China RWA Ecological Series Research Trilogy 2 - Langxin Technology

Research on China's RWA Trilogy - Langxin Technology Project (Industrial Standard Assets) 2

Research on China's RWA Trilogy - Langxin Technology Project (Industrial Standard Assets) 1

Continuing from the last post, let's continue with the study of China's RWA Trilogy - Langxin Technology.

This time we will study the financing cost issues of the Langxin Technology project, which is the most practical and realistic issue.

From this perspective, we can explore which development stage China’s RWA is currently in and what unavoidable issues exist.

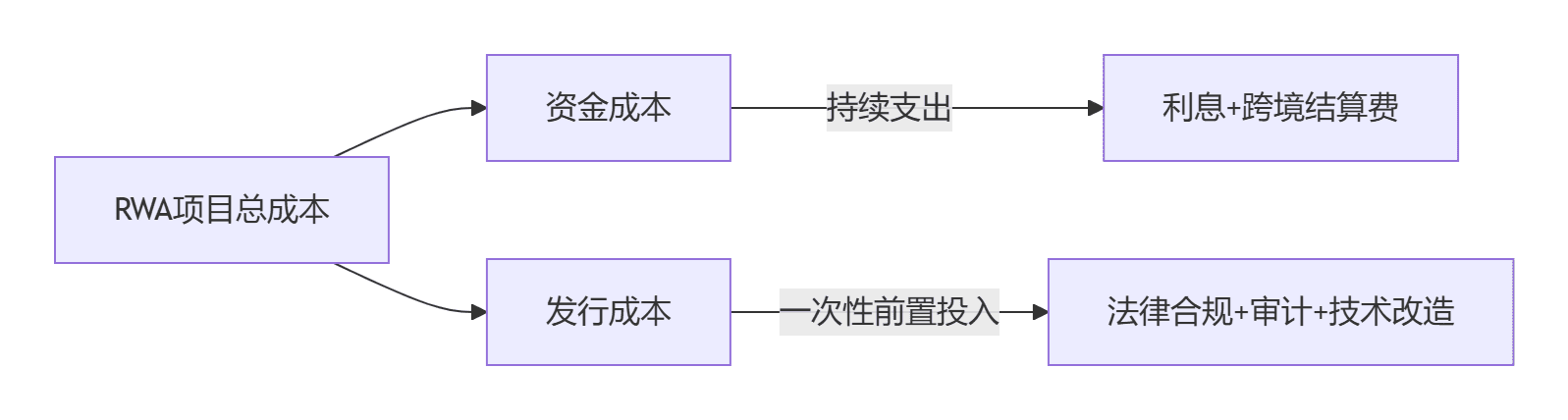

💰 Financing cost analysis

First of all, everyone needs to know that the total cost of an RWA project can be divided into one-time issuance costs and ongoing funding costs.

The former mainly includes legal compliance fees, auditing fees, and initial technological transformation costs; the latter mainly includes interest and cross-border settlement fees.

1. First, let’s look at the one-time issuance costs.

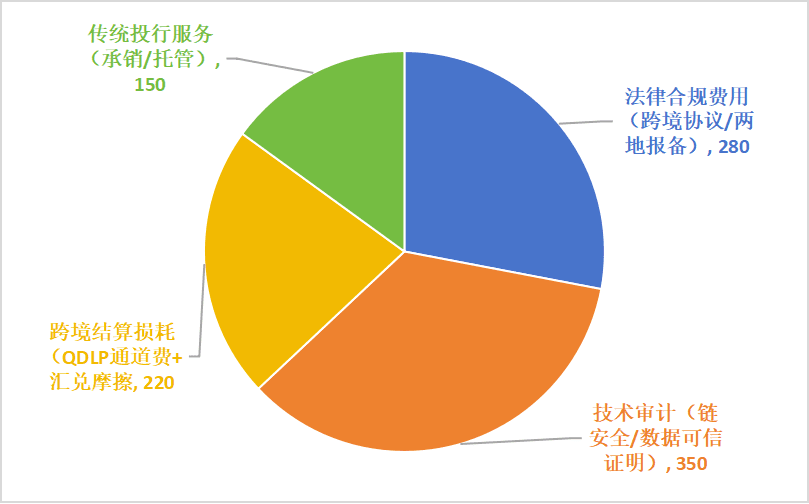

The issuance cost of the Langxin charging pile project is as high as 10 million RMB (accounting for 10% of the fundraising amount, significantly higher than the 6-8% of traditional ABS).

There are two reasons:

One is institutional friction, mainly focusing on dual auditing - PwC needs to simultaneously perform cash flow verification under mainland CAS 31 and auditing under Hong Kong HKFRS 9.

The second is foreign exchange losses - under the requirements of the State Administration of Foreign Exchange's QDLP mechanism, there is a fixed friction cost of 0.15% for RMB and wCBDC settlements.

From this image, we can see where the 10 million issuance costs were spent, with the main costs being technical auditing and compliance fees.

Contact previous agricultural projects - Malu, one of the reasons for choosing not to go through the Hong Kong sandbox is this.

For agricultural products, the product premium itself is often unable to cover the on-chain costs. If cross-border options are chosen, there will be huge costs from compliance and auditing.

On the other hand, the issuance costs of agricultural projects are even higher than those of Langxin due to the additional costs of early technological transformation.

2. Next, let’s look at the ongoing funding costs.

According to the data from Deloitte report DTT-2025-LXRWA-001, after the introduction of the Langxin RWA project, 100 million RMB was raised through Hong Kong offshore capital channels, and the funding cost was reduced to 5.2%.

The core optimization paths include:

● Interest rate differential capture: The cost of offshore RMB financing is 210 BP lower than domestic financing (compared to Standard Chartered Bank financing quotes).

● Intensity of issuance costs: Blockchain technology reduces intermediary links, saving 40% on underwriting fees (compared to traditional ABS).

Empirical effect - based on project scale calculations, it saves 3.5 million RMB in financial expenses annually, enabling the deployment of 42 liquid-cooled supercharging piles (cost per pile 83,000 RMB), directly improving asset yield by 1.8 percentage points (2024 ESG report P21).

Therefore, we can see that from the perspective of funding costs, asset on-chain indeed reduces financing costs.

3. So what is the situation regarding the total cost of RWA projects?

Let's look at this data. I couldn't find specific data here, but compared to traditional ABS projects' financing costs...

The significant reduction in the long-term funding costs of the project (8.7%→5.2%) will cover the initial premium when the duration is ≥3 years, forming economies of scale.

In other words, due to the current system, the issuance costs in the short term are greater than the average of ABS, but in the long term, cross-border RWA is more economical in long-term operations.

💵 From the above cost analysis, we can see that the current high financing costs of RWA projects in China, compared to existing ABS financing channels, are mainly due to institutional constraints.

For China’s RWA to truly explode, institutional innovation is unavoidable, but from the current situation, it is not realistic in the short term.

Similarly, cost analysis can also indirectly confirm my previous views on the real ecological environment of RWA in China - it is still in a relatively early stage, and existing projects are more about strategic considerations or an experimental mindset.

To truly tokenize physical assets and innovate a new financing channel on a large scale, institutional openness is still needed.

——————————————————————

So, among these RWA projects in China, apart from creating a wave domestically, have they brought any actual meaningful progress?

In the next post, I will show which institutional relaxations and progress these RWA, which we see as a stripped-down version, have promoted.