Written by: Prathik Desai

Compiled by: Block unicorn

Today, we take a deep dive into Galaxy Digital's second-quarter financial report, as this digital asset and data center solutions provider is preparing for a transformation. From its core business—which accounts for 95% of revenue but has a profit margin of less than 1%—to a business model that sounds incredibly appealing in terms of revenue-to-expense ratio.

Summary

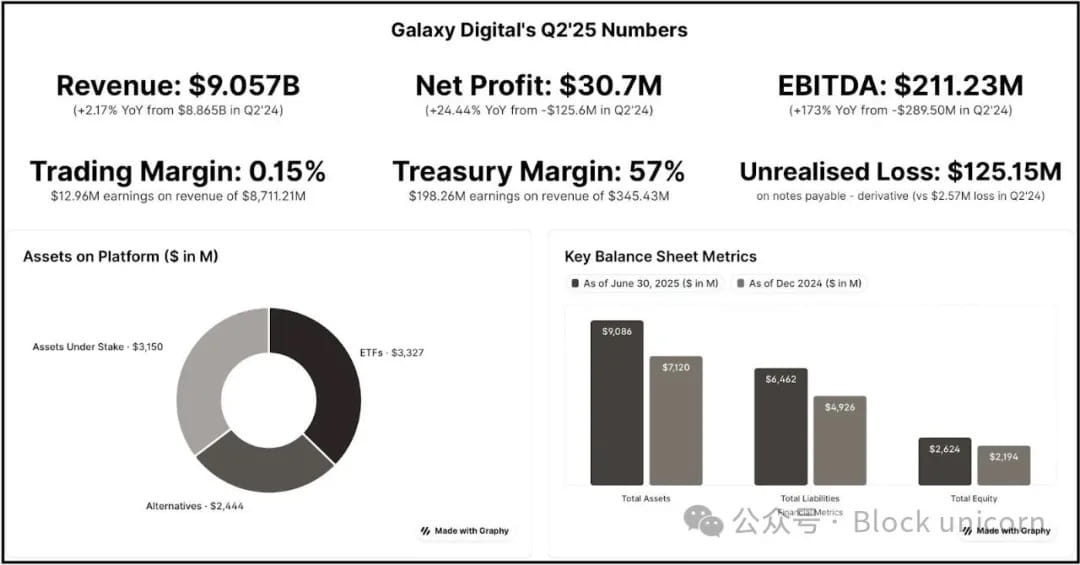

Galaxy's cryptocurrency trading business generated only $13 million in profit from $8.7 billion in revenue (profit margin of 0.15%), while paying $18.8 million in compensation each quarter—resulting in negative cash flow from core operations.

