Want to know why BTC has been continuously dropping this week? The main reason is the selling by whales holding 10K-100K BTC! ETH is rebounding but there are concerns about its chip structure. Altcoin sentiment is cooling but there is no panic. This article breaks down the fund flow of BTC/ETH, highlights in the altcoin market, and analyzes the key level of $113,230 to help you grasp the market situation.

1. Core Market Review This Week (8.16-8.22)

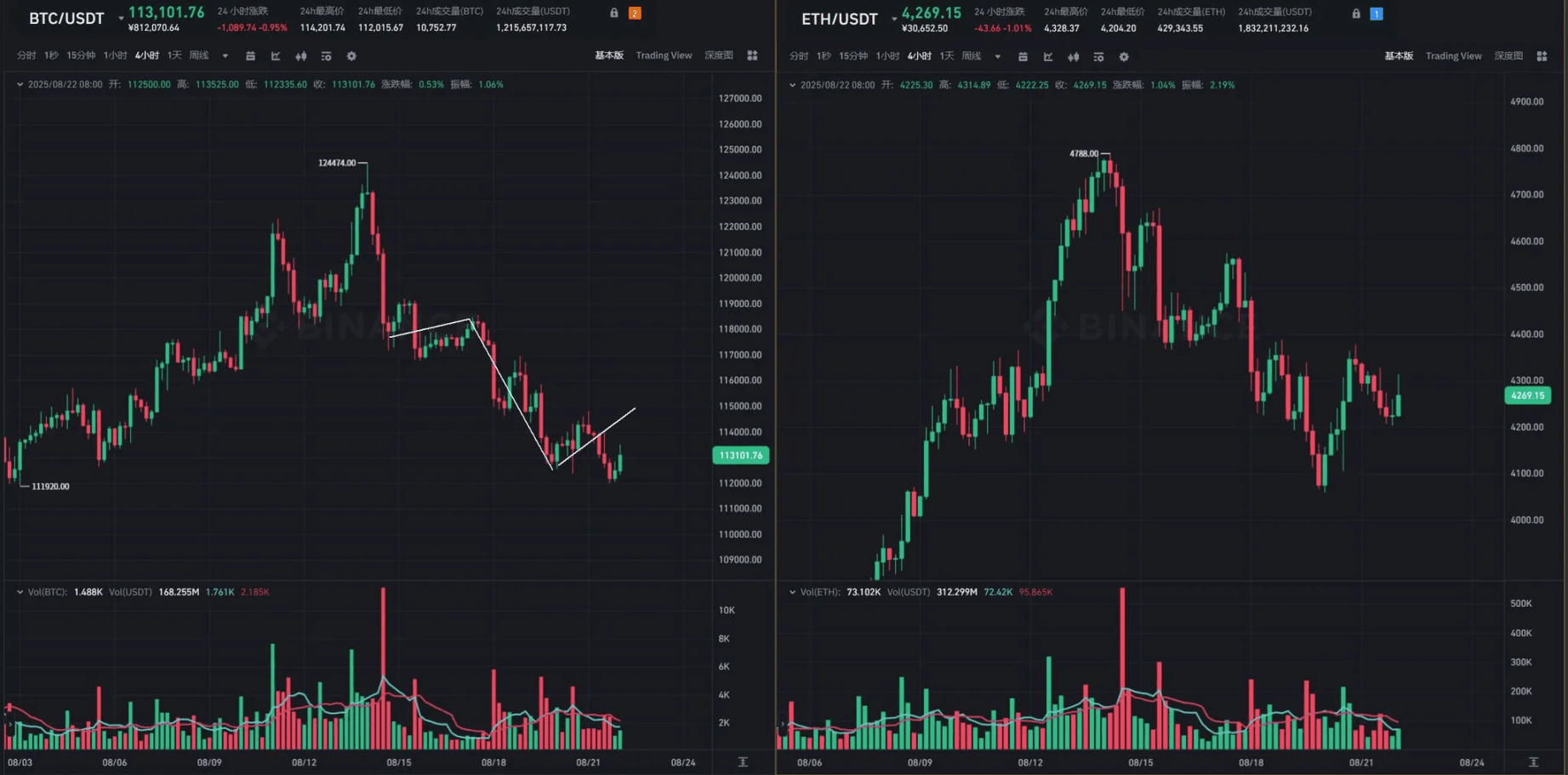

This week, the main theme of the crypto market revolves around 'BTC's weak decline and ETH's relative resilience', with the overall rhythm significantly influenced by US stock fluctuations and fund flows.

