Last Friday evening, Alice and Bob, along with Jay from The Kus, officially launched three WFC (Wish For Change) proposals on the Polkadot chain — three proposals aimed at reducing the DOT inflation model to varying degrees.

The community has actually been discussing inflation reduction for quite some time, especially among friends in the Chinese community. Now, after months of community discussion and off-chain proposal design, three specific on-chain proposals have entered the WFC voting phase. It is worth noting that these three proposals are not simple repetitions but have significant differences in details and mechanisms, which will profoundly affect DOT's long-term inflation path, staking rewards, and the flow of ecological funds.

This article will systematically sort out the design logic, specific parameters of the three proposals, and the potential impacts they may have on the future economic landscape of Polkadot.

Proposal 1: Hard Pressure — the most aggressive inflation tightening

Total supply cap: 2.1 billion DOT

Inflation reduction mechanism: reduce the remaining issuance by 13.14% every two years

First adjustment: March 14, 2026

Expected peak: 2160

Core feature: A one-time significant compression of inflation. On March 14, 2026:

Inflation will be directly reduced by 53.6%, from the current level down to 3.1%

Staking yield will drop to 5.6% (if the inflation allocation ratio for validators and treasury remains at the current 85%:15%)

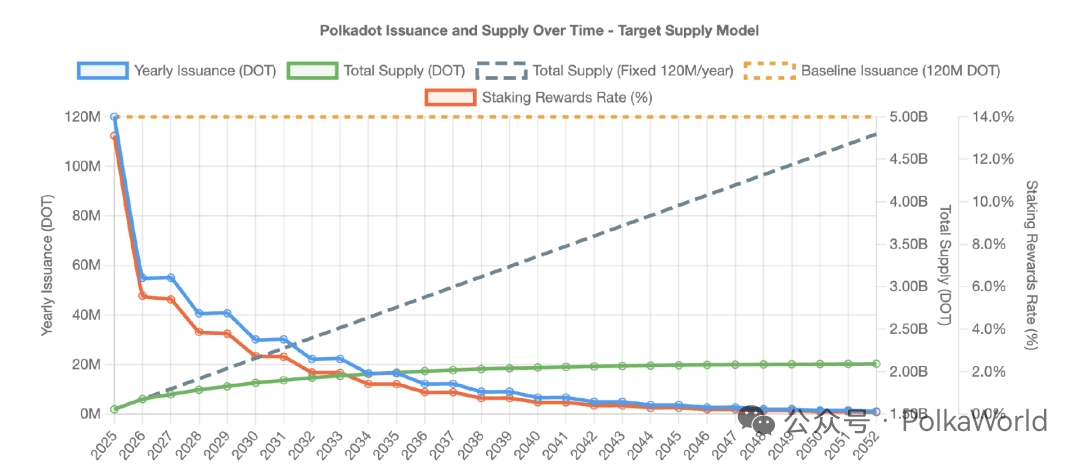

The following chart shows the issuance and total supply trends of DOT under Hard Pressure:

The blue line (Yearly Issuance): represents the annual new issuance under Hard Pressure. We can see that it remains around 120 million DOT in 2025, but rapidly declines starting in 2026, halving to below 40 million around 2030, eventually approaching zero after 2040.

The green line (Total Supply): represents the total supply of DOT. As inflation gradually decreases under Hard Pressure, the total supply approaches the cap of 2.1 billion, remaining almost unchanged after 2040.

The gray dashed line (Fixed 120M/year): if the current fixed issuance (120 million DOT per year) is maintained, the total supply will approach 5 billion DOT around 2050, far exceeding the levels under the tightening model.

The orange dashed line (Baseline Issuance): represents the annual new issuance of maintaining the current fixed issuance — i.e., a constant 120 million issuance, used to compare the changes after tightening.

The orange line (Staking Rewards Rate): represents the staking yield (if the inflation allocation ratio for validators and treasury remains at the current 85%:15%). With the tightening of issuance, staking returns decline from double-digit levels in 2025, year by year, falling below 5% around 2035, and maintaining at extremely low levels after 2040.

This chart intuitively illustrates why this model is called the 'Hard Pressure' proposal, as it significantly compresses the annual issuance of DOT in the short term and locks the total supply in the long term, leading DOT towards an asset logic of nearly fixed supply.

Additionally, it's important to note that under this model, all DOT inflation and protocol revenue (such as Coretime, Hub, service fees, MEV, etc.) will enter a revenue pool. Rewards for validators/stakers will no longer be directly tied to inflation but will be paid from the revenue pool. This can decouple 'security spending' from 'inflation issuance' and avoid infinite inflation.

