I. The imagination of 24/7 trading: A new window for SME financing

Equity tokenization provides SMEs with unprecedented financing channels. By breaking equity into digital tokens that can be traded 24/7 on the blockchain, companies can lower financing thresholds and enhance liquidity. The introduction of smart contracts automates operations such as dividends and transfers, enhancing transparency and efficiency.

According to research by Yann Robard, a partner at Dawson Management, the private equity market has created value about three times that of the public stock market over the past 25 years. Many excellent companies delay or even bypass listing, obtaining billions of dollars in funding through multiple rounds of private placement financing. For example, OpenAI received $6.6 billion from investors such as Microsoft and SoftBank in October 2024, and in March 2025 completed a massive financing of $40 billion, becoming the largest private financing case in history. This demonstrates that ample financing support allows companies to remain unlisted or delay their listing, achieving more flexible strategic layouts. Theoretically, equity RWA can extend this financing advantage to global investors, efficiently resolving issues of insufficient early-stage funding and the inability to monetize brand value.

However, this convenient financing method highly relies on the platform's stability and compliance. Once problems arise on the platform, investor funds may be frozen, the company’s reputation may be affected, and subsequent financing opportunities may be jeopardized, ringing alarm bells for SMEs.

II. $6.2 million frozen: The 'seven terrifying days' of inaccessible funds

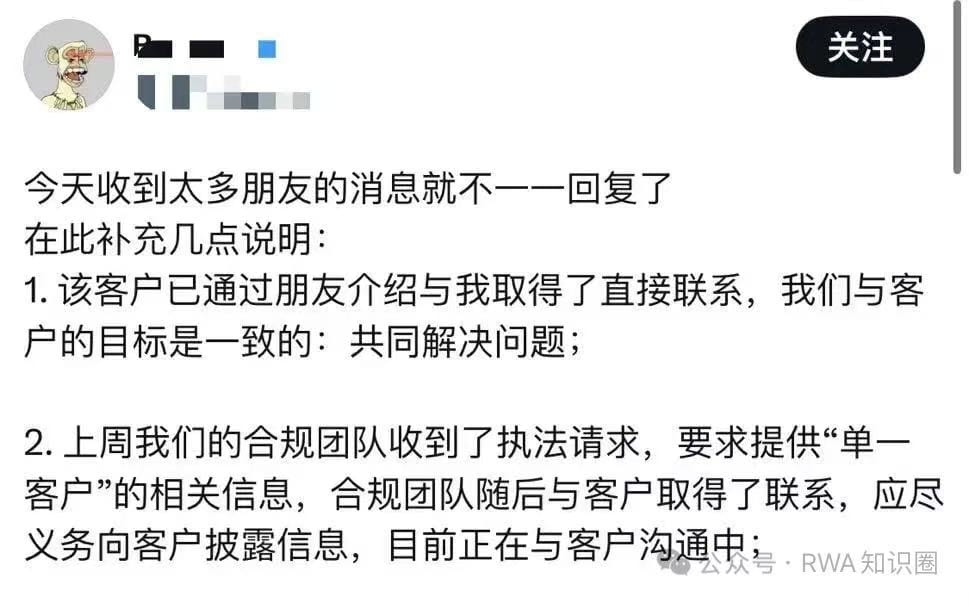

On August 7, the U.S. stock tokenization platform MyStonks announced an emergency upgrade, originally scheduled for completion at 11:30 PM that night, but it was delayed for 7 days. During this period, an investor publicly accused the platform of freezing his $6.2 million funds under the excuse of an 'AML investigation,' and the news quickly escalated, triggering a crisis of trust. It was not until late on August 14 that the platform restored the withdrawal function. The founder responded that this was a request from law enforcement agencies rather than an initiative from the platform, but this claim has not been externally confirmed.

For investors, this is a thrilling experience of trapped funds; for SMEs, such events serve as a warning. When choosing an equity tokenization platform, businesses must assess the platform's stability and compliance capabilities; otherwise, if problems arise, the losses may not only be investor funds but could also directly impact the company's financing credibility and reputation.

III. $575,000 filing and MSB license: Compliance ≠ endorsement

Compliance qualifications are an important aspect that SMEs need to pay attention to when conducting equity RWA. MyStonks constantly emphasizes 'we have MSB licenses and completed STO filing' during promotions, but a deeper analysis reveals that the actual protective effect of these qualifications is very limited.

According to data from the SEC official website, the Form D filed by MyStonks shows that its filing type is a private placement exemption under Regulation D 506(c), with an issuance scale of only $575,000, and an investment threshold starting at $50,000, limited to 'accredited investors.' In other words, this is just a small-scale private placement notification filing. The purpose of Form D is merely to inform the SEC 'I have conducted a private placement,' and does not imply obtaining any operating license, nor does it mean the SEC endorses the company's qualifications or project authenticity.

At the same time, the MSB license can also be easily misunderstood. The regulatory agency for MSB (Money Services Business) is FinCEN, under the U.S. Department of the Treasury, with the core responsibility of anti-money laundering (AML) and counter-terrorism financing (CFT). It requires platforms to report suspicious transactions regarding fund flows but does not take responsibility for the safety of investor funds, nor does it review the platform's business model or technological implementation.

For companies, if they mistakenly believe that having a filing or license means absolute safety, they may overestimate the platform's ability to provide guarantees. If the platform's actual operations deviate from the filing requirements, companies may face investor skepticism or compliance scrutiny.

IV. $50 million custody commitment: The black box under complex links

In addition to compliance qualifications, MyStonks also claims to have partnered with Fidelity to custody $50 million in assets, covering 95 U.S. stocks and 5 ETFs. On the surface, this seems to imply that asset safety is guaranteed, but a careful tracing of the details reveals several risk blind spots:

Lack of official confirmation: Fidelity has not publicly confirmed its partnership with MyStonks for custody services.

Lack of third-party audit: The platform has not disclosed external audit reports or off-chain proof documents, leaving investors to rely solely on the platform's statements.

The mapping from off-chain to on-chain is opaque: MyStonks claims '1:1 mapping of U.S. stocks,' but how this is achieved lacks disclosure. If the off-chain assets do not match the on-chain tokens, it may lead to the risk of 'tokens being valuable while assets are unbacked.'

For businesses, this 'opaque custody chain' has a significant impact. Because in the eyes of investors, the platform chosen by the company is the 'endorsement.' Once the platform's custody commitments are questioned, investors are likely to shift the blame to the company itself, believing that the company has chosen an unreliable platform, leading to funding risks. This situation not only damages financing credibility but may also burden the company with the reputational risk of 'misleading investors.'

V. The cost beyond $6.5 million: The necessary path from learning to practice

MyStonks event shows that the potential risks behind digital assets may far exceed the frozen $6.2 million. For small and medium-sized enterprises (SMEs), attempting RWA on platforms lacking transparency and compliance guarantees poses risks not only at the funding level but also potentially affects corporate reputation and future financing capabilities.

Equity tokenization is not a shortcut but a project that requires systematic understanding and professional execution. From compliance frameworks and public chain infrastructure to exchange licenses, custody, and clearing, every link cannot be ignored. If companies act rashly, risks may be amplified, and investor skepticism may also be transferred to the companies themselves.

Therefore, when attempting equity RWA, companies are advised to first engage in systematic learning and seek professional RWA accelerator support to ensure that each link is implemented. Only in this way can equity tokenization truly become a tool to facilitate growth rather than a potential burden.