment capital in the cryptocurrency market will drive up their values. André Dragosch, head of European research at Bitwise, a cryptocurrency asset management company, shared on the 'Chain Reaction' program on the X platform that Bitcoin could exceed $200,000 by the end of this year.

CJ Burnett, the revenue director of Compass Mining, emphasized: 'Accepting Bitcoin in 401(k) plans would open up a significant source of capital and passive investment flow, thereby increasing stability and minimizing the volatility of the asset.'

The 401(k) plan allows employees to contribute a portion of their income, often partially supported by employers, to invest in various funds and typically offers tax advantages.

Although 401(k) plans may benefit cryptocurrency, financial experts remain uncertain whether cryptocurrency is truly suitable for these plans.

One of the concerns raised by observers is the high fees associated with some alternative investments. According to the Investment Company Institute (ICI), the average fee for most assets in 401(k) plans is only 0.26%, while private investments often use a '2 and 20' structure, where managers charge a total fee of 2% and 20% on profits.

Philitsa Hanson, head of product, capital, and fund management at Allvue Systems, said: 'I don't think people are discussing the potential for higher fees enough.'

This executive order 'raises more questions than it answers,' Hanson continued. 'There are many things that need to be carefully considered about how these types of assets can be integrated into the system.'

Bitcoin ETF funds often have fees equivalent to the ICI average, although some large funds like ProShares Bitcoin Strategy ETF, Valkyrie Bitcoin and Ether Strategy ETF, and Grayscale Bitcoin Trust ETF have fees of 0.95%, 1.24%, and 1.50% respectively. These fees also do not include other factors affecting returns, such as liquidity and trading costs.

Ary Rosenbaum from the law firm Rosenbaum argues that Bitcoin is too volatile to be included in 401(k): 'When Bitcoin drops 40% in a week — and that will happen — lawyers will ask, 'Why are you offering such a risky asset?' 'What due diligence have you performed?' 'Where is the risk information?' He calls cryptocurrency a 'fiduciary maze' with complex mechanisms like staking, forks, and airdrops, along with complicated tax treatment. 'Suddenly, you've created a nightmare of education for participants.'

Margaret Rosenfeld, legal director of the staking provider Everstake, stated: 'The biggest risks remain the familiar risks of any investment: market volatility, cybersecurity, and fiduciary risk.' She also emphasized that 'these risks are not insurmountable.'

The need to 'improve the infrastructure' for 401(k)

Rosenfeld believes that updating regulations and guidelines related to 401(k) plans could alleviate many associated risks. She proposed establishing a clear standard for digital assets considered 'prudent.' She also noted that the Employee Retirement Income Security Act of 1974, which specifies what should be included in retirement plans, 'was built for stocks and bonds, not for blockchain.'

She recommended the need to 'improve the infrastructure' for retirement plans, emphasizing that 'the record-keeping systems supporting 401(k) plans are not designed for forks, airdrops, or real-time volatility. We need platforms ready for digital assets that can automatically track all on-chain events.'

Additionally, she also believes regulators should establish standards for liquidity, price transparency, custody, and cybersecurity to ensure that certain digital assets are 'retirement-ready,' including independent risk ratings.

'When managed properly, cryptocurrency in 401(k) plans can diversify retirement portfolios and provide greater transparency for a sector that often operates outside institutional oversight,' Rosenfeld said. However, this depends on cryptocurrency being managed effectively. Rosenbaum emphasized that cryptocurrency could be a valuable addition to a retirement portfolio as it offers diversification, protection against inflation, and 'exposure to financial innovation.' However, he asserts that cryptocurrency should not be in a 401(k) plan.

'Instead, use a brokerage account, a Roth IRA with a self-directed option, or use your discretionary income. But don't use a plan designed to be a financial lifeline for a retiree,' he said. Rosenbaum believes that, in the current situation, cryptocurrency is not a viable asset for 401(k) plans. 'It's just a shiny object, and pursuing it could put participants — and sponsors — at unnecessary risk. A conservative allocation rate of 1% to 5% does not address the underlying issue: volatility and complexity are incompatible with retirement plans.'

The Trump administration's move to loosen 401(k) requirements reflects a recent trend in legislation, where user protection and systemic risk are often overlooked to promote cryptocurrency acceptance and the development of the digital asset industry. The integration of cryptocurrency into the traditional financial system remains untested, and its outcomes are unpredictable.