In June this year, internet brokerage giant Robinhood launched a new service for European users, providing trading opportunities for 'stock tokens' of top unlisted unicorn companies like OpenAI and SpaceX. Robinhood even airdropped a small number of OpenAI and SpaceX tokens to eligible new users as a means of attracting them.

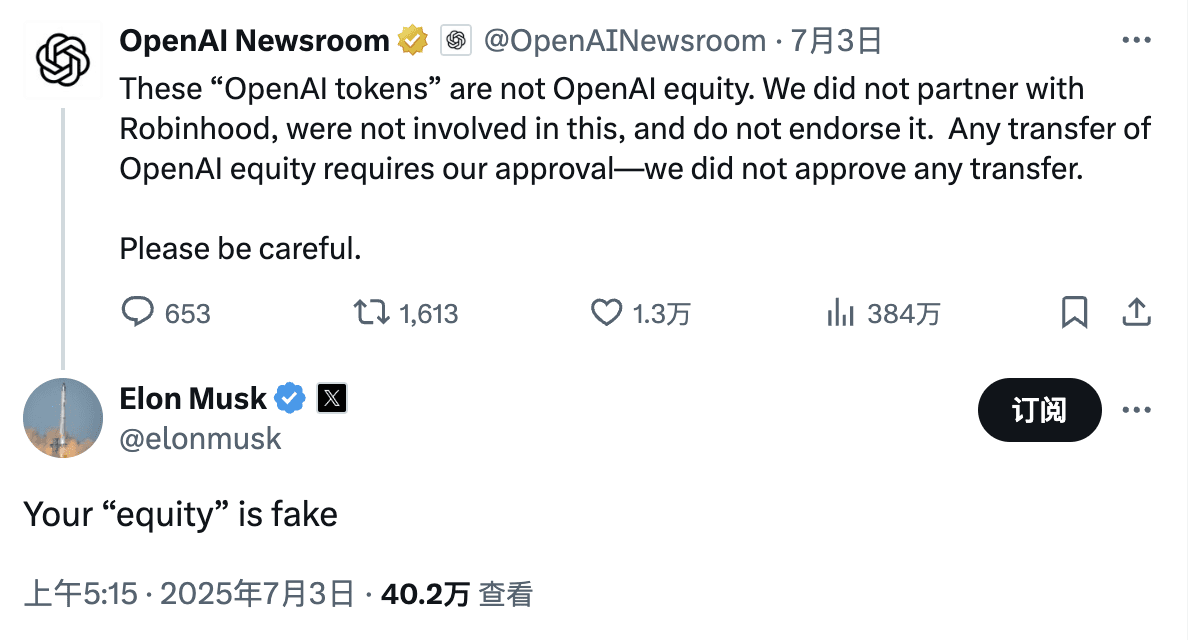

However, this move was immediately opposed by OpenAI. The official OpenAI account clarified on X, stating, "These OpenAI tokens do not represent equity in OpenAI, and we have no partnership with Robinhood." Under this message, Elon Musk did not directly comment on Robinhood's tokens, but he retweeted and remarked on OpenAI's statement, sarcastically saying, "Your own 'equity' is the fake one." This jest not only mocks OpenAI's capital operations after becoming a profit-oriented institution but also subtly highlights the strong resistance of unlisted companies to the loss of 'pricing power' over such shares.

Despite the skepticism, traditional brokerage attempts reflect strong market interest in on-chain Pre-IPO asset trading. The reason is simple: the enormous profits in the primary market have long been held by a few institutions and high-net-worth individuals, with many star companies experiencing exponential valuation growth when going public (or being acquired). Take design software company Figma as an example; after failing to complete its acquisition by Adobe due to antitrust reasons, Figma went public independently in 2025, with an offering price of $33 per share, which soared to $115.5 on its first day of trading, surging by 250%; this price corresponds to a market value of nearly $68 billion, far exceeding the previous $20 billion valuation during Adobe's acquisition talks. Similarly, the recently listed crypto exchange Bullish surged by 290% after opening. These cases indicate that investing in such companies before they go public may yield multiples or even tens of times returns. However, under traditional circumstances, it is relatively difficult and complex for ordinary investors to participate in such opportunities. Enabling retail investors to share in the appreciating dividends of future star companies through blockchain is precisely what makes the concept of on-chain Pre-IPO appealing.

The scale and barriers of the private equity market

Over the past few decades, the global private equity market has seen massive scale and rapid growth, yet it remains highly closed off. According to a survey by Yann Robard of Dawson Partners in the article 'Why Private Equity Wins: Reflections on a Quarter Century of Outperformance,' the value created by the private market over the past 25 years is about three times that of the public stock market during the same period. Many outstanding companies delay or even bypass going public, raising billions of dollars through multiple rounds of private financing. For example, OpenAI received $6.6 billion in investments from Microsoft, SoftBank, and others in October 2024, followed by another $40 billion funding round in March 2025, making it the largest private financing case in history. With ample private funds, many companies can remain private for a long time or choose not to go public at all. As a result, significant growth dividends are generated before the company goes public, yet only institutional investors can participate in these gains, leaving ordinary people completely excluded.

A comparison chart of value creation in the private equity market versus the public stock market over the past 25 years, source: Dawsonpartners

Traditionally, a few secondary trading platforms aimed at wealthy investors (such as Forge and EquityZen in the U.S.) have offered limited channels for the transfer of Pre-IPO shares. However, these platforms generally adopt a peer-to-peer matching model, with high trading thresholds, usually only targeting accredited investors, often requiring a minimum investment of tens of thousands of dollars. This kind of OTC model leads to poor market liquidity, a lack of pricing discovery mechanisms, and low trading efficiency. Moreover, many unicorn companies have highly restrictive articles of association regarding share transfers, and employees or early shareholders often need company approval to sell their shares.

