Author: Xiaozhu Web3

Introduction

On August 12, 2025, pre-market, Circle, the 'first stablecoin stock' in the U.S., released its first financial report since going public: as of June 30, USDC's circulation reached $61.3 billion, a 90% increase compared to the same period last year.

Thanks to the significant increase in USDC circulation, revenue and reserve income reached $658 million, a 53% year-on-year growth. The financial report also showed that Circle had a net loss of $482 million, primarily due to two non-cash expenses related to the IPO, including employee stock award costs attributable at the time of the company’s listing and the increase in the valuation of convertible bonds due to stock price appreciation. Following the report, Circle's pre-market stock price quickly rose nearly 14%.

On July 31, the 'first cryptocurrency exchange stock' Coinbase released its second quarter financial report, showing profits soaring to $1.4 billion, far exceeding last year's profit of $36 million, primarily due to its substantial gains from investing in Circle. However, core business performance was weak, and revenue fell short of Wall Street expectations, leading to a more than 16% drop in stock price the next day, dragging Circle's stock price down by over 8%.

The partnership between Circle and Coinbase is one of the most notable strategic alliances in the cryptocurrency space. If we compare USDC to a circle, Circle and Coinbase can be likened to the two legs of a compass; the two companies have formed a unique symbiotic relationship within the USDC stablecoin ecosystem through a carefully designed business structure.

Circle's Past and Present

In 2012, Coinbase was founded in Delaware, USA, by former Airbnb engineer Brian Armstrong and former Goldman Sachs trader Fred Ehrsam, with its earliest product being a Bitcoin wallet. The following year, Circle was founded by Jeremy Allaire in Boston, USA, launching the Bitcoin payment product 'Circle Pay' to help investors 'more easily convert, store, send, and receive Bitcoin and other digital currencies.'

In 2013, Coinbase began its foray into cryptocurrency exchanges, becoming one of the earliest cryptocurrency exchanges. In 2015, Coinbase became the first licensed cryptocurrency exchange in the United States. In 2017, Circle acquired the U.S. compliant exchange Poloniex for approximately $400 million, entering the exchange business and forming three major business lines: exchange, OTC, and its original payment business.

In 2018, Coinbase and Circle jointly founded the Centre Consortium to collaborate on the launch of the USDC stablecoin. USDC is co-owned by Coinbase and Circle, and in terms of USDC revenue distribution, USDC on the Coinbase platform earns 100% of the reserve interest income for Coinbase, while USDC outside the Coinbase platform is split 50% each between Coinbase and Circle in reserve interest income.

In 2019, Circle shut down all three major business lines, fully focusing on the operation of the Centre Consortium. On April 14, 2021, Coinbase went public on the NASDAQ in the U.S., with a market value that once reached $100 billion after its IPO, becoming the first publicly listed cryptocurrency company in the U.S.

In March 2023, Circle held some reserves in Silicon Valley Bank, which collapsed, causing USDC to briefly de-peg to $0.87. In August, Circle and Coinbase restructured their partnership: the Centre Consortium was dissolved, and Circle acquired the remaining shares of Coinbase in it, becoming the sole issuer of USDC, while Coinbase retained a portion of Circle's equity as a strategic investor and maintained the revenue-sharing agreement.

On May 5, 2025, Coinbase was approved for inclusion in the S&P 500 index. On June 5, 2025, Circle successfully listed on the New York Stock Exchange, with an issue price of $31 per share. On its first day of trading, it began a rapid rise, reaching a peak of $298 on June 23, nearly a tenfold increase, with a market value surpassing its reserve asset value. Circle's listing also became the largest cryptocurrency company IPO since Coinbase's IPO in 2021 and the first large IPO conducted by a stablecoin issuer.

Coinbase and Circle have formed a symbiotic relationship in the USDC ecosystem, with Coinbase providing critical distribution channels and liquidity support for USDC, while Circle is responsible for issuance and compliance.

In terms of financing, from 2013 to 2016, Circle completed four rounds of financing, raising a total of $136 million, and following the D round in 2016, it was valued at $480 million. In 2018, Circle completed $110 million in E round financing led by Bitmain, with a valuation of $3 billion. In 2022, Circle brought in important partner BlackRock as the USDC reserve fund manager and completed $400 million in F round financing led by BlackRock, with a valuation of $7.7 billion.

In terms of revenue, Circle's income for 2024 relies 99% on investment income from reserve fund investments and bank deposit interest, totaling $1.661 billion. Of this, 90% of the reserves are managed by BlackRock's fund for investments in U.S. Treasury securities maturing within 93 days, while the remaining 10% is deposited at Bank of New York Mellon as bank deposits. Due to the revenue-sharing agreement with Coinbase, Circle will pay Coinbase $908 million in shares in 2024, accounting for 54.2% of its revenue.

