I would suggest that everyone should allocate some funds to DEFI. In the wave of DEFI and so-called RWA, identifying truly promising projects becomes very important.

Why I have a clear view of ENA and have been continuously monitoring this project.

1. Analysis from an investment research perspective

The role of dual-token protocols

1. How big is the expectation for the ENA project? Without considering the cost to the market makers and technical aspects, the main focus should be on what the ENA project ecology is actually doing.

--Without all the embellishments, ENA is a DEFI protocol for stablecoins, and is also a protocol similar to RWA. More importantly, it is backed by institutional support, hence the native stablecoin protocol, USDE.

--It is worth noting that USDE, the core value of ENA, is similar to Luna, but the demand for USDE is greater. Stablecoins are the only cryptocurrencies that can truly land apart from Bitcoin, and the number of stablecoins also represents the degree of blockchain prosperity. Most cryptocurrency projects' market caps are supported by stablecoins.

The role of ENA tokens and USDE

If the core of the ENA project is USDE, then the role of ENA seems somewhat decorative. However, as long as the allocated profits are high enough and the repurchased value is sufficient, the high price of ENA can attract many people to continue participating in USDE staking, and the expansion of USDe scales will drive protocol income, thus enhancing ENA's value.

The collaborative relationship between USDE and ENA

From a fundamental perspective, it can be concluded that compared to the strong anchoring relationship of Luna, ENA's so-called anchoring is relatively weaker. Meanwhile, the risk of a spiral decline in USDE's value is not as severe as that of Luna, at least with the current model of USDE. There is no risk of collapse as described.

Opportunities and risks of ENA and USDE

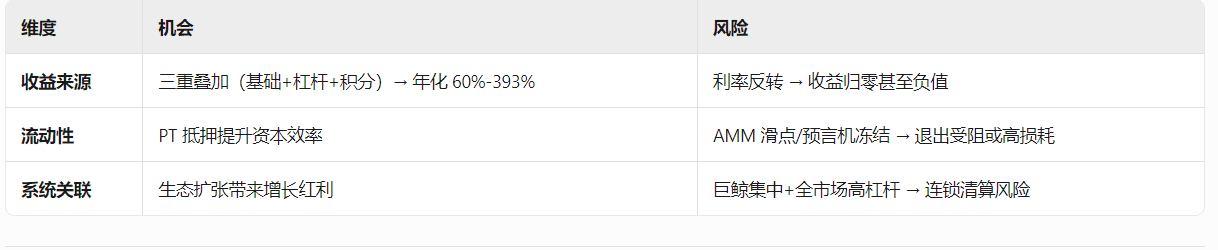

1. Opportunities

If the opportunity lies only in ENA and USDE, then as a DEFI, it is not particularly eye-catching and would not be called a small Luna. Its truly feasible core reason is:

USDe offers an annualized stable return of approximately 8.5% (funding rate + staking yield)

AAVE offers up to 9x leverage (LTV 88.9%), with a theoretical annualized return of over 60%

Pendle's PT-sUSDe used as collateral in AAVE achieves the conversion of 'yield rights → lending capital', enhancing the utilization of funds

The borrowing rate of USDe in AAVE is often lower than the PT yield, creating a stable interest margin

In simpler terms, AAVE, ENA, and PENDLE are three manufacturers that are becoming bubbles, forming an iron triangle that can anchor each other.

Through cyclical loans, 1 USDT can be cycled into 10x by minting usde → minting pt → depositing pt → borrowing usdt → minting usde, turning into $10 in deposits.

And this $10 deposit exists in three protocols. This $1 turns into $30 in deposits, a leverage of 1 to 30.

Is there a better opportunity than this?

2. Risks

Bubbles will eventually burst, so should we stay away from bubbles? Embracing bubbles while understanding roughly when and why they might burst is particularly important.