Under the existing regulatory framework, the secondary market for private equity is almost closed off to ordinary investors. However, this barrier is slowly opening some 'gaps.' For instance, in June this year, the Nasdaq Private Market (NPM) launched Tape D, a real-time dataset of private companies that enhances price transparency and valuation visibility for private and pre-IPO companies. Users can access desired information through API interfaces. This also provides a relatively fair environment for 'oracles.'

The Pre-IPO market has not appeared for the first time in the crypto field. In recent years, this model has struggled to scale due to technical performance constraints, compliance environments, and insufficient investor education. However, the situation is gradually maturing, with significant improvements in blockchain scalability and user experience, as well as increasingly complete infrastructure for custody, KYC/AML, etc. At the same time, AI and crypto companies are frequently nearing their IPO points, providing new narratives and investment demands for early involvement in these high-growth targets. Compared to locking funds into highly volatile crypto assets, Pre-IPO tokenized products offer structured and predictable exit paths in addition to speculation, attracting more funds seeking diversified allocations.

More importantly, millennials and Gen Z are becoming the main investment force, showing a preference for direct investments, frequent trading, and actively seeking high-potential private equity opportunities such as SpaceX, OpenAI, and Anthropic. However, under the traditional framework, they find it nearly impossible to access these transactions. If the Pre-IPO market can leverage on-chain tokenization to break unlisted equity into smaller units for low-threshold participation and introduce a transparent secondary liquidity mechanism, it could provide this young investor demographic with a controllable cost investment entry that aligns with their values, as well as an unprecedented influx of retail capital into private equity.

Gen Z and millennials are more inclined to invest rather than put money into pensions; more detailed data can be found in Jarsy's Medium report.

Through tokenization, the originally expensive and scarce unlisted equity can be broken down into small digital tokens and traded on-chain 24/7. Smart contracts can also automatically execute rights such as dividends and voting, enhancing transparency and efficiency. More importantly, if these tokens can be traded on DEX or compliant platforms, market makers and liquidity pools can provide continuous quotes, avoiding the liquidity issues of purely peer-to-peer transactions. Theoretically, private equity tokenization could allow global retail investors to participate in the growth of top private companies with extremely low thresholds, improving the price discovery mechanism to make pricing more market-oriented and transparent.

Of course, the grander the vision, the more constricted the reality. The complexities of traditional regulation, the resistance from private companies, and the complexities of technological integration are unresolved challenges on the path to tokenization. Nonetheless, over the past year, with a shift in policy direction, we have seen a wave of projects exploring on-chain Pre-IPO trading emerging. Some of these focus on derivatives and leveraged trading, while others concentrate on the tokenization of real equity transfers.

On-chain trading of Pre-IPO shares

This category of platforms focuses on trading experiences, often not directly holding the actual equity of the companies involved, but allowing users to bet on the valuation fluctuations of unlisted companies through derivatives or other mechanisms. The advantage is a low entry threshold with no complex equity delivery processes involved; however, the challenge lies in pricing basis and compliance risks.

Ventuals: 'Pre-IPO perpetual contracts' that can leverage up to 10 times on Hyperliquid

Ventuals is a new project incubated by Paradigm, founded by Alvin Hsia, who is also a co-founder of the recently popular content platform Subs.fun and has previously collaborated with Paradigm as an EIR (Entrepreneur in Residence) to co-incubate the end-to-end data platform Shadow.

Ventuals aims to allow users to trade perpetual contracts of unlisted companies on the Hyperliquid blockchain. This model is similar to the common contract trading seen in the crypto market but substitutes the underlying assets with valuation indices of popular startups. Ventuals' core advantage lies in its ability to provide a trading market without holding the underlying stocks, making it more akin to prediction platforms like Polymarket. This also allows it to bypass many traditional securities regulatory requirements (such as identity verification and accredited investor qualifications).

The platform creates custom perpetual contract markets using Hyperliquid's HIP-3 standard and employs an 'optimistic oracle' mechanism to obtain valuation data: anyone can submit valuation data for a company and stake collateral; if no one challenges it, the price becomes effective; if there is a dispute, it is resolved through on-chain voting. This mechanism puts private valuation consensus on-chain, providing a basis for pricing.

Ventuals' pricing method is also interesting; it does not directly use the company's latest financing share price but anchors the token price by dividing the company's valuation by 1 billion. For example, if OpenAI's latest valuation is $350 billion, the initial price for one vOAI token is set at $350. This design lowers the trading threshold and makes the price figure intuitive. However, the problem lies in the opacity and low update frequency of private company valuations, which mainly rely on occasional financing or secondary trading information. Although Ventuals has introduced technologies like oracles + EMA (exponential moving average) to smooth prices, information asymmetry remains a hard issue: when the underlying data is lagging or distorted, derivatives trading based on it may amplify market fluctuations. Platforms utilizing oracles, like Polymarket, have encountered issues due to these flaws, and as volumes increase, the rapid trading process may lead Ventuals into greater trouble.

