Original author: Alex Liu, Foresight News

Reprinted: Oliver, Mars Finance

"Stablecoins" are just the outer garment of Ethena. Now let's take off the outer garment:

You have transferred funds into a trading company, which has a hedge fund that is risk-neutral (will not lose due to asset price fluctuations), offering an annualized return of up to 10% with a large capital capacity. The net value of this fund product was $1 at issuance and accumulates returns as the net value updates. You can buy in at any time, but selling through official channels requires a wait of 7 days.

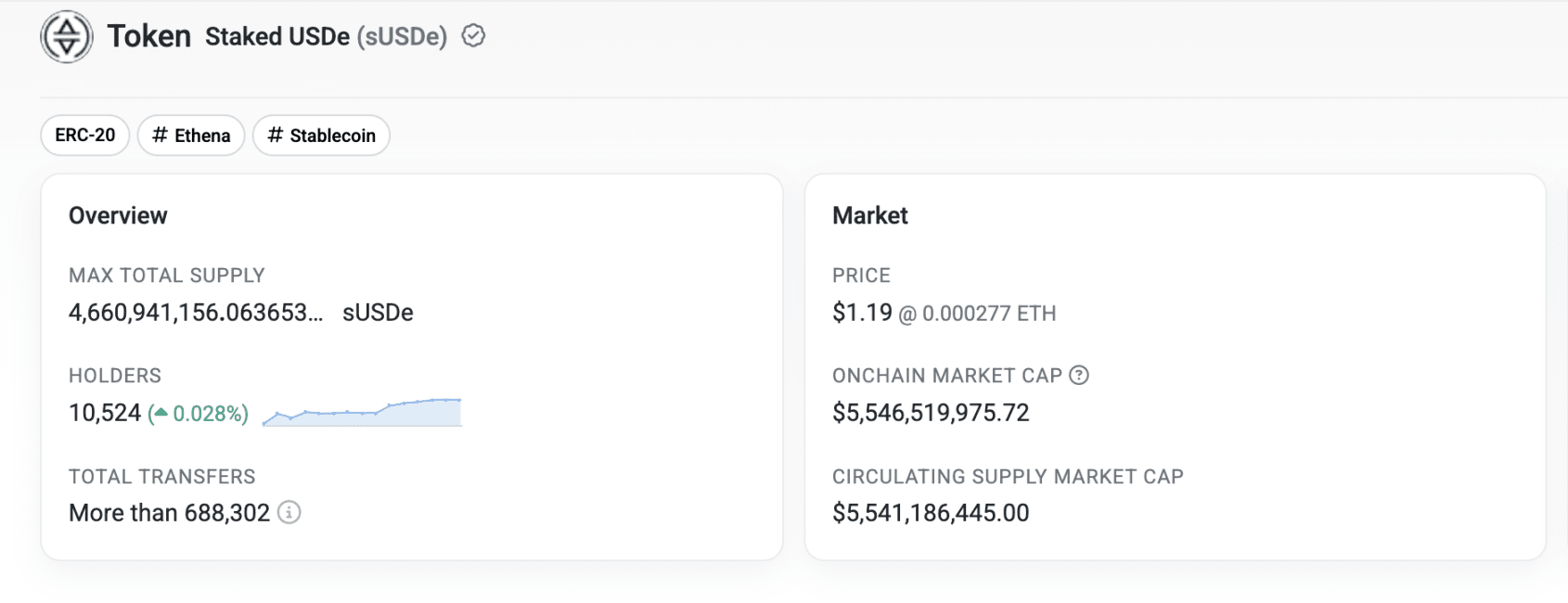

This trading company is called Ethena. For every $1 you deposit, you will receive 1 USDe as a deposit receipt. The fund product is called sUSDe, and over 4.6 billion have been issued, with a net value of $1.19 for each sUSDe.

By sending all customers' USDe and sUSDe to the on-chain wallet, registered on the blockchain, the trading company transforms into a "chain protocol." USDe then becomes a synthetic dollar stablecoin.

On the Ethereum mainnet, the sUSDe token

In the current heated narrative of "stablecoins," there are increasing numbers of companies that operate with stablecoins as shells but behind which run high-risk trading strategies, often referred to as "stablecoins backed by derivatives."

However, compared to stablecoins based on short-term Treasury bonds, the risks of these stablecoins are not comparable, and whether they are truly "stable" is also a big question mark. For example, Ethena's trading strategy (which will be elaborated later) requires deploying funds in perpetual contract exchanges - previously, the centralized exchange Bybit suffered over $1 billion in ETH funds being stolen, while Ethena has a large amount of funds in Bybit. If there is a funding gap at the exchange and withdrawals stop, the collateral behind USDe would actually be insufficient.

U.S. Treasury bonds are seen as the safest investment, and the market almost defaults to their "zero risk."

So why does Ethena take such risks by wrapping trading strategies into stablecoins using blockchain? What are the benefits of this operation?

First is the "premium in the crypto circle" because if we only look at Ethena from the perspective of a trading company, its valuation is "overvalued."

Overvalued?

Ethena conforms to the model of a "hedge fund" in all aspects, including its revenue model.

Revenue model

Ethena's main source of revenue is "funding fee arbitrage." For example, Ethena stakes some stablecoins deposited by users as ETH and opens a short position of equal value in the exchange. The gains and losses from spot and contract positions offset each other, achieving Delta-Neutral (risk-neutral, profits are unrelated to asset price fluctuations).