From a compliance perspective, Circle holds MTL licenses in 46 states, including New York DFS BitLicense; in the EU market, Circle is the first stablecoin issuer to obtain a MiCA compliance license, allowing USDC and EURC (the euro stablecoin issued by Circle) to circulate legally in the EU; Circle has also received approval from Singapore's MAS. In some countries and regions, although licenses have not yet been issued, the legality of USDC has been recognized, such as in Thailand, Argentina, Japan, Brazil, and Mexico.

Circle's Future — CPN

Circle's January report (2025 State of the USDC Economy) has clarified the future development of Circle and USDC, which is to replace outdated global payment channels — such as SWIFT and ACH — with the Circle Payments Network (CPN).

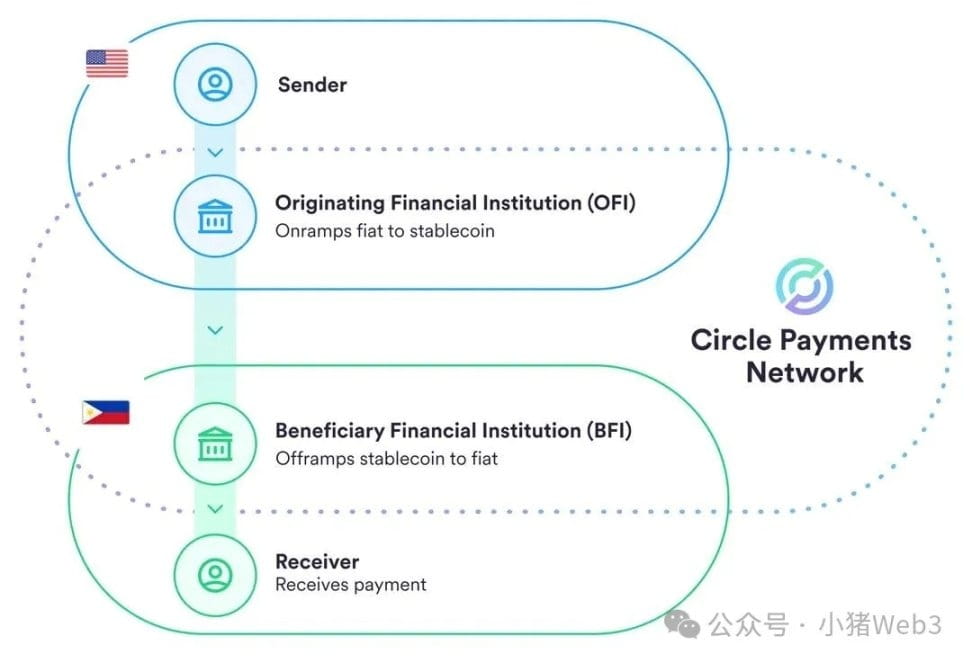

SWIFT and ACH were established in 1977 and 1972, respectively. Today, global communications have undergone a complete transformation, allowing people to connect instantly worldwide, but global payments remain stuck half a century ago. This is reflected in extremely high transaction costs (0.1% remittance fees and fixed remittance communication fees), long transaction delays (1 to 6 business days), significant transaction friction (exchange rate friction), and the financial inclusion issues faced by many who cannot access the global banking system.

The emergence of stablecoins can utilize the innovative achievements of blockchain networks to improve the global banking and financial system. Circle is building a value internet based on stablecoins to upgrade the global financial network, which is referred to as the CPN mentioned above. CPN connects leading global banks, payment service providers, and other institutions, with USDC, the world's largest regulated stablecoin, at its core, linking all participants in a real-time global settlement system with extremely low transaction costs and global accessibility.

Circle serves as the primary governance and standard-setting body for CPN, as well as the network operator. Through CPN, Circle is building a new platform and network ecosystem that will create value for every stakeholder in the global economy, helping to accelerate the benefits of this new financial system based on the internet for society. These stakeholders include:

Businesses: importers, exporters, merchants, and large enterprises: can utilize financial institutions supporting CPN to eliminate significant costs and friction, strengthen global supply chains, optimize capital management operations, and reduce reliance on expensive short-term operating capital financing.

Individuals: remittance senders and receivers, content creators, and other individuals who frequently send or receive small payments: will gain greater value, as financial institutions utilizing CPN can provide these enhanced services faster, at lower costs, and more simply;

Ecosystem builders: banks, payment companies, and other providers: can leverage CPN's platform services to develop innovative payment use cases, utilizing the programmability of stablecoins, SDKs (software development kits), and smart contracts to create a thriving ecosystem. Over time, this will fully unlock the potential of stablecoin payments for businesses and individuals. Additionally, third-party developers and companies can introduce value-added services to further expand the network's capabilities.

