Author: @agintender

Original link: https://x.com/agintender/status/1955114555685949613?t=8Bj6c7MFn825eboqmSB-iQ&s=19

Disclaimer: This article is a reprint. Readers can obtain more information through the original link. If the author has any objections to the reprint format, please contact us, and we will modify it according to the author's request. Reprinting is for information sharing only and does not constitute any investment advice or represent the views and positions of Wu's statement.

The true nature of perpetual contracts does not reveal itself in its smooth operation but becomes glaringly obvious when it is under extreme pressure and on the brink of collapse. The abnormal events surrounding the Alpaca Finance ($ALPACA) perpetual contract after its announcement of delisting serve as an excellent case study to reveal this nature of 'short squeezing.'

'Short squeeze' is a classic financial hunting game that merges market structure, capital leverage, and group psychology into a violent art. The bloodshed and violence attract a group of clueless spectators.

Traditional market logic holds that an exchange delisting is a strong bearish signal that will inevitably lead to a crash in asset prices, as its liquidity will be stripped away and trading channels closed. However, in the ALPACA incident, a major bearish fundamental announcement triggered an explosive price surge of thousands of percentage points. The driving force behind this anomaly did not stem from any improvement in the project's fundamentals but was entirely dominated by the unique mechanisms of its perpetual contract market.

This 'perpetual contract paradox'—where a negative catalyst triggers an extreme positive price reaction—means that the perpetual contract itself is both the stage of this game and the weapon of the game, creating a market reality completely independent of the project's health or future prospects.

Here, it is the mechanism of the tool that determines the outcome, not the intrinsic value of the asset;

Here, perpetual contracts are not a place for price discovery, and the funding rate is not a tool for regulating the market's game but a 'weapon' for harvesting retail investors.

Reading Guide: For friends who are unfamiliar with the background and factors of the Alpaca incident, it is recommended to start from Part One; for those who want to understand the specific operational methods of Alpaca, it is recommended to start from Part Four; for those who have previously read long articles about Alpaca (https://x.com/agintender/status/1954160744678699396), it is recommended to start from Part Five.