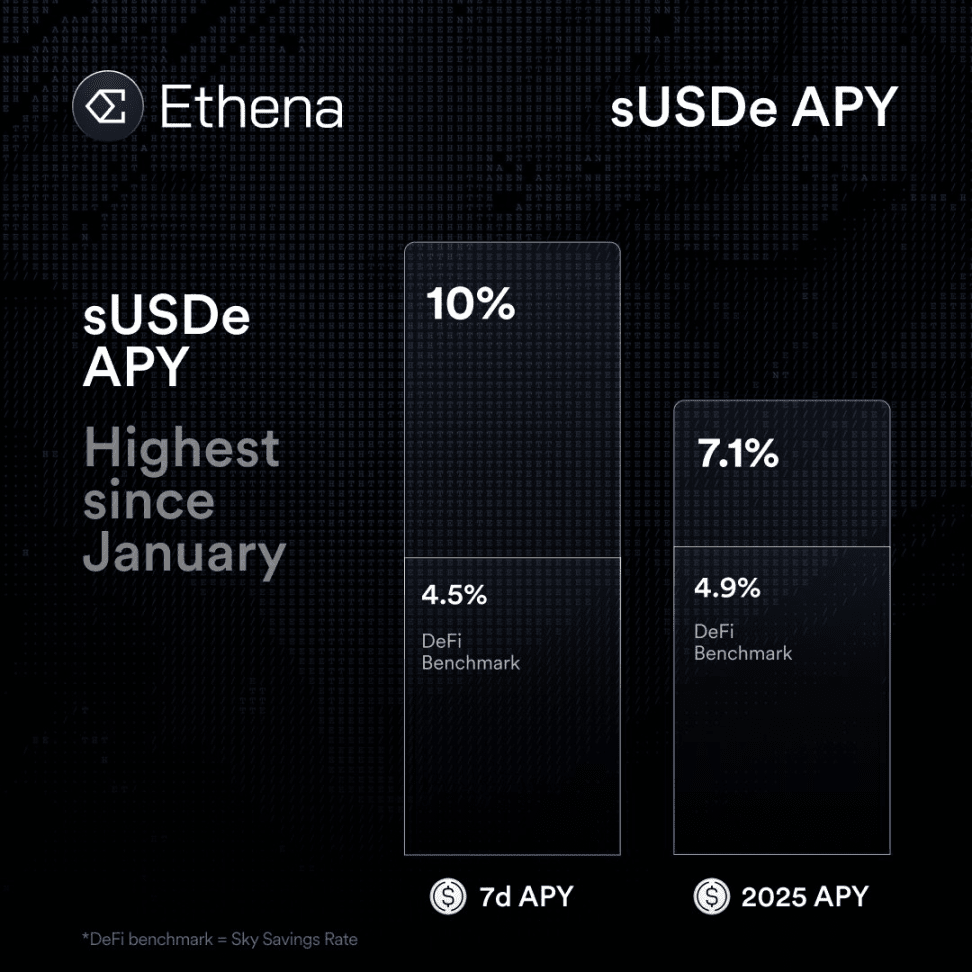

In this way, the spot ETH position can earn annualized staking yields of about 3%, while in neutral or bullish sentiment, the short contract position will continuously earn the funding fees paid by the long side. Idle stablecoins can also be deployed in protocols like Sky to earn returns. Multiple sources of income combined can bring an annualized return of 18% in 2024. As of July 18, Ethena's projected return rate for 2025 is 7.1%.

Ethena takes 20% of strategy earnings as protocol fees, with the remaining 80% as profits for sUSDe, which is equivalent to charging a 20% Performance Fee, a common practice in private hedge funds. So what is Ethena worth based on this model?

Traditional valuation models

The valuation model of private hedge fund companies (unlisted, such as Citadel and Two Sigma) generally uses a multiple of 5-15 times net income as the benchmark, with the multiple depending on the stability of funds and the replicability of strategies. In the actual valuation process, investors primarily focus on several core factors:

First is capacity, whether the fund has the space to expand its assets under management (AUM); second is stability, whether it can consistently deliver stable annualized returns; third is investor stickiness, including the locking period of funds and long-term retention rate. Ethena's annualized returns are currently influenced by market conditions and are not stable.

In terms of specific breakdown, fee-related earnings (FRE) are generally more stable and predictable, allowing for a higher valuation multiple of 10-15 times; while performance fees, due to their volatility, generally receive a lower multiple of 2-5 times. The final valuation is usually calculated using a mixed model, such as "FRE × 10 + Performance Fees × 3." Ethena's current revenue model includes only performance fees with no management fee income.

Furthermore, if the fund is in a rapid expansion phase, such as doubling its AUM every year, the valuation will also add a growth premium, further pushing up the overall valuation level. Ethena's recent rapid increase in TVL is a plus for it. However, considering its underlying strategy has a cap on capital capacity (limited by the market value of crypto assets and the corresponding perpetual contracts), one should not be overly optimistic about the growth potential of its hedging strategy.

Ethena's current total locked value (TVL) is $13 billion, equivalent to $13 billion AUM. When acquiring or investing in the industry, fund management companies often value based on 2%–6% of AUM. Even if calculated at 10%, the valuation would only be $1.3 billion, but Ethena is a trading company, not an asset management company, so this metric does not apply.