In this revenue pool:

What proportion goes to the treasury

Will the treasury destroy a portion of the funds

What proportion of the fees are destroyed

Destruction ratio of Coretime

Minimum price (floor price) of Coretime

Future ecological growth incentives (such as subsidies for DeFi or parachains)

These ratios and parameters can be decided through voting in OpenGov!

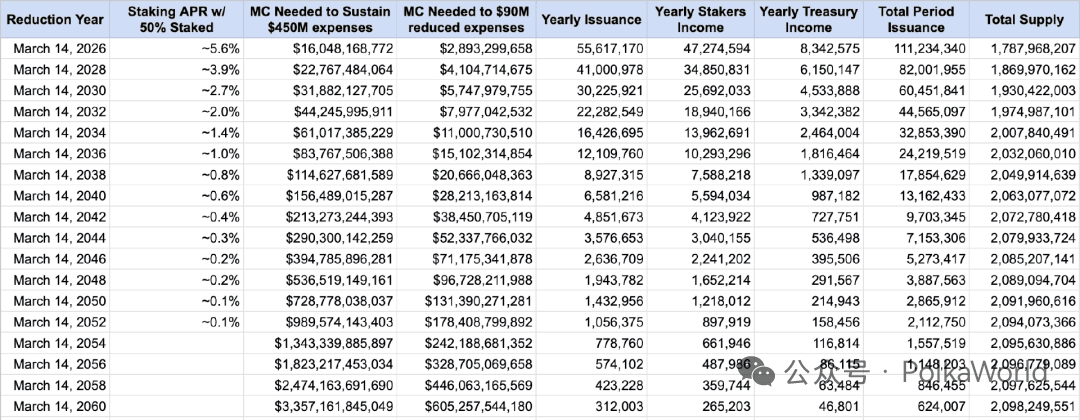

If the inflation allocation ratio for validators and treasury remains at the current 85%:15%, then if we calculate based on an annual network security spending of $450 million, DOT needs to rely on rapid market cap growth to support network expenses:

Market cap needs to catch up with SUI (price > $10) by 2026.

Catch up with ADA by 2030, and catch up with SOL by 2038.

If network expenses can be reduced to $90 million/year, the situation is relatively relaxed:

The current market cap can support network security until 2031,

But needs to catch up with LINK by 2037 and SOL by 2049.

However, based on the current situation of Polkadot, it is difficult to introduce PoP in a short time to directly replace NPoS, so boosting DOT's market cap is still an important task. It is necessary to maintain the DOT price above $10 when starting to significantly reduce inflation in 2026 (assuming validators can receive 85% of the inflation ratio).

So, if OpenGov decides to allocate DOT inflation proportionally to validators, treasury, and incentive parachains, say at a ratio of 50:15:35, then based on an annual network security spending of $450 million, the price of DOT would need to reach around $15 to support the network's expenses!

Therefore, placing all DOT inflation and protocol revenue into the revenue pool and then adjusting through OpenGov provides more flexibility for the entire ecological fund allocation and market regulation.

Voting link: https://polkadot.subsquare.io/referenda/1710

Proposal 2: Soft Pressure — a relatively mild inflation path

Total supply cap: 3.14 billion DOT

Inflation reduction mechanism: reduce the issuance of the previous cycle by 13.14% each time

First adjustment: March 14, 2026

Expected peak: 2160

Core feature: Retain a longer fund release cycle while reducing inflation.

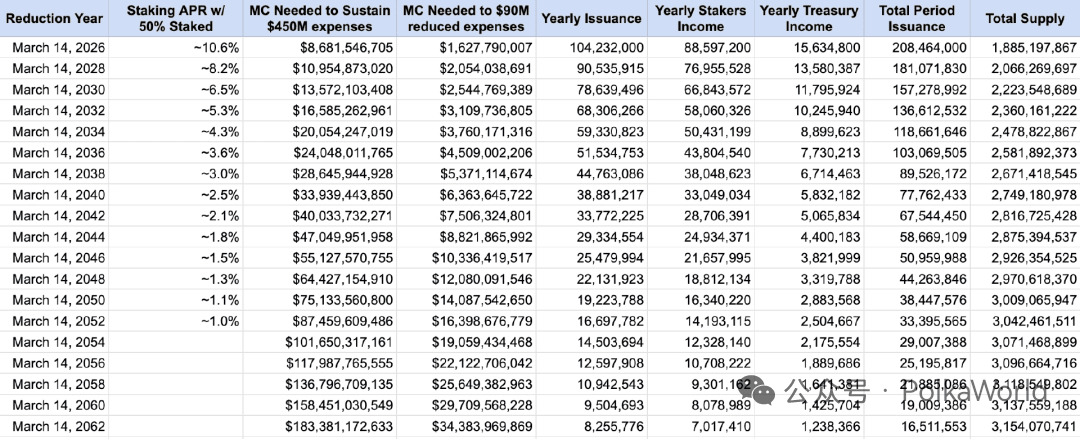

On March 14, 2026, inflation will drop to 5.5%.