From BTC's trend, the entire week has shown a multi-segment downward pattern with continuously refreshing lows: After the decline last Thursday (8.14), although it entered a bullish rebound, the rebound strength was weak, encountering resistance and falling at $119,000; the adjustment level of the decline starting on the evening of the 17th was insufficient, leading to the four-hour rebound on the 18th and 19th not being sustained. On the evening of the 20th at 8 PM, the technical aspect was expected to initiate a four-hour to daily-level rebound, but was dragged down by US stocks, suddenly plunging around 9 PM, followed by continued low-level fluctuations.

ETH's performance is relatively bright, having recovered the last wave of decline, but affected by BTC's sluggish performance, it still faces potential pressure at $115,000 in the short term. Whether it can maintain strength needs to be observed based on the subsequent fund support.

2. Key Data for the Medium and Short Term: Fund flows reveal market signals

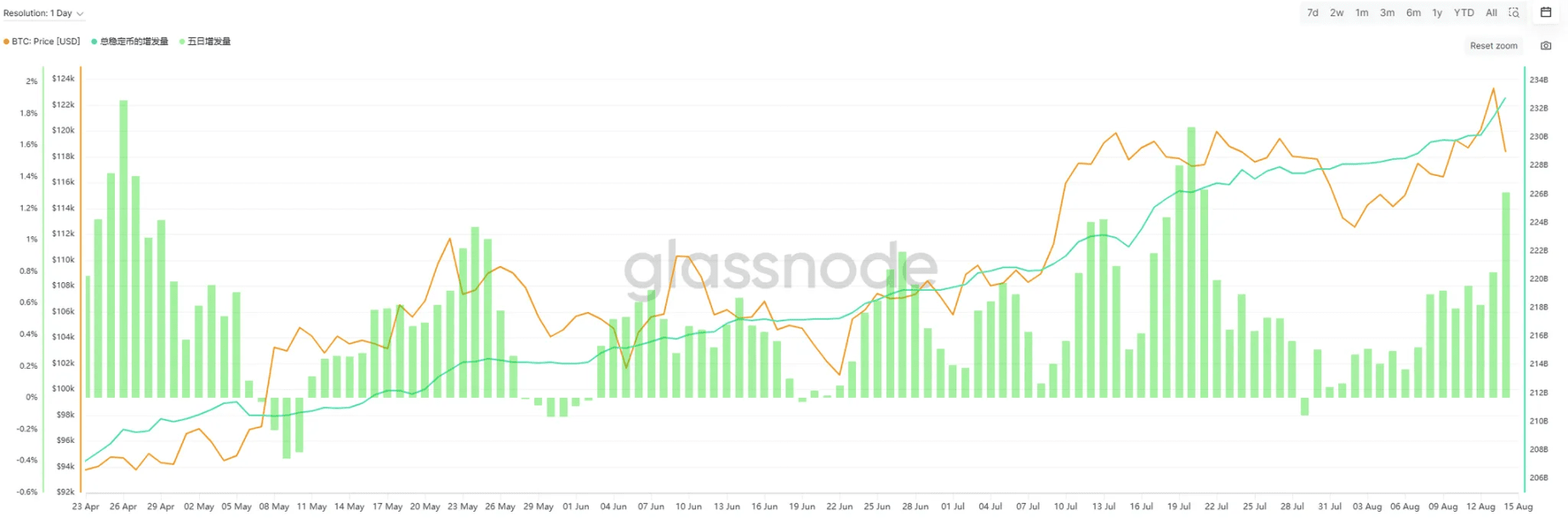

2.1 Stablecoins: Growth rate has significantly slowed, August 18 acts as a divide between bulls and bears

This week, the total scale of stablecoins reached $234.246 billion, but the inflow of funds has clearly cooled: the weekly issuance amount dropped from $3.958 billion last week to $1.442 billion, with the daily average issuance falling from $565 million to $206 million, a month-on-month decrease of 63%.

From the rhythm, August 18 is a key node: previously stablecoins showed a net inflow for a single day, but after the 18th, it turned into a continuous net outflow, which corresponds with the market's correction starting on the 18th. If the market wants to stabilize and stop falling, it is crucial to track when stablecoins will resume single-day net inflows — this is an important signal for the re-entry of off-market funds.