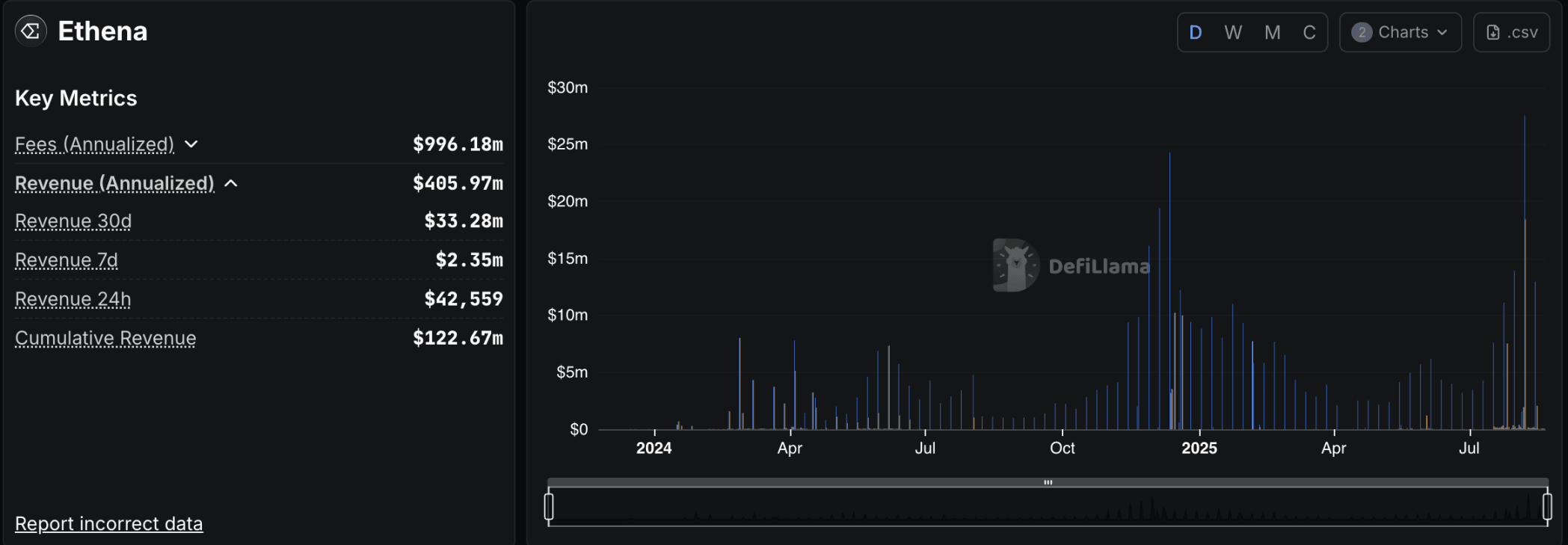

Ethena's annualized income is about $400 million, data from: DeFiLlama.

Based on the revenue over the past 30 days, Ethena's annualized revenue is estimated to be $400 million, and based on a high multiple of 15, the valuation should be $6 billion. The data used here is not conservative because Ethena may not be able to maintain its current annualized revenue and growth curve.

Currently, the fully circulating market value of Ethena token ENA is $9.7 billion, which is a 60% premium compared to the earlier calculations. What further makes its valuation "overvalued" is that its token currently does not have substantial "empowerment."

Token value capture

Ethena has currently not activated the "Fee Switch," meaning that all revenue from the Ethena protocol is currently unrelated to ENA holders.

So what is ENA useful for now?

Staking ENA tokens can earn sENA tokens (unstaking requires 7 days). Besides the negligible annual interest rate from staking itself, sENA tokens can also earn rewards from Ethena's own points and numerous ecosystem project points. These projects have all committed a certain amount of their own tokens to sENA token stakers, including Ethereal (15%), Derive (5%), Echelon (5%), Terminal (10%), and Strata (7.5%). Several of these projects will be elaborated on later.

In addition to earning Ethena points, sENA can also provide a bonus to the USDe-earned Ethena points, empowering the basic structure around points. These points will eventually be exchanged for sENA tokens during Ethena's next season airdrop, which can be termed as "digging for oneself." However, the total supply of tokens is limited, and the airdrop game cannot continue indefinitely; the lack of underlying value support is a challenge that ENA must face.

Fortunately, Ethena has not overlooked the option to open the "fee switch" to share protocol revenue with token holders, but has proposed the following conditions:

The circulating supply of USDe exceeds $6 billion.

Cumulative protocol revenue exceeds $250 million.

Among the top five centralized exchanges by derivatives trading volume, at least four have integrated USDe into their CEX platforms.

The reserve fund has grown to 1% or more of the USDe supply.

Expand the yield gap between sUSDe APY and competitive benchmarks (e.g., Aave's USDC).

As of today, some of the aforementioned indicators have been achieved. The remaining challenge is to increase the reserve fund size and improve the relative annualized interest spread to strengthen the competitiveness of sUSDe compared to other yield products.

However, the conditions for exchanges to integrate USDe are also cryptic; among the top five centralized exchanges by derivatives trading volume, OKX and Binance have not yet integrated USDe. Binance's own BFUSD, which adopts a similar hedging strategy to Ethena, is a direct competitor, reducing the likelihood of integrating USDe. Moreover, OKX has not even launched ENA token spot trading, and its attitude towards Ethena may not be friendly.

In this light, the fee switch for ENA doesn't seem as "imminent" as some expect. Even if the fee switch is activated, how much revenue can it generate for ENA stakers?