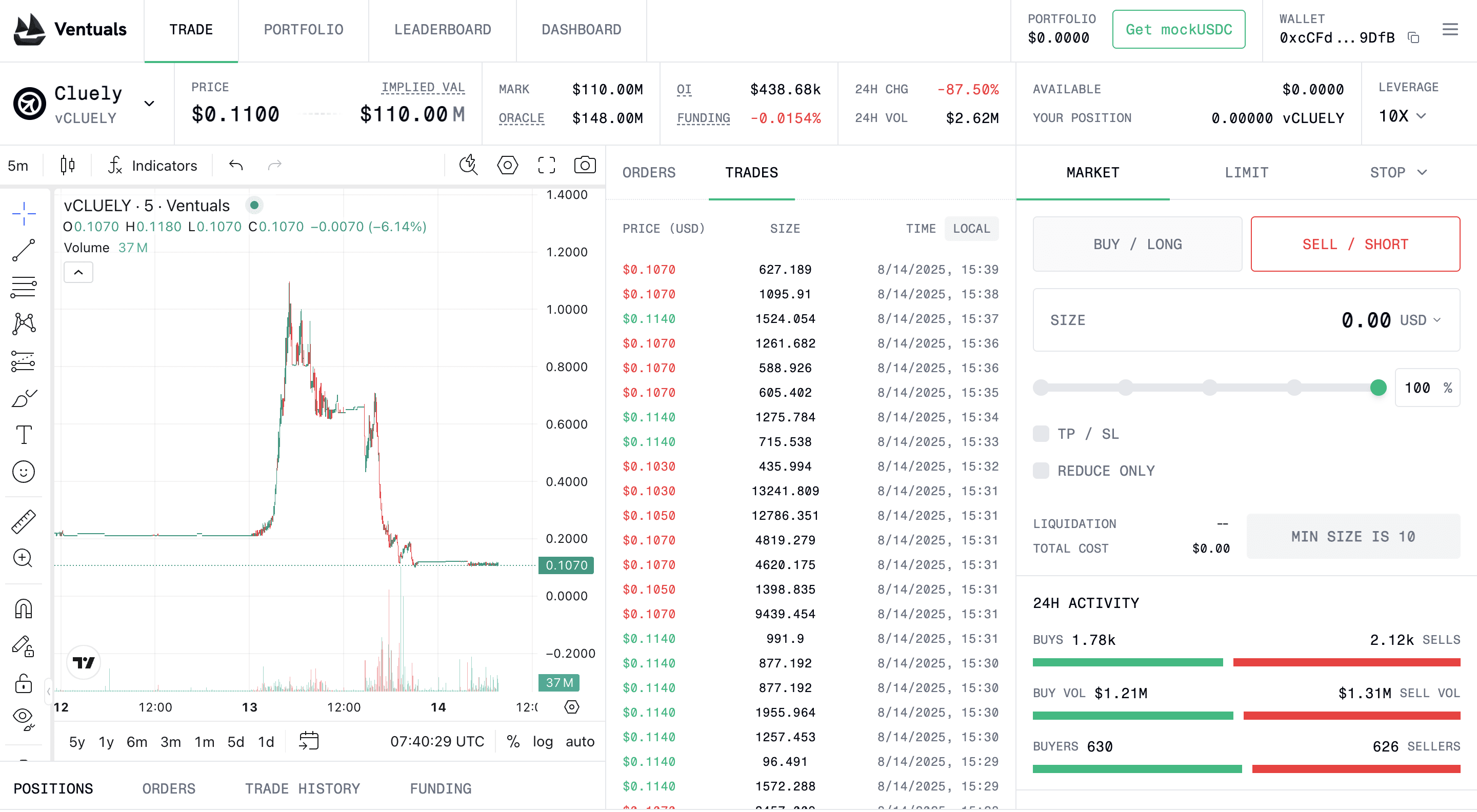

Thanks to the founding team that bought Ferraris with investors' money, market valuations have plummeted, source: Ventuals

As a trading platform, Ventuals' biggest selling point is providing opportunities to long or short with leverage of up to 10 times, allowing users to 'bet small to win big.' However, the platform is still in the testing phase (only operating on the testnet). Ventuals is taking a completely decentralized derivatives route, attempting to create a global Pre-IPO exchange through high-performance on-chain matching (Hyperliquid can handle 100,000 orders per second) without the need for trusted intermediaries. Of course, it still faces significant compliance challenges. Even though it does not hold actual shares, these contracts essentially bet on security prices and may still be viewed as security derivatives by regulators. Additionally, who provides liquidity and guarantees the accuracy of oracles remains unknown.

Earlybird: Long and short market for Pre-IPO on Solana

Earlybird was created by the team behind the NFT market Hyperspace on Solana (which ceased operations in 2024, and its Twitter was even renamed to Earlybird), focusing on allowing users to 'go long or short on companies before IPOs,' positioning itself as the next-generation private equity trading platform for retail investors. The team has received investments from top crypto VCs (like Dragonfly and Pantera) and has accumulated experience in the Solana NFT field, now turning to the Pre-IPO track.

