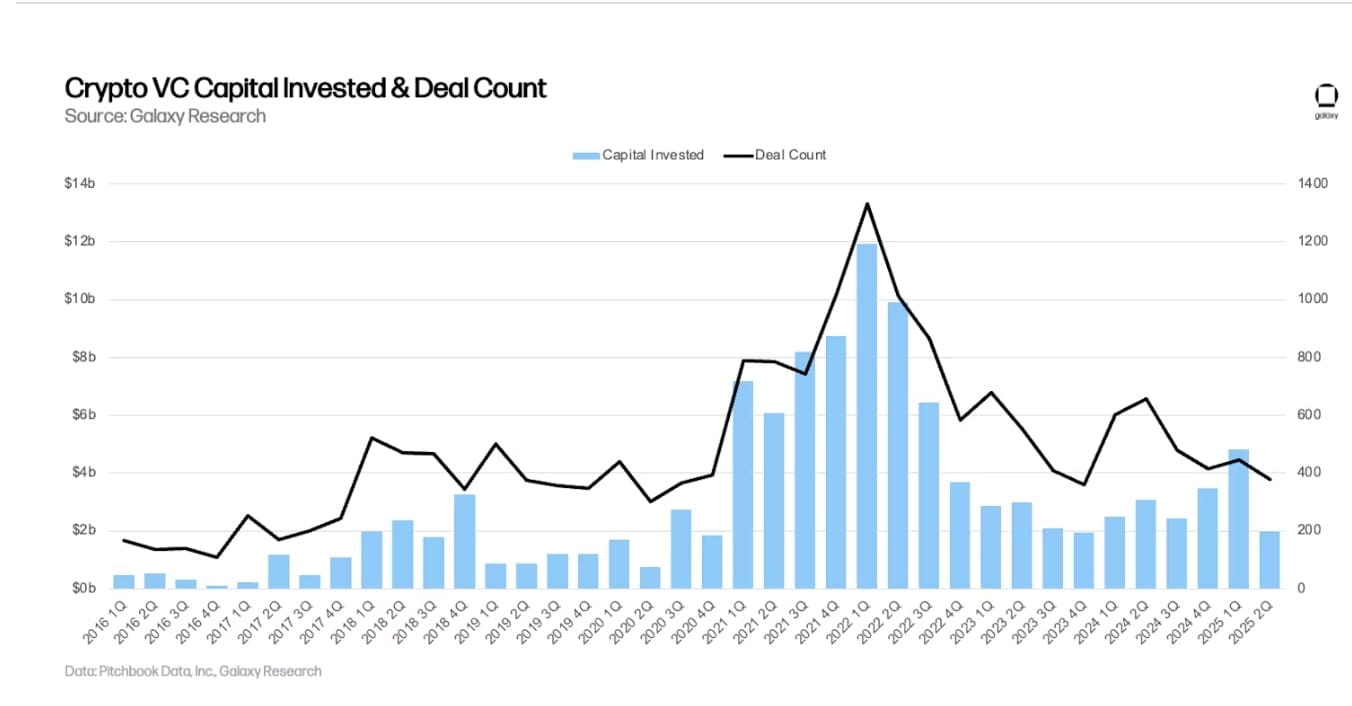

Investment flow into the cryptocurrency sector has decreased by 59% compared to the previous quarter, down to $1.976 billion in Q2, spread across 378 deals.

According to Galaxy's report, the last quarter was the second lowest investment quarter since Q4 2020.

Late-stage businesses dominate

Late-stage deals account for 52% of total investment, marking the second time since Q1 2021 that mature companies received more capital than early-stage startups.

The sharp quarter-over-quarter decline appears less severe when considering the unusual activity in Q1, including MGX's $2 billion investment in Binance. Excluding this deal, investment capital in Q2 only decreased by 29% compared to the previous quarter.

Galaxy Digital's report shows that venture capital investment in crypto remains low compared to previous bull cycles, despite Bitcoin's impressive price performance in 2025.