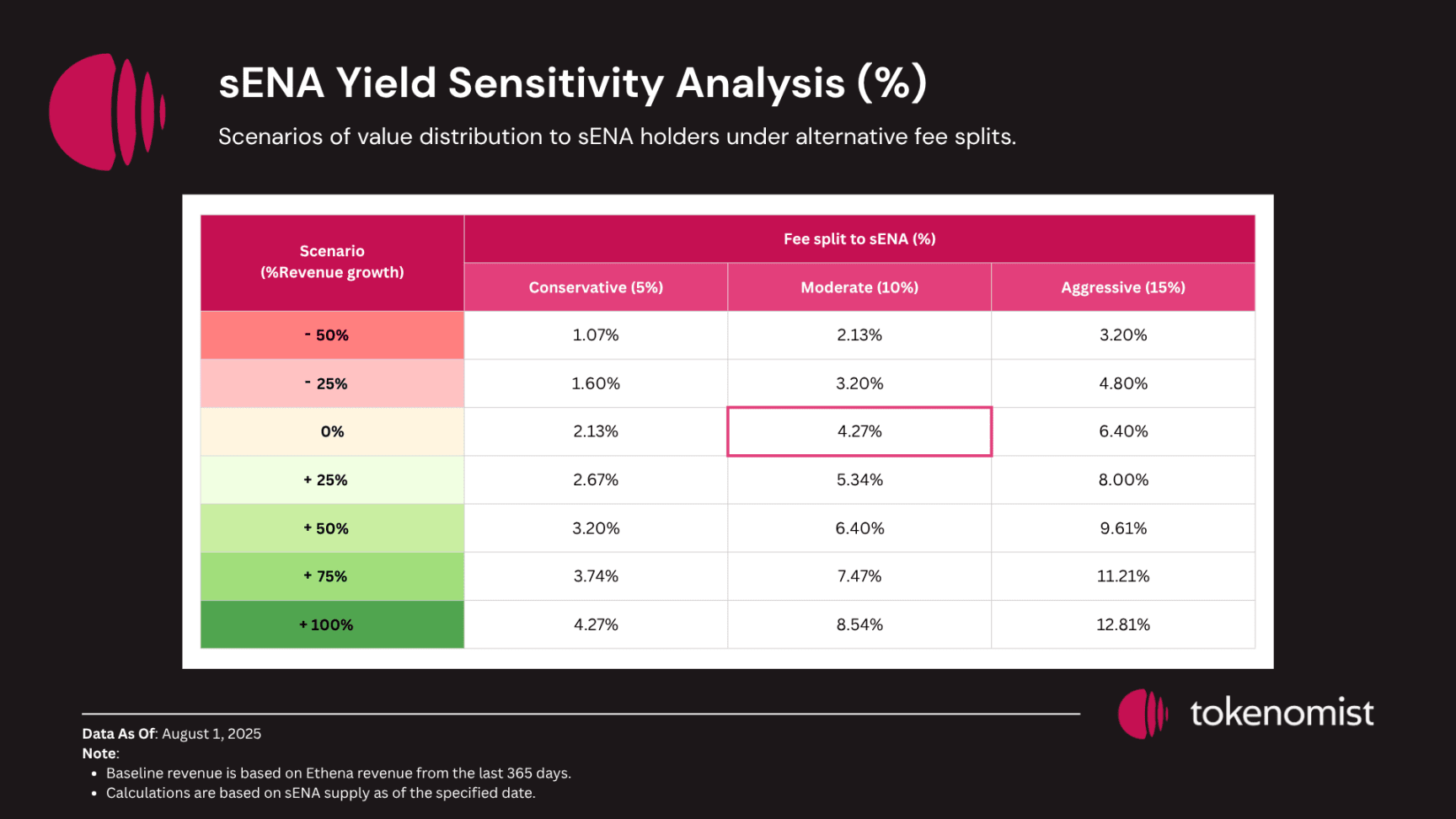

Potential yield of sENA

The potential yield of sENA is influenced by Ethena's revenue growth and the actual sharing ratio. According to tokenomist's calculations, the yield in the worst-case and ideal scenarios are 1.07% and 12.81% respectively.

If viewed from the perspective of dividends, the yield of 1.07% to 12.81% is actually satisfying. So why is ENA's valuation considered overvalued? Because such yields are based on a large amount of ENA tokens that have not yet been unlocked and staked.