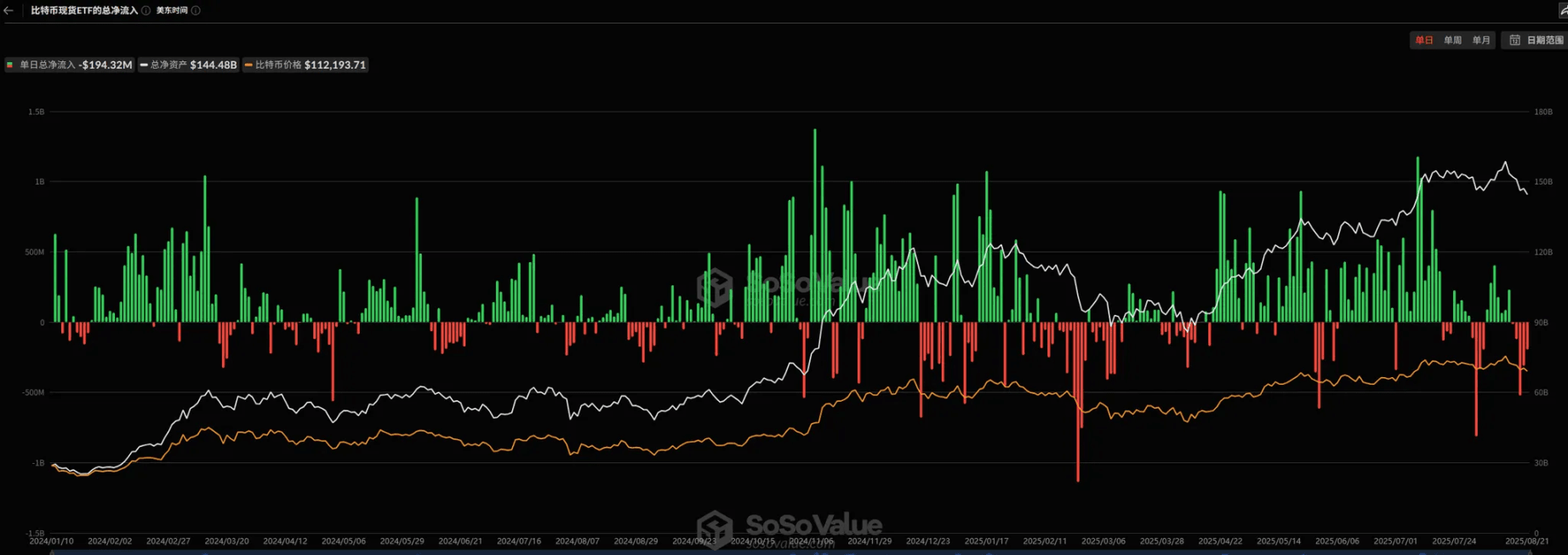

2.2 ETF Funds: BTC is experiencing severe blood loss, while ETH shows signs of recovery

BTC ETF: This week saw a net outflow of $1.165 billion, with daily net outflows throughout the week, setting a new recent outflow high. What is more concerning is that even as BTC prices continue to weaken, there are no signs of US stock investors or institutions bottom-fishing through ETFs, and ETF net inflows may become a 'precondition' for BTC to stop falling.

ETH ETF: Although it also recorded a net outflow of $638.22 million, the situation is better than BTC — on August 21, it resumed a single-day net inflow of $287.61 million, supporting the trend of ETH not making new lows after the rebound on the 20th. It is necessary to continuously track whether ETF funds can maintain net inflows.

2.3 Off-market Discount/Premium: Hidden bottom-fishing funds during the correction

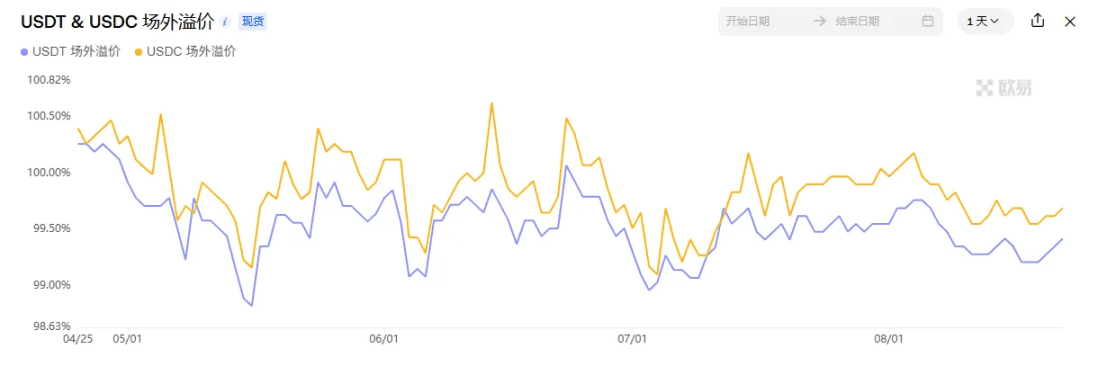

This week, the overall premium rate of USDT and USDC is in a fluctuating range, with no slight premium under the bullish FOMO sentiment, but starting from August 18, the premium rate has clearly turned upward, indicating that during the market correction, some off-market funds have quietly entered to bottom-fish, providing certain support for the market.