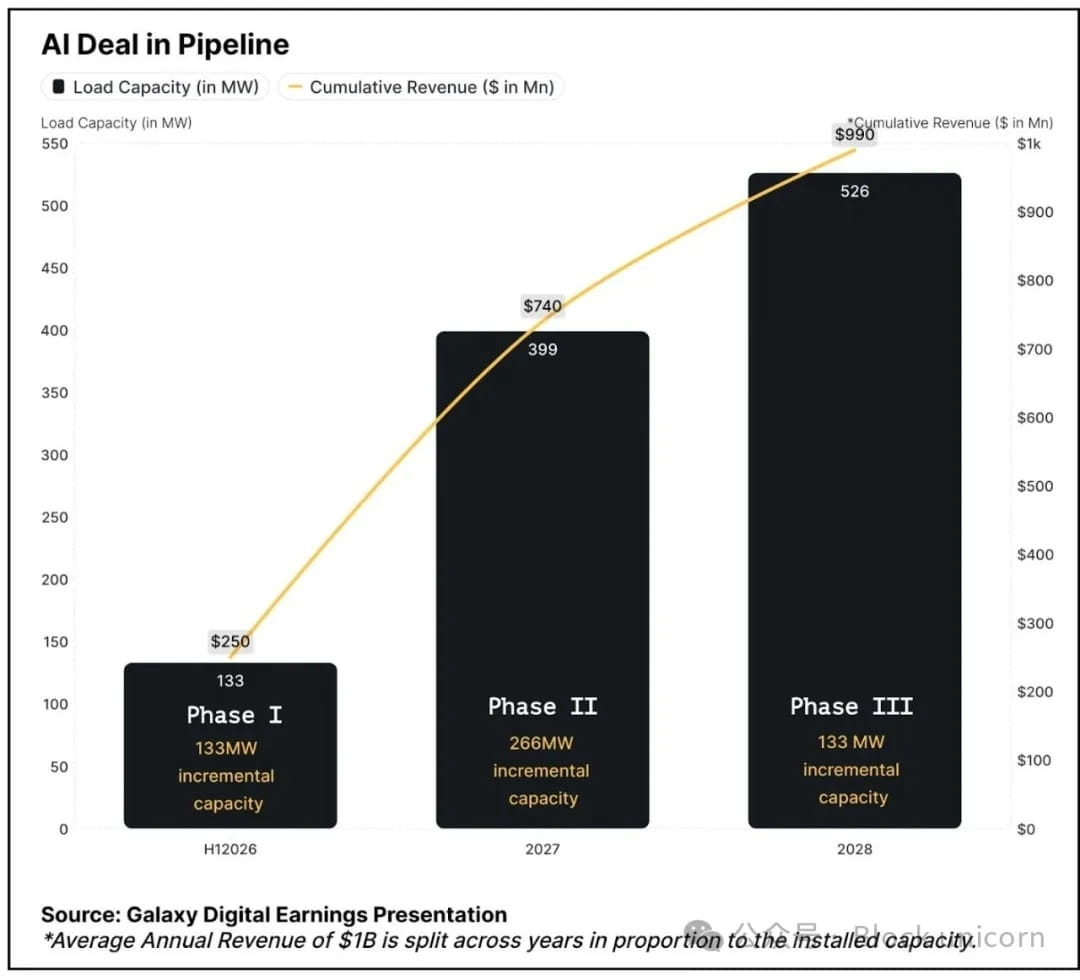

AI Transformation: Signing a 15-year, 526-megawatt contract with CoreWeave, expected to realize over $1 billion in annual revenue with a 90% profit margin starting from the first half of 2026.

Controlling 3.5 gigawatts of capacity in a constrained market, data center demand must quadruple by 2030.

Secured $1.4 billion in project financing, validating commercial viability and eliminating execution risk.

The current model relies on cryptocurrency asset returns ($198 million in the second quarter) to fund operations, as capital-intensive trading yields thin returns.

After a 17% rise in stock price, it fell back as investors see no incremental revenue before the first half of 2026.

When you look at Galaxy Digital's second-quarter data, it's easy to overlook one thing: what happens next. A closer look reveals that this company, led by Michael Novogratz, is at the turning point of shifting from cyclical cryptocurrency trading to more stable AI infrastructure revenue.

Goldmine of AI Infrastructure

Galaxy Digital is undergoing one of the largest business transformations in the cryptocurrency industry—shifting from low-margin trading to high-margin AI data centers.

