Today, while researching Aptos RWA-related materials, I discovered an interesting fact:

Aptos currently has a total RWA value of 723 million, ranking third in the crypto market. The top two are Ethereum and ZKsync Era.

It's not difficult to understand that ETH dominates the RWA market, but how did zksync, an L2 that I haven't focused on for a long time, achieve nearly $2.4 billion in RWA growth?

To avoid any advertising implications, let's get straight to the conclusion:

Nearly 90% of RWA TVL on zkSync comes from a single project, Tradable. Tradable is an asset tokenization platform that allows institutions to label and manage assets while remaining compliant.

RWA assets are closed private placement credit certificates and cannot be reused in open DeFi protocols. Although zkSync ranks second in the RWA market share, its Defi TVL ranking on Defillama is only 61st. This shows that the activity in the RWA field cannot intuitively bring trading volume and inject ecological vitality to public chains.

Looking at the statements regarding Aptos:

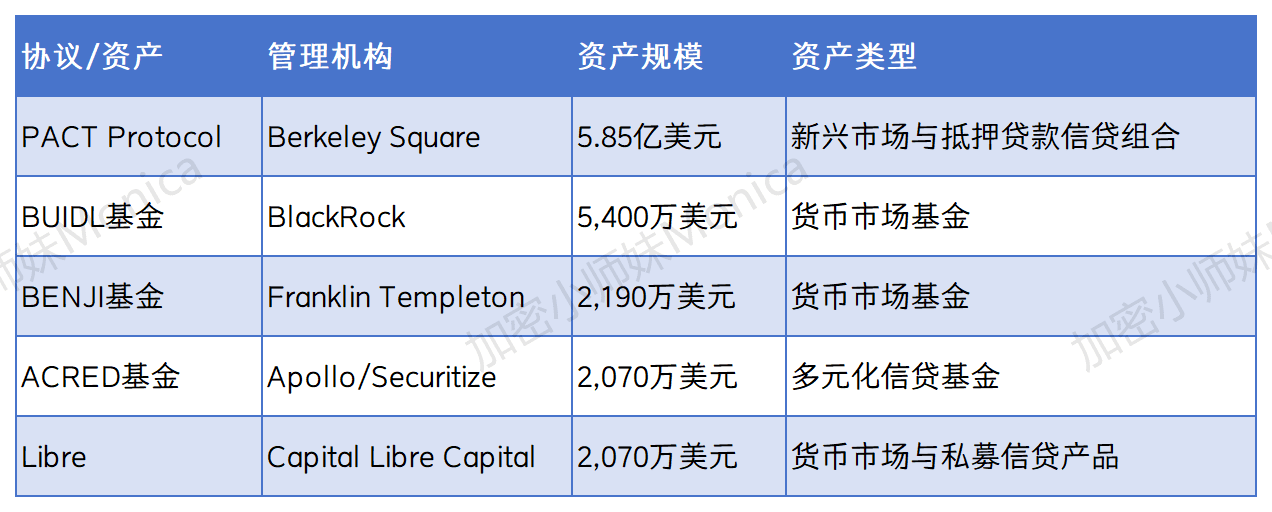

Looking at Aptos, it basically supports most mainstream RWA protocols, supporting a total of 22 tokenized products, mainly in the private credit field. The difference from zkSync is that Aptos supports more large institutional products; here are a few examples:

If you want to revitalize the ecosystem relying on RWA's popularity, I believe Aptos still needs to enhance the liquidity of RWA assets within a compliant framework and connect traditional finance with the DeFi ecosystem.

The next step is to introduce blue-chip protocols like Aave, which I estimate also has considerations in this regard. In simple terms: the advantage of compliant RWA issuance is merely becoming a qualified money printer; if you want to make money, you still have to find a way to become a bank.