Author: Will Owens, Research Analyst at Galaxy Digital

Translation: Golden Finance xiaozou

With the emergence of digital asset treasury companies and Bitcoin prices breaking historical highs, people have gradually forgotten the core value proposition of the Bitcoin network: a decentralized, censorship-resistant currency system aimed at providing permissionless global value transfer.

Since the decline of non-monetary activities from the Runes protocol and Ordinals protocol at the end of 2024, Bitcoin's on-chain usage has sharply declined. Now we see an increasing number of "free" or nearly free blocks, which means that the average fee paid per virtual byte (a standard unit measuring the size of Bitcoin transactions) is only 1 sat (one hundred millionth of a Bitcoin) or even lower. While this creates short-term benefits for users seeking cheap and fast transfers, it adds a burden to the mining economy already under pressure from the 2024 halving.

This article analyzes the structure of the Bitcoin transaction fee market, assesses the real dynamics on-chain and their impact on the health of the network economy, and examines the evolution of OP_RETURN transactions and their usage patterns. In light of the impending release of Bitcoin Core client version 30, which has sparked controversy—this open-source software will by default allow single transactions to contain larger capacities and more OP_RETURN outputs—related analysis is particularly relevant. Some members of the Bitcoin community worry that this move will lead to a flood of spam transactions, and sharp criticisms have been made against this update proposal.

Article Summary

Bitcoin fee pressure has collapsed: since April 2024, the median daily fee has dropped by over 80%; as of August 2025, about 15% of blocks are "free blocks."

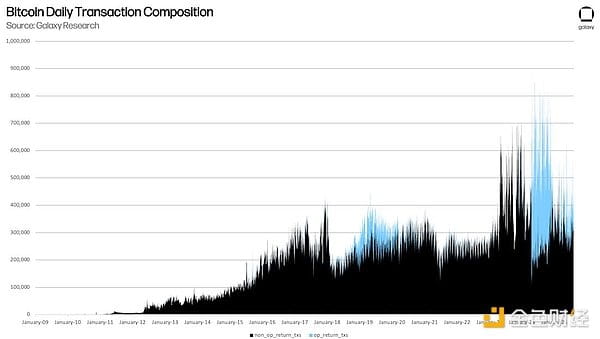

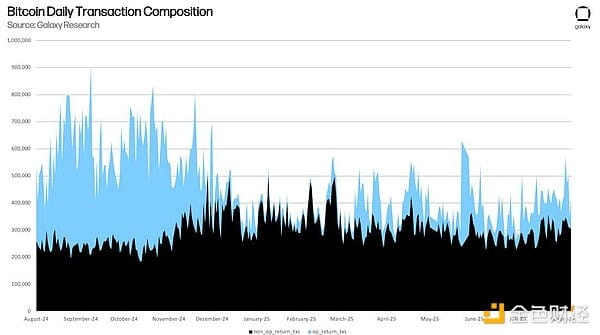

OP_RETURN activity has experienced surges and declines: during the peak adoption period of the Runes protocol (Q2-Q3 2024), OP_RETURN transactions often accounted for 40-60% of daily transaction volume; as of August 2025, this proportion has dropped to about 20%.

Memory pool activity is scarce: in recent months, the proportion of non-full blocks has repeatedly soared to nearly 50%; after the 2024 halving reduced block rewards to 3.125 BTC, the dormant memory pool may pose challenges to the long-term sustainability of miner income.

On-chain activity may be replaced by alternative solutions: spot Bitcoin ETFs currently hold about 1.3 million BTC, most of which have not undergone substantial on-chain transfers; trading and speculative activities are shifting towards alternative Layer 1 solutions like Solana, especially in use cases such as meme coins and NFTs.

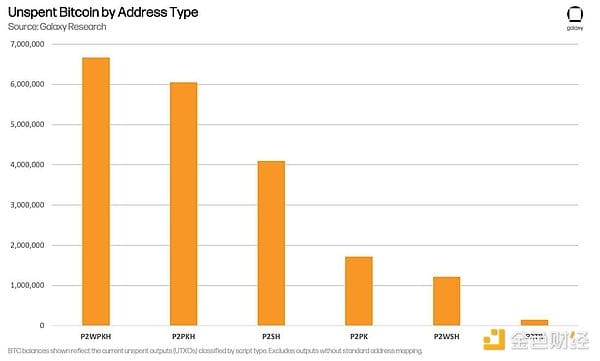

Over 1.5 million BTC is still stored in traditional P2PK addresses: these naked public key addresses are considered extremely vulnerable to potential quantum computing attacks due to the public key always being exposed on-chain.

Over 6 million BTC is still stored in traditional P2PKH addresses.

The P2WPKH address format currently holds the largest share of unspent BTC.

1. Methodology

All on-chain data in this article comes from Galaxy's internal Bitcoin infrastructure, including our self-built full nodes. Unless otherwise stated, the statistics reflect the state of the Bitcoin network as of August 12.

