Author: Jay Jo, Source: Tiger Research, Compiler: Shaw Golden Finance

Summary

Global centralized exchanges (CEX) are launching their own blockchains to ensure new revenue sources. Upbit and Bithumb may join this competition.

Four scenarios may emerge: a Layer 2 network based on OP Stack, a Korean won stablecoin infrastructure, leveraging Korea's unique market liquidity, and pre-IPO stock tokenization. Each scenario reflects the unique market conditions in Korea.

Regulatory restrictions and technological complexity remain significant obstacles. Implementing these in the short term is quite challenging. However, declining trading volumes and increasing global competition indicate that both centralized exchanges must seek new growth drivers.

1. Preparation, Setup, Launch: The competition for infrastructure led by CEX begins

Centralized exchanges (CEX) are diving into the competition for blockchain infrastructure. Coinbase has launched Base, Kraken has launched Ink, and Robinhood has recently joined in. The competition is becoming increasingly fierce.

This fierce competition stems from the limitations of the fee-based business model. Centralized exchanges (CEX) rely on the fee model as the most stable source of revenue in the cryptocurrency industry. However, these models are heavily dependent on market conditions. This has created a need for revenue diversification. Furthermore, CEXs previously only competed in limited regulatory jurisdictions. Now, the competitive landscape has expanded globally. DEXs have also challenged centralized platforms by capturing more than 25% of the market share at peak times.

At the same time, mainstream adoption of cryptocurrencies is accelerating. This opens up new business opportunities for CEXs through blockchain infrastructure beyond trading. These changes will accelerate CEXs' competition in launching their own blockchains.

2. What would happen if Upbit and Bithumb launched their own blockchains?

Global CEXs are racing to launch their own blockchains. This naturally raises the question: 'Will Korea's major CEXs, Upbit and Bithumb, follow suit?' To assess this possibility, we need to examine the current status of these CEXs and their previous attempts.

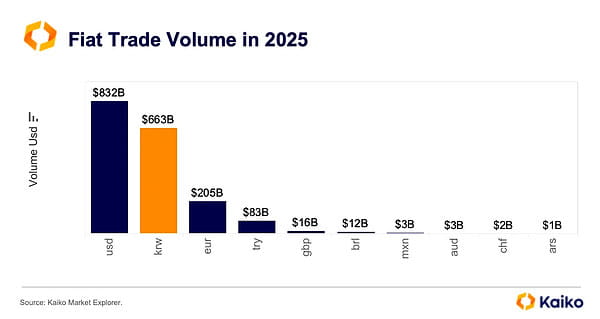

Korea occupies a unique position in the global cryptocurrency market. The trading volume of the Korean won (KRW) is second only to the US dollar (USD) among global fiat currencies, and it sometimes even surpasses the dollar. No other country has such a high trading volume. Such a market environment has allowed Upbit and Bithumb to grow into large companies (in Korea, companies with assets exceeding 50 trillion KRW are considered large enterprises).

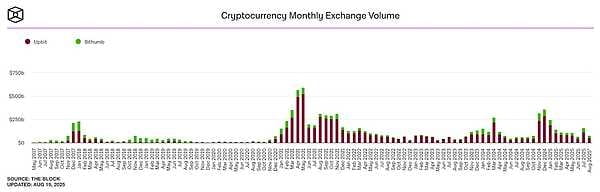

However, this structure is changing. Since peaking in 2021, trading volumes at Korea's centralized exchanges have been declining. Local users are migrating to global centralized exchanges such as Binance and Bybit or DEXs. This means that Korea's centralized exchanges are gradually entering an environment where they cannot rely solely on the Korean liquidity premium.

Korea's centralized exchanges (CEX) have sensed these changes. Upbit and Bithumb are both trying to achieve global expansion through overseas subsidiaries and business diversification. However, relying solely on the 'Korean CEX' brand makes it difficult to gain a competitive edge abroad. They have launched various platform-based businesses, but most have failed. These businesses lack a connection to the core strengths of CEXs. Regulatory sanctions have also limited efforts for business diversification.