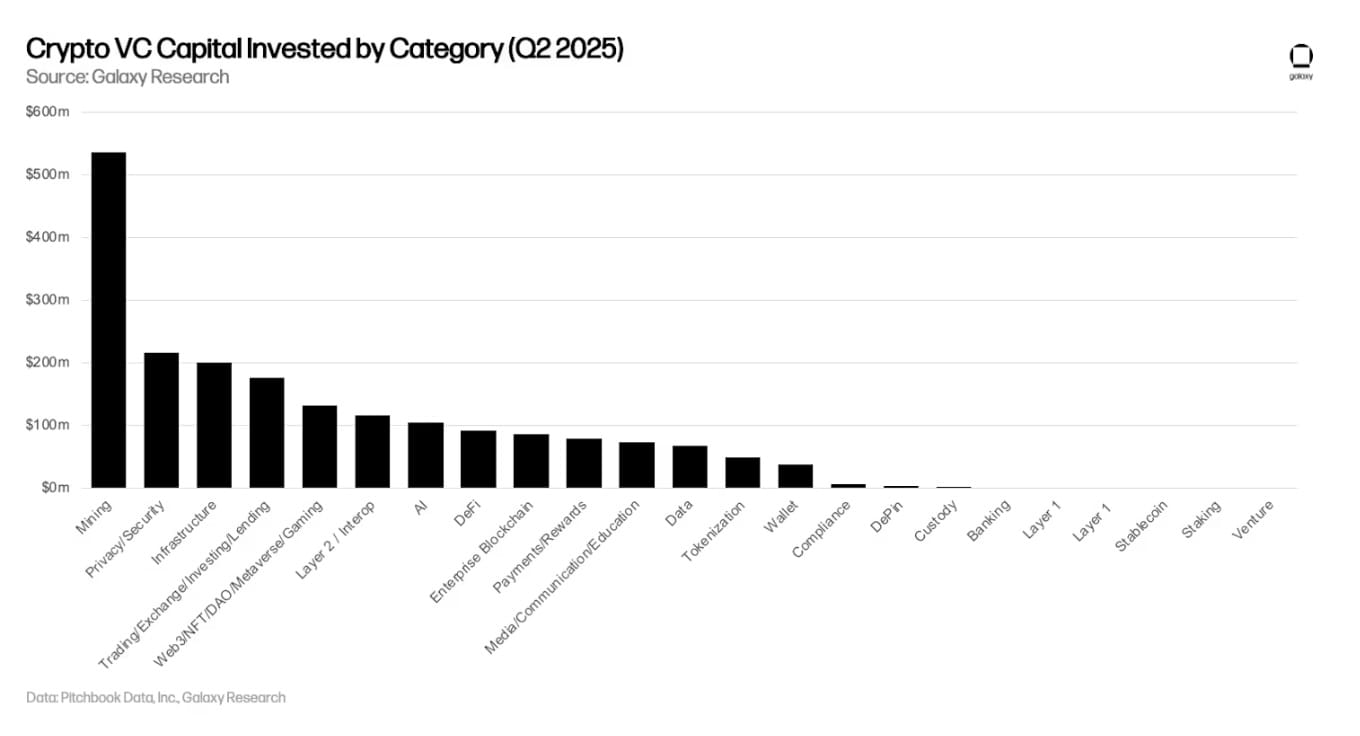

The mining sector becomes a bright spot

For the first time in years, mining companies accounted for the largest share of venture capital investment, over 20% of total disbursements. This sector received about $500 million, the majority coming from Sequoia's $300 million investment in XY Miners – a cloud-based mining company. This trend reflects the increasing demand for computing power driven by the robust growth of the artificial intelligence sector.

Distribution by region and stage

Companies in the U.S. continue to dominate the crypto startup ecosystem, receiving 47.8% of total investment and 41.2% of deals. The UK ranks second with 22.9%, followed by Japan with 4.3% and Singapore with 3.6%. The U.S. remains the crypto hub of the world.

The shift towards late-stage deals reflects the maturity level of the market, as many companies have achieved product-market fit and traditional corporations are beginning to adopt blockchain technology.

The proportion of pre-seed deals has continuously decreased as the industry gradually moves beyond the experimental phase. Companies established in 2018 accounted for the most capital raised, while those founded in 2024 led in the number of deals.

Challenges and competition

Fundraising activities of crypto venture funds continue to be challenging, with only $1.7 billion raised across 21 funds in Q2.

Macroeconomic factors such as high interest rates continue to dampen the incentive to commit capital to venture investments. Meanwhile, competition from spot Bitcoin ETF funds and digital asset management firms is providing alternative access channels for institutional investors looking to enter the crypto market.

Additionally, the report notes that the historical correlation between Bitcoin prices and venture capital activity has weakened over the past two years. Although Bitcoin has surged since January 2023, venture capital has not kept pace with previous cyclical patterns.

Decreased interest in once-popular fields such as blockchain gaming, NFTs, and Web3 applications has also contributed to the reduced appeal of venture investment strategies in crypto.

Outlook ahead

The report predicts that investment activity in crypto startups in the U.S. may improve thanks to industry-friendly policies from the new administration.

Clarifying the legal framework for stablecoins and market structure could pave the way for traditional financial institutions to participate more deeply in the crypto sector, thereby increasing the demand for investment capital across the ecosystem.