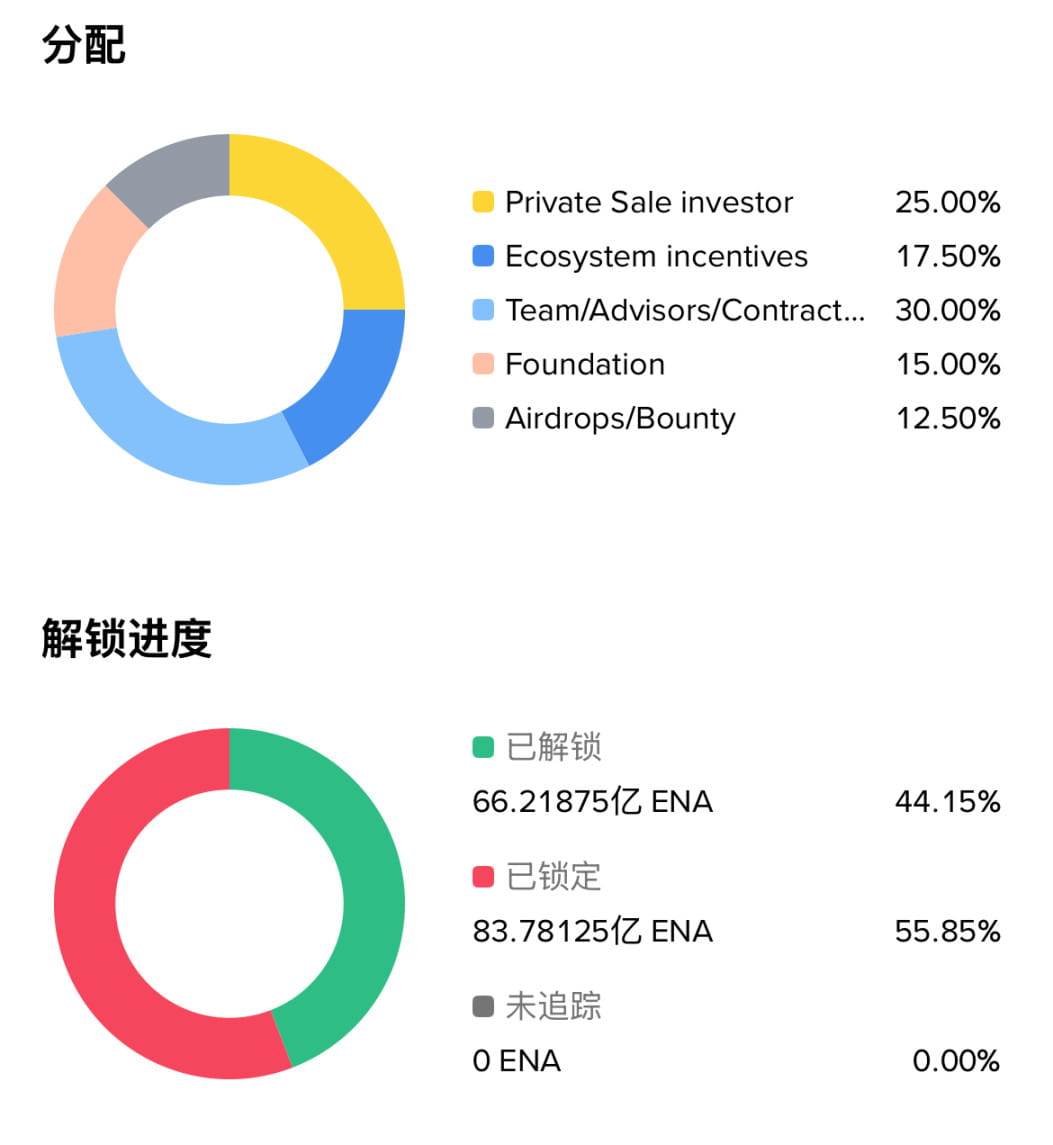

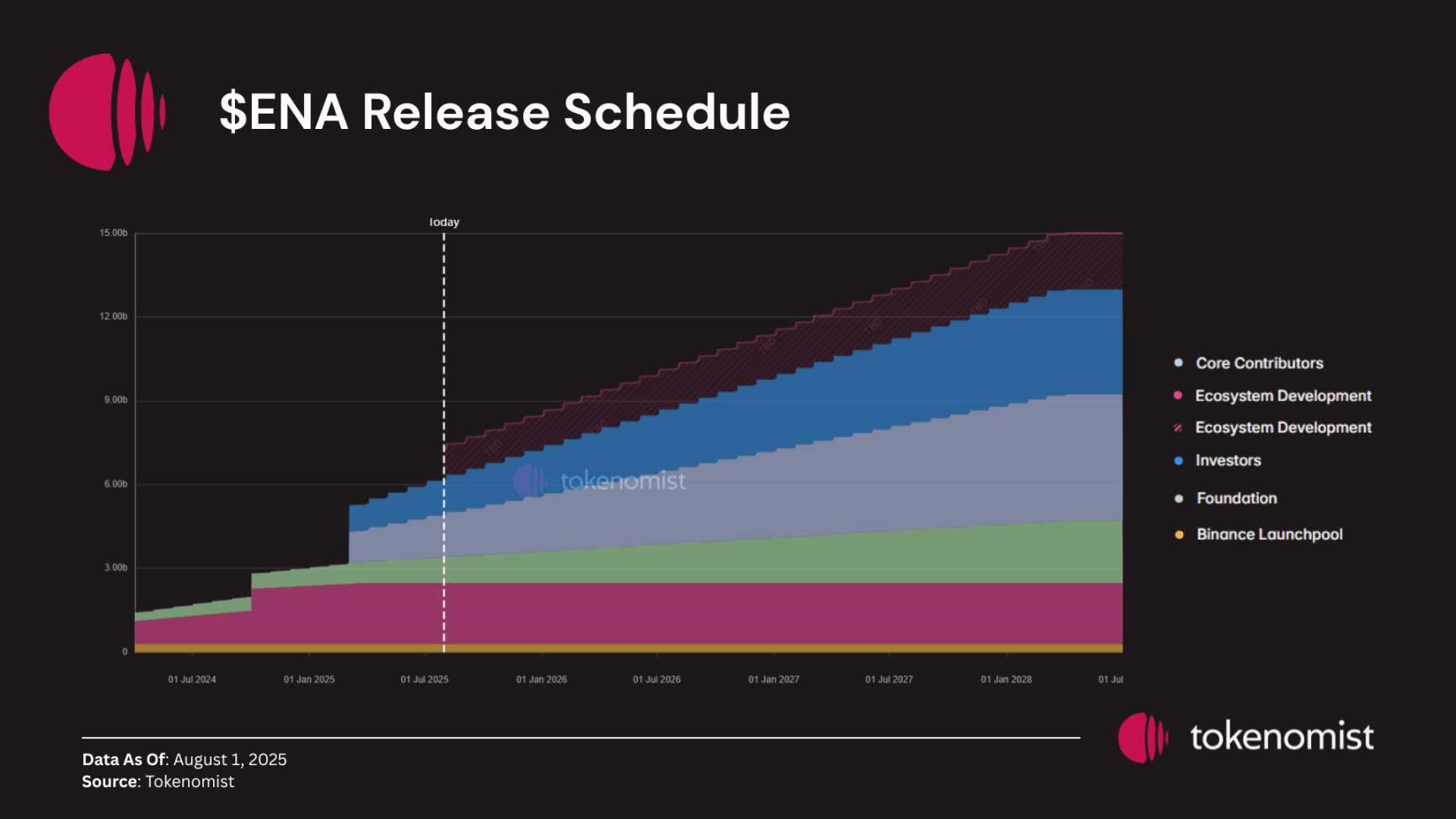

The total supply of ENA tokens is 15 billion, of which about 6.6 billion have been unlocked, while the circulating supply of sENA is only 910 million at this moment. Besides diluting potential yield, this also raises another issue for ENA - the pressure from unlocked sales.

Unlocking risks

Within the next 12 months, over $500 million worth of tokens will be unlocked for private investors, and about $650 million worth of tokens will be allocated to the founding team and early contributors.

At the same time, the distribution of Ethena's large ecosystem development remains largely uncertain. Currently, it is in the fourth season of airdrop activities (starting from March 2025), and Ethena has distributed 2.25 billion ENA tokens in the first three seasons, 750 million each season. With the fourth season underway and 13.5% of the total supply allocated for future ecosystem development, Ethena faces over $1 billion in distribution uncertainty.

Unlocking represents potential dilution of already circulating tokens. The speed of new token unlocks far exceeds the speed at which returns are generated, and could overshadow the impact of any fee switch or buyback mechanism.

But the buying pressure brought by Ethena's ENA treasury company might cushion the corresponding supply shock, and I will not elaborate further for brevity.

So is Ethena just a hedge fund that borrows the blockchain concept to gain valuation premiums, with unclear token value capture and unlocking risks? Is it a bubble in the sunlight, ready to burst at any moment in the future?

