1. Protocol Logic: From 'Fragmented Interest Rates' to 'Risk-Free Curve'

The original intention of Treehouse is not merely to create a new liquid staking token, but to address the infrastructure gap in the on-chain interest rate system.

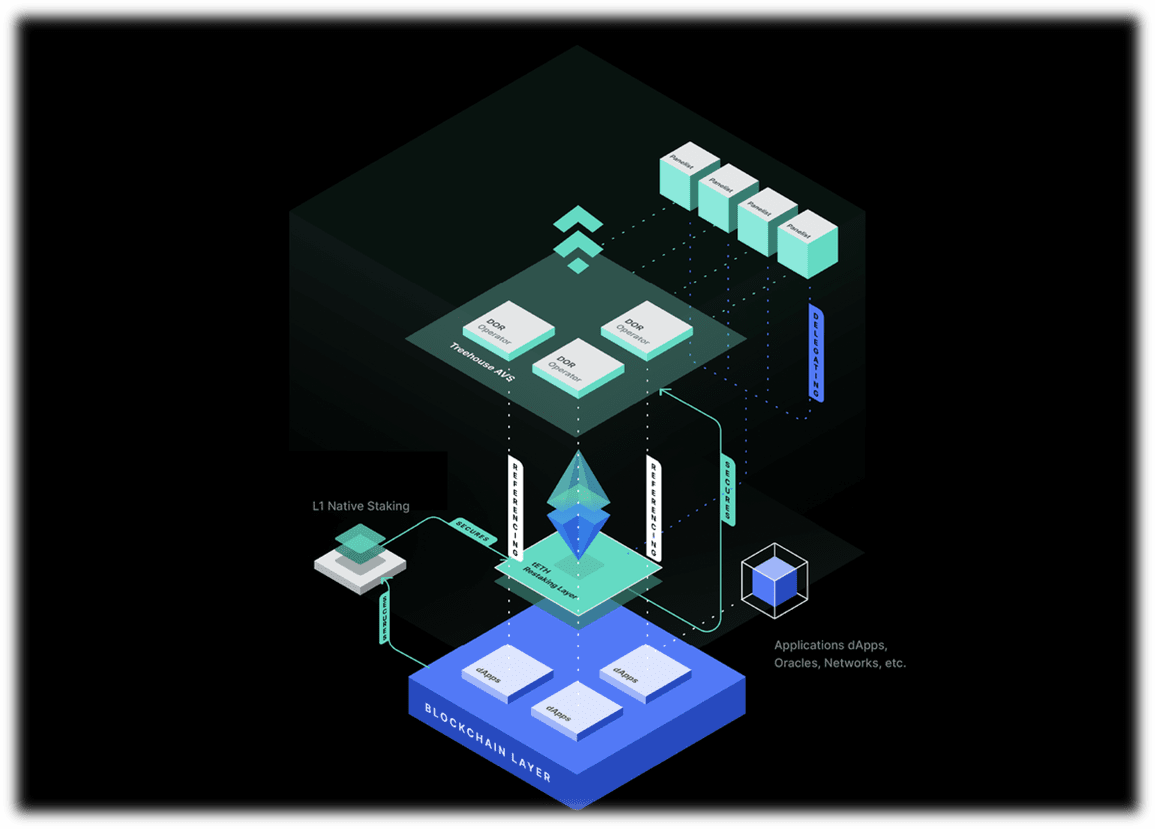

tAssets (represented by tETH) are not just 'LST 2.0'; they are designed to be more like an 'interest rate convergence tool.' By arbitraging between different lending protocols, tETH integrates the fragmented on-chain ETH interest rates into a more representative yield curve.

DOR (Decentralized Quoted Interest Rate) is a more macro step. It standardizes on-chain interest rates, attempting to build a crypto version of benchmark rates similar to LIBOR and SOFR in traditional finance.

This logic positions Treehouse more like the 'settlement layer' of DeFi fixed income: all yield-bearing derivatives (swaps, FRAs, fixed lending) on the protocol can be priced against DOR. In other words, Treehouse is not 'issuing a coin,' but 'reconstructing the interest rate infrastructure.'

2. Token Functions: Dual Binding of Utility and Governance

TREE does not follow the old path of 'pure governance tokens' or 'simple fee tokens,' but binds the token value forcefully to protocol security and ecological development through a multi-layer binding mechanism:

Query fees: Referencers must pay query fees in TREE, which means that protocol data liquidity = token demand.

Staking Requirement: Panel members must stake TREE before submitting interest rate predictions, and incorrect predictions will be penalized. This gives TREE both the function of insurance collateral and a system safety valve.

Consensus Rewards: Panel members and delegates with accurate predictions will receive TREE rewards, creating a closed-loop between the incentive mechanism and the secondary market value of the token.

DAO Bonus: A portion of TREE's issuance directly flows to ecological developers, forming a positive cycle of 'token as an incubation fund.'

This mechanism makes TREE's value logic different from most LST projects: it does not rely solely on secondary market speculation but is bound to the 'usage rate' of the DeFi ecosystem.

3. Market Positioning: DeFi's 'Interest Rate Clearinghouse'

Currently, there are three pain points in the DeFi interest rate market:

Fragmented interest rates across protocols, lacking a unified benchmark;

Lack of a transparent and manipulation-resistant forward interest rate system;

Development of fixed-income products is limited, mostly 'floating lending + simple hedging.'

Treehouse's entry point is equivalent to building an 'interest rate clearinghouse' on-chain:

tETH: Provides true yield rate products, enhancing user-side attractiveness;

DOR: Provides standardized interest rate benchmarks, serving institutional clients and derivative designers.