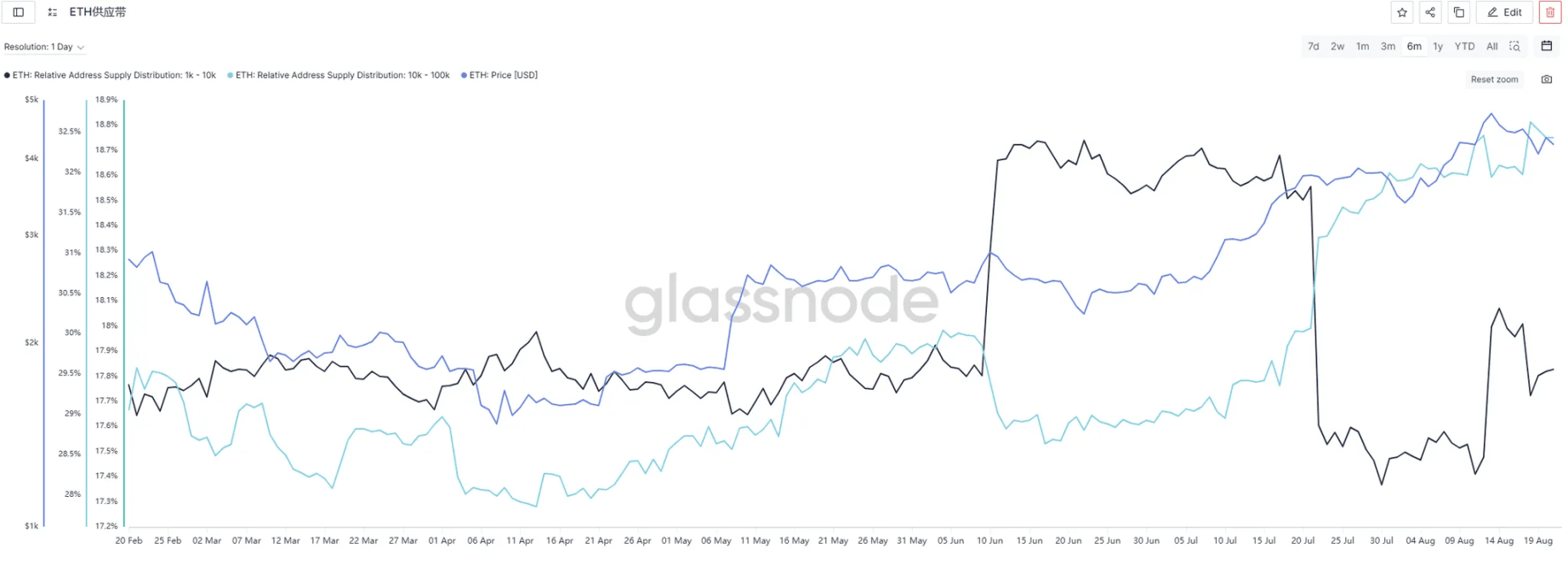

2.4 Ethereum Holding Addresses: Chip structure shows slight divergence

This week (8/16-8/22), from the perspective of addresses holding Ethereum, it can be observed that the proportion of holdings for addresses larger than 10K and smaller than 100K has shown a clear downward trend since August 18, and as of today, it has not regained an upward trend. However, Ethereum's price rebounded in advance on August 20, and considering the past year's trend, the price of Ethereum is highly correlated with the proportion of holdings for addresses between 10K and 100K. Thus, the rebound in Ethereum can be considered slightly diverging from the holdings proportion of addresses between 10K and 100K. Although when looking at the holdings proportion for addresses between 1K and 10K, it can be temporarily believed that this rebound was driven by these addresses, the correlation of the holdings proportion for addresses between 1K and 10K with Ethereum's price is not as strong as that of addresses between 10K and 100K. Therefore, continuous attention is needed.