No. What Ethena aims to build is actually a vast CeDeFi ecosystem. (CeDeFi, the fusion of centralized finance and decentralized finance.)

From application to ecosystem

sUSDe is a user-recognized application with PMF (Product Market Fit), but it has a developmental ceiling. Ethena realizes this and chooses to build a large ecosystem around this core application, striving to tell a bigger story.

Ethena is not the only project taking the path of "from application to ecosystem." Similar examples include Hyperliquid, which launched the L1 public chain component HyperEVM after the successful decentralized perpetual contract trading application HyperCore, attracting many quality teams to build projects in its ecosystem.

Ethena's 2025 roadmap is named Convergence, which means intersecting, gathering, merging, and converging. Later, Converge became the name of the public chain launched in collaboration with Secruritize. Ethena has grand ambitions: it aims to create CeDeFi - a bridge linking CeFi (centralized finance) and DeFi (decentralized finance), bringing the trillion-dollar TradFi (traditional finance) onto the chain.

Converge is the first step in its layout.

Converge

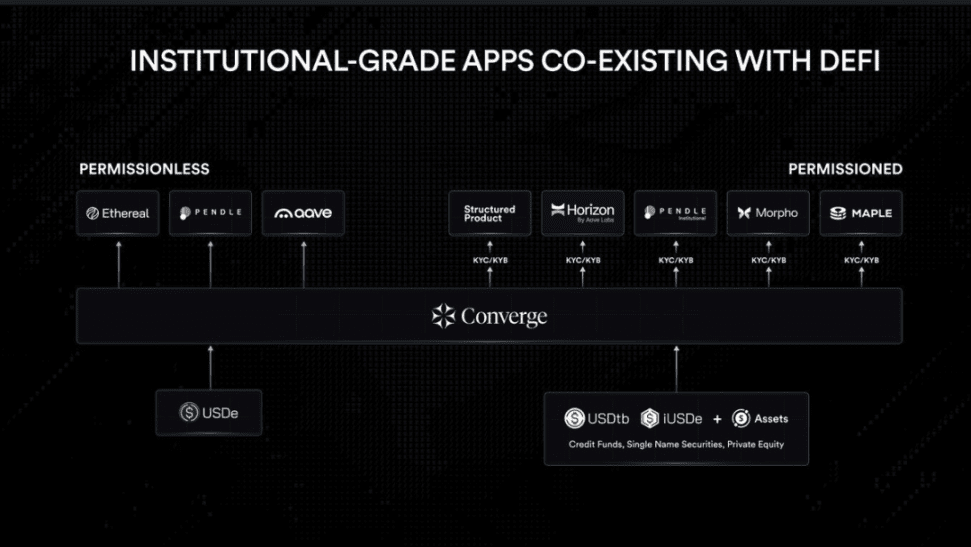

Converge is a blockchain network announced jointly by Ethena and the asset tokenization platform Securitize, designed specifically for institutional investors, positioned as a "settlement layer for traditional finance and digital dollars," aiming to provide a foundational platform for traditional financial institutions that meets strict compliance requirements without compromising technical performance.