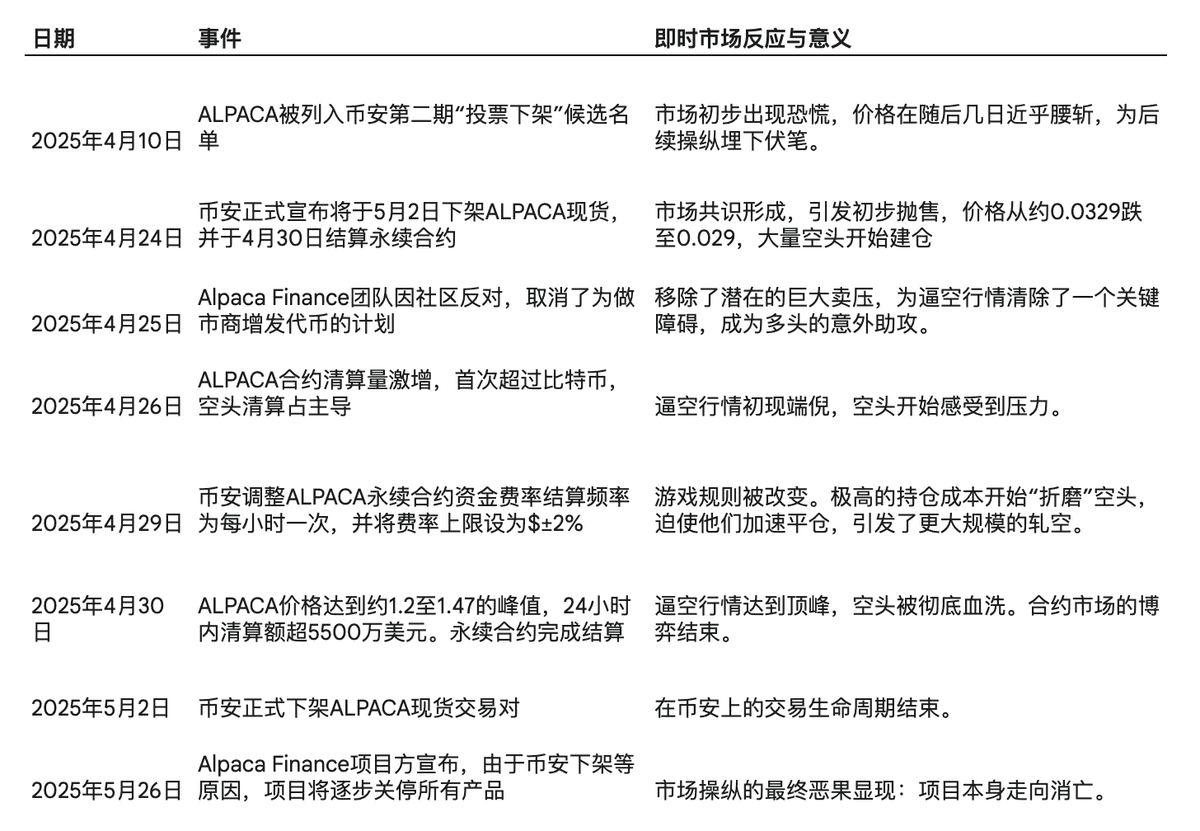

A brief review of the timeline:

1. Timing: The Weaponized 'Zeroing Consensus' In any meticulously planned battle, timing is everything. For the manipulators of ALPACA, the best 'timing' was not a breakthrough of a technical indicator but an impeccable psychological consensus crafted by the world's top exchange, Binance.

Catalyst: The 'Oracle' Effect of the Delisting Announcement

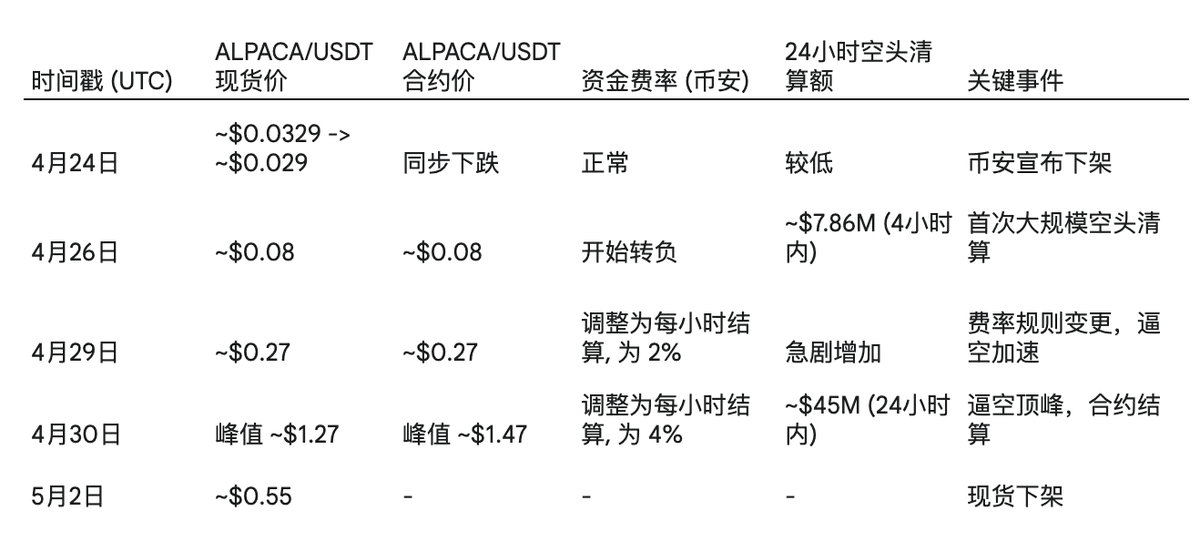

On April 24, 2025, Binance officially announced that it would delist the ALPACA spot trading pair on May 2 and settle its perpetual contract on April 30. In the crypto world, Binance's announcements are almost equivalent to 'oracles.' A 'delisting order' is, in the minds of most traders, tantamount to sentencing a project to death.

This recognition quickly formed a simple, clear, and highly tempting logic chain: delisting → liquidity exhaustion → loss of trading value → price must return to zero. This mindset of 'must return to zero' spread through the market like a virus, rapidly unifying the expectations of almost all retail investors. For them, shorting a token about to be abandoned by Binance was no longer a high-risk speculation but a 'sure-win' arbitrage opportunity.

Hunting Ground Construction: The Crowded Short Trap

This strong psychological consensus directly translated into market behavior: an extremely crowded, highly leveraged, and behaviorally uniform short camp quickly formed. Data shows that after the announcement, the open interest of short positions in the ALPACA perpetual contract surged dramatically. The market had dug itself a perfect 'short trap.'