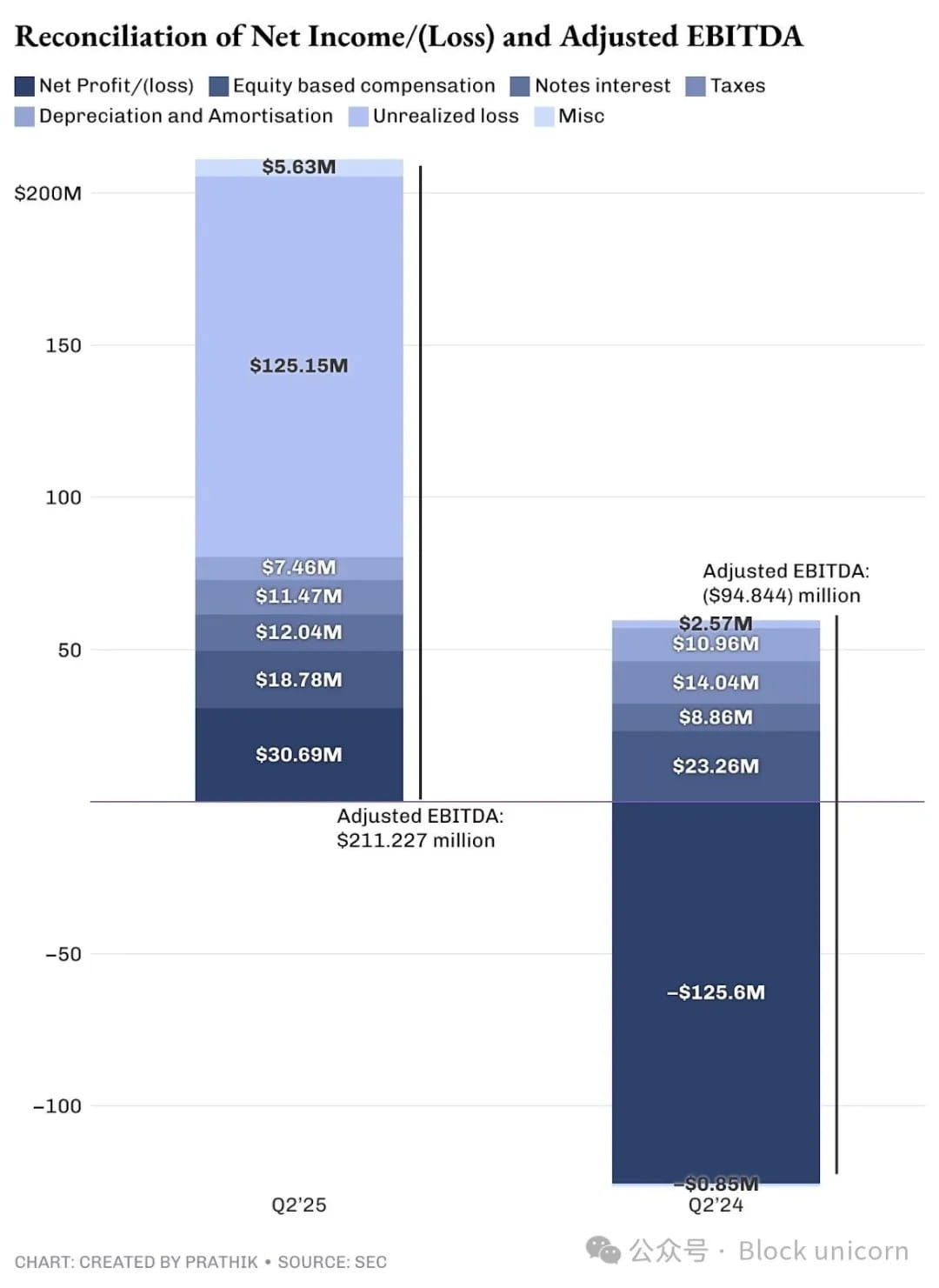

Galaxy reported $31 million in net income this quarter, with adjusted EBITDA totaling $211 million after adjusting for non-cash and unrealized expenses.

In its total revenue, the trading business earned only $13 million in profit from $8.7 billion in sales—a profit margin of just 0.15%. Therefore, 95% of its revenue is nearly unprofitable.

In contrast, their new AI data center contracts promise a 90% profit margin on over $1 billion in annual average revenue.

While I am optimistic about building AI and high-performance computing capabilities, I believe the promised profit margins are overly exaggerated. But don't just take my word for it; you can compare with the profit margins announced this quarter by top AI data operators like Equinix and Digital Realty: 46-47%.

However, I believe the direction is correct, purely from a revenue generation perspective. Currently, most of Galaxy's income comes from high-cost, low-profit trading operations. Most of its profits (revenue minus expenses) come from its asset and enterprise divisions.

The asset division includes investments in digital assets and mining activities, equity investments, realized and unrealized gains and losses from digital assets and equity investments.