Ethena plans to migrate its entire ecosystem to a new chain and issue native stablecoins USDe, USDtb supported by the BlackRock BUIDL fund, and iUSDe designed specifically for asset management institutions; while Securitize will deploy its complete tokenized securities issuance and management system on Converge, covering various asset classes such as stocks, bonds, and real estate, and actively exploring new application scenarios like on-chain stock trading.

The Converge network will support two parallel operational modes - on one hand, ensuring that permissionless DeFi applications can develop freely, while on the other, creating compliant products for traditional financial institutions. For example, the tokenized securities issued by Securitize can not only serve as on-chain collateral for customized money markets, but their compliance design also provides a trustworthy entry point for institutional investors.

Converge has introduced strict compliance measures, including KYC/KYB verification, institutional-grade custody services (provided by institutions like Anchorage and Fireblocks), and permissioned validator nodes. Network validators need to stake Ethena governance token ENA (to empower ENA, transitioning from a simple application to a public chain token). Additionally, USDe and USDtb will serve as the native gas tokens for the network.

The public chain is just the starting point; Ethena is also preparing to build its own decentralized exchange - Ethereal.

Ethereal

Ethereal is a decentralized exchange, centered around USDe as the core asset, building a spot exchange, perpetual contract exchange, lending and deposit functions, RWA (real-world assets), and a series of features to create an "All-in-one" super application, alleviating the fragmented experience of DeFi (which requires multiple applications to achieve the above functions). Ethereal will allow margin trading while earning returns, and using USDe as margin increases USDe's use cases, which helps Ethena grow.

On the deployment front, Ethereal has chosen to operate as an L3 application chain running on Converge (even though Converge is built on Arbitrum's L2 stack and chooses Celestia for data availability, it has not publicly advertised itself as L2) and has stated that this decision is not made for the sake of pursuing a trendy technology but is a necessity for the product itself to achieve optimal performance, composability, and the dedicated block space required by exchanges.

Using its own compliant public chain to execute Ethena's hedging strategy in its own exchanges can alleviate funding security risks brought about by trading locations to a certain extent. Using USDe on Ethereal also helps Ethena improve capital efficiency and reduce trading losses.

Ethereal is currently in the testnet phase. It has previously opened pre-deposits, and depositing USDe can earn airdrop points from both Ethereal and Ethena. The total locked value (TVL) once reached $1.25 billion, but has now fallen to $300 million due to reasons such as the expiry of Pendle pools and the conclusion of Season 0 and snapshot points, as well as the start of Season 1.

However, Ethereal is not the only exchange on Converge; another contender, Terminal, is targeting a different track.

Terminal

Unlike Ethereal, which focuses on a "super application-style DeFi comprehensive platform," Terminal Finance pays more attention to the institutional market. Its positioning is as a liquidity hub for the Converge ecosystem, focusing on trading institutional assets and digital dollars.

The question raised by Terminal is: the current "yield-bearing stablecoins" represented by sUSDe lack an efficient secondary market, leading to liquidity insufficiencies for large transactions. Therefore, Terminal aims to build a spot DEX centered around sUSDe, providing an efficient trading channel between stablecoins and institutional assets.

On the product level, Terminal will be divided into two parts:

First, a completely open decentralized trading platform where anyone can trade and provide liquidity;

Second, a licensed trading platform for institutions that supports compliance needs and tokenization of RWA (real-world assets).

In terms of mechanism design, Terminal adopts the redeemable "yield-wrapped asset" model. For example, in the case of sUSDe, its returns will be skimmed to ensure it maintains the stability of the dollar while also being reliably circulated as the protocol's base currency.

Terminal's pre-deposit is also ongoing, depositing USDe can earn airdrop points from both itself and Ethena, depositing WETH can earn points from both itself and ether.fi, and depositing WBTC can earn Terminal's own points.