3. Mid-term Data: Sources of BTC selling pressure and chip support levels

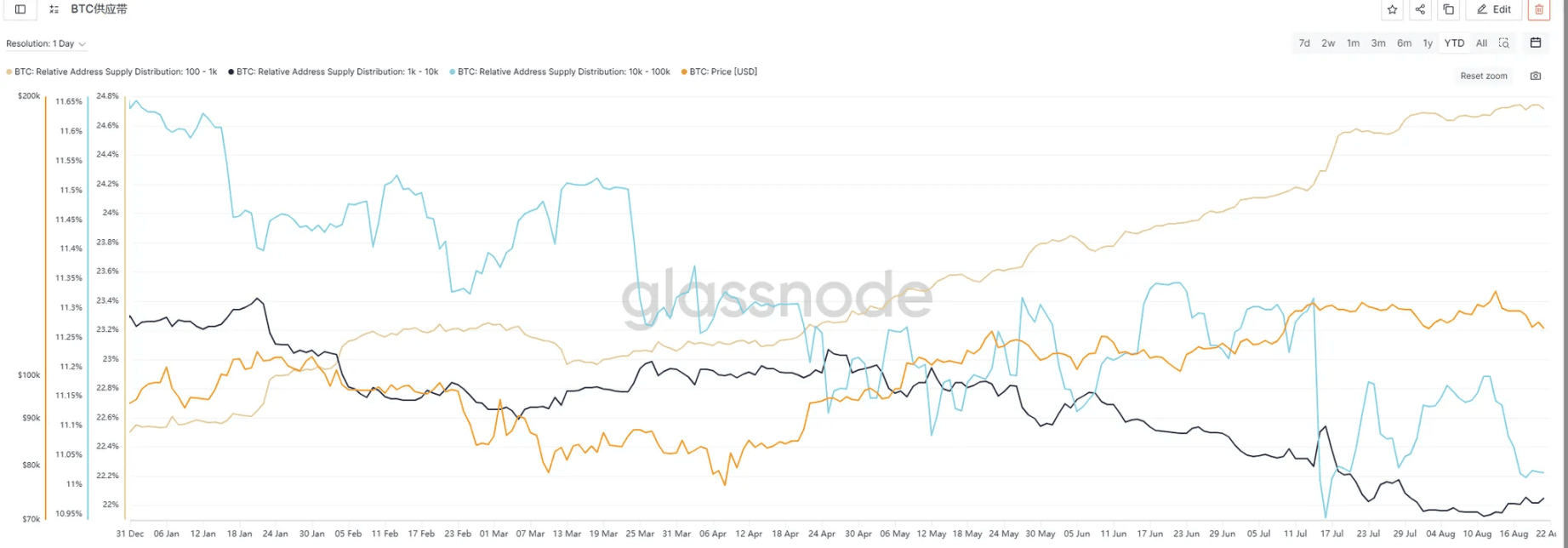

3.1 Holding Addresses: Whale selling pressure dominates BTC decline

This week, the performance of BTC addresses of different scales is diverging:

Addresses holding 100-1K BTC: The proportion of holdings is still on an upward trend, with no obvious turning point;

Addresses holding 1K-10K BTC: Stopped the previous downward trend, gradually leveling off or even slightly increasing, indicating that this group has stopped selling and started accumulating;

Addresses holding 10K-100K BTC: The proportion of holdings has significantly declined, and selling actions are evident — this is the core reason for BTC's continued weakness this week.