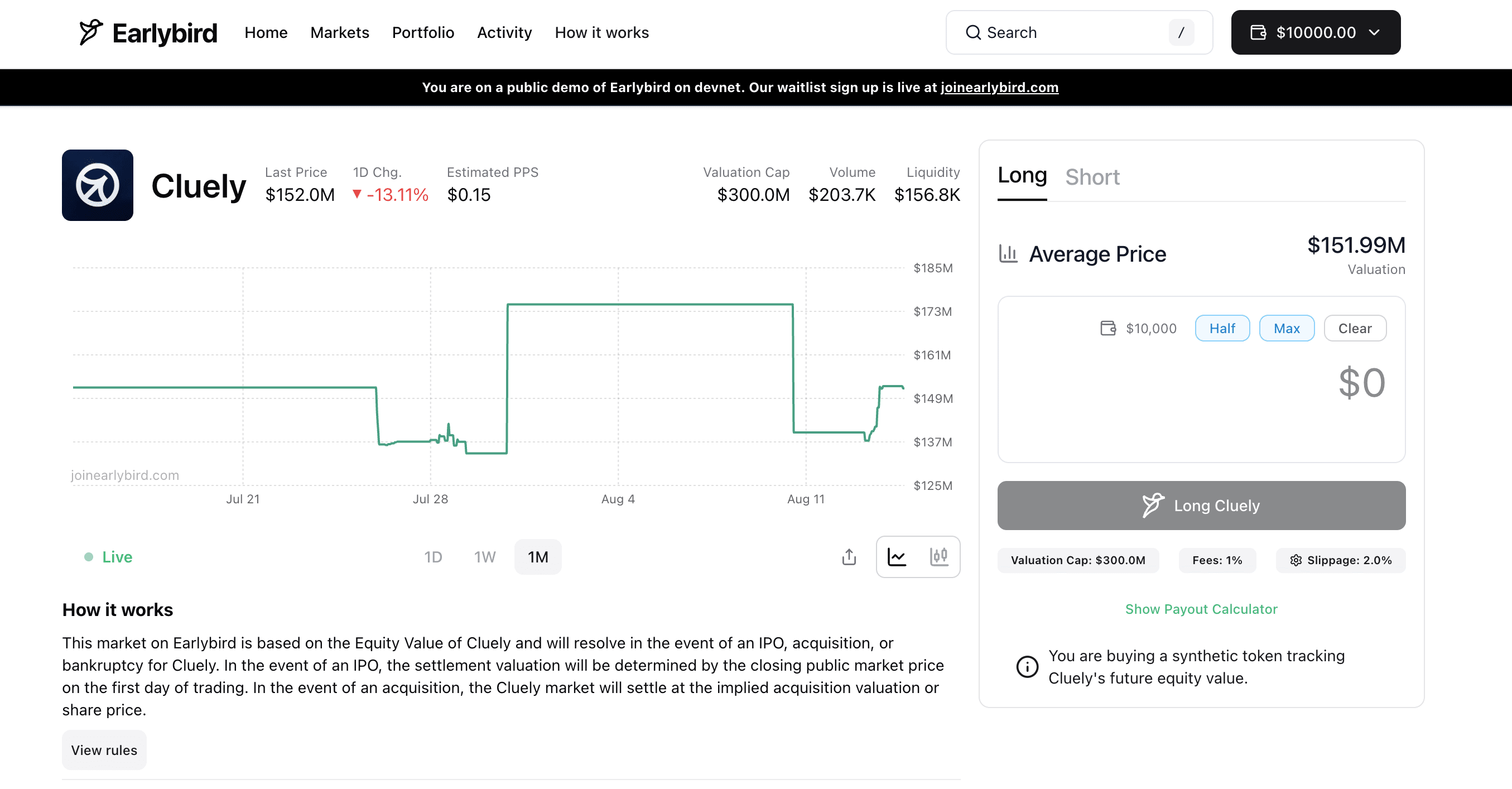

It seems that the prices given by the oracles of the two platforms are a bit different, and it's uncertain whether this will be fixed after going live; in the future, there may be opportunities for cross-platform arbitrage with Polymarket.

The founding team of Earlybird includes Kamil Mafoud and Santhosh Narayan, co-founders of Hyperspace. It is said that after Hyperspace closed its NFT business in 2024, this team began focusing on the development of Earlybird. In fact, for them, a 'Pre IPO platform' might be more intuitive than an 'NFT platform,' as both have experience working as investment analysts at Morgan Stanley, where Wall Street connections may be more important in this field than in cryptocurrency.

The specific product form of Earlybird has not been fully disclosed (the platform is still in a closed testing phase), but it can be accessed via the Dev test network (with a $10,000 experience fund lol). From its promotional materials, it likely shares similarities with Ventuals, using on-chain derivatives or synthetic assets to allow users to bet on the valuation fluctuations of unlisted companies. The fast and low-cost on-chain environment of Solana is also suitable for building real-time trading markets. The team may adopt an order book or AMM market-making mechanism to provide more continuous liquidity than traditional OTC. Notably, similar practices for trading Pre-IPO assets already exist on Solana, such as PreStocks and the earlier on-chain U.S. stocks (like the now-defunct synthetic assets mStock on Mango Markets).