Staking yield drops to 10.6%, if the inflation allocation ratio for validators and treasury remains at the current 85%:15%.

If maintaining $450 million/year in spending, DOT needs to continuously grow its market cap:

Market cap needs to catch up with AVAX (price around $7) by 2028.

Catch up with LINK by 2032, ADA by 2040, USDC by 2050.

If spending is only $90 million/year, the current market cap can be maintained until 2040:

Catch up with AVAX by 2046, LINK by 2052.

Similarly, the estimate here is calculated based on the current inflation allocation ratio of validators and treasury, maintaining 85%:15%. This proposal will also channel all DOT inflation and protocol revenue (such as Coretime, Hub, service fees, MEV, etc.) into the revenue pool. Specific allocation parameters will be decided by Polkadot OpenGov!

Voting link: https://polkadot.subsquare.io/referenda/1709

Proposal 3: Growth Pressure — dual-track system of inflation reduction + incentive growth

This proposal was put forward by Alice and Bob, who believe that simply suppressing inflation is dangerous. Although the first two proposals are good, they have a common problem: they only address the supply side and do not touch the demand side. If we remove the incentives for staking DOT and there are no outlets or productive uses for DOT, it may become idle, further reducing demand for DOT, lowering prices, and further undermining the motivation to hold DOT, ultimately pushing DOT onto a dangerous downward trajectory. As for how much additional demand can be generated by the psychological effect of a 'total supply cap', this is purely speculative. For an asset worth tens of billions of dollars, such risks are too great.

The main problem with the current token economy is not too much supply, but too little demand. There are almost no incentives for using DOT on parachains, and worse, the ridiculously high staking yield itself is a form of 'disincentive', preventing DOT from flowing to parachains. Even if inflation is halved, this problem will not be eliminated.

The main driving force for DOT demand can only come from the economy itself. And in Polkadot, parachains are the economy. But the reality is that currently only 0.7% of DOT is used for economic activities on parachains, while 54% is staked and 45% is idle. In other words, the economy of DOT is almost non-existent.

Therefore, to create demand for DOT, simply tightening the supply curve is not enough; we need to actively create demand drivers.

To this end, it is necessary to design 'policy levers'. The 'Growth Incentives' pool is such a lever.

This proposal suggests introducing such a mechanism: establish a new account to receive a portion of the inflation share, which will not go into staking rewards or the treasury. OpenGov can decide how much to allocate for staking rewards and guide the excess portion into this buffer fund.

This proposal advocates that the buffer fund will stimulate economic growth through an algorithmic mechanism or flow back to staking rewards when needed. By introducing a growth incentive pool that can only be allocated indirectly and algorithmically rather than directly by OpenGov, Polkadot will retain an important economic policy tool.

Currently, Polkadot's inflation allocation method is:

• 85% → Staking rewards

• 15% → Treasury revenue

After introducing new accounts and variables controlled by OpenGov, the allocation method can change, for example:

• 45% → Staking rewards

• 15% → Treasury revenue

• 40% → Buffer fund

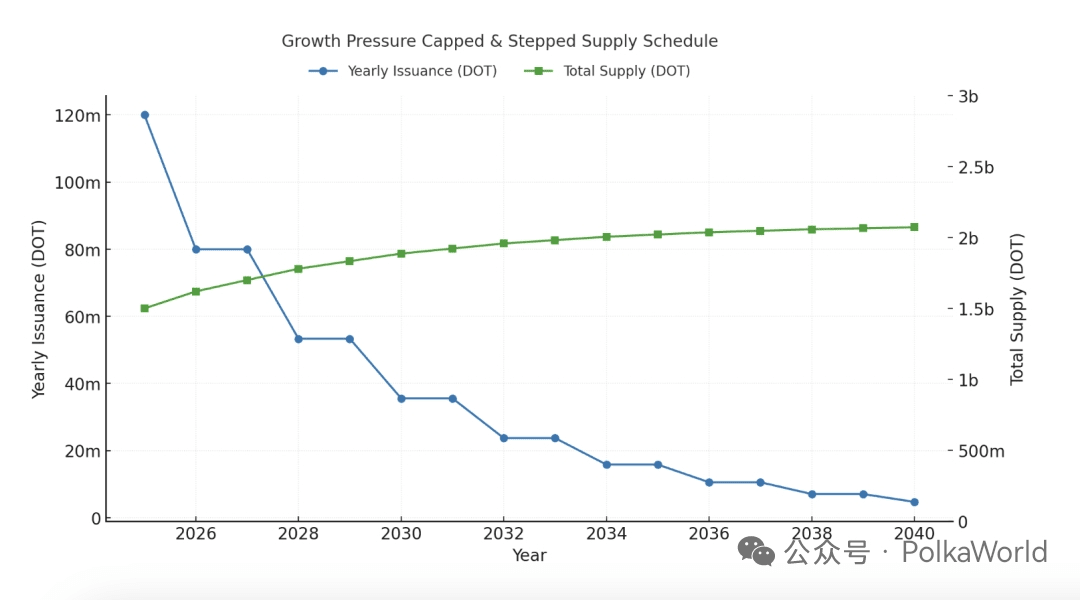

So, the overall suggestion of this proposal is:

Total supply cap: 2.1 billion DOT

Inflation reduction mechanism: tiered reduction every two years, inflation decreases by 33%, and staking rewards also decrease by 50%!