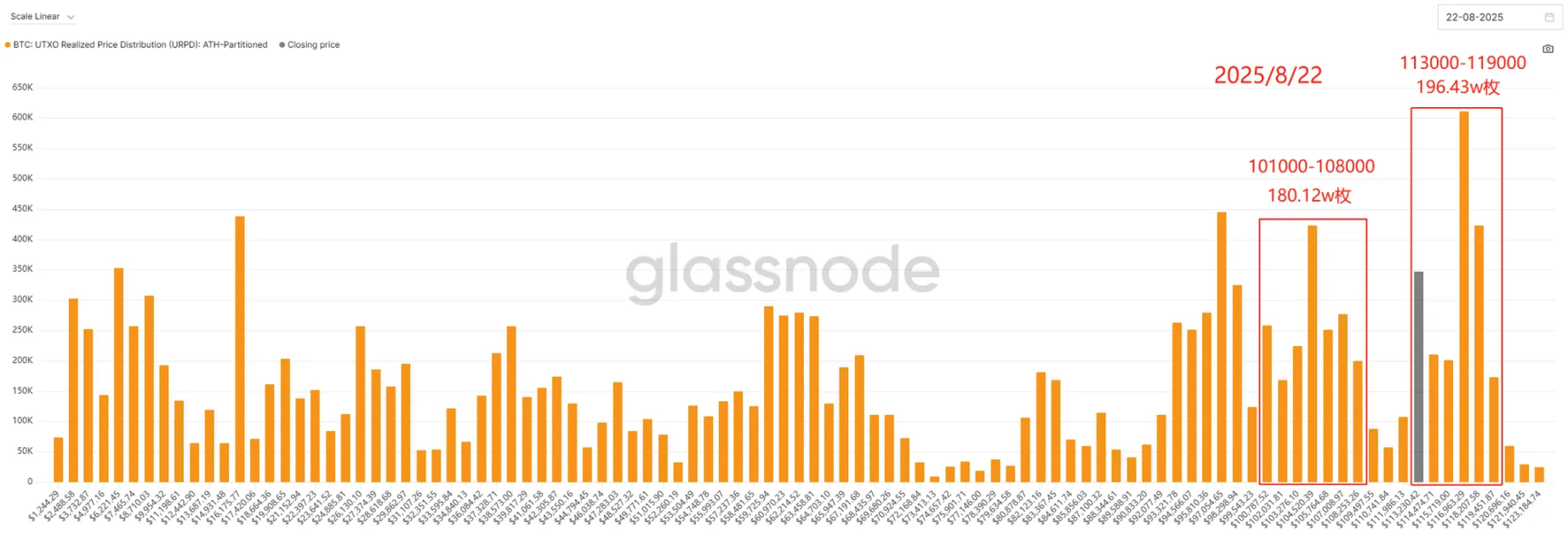

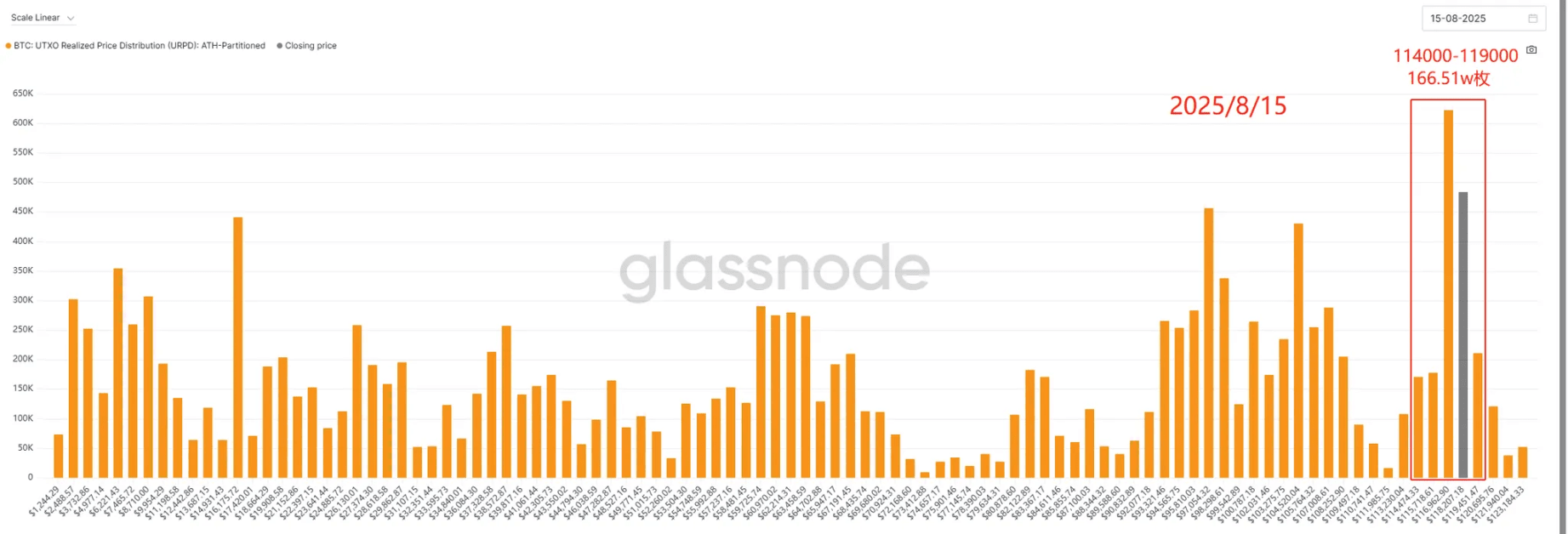

3.2 Chip Distribution: $113,230 as a Key Level

BTC's price this week filled the URPD gap near $112,000 from last week and found support at that position; at the same time, the chip concentration area between $114,000-$119,000 expanded to $113,000-$119,000, where approximately 340,000 BTC have accumulated near $113,230, which will become an important support or resistance level in the short term. The direction of breaking through/breaking down will affect the subsequent trend.