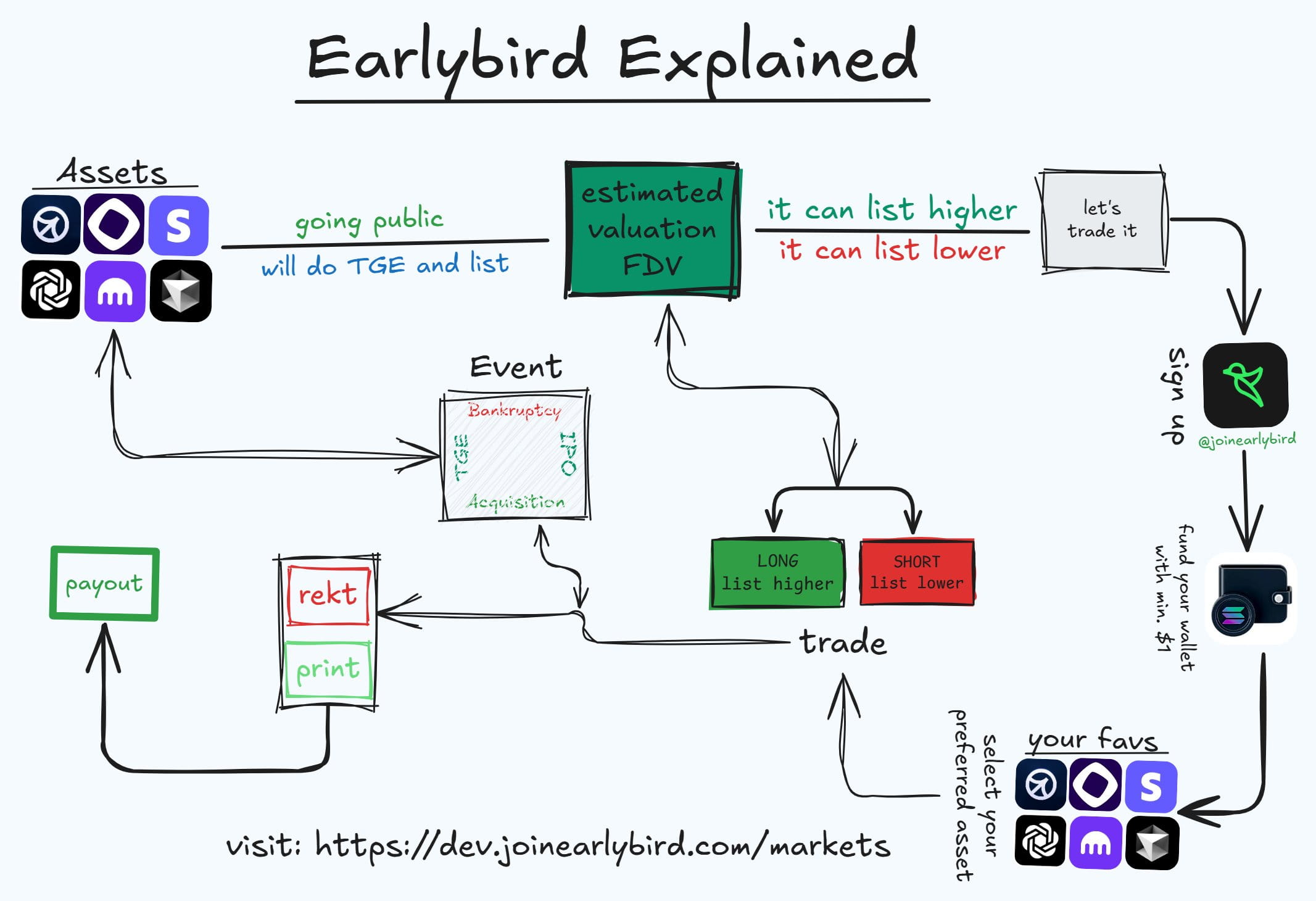

The trading logic of Earlybird, source: @0xprotonkid

From a market positioning perspective, Earlybird may take a more open and decentralized route, with relatively relaxed user geographic restrictions and qualification requirements. In summary, Earlybird is an active explorer of the Pre-IPO track within the Solana ecosystem, and like Ventuals, it has chosen the approach of 'not touching real equity, realizing markets through derivatives.' Its success largely depends on solving the two core issues of valuation pricing and compliance risk.