Fee metrics: Calculated using block-level data, including average/median fees, the ratio of "free blocks" (blocks with an average fee of ≤ 1 sat/vB), and the proportion of non-full blocks. In this study, we define blocks with total weight below 3.9 million weight units (relative to a maximum of 4 million) as non-full blocks.

OP_RETURN analysis: Identifying transactions containing OP_RETURN opcodes by analyzing transaction data. The daily proportion of OP_RETURN transactions is expressed as the percentage of such transactions out of the total transaction volume for that day.

Address format classification: Unspent outputs are categorized by script type (such as P2PKH, P2PK, P2SH, P2TR, P2WPKH). The total balance statistics are as of August 12.

2. Current state of the fee market

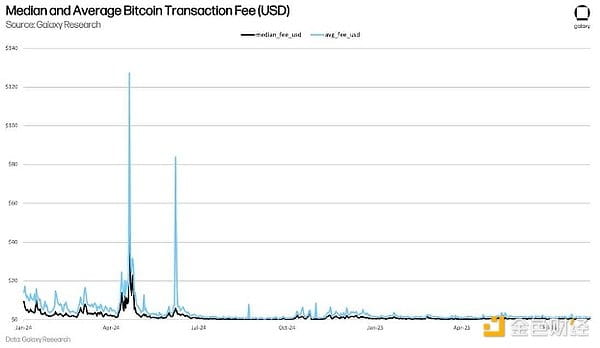

The Bitcoin fee market—the mechanism by which users bid to have their transactions included in the next block—has entered a stagnation period. Although almost all Bitcoin transactions come with a fee, users can choose the amount to pay, with transactions that pay higher fees typically getting confirmed faster. After several months of network congestion caused by Bitcoin's fungible/non-fungible tokens (namely Runes and Ordinals), the current pressure on network fees has sharply diminished. The average daily transaction fee has dropped to its lowest level since the beginning of 2023.

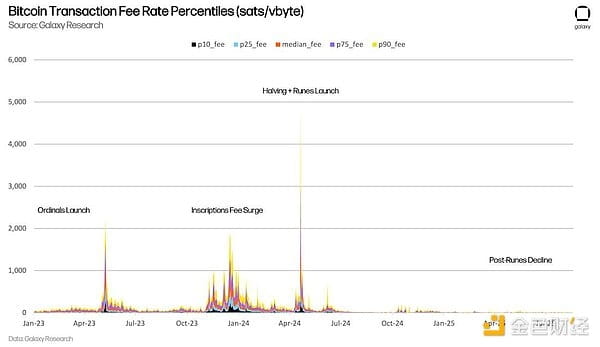

Although average and median fees can effectively summarize market trends, they cannot reflect the full picture. The figure below presents the data through more refined dimensions: daily transaction fee percentiles calculated by virtual byte price (sats/vB).

This chart covers the time span from January 2023 to the present, displaying the fee levels at the 10th, 25th, 50th (median), 75th, and 90th percentiles. This perspective not only reflects median changes but also presents a complete picture of the evolution of fee pressure in the memory pool, clearly revealing the sharp narrowing of fee differences since the end of 2024.

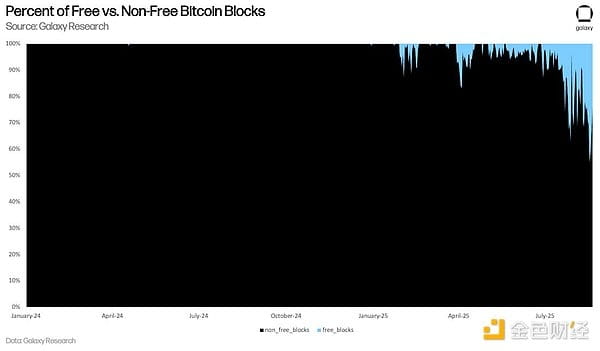

The most intuitive manifestation of this trend is the surge in the number of "free blocks" (blocks with an average fee of ≤ 1 sat/vB). Such blocks were virtually nonexistent in 2024, but are now increasingly common. As of the writing of this article, free blocks account for a significant proportion of daily produced blocks, fully evidencing the collapse of block space competition.

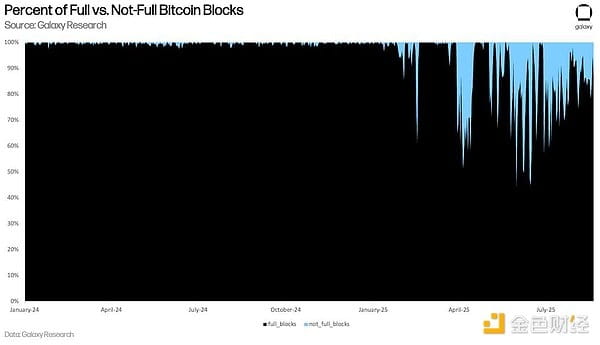

Meanwhile, the proportion of "non-full blocks" remains high. These blocks, although still having space to accommodate more transactions, have not reached the upper limit of 4 million weight units. In short, Bitcoin's memory pool (the waiting area for pending transactions) often remains vacant; even when not empty, it is filled with transactions that can be processed quickly without paying high fees.