The winds of change are blowing. Trump's support for cryptocurrency has improved the global regulatory environment. Centralized exchanges (CEX) can now more aggressively implement new growth strategies. In this context, launching their own chains has become a viable option for Upbit and Bithumb.

If they launch a blockchain, different outcomes can be expected. They can directly leverage their own strengths: a large user base and ample liquidity. Korea's unique market characteristics further increase the potential to create differentiated value.

Expected Scenario 1: Building a Layer 2 network based on OP architecture

If these centralized exchanges build their own chains, they are likely to choose Layer 2 over Layer 1.

The main reason is the complexity of development and the required resources. Developing and operating Layer 1 requires significant resources. Although Rollup services lower the threshold, Layer 2 still requires a lot of expertise. Kraken's Ink project involves about 40 developers. For centralized exchanges, independently building and operating such infrastructure would be a heavy burden. Their goal is to expand platform business through infrastructure rather than creating high-performance infrastructure themselves.

Regulatory risks further complicate the situation. Layer 1 blockchains require the issuance of native tokens, but Korea's regulatory environment makes token issuance nearly impossible and subject to severe penalties. Therefore, mimicking Coinbase's approach, a Layer 2 model that can operate without a native token becomes the most viable alternative.

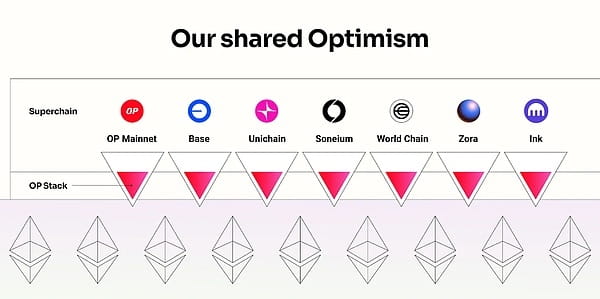

Layer 2 development encompasses various architectures, but global centralized exchanges (CEX) have adopted the Optimism (OP) Stack as the de facto standard. Coinbase's Base and Kraken's Ink are both built on this foundation and have become reference models for CEXs. Robinhood chose Arbitrum due to different strategic goals. Coinbase and Kraken are committed to expanding a broad ecosystem through interoperability, while Robinhood focuses on bringing financial services on-chain. The greater customization flexibility of Arbitrum may be more suitable for this model.

Upbit and Bithumb have similar goals to Coinbase. Both centralized exchanges must leverage their large user bases to expand on-chain services in order to overcome the limitations of fee-based models and create new revenue streams. Openness and interoperability are crucial for this expansion. Therefore, if Upbit and Bithumb launch their own public chains, the most likely option would be a public Layer 2 network based on the OP Stack.

Expected Scenario 2: Korean won stablecoin infrastructure

Another scenario for Upbit and Bithumb launching their own chains is to build specialized infrastructure around Korean won stablecoins.

Both centralized exchanges are actively engaging in the stablecoin market. Upbit and Bithumb have applied for trademarks related to stablecoins. Upbit has officially announced plans to enter the Korean won stablecoin market in collaboration with Korea's leading mobile payment service Naver Pay. Given that Upbit is the most likely candidate, the reality is that Naver Pay issues a won-based stablecoin while Upbit provides blockchain infrastructure. This structure complies with the Virtual Asset User Protection Act, which prohibits CEXs from trading virtual assets issued by themselves or related parties.

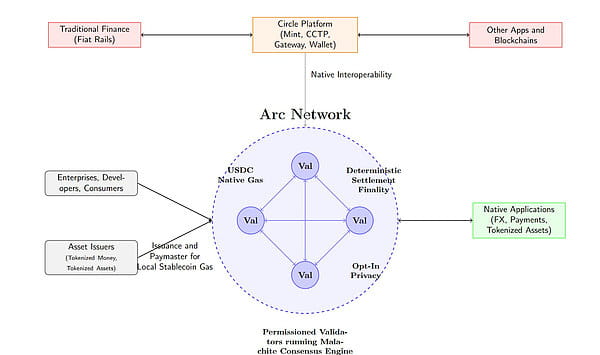

In this context, the key lies in building dedicated infrastructure for stablecoins. They can achieve differentiated services by adding real-world payment and privacy protection features. The network can be designed to use Korean won stablecoins for transaction fees. This is similar to the USDC Arc network model. The goal is to create an ecosystem where all transactions are centered around stablecoins. This structure provides users with stable costs while creating sustainable demand for Korean won stablecoins.