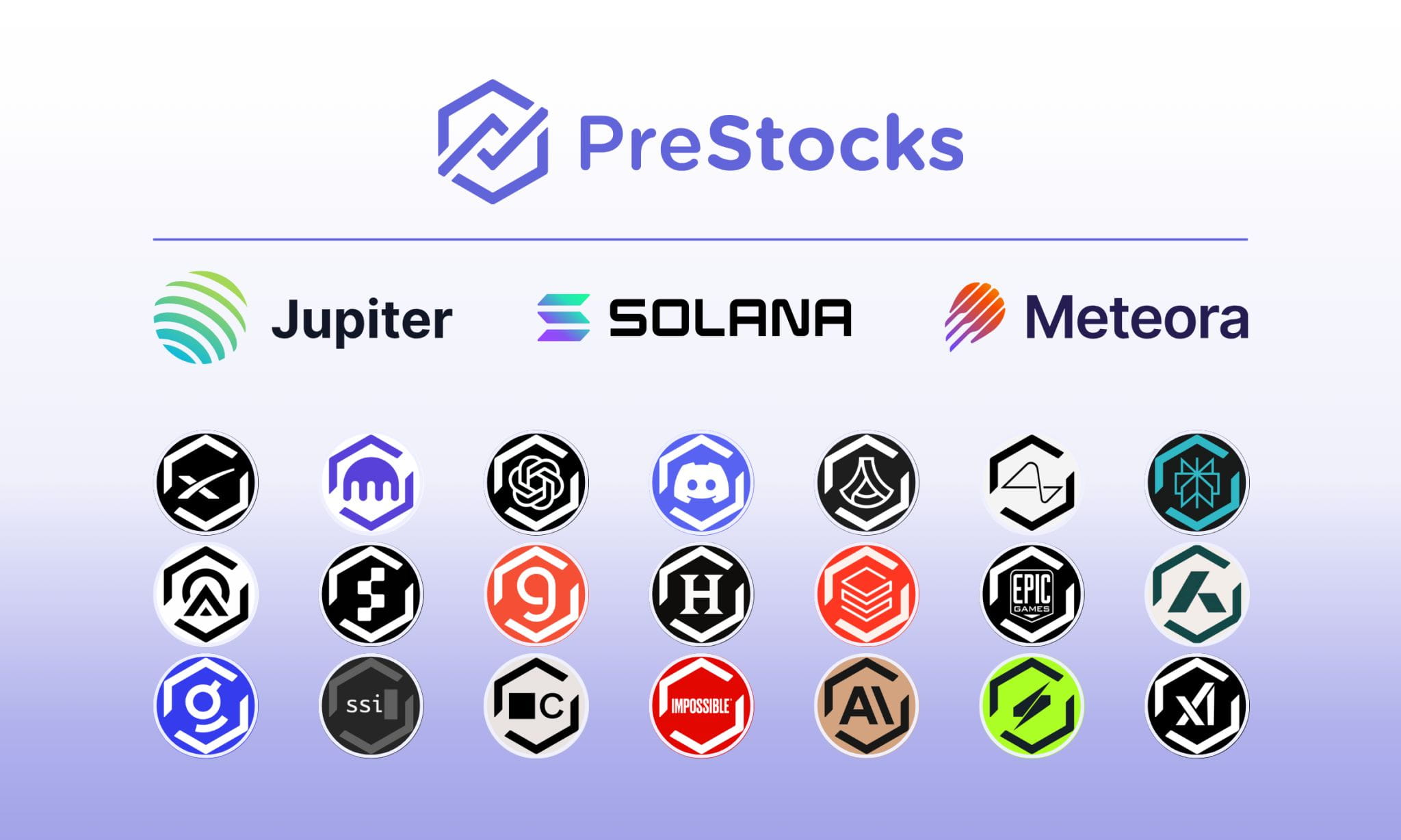

PreStock (backed by Republic): The 'good child' among equity token trading platforms

Compared to the 'light asset' models of Ventuals and Earlybird, PreStocks is closer to the traditional concept of stock trading, just transferred to the blockchain. PreStocks was founded by a Singapore team backed by the established private equity platform Republic Capital, holding real private company shares through special purpose vehicles (SPV) and issuing 1:1 pegged tokens.

In simple terms, if PreStocks buys a batch of original shares of OpenAI through an SPV, it will mint 'pOPENAI' tokens on Solana at a ratio of one token for each share. Each token is backed by a real share, allowing investors holding tokens to enjoy economic rights almost identical to shareholding (such as profits from rising stock prices and future IPO cash-outs), but without direct legal shareholder status or receiving dividends.

Currently, PreStocks supports token trading for 22 private companies, including well-known unicorns like OpenAI and Canva. Users only need a Solana wallet and can trade these tokens for as little as a few dollars, with no investment threshold restrictions. Tokens on PreStocks can be freely transferred on-chain, traded or lent on DEX platforms, and even provide liquidity to earn transaction fees, or be used to create new structured products. PreStocks integrates the Jupiter aggregator and Meteora market maker, achieving 24/7 trading and instant settlement.

To ensure that each token is backed by real shares, PreStocks is held by a regulated custodian for the underlying stocks and promises to regularly disclose audit reports. However, the team has yet to publicly disclose detailed proof of holdings, only claiming that all tokens are 100% fully collateralized. Given the involvement of unlisted company equity, PreStocks faces significant compliance pressures, leading it to block users from major jurisdictions like the U.S. (on-chain buying and selling does not require KYC, but minting or redeeming PreStocks does require KYC). The company's registration location in Singapore is also due to relatively relaxed regulations.

PreStocks' founder Xavier Ekkel has stated that its vision is to make private equity investment as simple as trading public stocks. By providing a zero-threshold entry channel for retail investors into unicorns, PreStocks has indeed weakened the monopoly of traditional secondary markets to some extent. However, this model also has clear limitations. The first is liquidity: as the share source for each company is limited (currently on the PreStocks platform, a single company's token market cap is usually only a few hundred thousand dollars), the market depth is shallow, and large trades can impact prices significantly. In contrast, established secondary institutions like Forge handle median transaction sizes exceeding $5 million and have institutional-grade order management systems; PreStocks' trading system will require a broader user base for support.

Secondly, its scalability is also limited by the '1:1 shareholding' model. For each new target, PreStocks must negotiate the purchase of real shares offline, which requires case-by-case communication with sellers (employees, VCs, funds, etc.), making the process lengthy and subject to the willingness of the target company. Furthermore, PreStocks itself is not a licensed securities exchange but operates more in a gray area; if the regulatory authorities change their stance, the platform may be forced to restrict or withdraw related assets.

Overall, PreStocks adopts a more tangible path than derivatives, using real capital to 'buy a path' for retail investors. Its advantage lies in better protection of investors' rights (backed by real shares, with real payouts in future IPOs), but the downside is high operational costs and significant compliance challenges. I believe Republic aims to develop PreStocks into a 'high liquidity trading platform' for distributing its mirror tokens because its operations are governed by Reg CF rules, limiting investments to $5,000 and requiring a one-year lock-up, while liquidity and 'lock-up' restrictions on its own acquired compliant centralized trading platform, INX, contradict the original product intent, thus choosing the 'alternative path' of PreStocks.

Further reading: (Figma is set for the largest IPO on U.S. stocks this year; can Republic buy its private equity?)

A platform focused on real equity tokenization

This category of platforms directly offers end investors the opportunity to purchase rights in unlisted companies, essentially acting as on-chain securities issuance or private crowdfunding. They typically require holding or locking real shares, using tokens as proof to allow investors to share in future profits. This model is closer to traditional finance but utilizes blockchain for registration and transfer, often managed by traditional financial firms or fintech companies.

