In today's rapidly evolving digital asset landscape, the cryptocurrency fixed income market presents two distinctly different development paths: centralized finance and decentralized finance. These two models each have their own characteristics, competing and complementing each other, together forming a complete picture of the current cryptocurrency fixed income ecosystem.

The centralized finance fixed income model largely continues the practices of traditional finance, relying on a foundation of established legal precedents. In this system, market makers, credit books, or hedge funds participate in inter-project lending activities through legal agreements. This model encompasses a variety of tools, including simple margin lending on centralized exchanges and over-the-counter agreements between counterparties.

Currently, most cryptocurrency centralized fixed income trades are essentially bilateral in nature, characterized by a low degree of pricing standardization. This setup is reminiscent of the ancient Mesopotamian market discussed earlier, where the interest rates negotiated between parties followed a simple pattern: 'willing buyer (borrower), willing seller (lender)'.

It is worth noting that many cryptocurrency fixed income instruments possess characteristics of both models. Taking Maple Finance as an example, it adopts a so-called 'CeDeFi' hybrid model, which primarily relies on traditional legal contracts and terms beneath the blockchain surface. Although it operates on the blockchain, these protocols essentially follow the same legal framework as traditional corporate bonds. When defaults occur, as in the case of Orthogonal Trading failing to repay unsecured loans at the end of 2022, Maple still needs to seek recovery through traditional off-chain methods, including legal recourse.

In contrast, decentralized finance fixed income instruments primarily operate on-chain, with smart contracts defining algorithms based on the interaction between loan demand and funding supply. Overall, this sub-market exists in a limited and fragmented manner, with most tools restricted to simple agreements that can facilitate efficiency similar to centralized finance or traditional finance. Before strong market conventions are established, the adoption of more complex on-chain credit systems (such as unsecured and under-collateralized loans) remains a distant prospect.

Currently, the decentralized finance fixed income space is primarily dominated by two models: the collateralized debt position platforms represented by MakerDAO and the lending protocols represented by AAVE. These platforms adopt an over-collateralization model, with smart contracts serving as decentralized clearinghouses. When borrowers default, sufficient collateral held in the smart contracts can cover the lenders' losses, reflecting the historical evolution from trust-based credit systems to traditional finance's over-collateralization model.

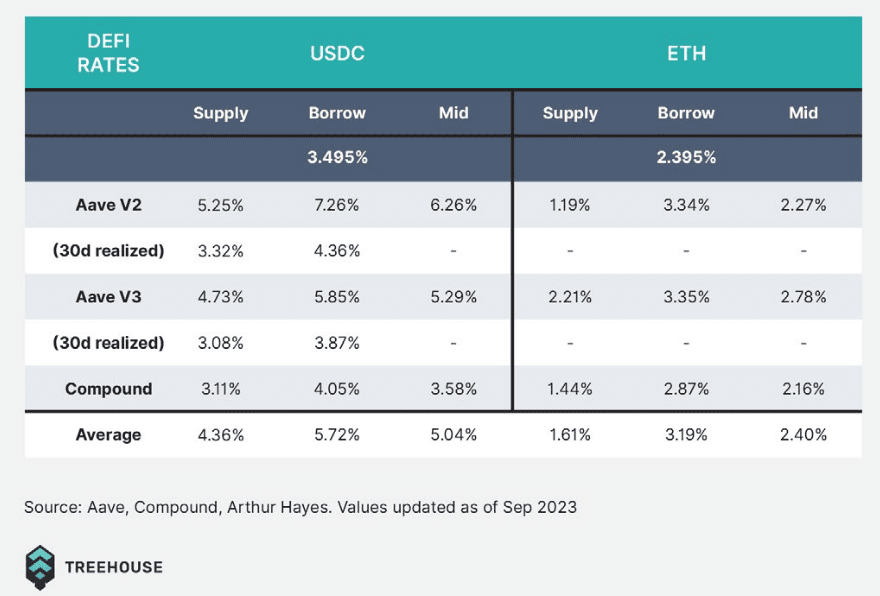

Taking the largest on-chain lending protocol AAVE as an example: as of May 2024, the annual yield for lenders of the most liquid asset ETH on this protocol is 1.74%, while borrowers bear a variable annual interest rate of 2.55%, meaning the midpoint interest rate for ETH is 2.145%.

This stands in stark contrast to traditional finance fixed income, where the most liquid U.S. Treasury bond bid-ask spreads can be precise to 1/128 of a basis point. Among different lending protocols, there are significant rate differences for the same asset, and this decentralized pricing reflects the lack of market standardization.

In mature financial markets, capital flows typically start from 'risk-free' and interest-bearing assets and then migrate to higher beta instruments. However, the adoption of decentralized finance fixed income is structurally quite the opposite, with retail investors rushing to the tail end of higher beta instruments first.

In addition to the two main categories mentioned above, there are also other decentralized finance fixed income solutions. For example, Pendle Finance pioneered a principal and interest separation trading model in decentralized finance, similar to the models used in mortgage-backed securities and U.S. Treasury bonds. Protocols like Exactly, Notional, and Yield also have considerable total locked value. However, due to the lack of standards or conventions between protocols, liquidity remains fragmented on these platforms, resulting in significant price discrepancies, wide bid-ask spreads, and high slippage issues.

Compared to traditional finance, individual corporate issuers can now launch bond issuances equivalent to the total locked value of the entire cryptocurrency fixed income industry, indicating that there is still significant growth potential in cryptocurrency fixed income. However, considering that this field has already caught up with traditional fixed income in many aspects despite the lack of infrastructure, its progress is noteworthy.

The trajectory of market development indicates that both centralized and decentralized models have their advantages. The centralized model has advantages in compliance, institutional participation, and complex product design, while the decentralized model excels in transparency, permissionlessness, and global accessibility. In the future, these two models may further merge to form a more complete and diversified ecosystem.

With ongoing technological advancements and an increasingly clear regulatory environment, the cryptocurrency fixed income market is at an important development juncture. Increased standardization, improved liquidity, and the entry of institutional investors will bring new vitality and opportunities to this market. In this transformative era, platforms that can effectively integrate the advantages of both models and provide quality services to investors will stand out.

It is in such a market environment that #Treehouse and $TREE

With its innovative technical architecture and profound market insights, it provides investors with a bridge connecting the centralized and decentralized financial worlds, opening a new chapter in cryptocurrency fixed income investment.