Many companies have already joined CPN, such as the Latin American bank Nubank, one of Africa's largest fintech companies Chipper Cash, global payment service provider Worldpay, U.S. payment giant Stripe, and Hong Kong stablecoin sandbox participant Round Coin Technology.

Compliance: A Brief Discussion on Hong Kong (Stablecoin Regulation)

In the global banking and financial system, compliance is paramount, which is why Circle places compliance first and actively applies for licenses worldwide. Circle's compliance must meet local government requirements, which usually manifest as follows:

Issuance/Redeeming Phase: Ensure KYC/AML, ensure the use of a 'full reserve model', ensure reasonable redemption periods;

Circulation Phase: Real-time transaction screening, continuous monitoring, and fulfilling obligations to regulatory authorities (e.g., freezing accounts).

On August 1, 2025, Hong Kong's (Stablecoin Regulation) officially took effect, with KYC verification requirements becoming a focal point of controversy. According to HKMA requirements, stablecoin issuers must not only verify user identity information and retain data records for over five years, but they also cannot provide services to anonymous users. This means that Hong Kong's stablecoins may initially lack the ability to interact directly with DeFi protocols, and decentralized wallets and unlicensed addresses will be isolated from the compliance framework. Such interactions will also be legally regarded as 'unauthorized use.'

It can be seen that compared to the scalability and freedom of on-chain protocols, Hong Kong regulators focus more on controlling the regulatory power during the stablecoin circulation phase. Although Circle's USDC also undergoes real-time transaction screening and ongoing monitoring in the circulation phase, this does not significantly affect wallet transfers and DeFi protocol interactions. This move effectively excludes ordinary users from using Hong Kong compliant stablecoins and also means that Circle's USDC is unlikely to obtain a compliant stablecoin license in Hong Kong.

In the author's view, ordinary users should continue to use USDT/USDC; Hong Kong's stablecoins cannot directly compete with USDT/USDC in scenarios like wallets and DeFi. The advantage of Hong Kong stablecoins or compliant stablecoins in other countries or regions lies in compliance scenarios controlled by the government, which inevitably limits USDT/USDC, for example, in the purchase of tokenized securities or other RWA tokens in cooperation with the Hong Kong Stock Exchange, where strict KYC and identity verification are required.

If we focus on the stablecoin payment network, there will be a significant impact. For example, user A in Hong Kong pays in Hong Kong dollars, and merchant B in the U.S. receives U.S. dollars converted at the corresponding exchange rate. In fact, the participants in the stablecoin trading and settlement process are Hong Kong payment company R (such as Round Coin Technology) and U.S. acquiring company S (such as Stripe), both of which are institutional users capable of meeting KYC verification conditions. Of course, user A also needs KYC, but follows the KYC system of stored-value payment licenses.

The real question is why they would use a market-accepted but more restricted Hong Kong dollar stablecoin in their trading and settlement processes. Clearly, if they used the widely adopted USDC, it would be easier for U.S. acquiring company S to accept, but there exists the step of payment company R using Hong Kong dollars to exchange for USDC during the payment process. They could either mint Hong Kong dollar stablecoins with Hong Kong dollars and then exchange USDC off-chain, which poses legal risks; or they could simply have an OTC license business, where the Hong Kong dollar stablecoin cannot participate.

Summary

Circle and Coinbase form a symbiotic relationship around USDC: they co-founded Centre in 2018, and after the 2023 restructuring, Circle exclusively issues USDC, while Coinbase acts as a strategic shareholder and shares reserve interest. Circle builds a value internet based on USDC as a foundational layer, with future strategies focusing on CPN to replace traditional global payment systems like SWIFT. If we compare USDC to a circle, Circle and Coinbase are the two indispensable legs of a compass.

The newly implemented Hong Kong (Stablecoin Regulation) KYC requirements may limit Circle's development in the Hong Kong market, but it also restricts the use of local stablecoins in the stablecoin payment network. From a legislator's perspective, strict KYC to combat money laundering and prevent financial risks is understandable, but it also leaves some room.

Looking at the development of mobile payments, it is actually financial technology companies like Alipay that, through their business models or innovations, force financial regulatory agencies to introduce new regulatory policies or rules to respond to the challenges posed by digital payments and fintech. The future payment field of stablecoins may see the emergence of a new 'Alipay', and perhaps we will witness history repeating itself.