Jarsy: The group buying site for equity tokens

Among numerous Pre-IPO projects, Jarsy has taken a steady and solid approach. It quietly launched on the Arbitrum network in 2024, and the company behind it, Jarsy, Inc., is headquartered in San Francisco, USA, founded by Hanqin, Chunyang Shen, and Yiying Hu, among others. The founding team includes former executives from Uber China and the engineering lead from Afterpay, with a deep understanding of internet product operations and regulation. They secured $5 million in investments from institutions like Breyer Capital, with notable investors including Evan Cheng, CEO of Mysten Labs, Nathan McCauley, CEO of Anchorage, and Richard Liu, CEO of Huma Finance.

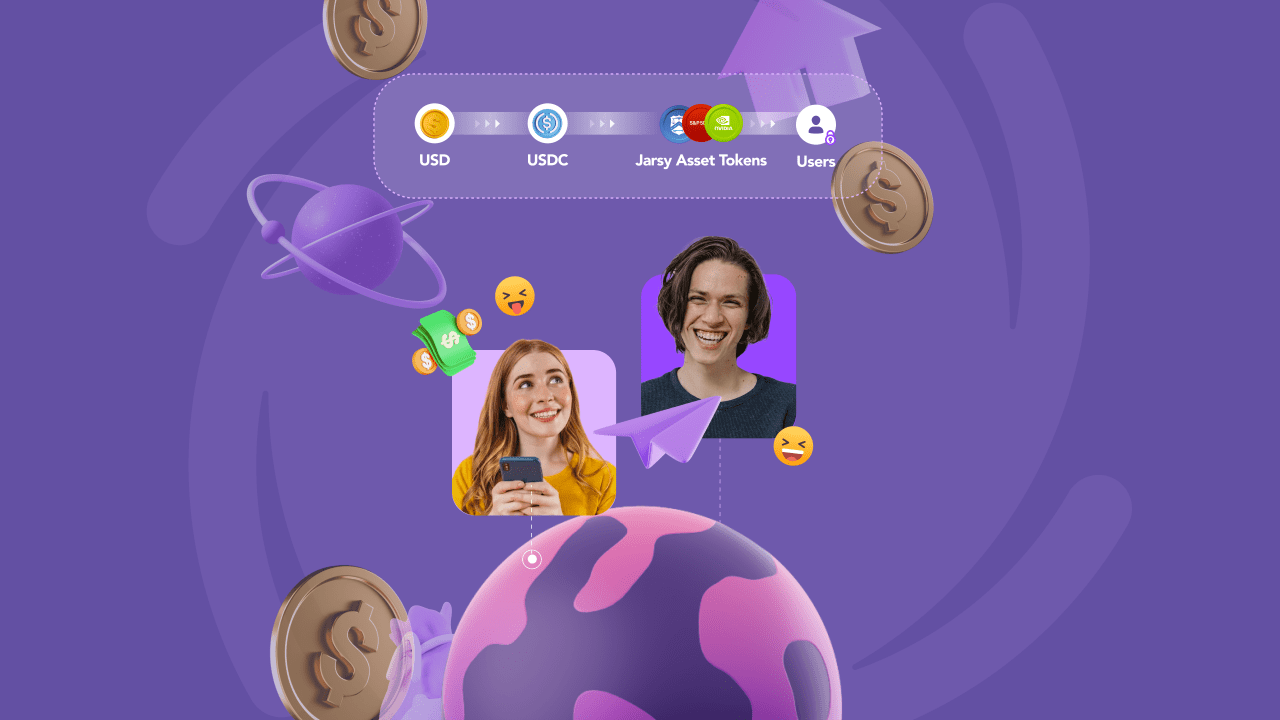

Jarsy operates by first launching target company Pre-IPO equity products on the platform, allowing users to pre-subscribe (paying in USDC or USD). Once a certain subscription amount is reached, Jarsy negotiates with risk funds, early shareholders, or employees holding shares of that company to use the raised funds to acquire a certain number of real shares. If the acquisition is successful, tokens equal to the actual number of shares acquired are minted and distributed to investors; if negotiations fail or fundraising is insufficient, funds are returned via the original route. This process is similar to traditional private equity share transfers, but utilizes the crowdfunding concept of 'raising funds before purchasing' and employs on-chain tokens as proof of rights.