For miners, this phenomenon is concerning. The 2024 halving has reduced the block reward to 3.125 BTC, and it was initially expected that transaction fees would play a more significant role in miner income, but the reality is that fee income is exhausted. The long-term economic model of Bitcoin network security relies on a healthy fee market, and the current market conditions are far from "healthy."

The rise of custodial solutions and "Bitcoin paper wallet" products (whether ETFs or other institutional derivatives) may be suppressing on-chain activity. Meanwhile, meme coin traders are accelerating their migration to faster and cheaper Layer 1 solutions like Solana—when the meme coin trading experience on Solana is so smooth, it is clearly not worth enduring the poor user experience of the Runes protocol.

3. OP_RETURN opcode

The OP_RETURN opcode for Bitcoin was introduced in 2014, allowing users to embed up to 80 bytes of arbitrary data in transaction outputs. These outputs have verifiable unspendability and typically carry no BTC value, thus not increasing the size of the unspent transaction output (UTXO) set. UTXOs are discrete units of Bitcoin that wallets can use for future transactions, forming the cornerstone of the Bitcoin accounting system—every transaction consumes existing outputs and generates new outputs. If BTC is sent to an OP_RETURN output, those coins will be permanently locked, but in return represents a whole new use case: permanently storing information or metadata on the blockchain.

In the past 18 months, the usage of this script type has surged. During the launch of the Runes protocol in April 2024 (at block height 840,000, coinciding with the recent halving of miner block rewards), OP_RETURN transaction volume reached a historical record. As shown in the figure below, these non-monetary transactions dominated block space at their peak.

As Runes activity cools, the current usage of OP_RETURN has gradually declined. However, developers and institutions continue to leverage it for anchoring data on-chain. For instance, a few weeks ago, Galaxy broadcasted a historic client transaction of 80,000 BTC via OP_RETURN.

OP_RETURN is being given innovative uses. An organization named after the Wall Street legend investment bank Salomon Brothers has begun using OP_RETURN to send legal notices to dormant Bitcoin wallets. These on-chain messages invoke the "abandonment principle" and require wallet owners to respond within 90 days, otherwise "Salomon" (the organization holds the trademark but is not related to Citigroup, which inherited the original investment banking business) will claim the right to pursue the funds on behalf of its clients (but how this organization controls these wallets remains unclear).

While this is an innovative practice for Bitcoin directly anchoring legal documents, it has sparked controversy in the context of the upcoming update of Bitcoin Core client version 30. This soon-to-be-released open-source software will loosen the default limits on OP_RETURN data payloads, allowing a single transaction to include larger capacities and multiple data outputs. Critics point out that although OP_RETURN outputs do not inflate the UTXO set (due to their verifiable unspendability), they still occupy block space, potentially squeezing out monetary transactions and threatening the long-term sustainability of the network. The Bitcoin Core development team responded that the final decision on whether to forward or package larger-scale OP_RETURN transactions still lies with node operators and miners.

4. Bitcoin holdings by script type

While fee trends can reflect short-term dynamics of Bitcoin, the UTXO set itself better reveals the long-term distribution of BTC in the network. By classifying unspent outputs by script type (i.e., address format), we can observe the adoption of various address types and their impact on spendability, security, and resistance to quantum computing.

The P2PKH (Pay-to-PubKey-Hash) format became mainstream after the early stages of Bitcoin and still holds a large amount of BTC (over 6 million coins). However, in recent years, new formats have gradually become popular: the P2WPKH (native SegWit) format launched in 2017 has become the largest holder of unspent BTC, while the P2TR (Taproot) format, enabled in 2021, is steadily growing, supporting more advanced script use cases.

The figure below shows the balance distribution of each script type as of August 11. This data also provides a basis for discussing future security risks.

The traditional P2PK (Pay-to-PubKey) format was mainly used for early coin creation transactions and is inherently vulnerable to quantum computing attacks—because this format has already exposed the full public key on-chain when unspent.

Other formats do not expose the public key before the output is spent. However, once spent (especially when the address is reused), the public key will also be exposed, putting those coins at similar risk.

5. Conclusion

Bitcoin on-chain activity has entered a period of stagnation, but the network infrastructure continues to evolve.

In the short term, low fees benefit users who wish to consolidate UTXOs or transfer assets at low cost. However, the long-term outlook is more ambiguous—the shrinkage of the fee market raises substantial doubts about network security.

In the context of block rewards being reduced to 3.125 BTC, miner incentives are increasingly reliant on fluctuations in organic demand. If more BTC transaction volume continues to flow towards ETFs, custodial institutions, and high-speed competitive chains, the core network may become a clearing layer lacking sufficient settlement activity.

With the expansion of "Bitcoin paper wallets" and stagnant fee income, the Bitcoin security model is increasingly reliant on a usage demand that is no longer guaranteed. While fee fluctuations are not a new phenomenon, Bitcoin does indeed need more substantive reasons for on-chain usage.