If Lido solves 'how to stake more efficiently,' then Treehouse aims to address 'how to make staking interest rates the fundamental pricing tool in the market.' This means that Treehouse's target clients are not only retail users but also DeFi protocols, institutional funds, and CeFi platforms.

4. Potential Risks and Challenges

Centralization issue of panel members: Initially, only whitelist members can participate in interest rate predictions, which ensures data quality in the short term but may lead to 'de facto centralization' in the long term.

Sustainability of yield arbitrage: The excess yield from tETH mainly comes from interest rate arbitrage, but if the market gradually approaches equilibrium, and arbitrage space shrinks, the attractiveness of tAssets may diminish.

Regulatory gray area: If DOR, as an on-chain interest rate benchmark, is regarded as a 'financial benchmark' by future financial regulatory agencies, its compliance may become a new risk point.

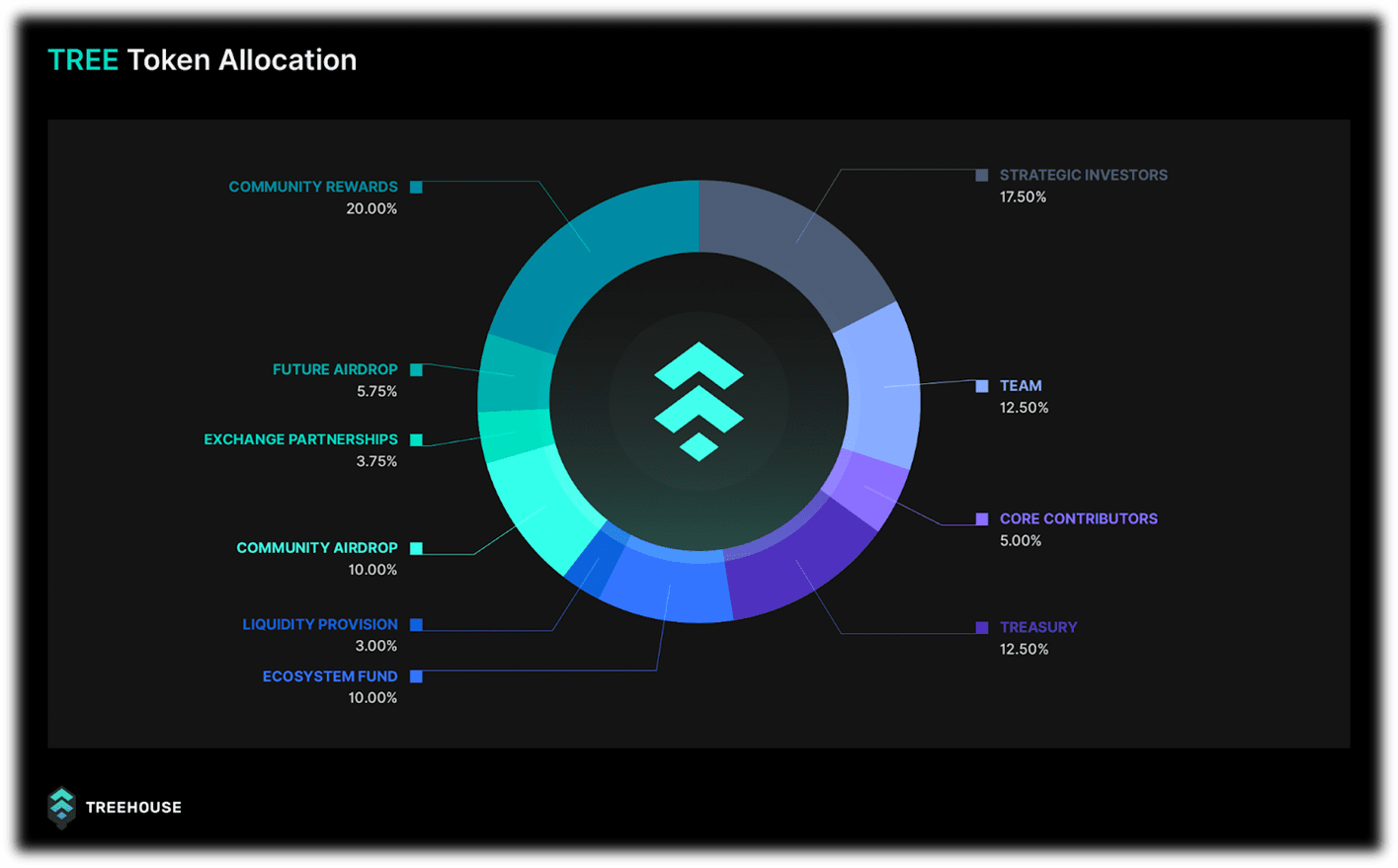

Token release pressure: The unlocking period for the team and investors is relatively reasonable, but in times of insufficient market liquidity, it may amplify price volatility.

5. Investment Logic of TREE

The uniqueness of the TREE token is that it is not merely a 'governance token' or a 'fee token,' but a 'value capture point' within the on-chain fixed income system. Its value depends on:

Whether tETH can truly integrate on-chain interest rates and serve as a proxy for the 'ETH risk-free curve';

Whether DOR can be widely adopted and become the pricing anchor for DeFi fixed-income products.

In other words, the long-term value of TREE does not depend on a single track but on whether it can establish an irreplaceable position in the DeFi interest rate system. If successful, it will become the 'yield curve of U.S. Treasury bonds' for on-chain fixed income; if it fails, it may remain 'just another LST derivative project.'