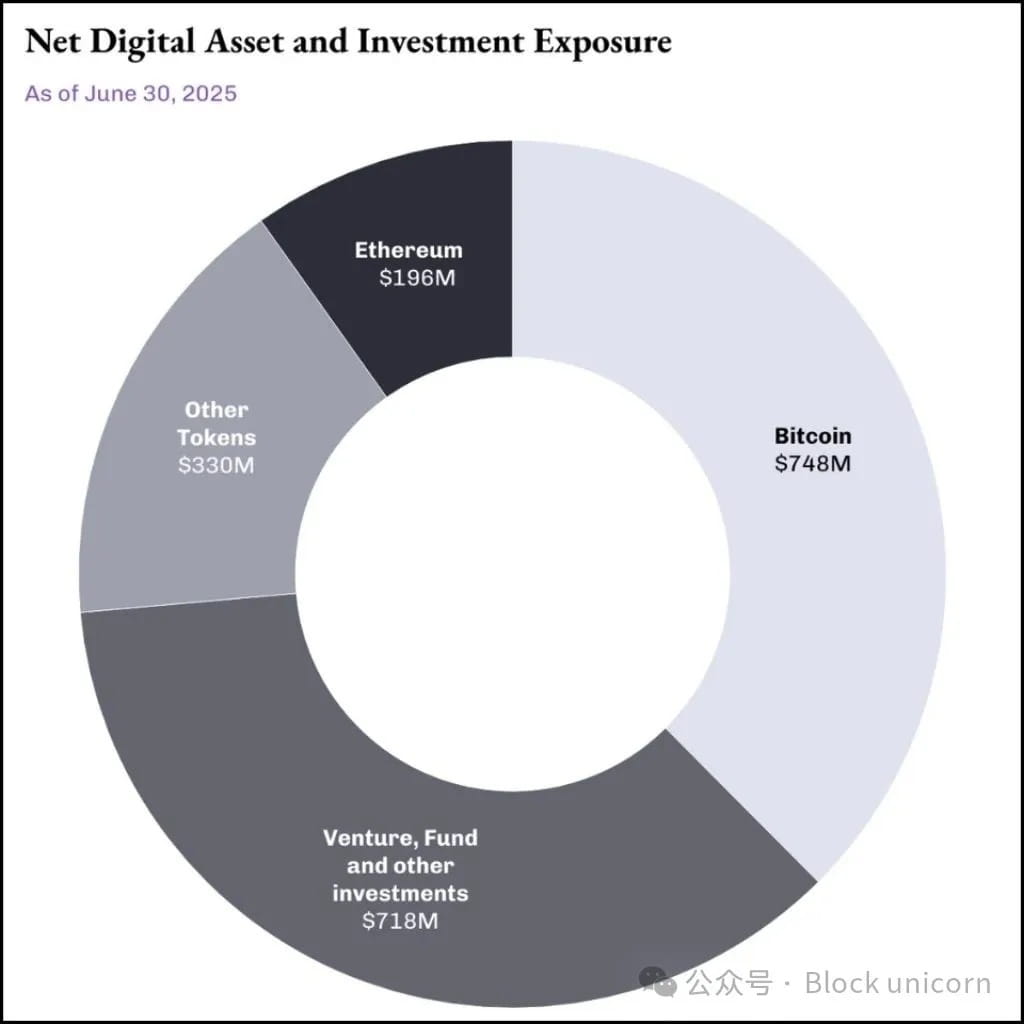

Its $2 billion asset pool serves as an investment tool, even acting as a strategic funding source under favorable market conditions.

The division generated $198 million in revenue without accounting for non-cash unrealized earnings. Unlike purely cryptocurrency companies, Galaxy's asset business funds itself by strategically selling assets at opportune times.

This is precisely where I believe Galaxy's cryptocurrency asset strategy differs from Michael Saylor's Bitcoin asset strategy. Saylor's 'buy, hold but never sell' strategy realized $14 billion in unrealized gains this quarter. But these are just paper profits that Saylor's shareholders cannot benefit from.

Galaxy is different. It not only buys and holds cryptocurrencies in its asset pool but also engages in strategic sales, generating realized profits. This is real cash that shareholders can share.

However, I believe that Galaxy's asset division is an unreliable source of income. As long as the cryptocurrency market is in optimal condition, this division will continue to generate returns. But the market does not operate that way, whether in traditional or cryptocurrency markets. Markets are at best cyclical, making these returns severely dependent on the state of the cryptocurrency market.

This is why Galaxy needs its AI transformation to succeed, as the current model is unsustainable.

Market Opportunities

Galaxy has positioned itself at the intersection of two massive trends: explosive demand for AI computing and a long-term shortage of electricity infrastructure in the U.S. A McKinsey report shows that global data center demand is expected to quadruple from 55 gigawatts in 2023 to 219 gigawatts in 2030.

Hyperscale cloud service providers are projected to invest $800 billion in data centers as capital expenditures (CapEx) by 2028, an increase of 70% from 2025, but constrained by power supply.