A tweet on April 25 about 'the need to issue more tokens as market makers' pushed this 'shorting' sentiment to the extreme. With the precedent of the Gifto incident, the market expected that this 'issuance' behavior might accelerate the delisting timeline. Although this 'issuance' event was not specifically implemented, it was nonetheless a successful 'catalyst.'

The manipulators/big players understood all of this. They did not see a failed project but a liquidity-rich fuel depot composed of countless future 'forced buyers' (shorts forced to close their positions). They did not need to create panic, but rather patiently waited for the panic to ferment to its peak, allowing as many shorts as possible to enter this carefully arranged hunting ground. The 'timing' created by authoritative announcements provided the perfect stage for subsequent harvesting actions.

2. Location: The Hidden Battlefield Rules

If 'timing' is the victory of psychological warfare, then 'location' is the ultimate exploitation of the microstructure and trading rules of the market. The manipulators cleverly chose two battlefields—the spot market and the perpetual contract market—and two messages—delisting and issuance—and leveraged 'extremely negative news' to turn the funding rate mechanism of the perpetual contract market into a tool for harvesting retail investors.

Fulcrum: The Low Market Cap Spot Market

The core strategy of the ALPACA incident was to exploit the structural weaknesses of its spot market. At the time of the incident, its circulating market cap had shrunk to only about $5 million. This meant that manipulators could create drastic price fluctuations with relatively little capital in the spot market, thereby impacting the much larger, highly leveraged derivatives market. The spot price became the 'price anchor' of this long-short battle.

Torture: The Funding Rate as a Financial Weapon

Perpetual contracts use the 'funding rate' mechanism to anchor their prices to spot prices. Typically, when bearish sentiment is strong and contract prices are below spot prices, the funding rate is negative, requiring shorts to pay fees to longs.

In this game, a key move by Binance on April 29 completely changed the rules of the game. The exchange announced that the funding rate settlement frequency for the ALPACA perpetual contract would change from the usual once every 8 hours to 4 hours/2 hours, finally adjusting to once every hour, and setting the rate ceiling to an astonishing '±2%'. (On the 30th, it was changed to ±4%)

The destructive power of this adjustment was devastating. It meant that:

Short position holders need to pay a 'holding cost' of ±2%/4% for every hour they hold their position.

The cost of holding a short position for one day can reach 48%/96%.

At this moment, the funding rate is no longer a transaction cost but an unbearable financial 'torture tool.' It sets a ticking 'death countdown' for all short positions, forcing them to choose between liquidation and paying exorbitant fees, with the only rational choice ultimately being surrender—buying to close. (Part Four will explain in detail)

3. Human Harmony: The Predicted Opponent

If timing and location are the manipulators' leverage and use of force, then the success of 'human harmony' comes from the precise anticipation and exploitation of the psychology and behavioral paradigms of the other party in the game—the retail investor group.

The Script of the Manipulators vs. The Paradigm of Retail Investors

Since the second half of 2024, a mental model has emerged in the market: 'Exchange announcements (whether adding or delisting = bearish = short).' The fatal flaw of this primary thinking is that it completely ignores the microstructure of the market, the extreme changes in trading mechanisms, and the existence of counterparties.

In contrast, the manipulators' script is multi-dimensional and multi-layered:

Accumulation Phase: Quietly accumulating a large amount of spot chips during market panic and price depression (around $0.03). (There are market rumors that ALPACA had previously completed a 'shell change.')

Luring Phase: Utilizing official announcements to fully ferment the 'zeroing narrative,' enticing massive short positions to enter the market and building a liquidity-rich opponent.

Attack Phase: When short positions are most crowded and the funding rate rules are most favorable to them, triggering the liquidation engine of the derivatives market by pulling up the spot price.

Exit Phase: When the short squeeze reaches its peak and market sentiment turns to FOMO, selling the accumulated spot chips to chasing retail investors, completing the profit harvest and causing the price to collapse.

The Cognitive Blind Spots of Retail Investors

The harvesting of retail capital is rooted in several key cognitive blind spots:

Ignoring Structural Risks: Failing to Assess ALPACA as a low market cap, low liquidity token, whose spot price can easily be manipulated with a small amount of capital.