Yield collapse: If the bull market turns into a bear market, the perpetual contract funding rate turns negative, and the basic yield of sUSDe plummets (for example, during the AAVE crisis in July 2025, the borrowing rate for ETH soared to over 10%)

PT discount risk: The price of PT depends on market interest rate expectations. When actual yields fall below expectations, the secondary market can experience significant discounts (e.g., expected 10% → actual 5%, PT price may drop from 0.9 to 0.85)

AMM failure: Pendle's AMM is only efficient within the preset yield range; when market sentiment changes drastically, trading slippage spikes, and exit costs surge.

Concentration of whale liquidations: The top four whales hold 450M positions, and liquidation of a single account may trigger a chain reaction of sell-offs (e.g., in 2025, AAVE whales faced a loss of $3.58 million due to the plunge in ETH)

Market-wide leverage bubble: Current DeFi + CeFi collateral loans total $53.09 billion, close to the peak of the 2021 bull market, with a very high risk of liquidation resonance.

Once several situations of appeal occur, the market will begin to crash. The only chance for these leveraged whales to rescue themselves is to hedge by shorting DEFI projects in the market, such as ENA.

2. Analysis from a technical perspective

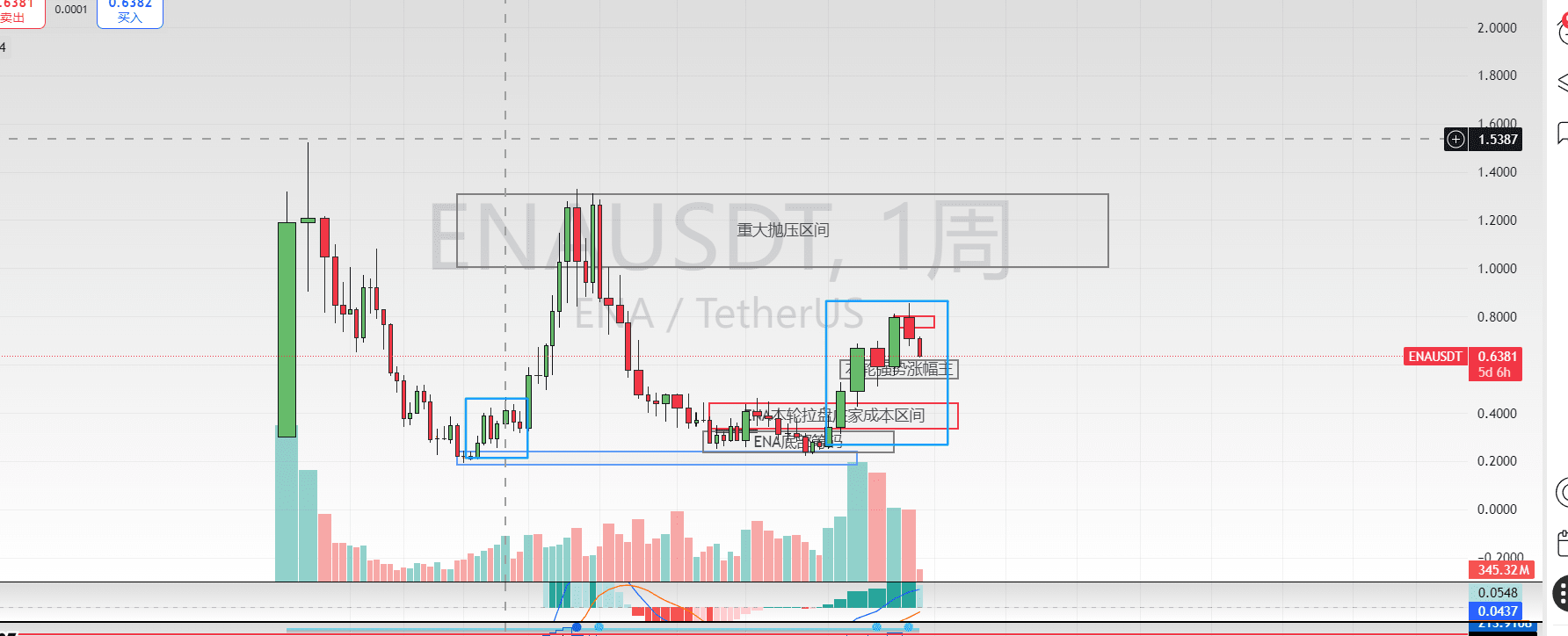

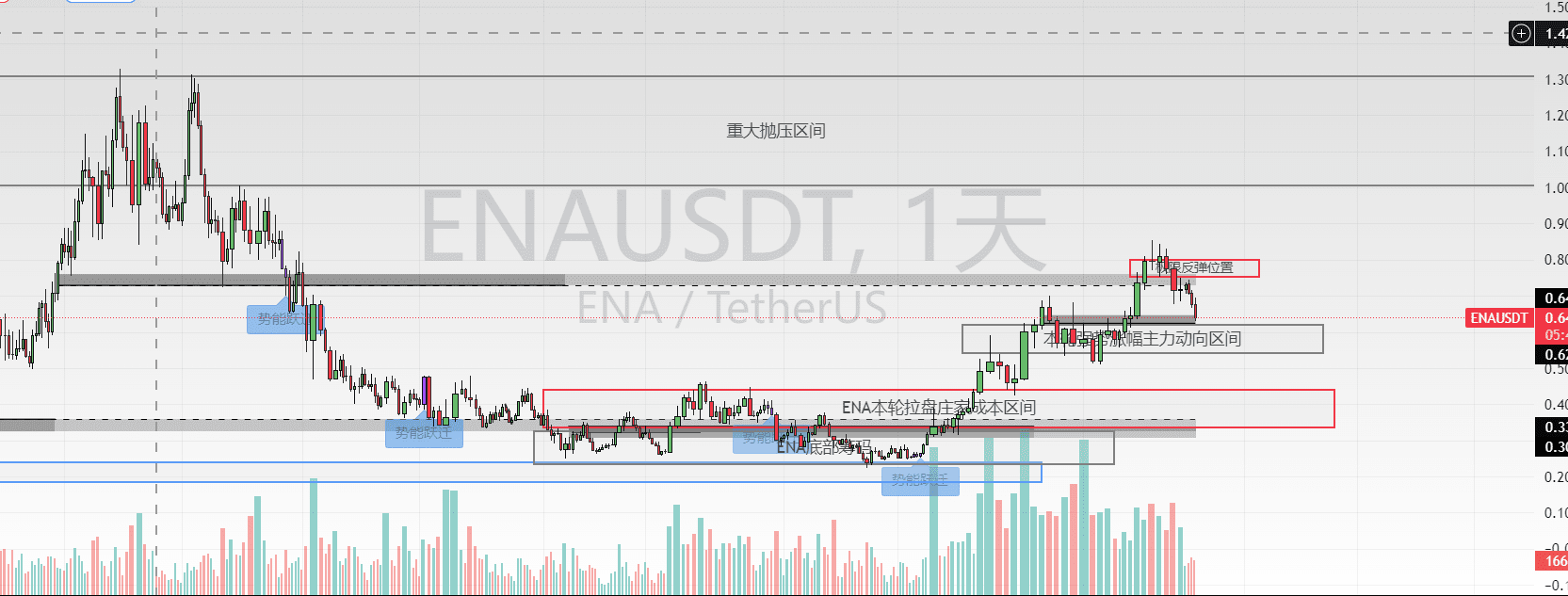

Regarding ENA's linear unlocking project, the selling pressure on the coin price seems limited. If a bull market arrives, then the main focus will be on ENA's main cost and pump expectations.

From a technical perspective, ENA has somewhat preemptively pumped, and the surge exceeded many people's expectations. Therefore, ENA's target is simple: since it has preemptively pumped to the 0.8 position, this indicates that after stabilizing from this pullback, there is a high probability of aiming for a surge to break through the chip position above 0.8.

The range between 0.55-0.61 has become a key strong position for ENA in this round. As long as it does not fall below this range, there is a chance to rebound and test the pressure position around 0.75, then observe the market's chip situation.

However, if a bull market really arrives, the early pump of ENA this round seems very intentional. Aiming for a very high peak is not out of the question, because if the monthly line stabilizes, and if the bull market indeed arrives with market rate cuts and liquidity, then ENA's monthly line should have a chance to impact the significant selling pressure area above.