Galaxy's advantage lies in its Helios campus in Texas, which has a potential capacity of 3.5 gigawatts, enough to supply electricity to over 700,000 homes in the state. 800 megawatts have already been approved, and an additional 2.7 gigawatts is under study by the Electric Reliability Council of Texas (ERCOT), giving Galaxy control over some of the largest available power capacities in the constrained AI infrastructure market.

Digital rendering of Galaxy's Helios AI and HPC data center campus located in Texas.

The foundation of Galaxy's transformation is a 15-year commitment made with CoreWeave, one of the largest AI infrastructure deals in the industry. CoreWeave has committed to providing 526 megawatts of critical IT capacity in three phases.

90% of the projected profit margin is attributed to the asset-light nature of data center operations after the infrastructure is built.

I see a significant risk in the CoreWeave transaction: execution. Just as I was contemplating the scale of funding Galaxy needs to raise, the planning and execution capabilities, this company cleared the first hurdle.

On August 16, Galaxy successfully completed $1.4 billion in project financing for the Helios data center, securing the necessary funds for the first phase of construction. This gives me more confidence in how to eliminate critical funding risks and validate the commercial viability of the Helios project.

Cash Flow Equation

Galaxy's current cash flow exposes the instability of its trading business while highlighting why AI infrastructure can provide true financial stability.

At the end of the second quarter, the company had $1.18 billion in cash and stablecoins, which sounds like a lot, but the reality is more complex. Galaxy's trading business operates on a capital-intensive model, and margin loans require substantial cash reserves. Most of the $1.18 billion is not freely usable.

The free cash flow generated by Galaxy is minimal. After paying $14.2 million in interest expenses and ongoing operational costs, the core business is barely breaking even in cash.

This forces Galaxy to rely on the appreciation of the cryptocurrency market, namely its treasury and mining operations, to generate funds to support operations amid inherent cyclicality and unpredictability. In contrast, CoreWeave's three-phase contract structure and high-margin business characteristics could immediately generate positive cash flow.

While the profit margin may not be as high as 90%, even a more conservative profit margin of 40-50% would still be more reliable and stable than the cyclical treasury business.

Unlike trading operations that require continuous investment in working capital and technological infrastructure, cash generated from data center operations can be reinvested into expansion or returned to shareholders.

Galaxy's recent Helios project financing has helped address cash flow issues. By obtaining dedicated construction funding, Galaxy separates infrastructure development from its operational cash flow needs. This was not achievable during the expansion of trading operations, as the balance sheet capital required for trading expansion would directly compete with other business needs.