Underestimating Mechanism Weapons: Failing to see extreme negative funding rates and high-frequency settlements as a financial weapon, but merely viewing them as manageable holding costs.

Misreading Market Consensus: Viewing a one-sided bearish consensus as a definitive signal, especially the 'issuance' tweet on April 25, which pushed it to the forefront, without realizing that when trading in one direction becomes overly crowded, the risks have disproportionately tilted in the opposite direction.

Retail investors see a project on the verge of failure, while the manipulators see a market full of structural loopholes that can be exploited to harvest their opponents' positions. More tragically, the manipulators did not issue an invitation; rather, retail investors entered on their own.

4. The 'Death Knell' of 4% and Conservative Liquidation Strategies

Catalyst: How Binance's Funding Rate Adjustment Weaponized Time Decay

If the accumulation by whales and the market's bearish consensus is a masterpiece of timing, location, and human harmony, then the Binance exchange's adjustment of funding rate rules became the catalyst that ignited this explosion ('death knell'). On April 25, 2025, Binance announced that the funding rate settlement frequency for the ALPACAUSDT perpetual contract would change from the usual once every 8 hours to once every hour. Then, on April 30, the rate ceiling was further raised to ±4%.

The power of this rule change is enormous. As whales began to drive up the spot price, the price of perpetual contracts lagged due to short suppression, causing a significant discount of the contract price relative to the spot index price. This caused the funding rate to quickly turn deeply negative. When the funding rate reached -2% or even -4% per hour, it meant that short traders had to pay 2% to 4% of their position's value to the longs for every hour they held their position.

Theoretically, with a -4% funding rate, the cost of holding a short position for 24 hours could reach as high as 96% of its principal, not including any losses due to price fluctuations. This mechanism transforms the funding rate from a price anchoring tool into a punitive, time-based weapon.

Short traders faced a dilemma: either be forcibly liquidated due to rising prices or voluntarily close their positions due to unbearable holding costs. Time itself became the enemy of shorts, as the pressure to surrender came not just from prices but from unsustainable capital losses. The longs were in an extremely advantageous position, as they could profit from rising prices and continuously 'bleed' by collecting high funding rates paid by shorts.

Some say that Binance's setting of a 4% funding rate per hour is 'aiding and abetting'—on the contrary, Binance's action is a desperate measure.

From the exchange's perspective, the greatest fear is 'liquidation' due to extreme volatility, which not only disrupts market liquidity but may also cause losses to the exchange. Therefore, before a definitive 'delisting,' exchanges take various measures, such as moving the liquidation line forward (allowing positions to be taken over by the liquidation engine earlier), separating the insurance fund from the Alpaca trading pair, and adjusting the funding rate to encourage positions to 'retreat.' The goal is to minimize the exchange's open interest (OI) as much as possible before the delisting.

One can imagine that at the very moment before the delisting, when all orders disappear—who will take on these positions? From another perspective, a 4% rate per hour is also 'advising' the market against entering.

Unfortunately, this 'bloodthirsty' behavior not only failed to scare off the 'fishermen' but instead attracted more sharks.

5. Hunting Moment: Analysis of the Chain Reaction of Gradual Liquidation

With all actors and props in place, the market welcomed its final climax. From April 29 to April 30, in less than 24 hours, ALPACA's price exhibited a jaw-dropping parabolic trend. The price skyrocketed from a low of about $0.065 to a high of over $1.47, an increase of over 2,160%, in which case 'any margin position' would vanish into thin air.

The extreme price volatility is quantitatively reflected in the liquidation data. At its peak, the total liquidation amount of ALPACA contracts exceeded $55 million within 24 hours, with about $45 million coming from the liquidation of short positions. This figure even surpassed Bitcoin's liquidation amount in a short time, highlighting the severity of this short squeeze battle.

Ignition: The Ingeniously Designed Liquidation Waterfall

With the 'timing, location, and human harmony' in place, combined with the '4% catalyst,' the harvesting officially began. The process resembled a precision chain reaction, namely the core mechanism of 'short squeezing':

Pulling Up the Spot: The manipulators inject capital into the illiquid spot market, violently raising the price.

Contract Following: The price of perpetual contracts, as a shadow of the spot price, is forced to follow the rise.

Funding Rate Assistance: The funding rate acts as 'support', eating away at the 'maintenance margin' of empty positions at a rate of 2%/4% per hour (increasing holding costs).