First adjustment: March 14, 2026

Additional mechanism: Excess DOT will enter the incentive pool for parachain economic growth.

Core feature: Balance between tightening and growth incentives. On March 14, 2026:

DOT inflation will fall to around 4.2%;

According to the tiered reduction logic, in 2026, 80 million DOT will be issued, and if based on a 85:15 ratio for validators and treasury, then stakers will receive 68 million;

If half of the funds need to be allocated to the incentive pool, that is, 34 million DOT used to support parachain economic activities;

Based on an annual network security spending of $450 million, the price of DOT would also need to reach around $13 to support network expenses!

Of course, this proposal does not set specific parameters, and adjustments can be made later through OpenGov. In short, this proposal emphasizes that DOT's inflation should no longer all flow into purely staking rewards and the treasury, but a portion should be converted into fuel for ecological growth.

PS: I actually think the issue emphasized in this proposal of converting a portion of DOT inflation into fuel for ecological growth can also be addressed by Proposal 1. The biggest difference is that Proposal 1 reduces inflation by 53%, while Proposal 3 reduces it by 33%! The specific proportion of inflation allocated to network security and how much DOT's market cap needs to be maintained can be adjusted through OpenGov.

Voting link: https://polkadot.subsquare.io/referenda/1711

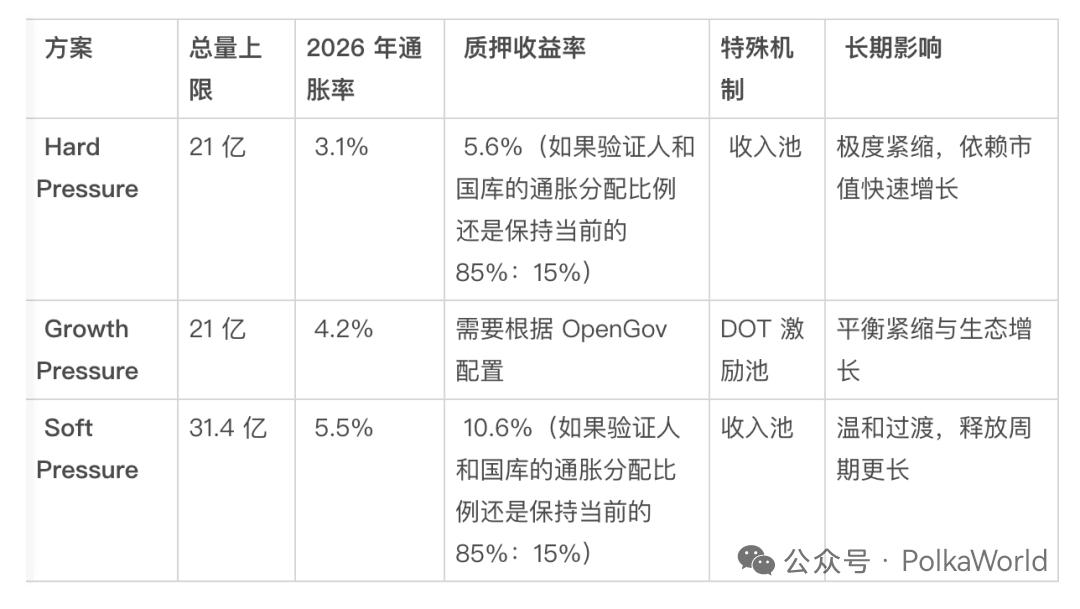

Comparison of the three major proposals

Conclusion

Currently, voting for the three major inflation proposals has opened simultaneously, and community members can express their positions through OpenGov. Whether it’s aggressive tightening, growth-driven, or a moderate transition, each path corresponds to different ecological expectations and market signals.

This is not just a vote on the inflation rate, but a choice about the future narrative and development strategy of Polkadot.

🗳️ Voting is ongoing, which one will you choose?

Hard Pressure: https://polkadot.subsquare.io/referenda/1710 Soft Pressure: https://polkadot.subsquare.io/referenda/1709 Growth Pressure: https://polkadot.subsquare.io/referenda/1711