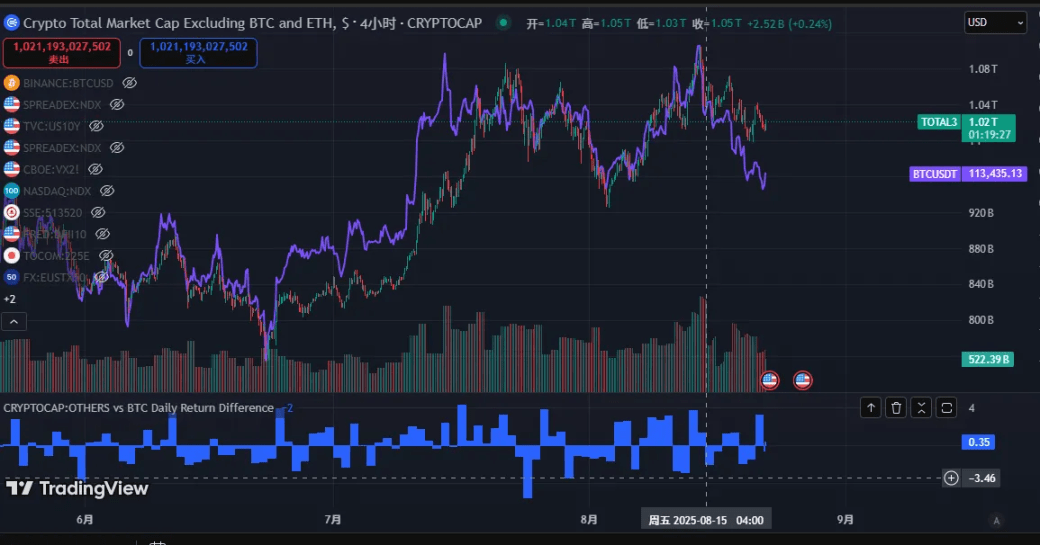

4. Altcoin Market: Sentiment cooling, local highlights cannot hide the overall weakness

4.1 Market Overview: Market value correction, no panic selling

Total market capitalization of altcoins (TOTAL2): This week at $1,020 billion, down 4% month-on-month, with the decline close to ETH's, and significantly less volatility compared to previous major market corrections;

Total on-chain TVL: $148.6 billion, down 4.1% month-on-month, consistent with the price decline, with no large-scale unlocking and selling; ETH staking amount is basically stable, indicating the market is in normal adjustment without panic sentiment;

Total market capitalization of stablecoins: $258 billion, up 0.8% month-on-month, with fiat-supported stablecoins showing a net inflow of $2.9 billion (month-on-month increase). The balance of stablecoins on exchanges has slightly declined, indicating that overall funds have not been significantly withdrawn.

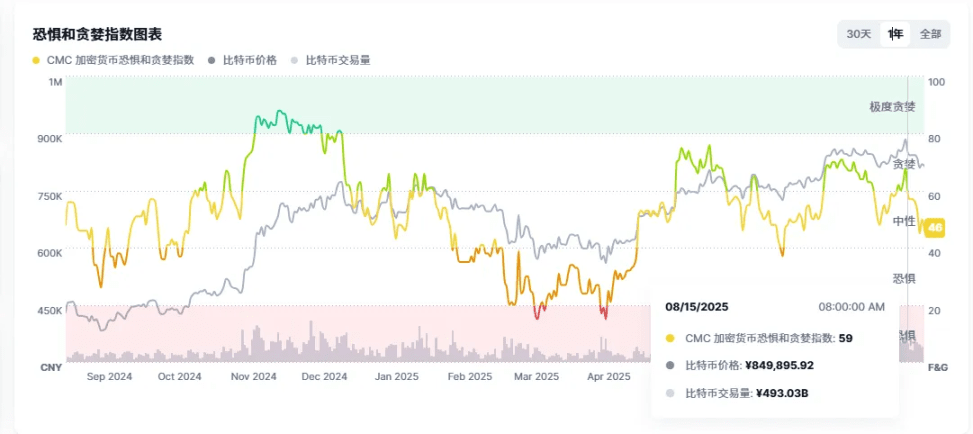

4.2 Sentiment and Heat: Rapid cooling, thin trading

Altcoin Index: Dropped from last week's high to 42, with increased volatility;

Market Sentiment Index: This week fell to 46, significantly cooling compared to last week;

Funding rates: Most altcoins show no significant fluctuations, and there was no large negative funding rate during the decline, indicating that bearish sentiment has not overly fermented.