Triggering Liquidation: The price surge first touches the forced liquidation line of the first batch of highly leveraged shorts (liquidation).

Vicious Cycle: The key is that the liquidation of short positions (liquidation) is essentially a forced market buy order. These forced buy orders further push up the contract prices, triggering more short positions with slightly lower leverage to be liquidated.

More Conservative Liquidation Strategies: The exchange, knowing that 'delisting' is imminent, will try to avoid 'liquidation' events as much as possible, which would affect the 'insurance fund', so more conservative liquidation strategies will be adopted (the liquidation line will be moved forward).

Waterfall Formation: Against the backdrop of the exchange implementing conservative strategies, this 'pull up → liquidation → buy → further pull up' cycle continuously reinforces itself, ultimately forming a spectacular liquidation waterfall, with prices showing vertical increases.

The table below records the key nodes of the ALPACA delisting short squeeze event based on public information, linking price, trading volume, liquidation data, and key events to visually present this 'magnificent' process.

6. The Delisting Coin Narrative Triggered by Short Squeezes

After the epic short squeeze, everything inevitably headed toward an end. With the final settlement of the perpetual contracts on April 30 and the delisting of the spot trading pair on May 2, ALPACA's price quickly collapsed, returning to its fundamentally determined value range.

By the end of May 2025, the project team officially announced that it would gradually shut down all operations by the end of the year. In the announcement, the team clearly stated that Binance's delisting was 'the last straw that broke the camel's back,' severely damaging market confidence, cutting off the token's liquidity and user acquisition channels, and forcing all potential new product development and acquisition plans to be halted. A project once highly regarded in the DeFi field thus came to a dismal end.

The price anomalies before the delisting were directly compared by many analysts to the ALPACA incident, proving that this 'delisting coin narrative' has become a recognized speculative strategy in the market. However, the demise of $ALPACA has given rise to a new and peculiar market narrative—the 'delisting coin concept.' This incident demonstrated to the market a possibility: a fundamentally dying token's perpetual contract market could explode with astonishing wealth effects due to structural imbalances. Inspired by this, some speculators began actively searching for tokens with small market caps and low liquidity, which fit the potential delisting characteristics across major exchanges, hoping to replicate ALPACA's short squeeze miracle. The price anomalies of $MEMEFI before its delisting were directly compared by many analysts to the ALPACA incident, proving that this 'delisting coin narrative' has become a recognized speculative strategy in the market.

This series of events reveals a core vulnerability in the perpetual contract market for low liquidity assets: its internal mechanisms can be manipulated to produce results that are completely contrary to fundamental logic. Delisting, which should signal the end of an asset's value, instead became a necessary prerequisite for triggering a brief but intense explosion in value. In an efficient liquidity market, the price of delisted assets should fall. However, the market size of ALPACA is extremely small (market cap around $5 million) and lacks liquidity.

This allows a determined actor to control spot prices with relatively little capital. By controlling the spot price, they can manipulate the price difference (basis) between spot and perpetual contracts, which in turn directly determines the direction and magnitude of the funding rate. The highly concentrated short positions in the market provided ample fuel for this fire, with whales controlling the spot price as the spark, and the exchange's funding rate rules acting as the accelerant. This illustrates that for certain specific assets, their perpetual contract market is no longer a place for price discovery but a self-contained battlefield full of game theory.

In this battlefield, the rules of the game are far more important than the value of the underlying asset.

Conclusion: A Perfect Hunt

The ALPACA 'delisting short squeeze' incident represents a capital hunt that utilized timing, location, and human harmony to the extreme. The manipulators leveraged authoritative information (timing) to create retail investors' mental models, exploited market structures and trading rules (location) to design an inescapable trap, and precisely utilized the group behavior of retail investors (human harmony) as fuel to ignite the trap.

The ironic conclusion of this game is that the speculative frenzy in the derivatives market ultimately became the last straw that broke Alpaca Finance itself. The project team clearly stated in the subsequent shutdown announcement that Binance's delisting and the subsequent price volatility 'seriously damaged market confidence' and forced all potential self-rescue plans to be halted.

For all market participants, the ALPACA incident serves as a brutal warning: In the dark forest of finance, what you trade is not just the asset itself, but also the game with all other players and the game rules. Those who cannot see the overall structural picture and act solely based on a single narrative and inertia are most likely to become prey from being hunters.

May we always hold a heart that reveres the market.

To know what is happening, and to know why it is happening.