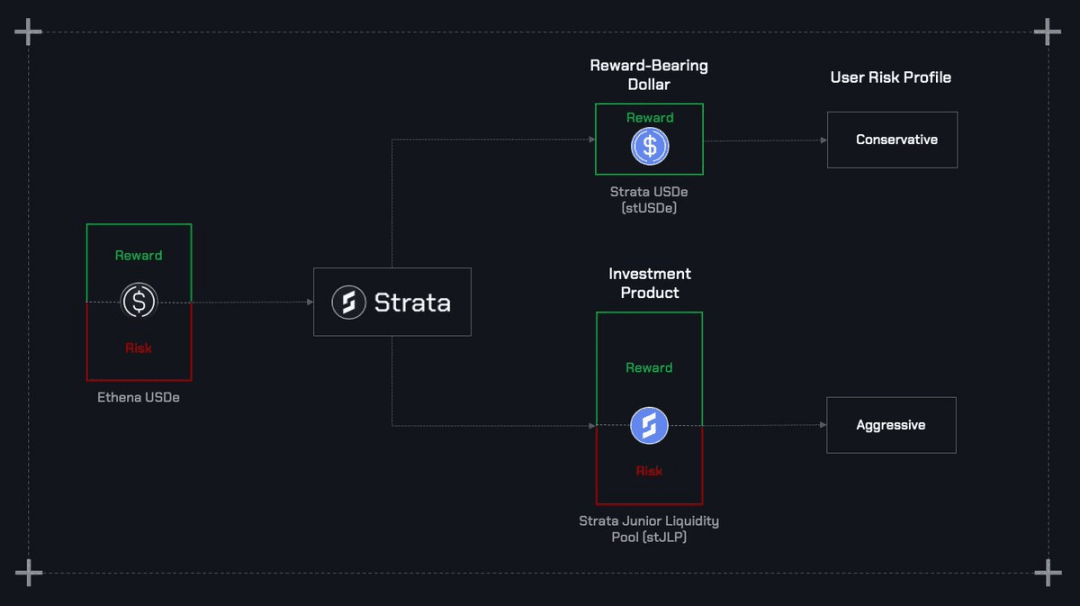

Strata

Ethena's success has led to a plethora of projects imitating it. Some projects are based on Ethena's mechanism and make "micro-innovations" on it to capture a certain market share, such as Resolv Labs (USR issuer). Ethena's mechanism has matured and should not be changed directly, but these innovations can be brought back to USDe through ecosystem projects. For example, Strata's mechanism is similar to Resolv.

Strata is a risk-tranching protocol based on Ethena, aiming to repackage the returns of yield-bearing stablecoins like USDe through structured products to meet the needs of investors with different risk preferences. It will also operate on Converge.

Specifically, Strata will split USDe returns into two categories of tokens:

Strata USDe (stUSDe): as a senior product, it offers more stable returns and principal protection, suitable for conservative investors. Its returns come from sUSDe, while ensuring a minimum APY and offering some upside exposure.

Strata Junior Liquidity Pool (stJLP): as a junior product, it bears additional risks and absorbs the volatility of sUSDe, but can achieve higher return rates, suitable for users willing to take risks.

This model is similar to structured wealth management in traditional finance, clearly layering returns and risks, thereby providing selectable risk exposure for institutional investors and retail investors.

For conservative funds, Strata's stUSDe provides predictable and weakly correlated stable returns to traditional interest rates; for risk-tolerant investors, stJLP offers the possibility of leveraged returns. If Ethereal and Terminal address trading and liquidity issues, Strata further fills in the puzzle of "risk management."

Against the backdrop of the integration of DeFi and TradFi, the emergence of Strata fills the gap in "institutional product design." Traditional finance often emphasizes risk-adjusted returns when entering DeFi, while Strata meets this demand with tokenized structured products.

Strata's airdrop season Season 0 is ongoing. Depositing USDe / eUSDe (pre-depositing USDe into Ethereal) not only earns its own and Ethena's airdrop points but also allows for multiple earnings from Ethereal's airdrop points. The three above Ethena ecosystem protocols have all integrated with DeFi protocols like Pendle and Euler, with various ways to earn points, such as LP, YT leveraged mining, and PT circular loans, and readers are encouraged to explore independently.

Model innovation

Ethena's story is quite compelling. Understanding the grand ecosystem it is building makes it hard to view its trading company business model merely as a strategy to gain premium valuation; it even leads one to ponder whether this approach could be considered true "model innovation."

For me personally, the answer is affirmative.

CeDeFi

When Ethena registers customer balances and hedge fund shares (USDe, sUSDe) on the blockchain, it indeed transforms from CeFi to "CeDeFi," possessing inherent DeFi advantages such as Permissionless - common private hedge funds are usually only accessible to institutions and high-net-worth users, with thresholds possibly reaching millions of dollars and may require various identity information to meet compliance needs; but on-chain, no identity verification is needed, only gas fees, allowing anyone to buy as much as they want, whether it's $10, $100, or $1,000, without anyone's consent.

The accessibility of DeFi benefits many who have been isolated from traditional finance. A citizen of an unstable country in South Africa may have no trustworthy banks around, but as long as they have internet access and crypto wallet software, they can enjoy gains from top hedge institutions.

These inherent advantages of DeFi, compared to CeFi, represent model innovation. Because for many retail investors, this is an investment opportunity that goes from nothing to something, and blockchain makes advanced finance accessible to the masses, giving retail investors more investment choices.

So the current empowerment of Ethena token ENA is the airdrop amplifier; the "digging for oneself" model might always be subpar? There is, in fact, another side.

Token marketing

Using token incentives (airdrops) to promote protocol growth may also represent model innovation in product distribution. Because it has indeed worked, USDe has become the fastest "dollar asset" to reach a supply of $10 billion, and the role of the ENA airdrop in the four seasons has been significant.

It is worth noting that sUSDe itself is a practical product with PMF (Product Market Fit) - there is already a demand for returns, and coupled with airdrop points, it can have multiple benefits, which is quite favorable. Token marketing has propelled its growth, but when incentives cease, the development trend of sUSDe is unlikely to be reversed.

For rapidly growing companies and products, not paying dividends but using funds for future development is quite normal; many technology stocks listed on NASDAQ operate this way.

Once products mature, tokens are always going to have empowerment. Even the long-standing governance meme token UNI is paving the way for opening the fee switch. Whether through buyback mechanisms or revenue sharing, empowered tokens represent a certain "ownership" of the underlying product, equivalent to equity in the Web2 world. Using equity to incentivize users to use products? This is typically not possible in traditional finance, but blockchain makes it possible.

Handing over the product to users is the fundamental idea of Web3 and also the "model innovation" of ownership distribution.

Ethena amplifies blockchain model innovation, and may grow into a huge and ubiquitous CeDeFi ecosystem.

Statement: The author of this article holds ENA tokens, the value of which meets the disclosure standard.