Expense Details

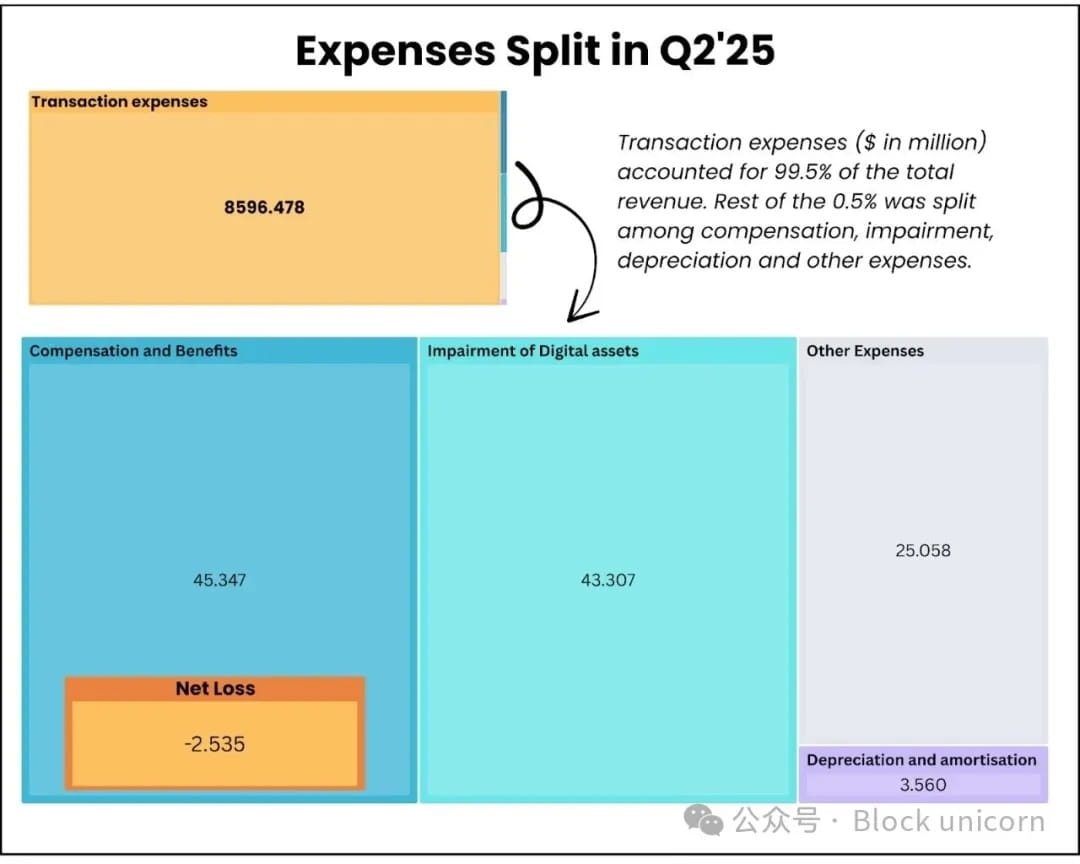

The total expenses of the digital assets division amount to $8.714 billion, with trading fees accounting for the largest share ($8.596 billion). These fees are purely pass-through costs, with almost no room for increase. Galaxy can hardly optimize these costs, as the spread in commoditized trading businesses continues to shrink, making these costs unavoidable.

More concerning is that quarterly compensation expenses include $18.8 million in stock compensation, which must be paid in cash. This means that Galaxy's costs to retain talent exceeded the earnings generated by its core business ($13 million).

The transformation to AI infrastructure will change the situation. Once the facilities are operational, the data center's operations require minimal variable costs.

To illustrate more intuitively, Galaxy's entire digital asset business generated $71.4 million in adjusted gross profit in the second quarter. At full capacity, just the first and second phases of Helios (approximately 400 megawatts) could generate $180 million in quarterly revenue, with operational complexity and costs being only a fraction of those of trading operations.

Market Response

Galaxy's stock price rose slightly by 5% within 24 hours of announcing its second-quarter financial report and jumped about 17% within a week, before investors began to withdraw.

This may be because investors realize that $180 million of the $211 million earnings came from non-cash adjustments and treasury earnings, rather than operational improvements.

Investors may not have fully considered the complex transformation of Galaxy towards AI infrastructure, as significant data center revenue is not expected until after the first half of 2026.

I remain optimistic about long-term market sentiment, given the potential for future developments.

According to ERCOT research, the addition of 2.7 gigawatts capacity by Galaxy indicates that the company intends to solidify its position as a long-term infrastructure provider rather than a single-tenant facility operator.

With comprehensive development, Galaxy's operations in Texas can rival some of the largest hyperscale data center campuses operated by Amazon, Microsoft, and Google. This scale can provide it with leverage in negotiations with other AI companies while improving operational efficiency and thus enhancing profit margins.

The company's expertise in cryptocurrency provides it with a unique positioning in the emerging intersection of AI and blockchain technology.

Path Forward

Galaxy is making a huge, polarized bet. If the AI infrastructure transformation is successful, they will transition from a low-margin trading company to a cash-generating machine. If they fail, they will have spent billions on expensive real estate in Texas while their core business gradually declines.

$1.4 billion in project financing confirms external confidence, but I'm watching two key indicators: can they truly deliver 133 megawatts of AI-ready capacity before the first half of 2026? Once they start incurring actual operating costs, can that 90% profit margin be maintained?

Current operations provide enough cash flow to sustain the business, but strong performance in the cryptocurrency market is needed for meaningful growth investments. The AI infrastructure opportunity promises ongoing and reliable revenue potential, with its success completely dependent on execution in the next 18-24 months.

The recent project financing has eliminated significant execution risks, but Galaxy must now prove they can successfully transform cryptocurrency mining infrastructure into enterprise-level AI computing facilities to attract long-term investor bets.