However, there are technical limitations. Optimism defaults to using Ethereum for transaction fees and has stopped supporting customized fee tokens. Therefore, a Layer 2 solution based on Arbitrum with customization capabilities or a Layer 1 using a Korean won stablecoin as the native token may be more suitable.

Expected Scenario 3: Strategies leveraging Korea's liquidity premium

One strategy that Upbit and Bithumb can try is to leverage Korea's liquidity premium. Korea currently possesses enormous liquidity, ranking second globally in terms of fiat currency. However, this liquidity is still limited to the internal systems of centralized exchanges.

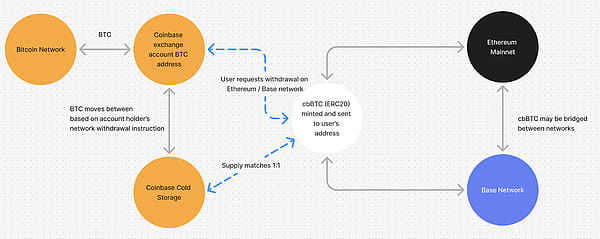

Centralized exchanges can issue wrapped tokens such as upBTC and bbBTC based on deposited assets. Coinbase's cbBTC is a typical example. These wrapped tokens can be used on other chains, but if the platform provides convenient features like one-click integration in its application, users may stay on the chain built by the CEX. This attracts project teams to build within these ecosystems to gain liquidity. An active ecosystem allows CEX to earn infrastructure-based revenue. CEX can also directly test other business models, such as lending using wrapped tokens.

Expected Scenario 4: Entering the pre-IPO stock tokenization market

Another strategy for Upbit and Bithumb could be to enter the pre-IPO stock tokenization market. Upbit has already been operating a pre-IPO stock trading platform through Ustockplus and has gained experience. However, this still operates as a P2P matching model, where buyers must respond to sell orders. Transactions cannot be completed without a counterparty. This model faces issues of low liquidity and unpredictable execution.

Tokenizing pre-IPO stocks on an independent chain changes the situation. Tokenized stocks can be continuously traded through liquidity pools or market makers. Ownership transfer is automated and transparent through smart contracts. In addition to simply improving trading efficiency, features such as automatic dividends, conditional trading, and programmable shareholder rights can also be realized on-chain. This enables the design of financial products that are not possible within existing securities systems.

Naver's recent bid to acquire Dunamu's Ustockplus shares is noteworthy. Upbit can provide blockchain infrastructure while Naver is responsible for platform operation and physical stock management. This structure operates well under current regulatory constraints. It separates the trading infrastructure from the securities management role, reducing institutional risk. It enables entry into the tokenization market while addressing the limitations of existing services.

3. Conclusion

We explored various scenarios that Upbit and Bithumb's own chains might present. However, there are still many obstacles in reality. The biggest limiting factor is regulation. Korea has adopted an active regulatory approach, making it difficult to launch services not explicitly defined by law. After being designated as large corporate groups, both centralized exchanges also face increased regulatory burdens. Additionally, they lack leaders with a Web3-native mindset like Jesse Pollak from Base. Technological complexity adds another layer of difficulty. The likelihood of these chains being realized in the short term remains low.

However, these attempts still hold sufficient potential. Domestic trading volumes in Korea have been declining since reaching a peak in 2021. Global competition continues to intensify. Solely relying on a fee-based model has obvious growth limitations. Previous revenue diversification attempts have not yielded significant results. Sustained growth requires new driving forces. Boldly attempting to build their own blockchain could become one of the pillars. This represents the most feasible business diversification strategy, leveraging their competitive advantages: user base and liquidity.

Moreover, these possibilities require a shift in regulatory attitudes to become a reality. With policy support for healthy market development and institutional flexibility, Upbit and Bithumb can more actively conduct various business experiments. This could become an opportunity to enhance the competitiveness of Korea's entire blockchain ecosystem, not just the growth of these two centralized exchanges.