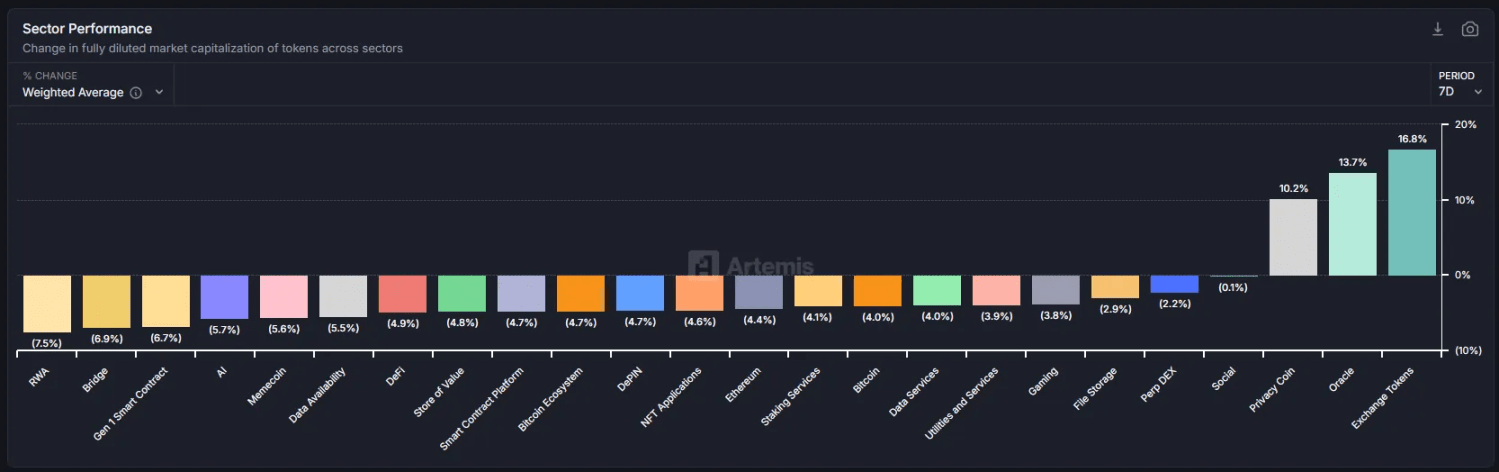

4.3 Secondary Market: Only a few targets are bright, with sectors largely declining

This week, only the exchange sector (OKB) and the database sector (LINK) rose against the trend, while other sectors fell across the board. Among them, OKB attracted market attention due to its high visibility and pump action, with trading volume briefly exceeding ETH, but such local highlights cannot drive the overall altcoin market — the vast majority of coins continue to follow the market trend and decline, and the exchange rates of SOL/BTC, ETH/BTC, BNB/BTC are basically flat, showing no signs of large-scale capital outflows.

4.4 Primary Market: Public chain TVL diverges, on-chain activity remains acceptable

TVL of the four major public chains: ETH chain fell by 5.95% this week, BSC chain grew by 4.16%, and SOL and BASE chains slightly declined, overall showing no significant contraction;

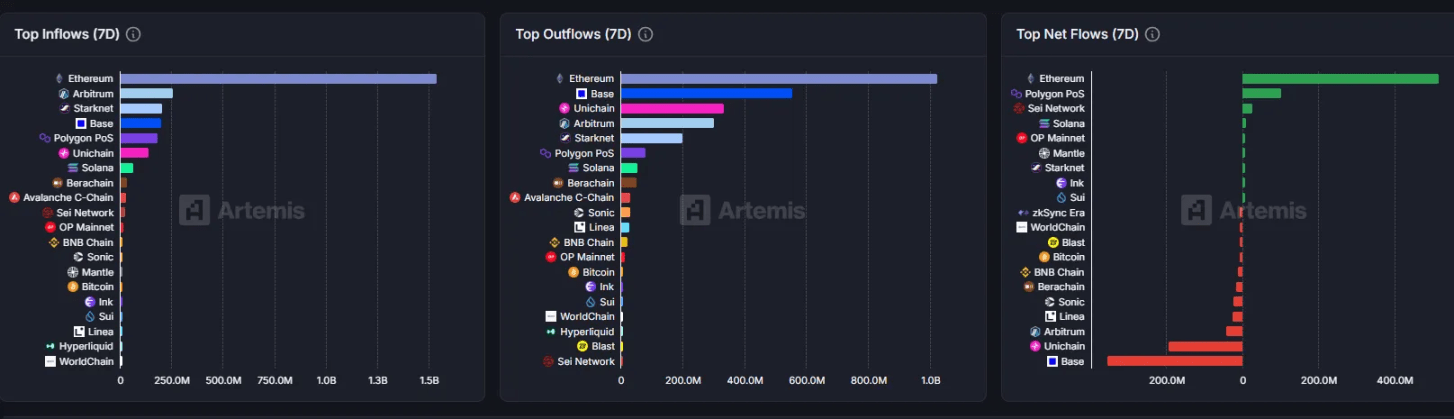

On-chain Asset Flow: The ETH chain is the public chain with the most asset inflows through DeFi bridging this week, while the BASE chain had the most outflows (accounting for 10% of its TVL), which needs continuous attention;

User Activity: BNB chain active users are growing the fastest, while ETH and SOL maintain good activity, not dropping significantly with market corrections;

On-chain Prosperity Index: This week at 50 points (breaking below the 60-point upward line), mainly due to increased ETF outflows and thin trading in the secondary market. However, fees and REV performance remain strong, and overall the market has not entered a recession zone.

5. Summary and Future Focus

The core contradiction in the market this week is the tug-of-war between 'BTC whale selling pressure + ETF fund outflows' and 'ETH's resilience + some bottom-fishing funds entering'. The altcoin market is adjusting in sync with cooling sentiment, but there is no panic selling, and overall it is in a 'weak balance' state.

In the future, three major signals need to be closely monitored:

When will BTC ETF resume net inflows, and will addresses holding 10K-100K BTC stop selling?

Will the proportion of holdings for addresses holding 10K-100K ETH rebound, avoiding further divergence?

Whether the single-day net inflow of stablecoins can resume, and if the altcoin market can see new sector hotspots.

The above report data is edited and organized by WolfDAO. If you have any questions, please contact us for updates;

Written by: WolfDAO