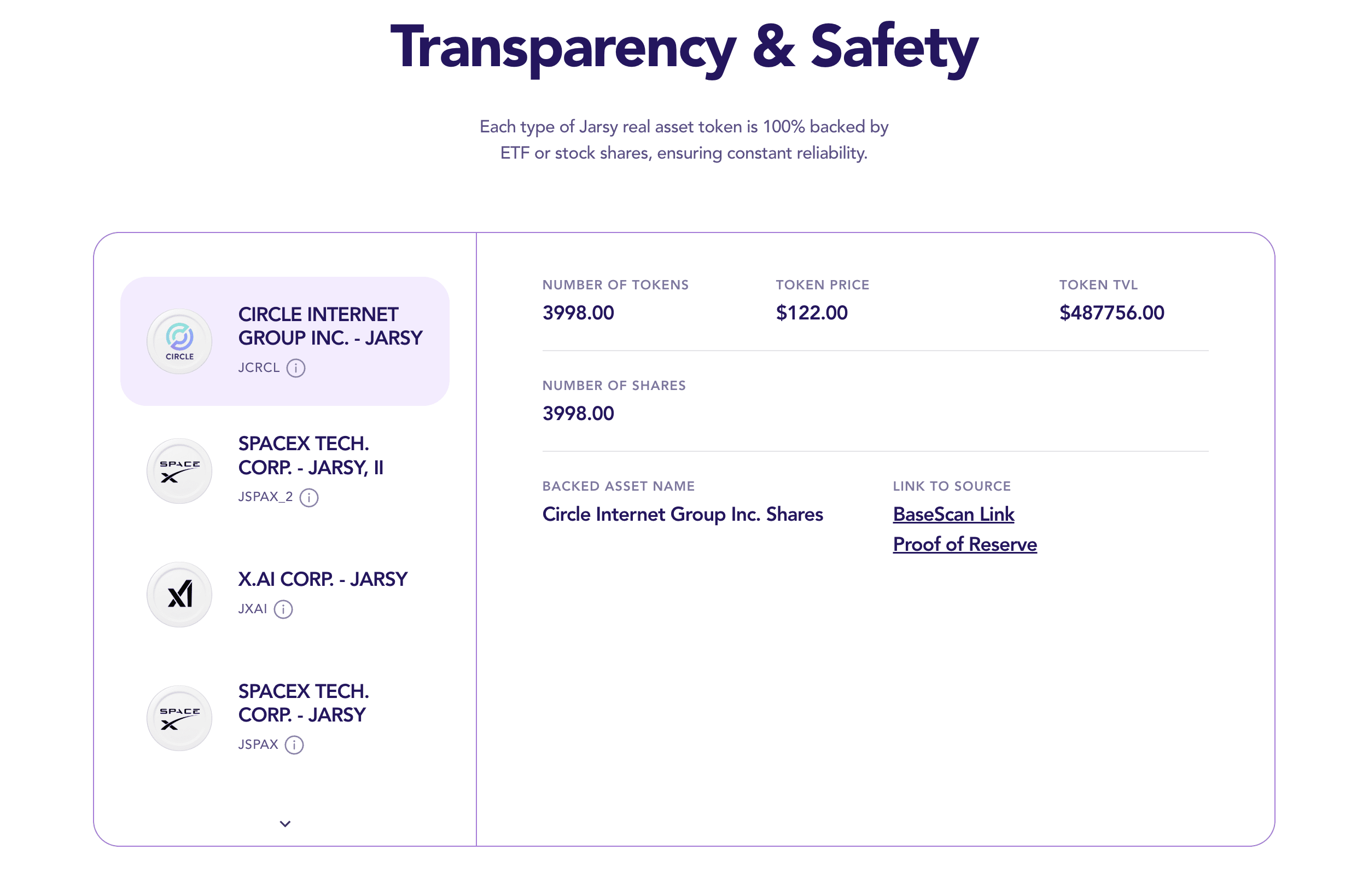

Jarsy will also place all held stock assets in a dedicated SPV (Special Purpose Vehicle) for custody and provide a real-time on-chain reserve proof page for inquiries. Each Jarsy token purchased by investors (e.g., JSPACEX representing SpaceX shares) corresponds to a real share as support. Although token holders are not legal shareholders of the company, they enjoy economic rights almost equivalent to shareholding, including cashing out at future IPOs, the consideration when being acquired, and even potential dividend earnings. This makes Jarsy different from the other projects mentioned above, resembling more of a 'group buying website' for private equity.

However, Jarsy still significantly lowers the participation threshold, with a minimum investment requirement of only $10. More importantly, apart from U.S. investors, users from around the world can participate without needing accredited investor certification. Jarsy has also optimized the user experience of Web2, supporting email registration and fiat payments, creating custodial wallets for users, and making the purchase of tokens almost feel free of blockchain complexity. Jarsy focuses more on compliance and ease of use, attempting to build a bridge product of 'Web2 interface + Web3 backend.' Since its launch, Jarsy has already introduced tokenized equities for star companies like Anthropic, Stripe, and Perplexity AI, with many products selling out immediately upon launch.

Of course, the Jarsy model still faces two significant challenges. The first is liquidity. Since the supply of each Jarsy token depends on the actual number of shares acquired, and private equity itself lacks public market pricing, a large holder selling a significant number of tokens can easily lead to a price crash or lack of buyers. Currently, the largest stocks held by Jarsy are X.ai (approximately $350,000), Circle ($490,000), and SpaceX ($670,000), all of which are not large in scale. In such a shallow market, a sell order of several tens of thousands of dollars could potentially crash prices, with insufficient trading depth.

The second challenge is the expansion bottleneck problem that all 'real holdings' projects encounter. Jarsy needs to exert significantly more effort for each new target than 'derivative model platforms,' and it requires high levels of connections and resources. Moreover, although Jarsy claims to prioritize compliance, it still provides unregistered security tokens, which carry uncertainties under the U.S. regulatory environment. However, Jarsy has actively collaborated with top law firms like WSGR (Wilson Sonsini, Goodrich & Rosati) to plan compliance routes, indicating its intention to seek regulatory exemptions or approvals, making it potentially more welcomed by institutions in the current compliance environment.

As CEO Han Qin stated, 'We founded Jarsy to bring the long-monopolized private investment opportunities to ordinary people.' Despite challenges like liquidity and compliance, Jarsy has already taken significant first steps, making it one of the more compliant 'equity tokenization platforms' currently available. With user growth and asset scale expansion, if it can gradually obtain regulatory recognition, its tokens may eventually circulate in compliant secondary markets, making 'Pre-IPO equity' truly a public asset class.

Opening Bell: A pioneer in the blockchain transformation of traditional stocks

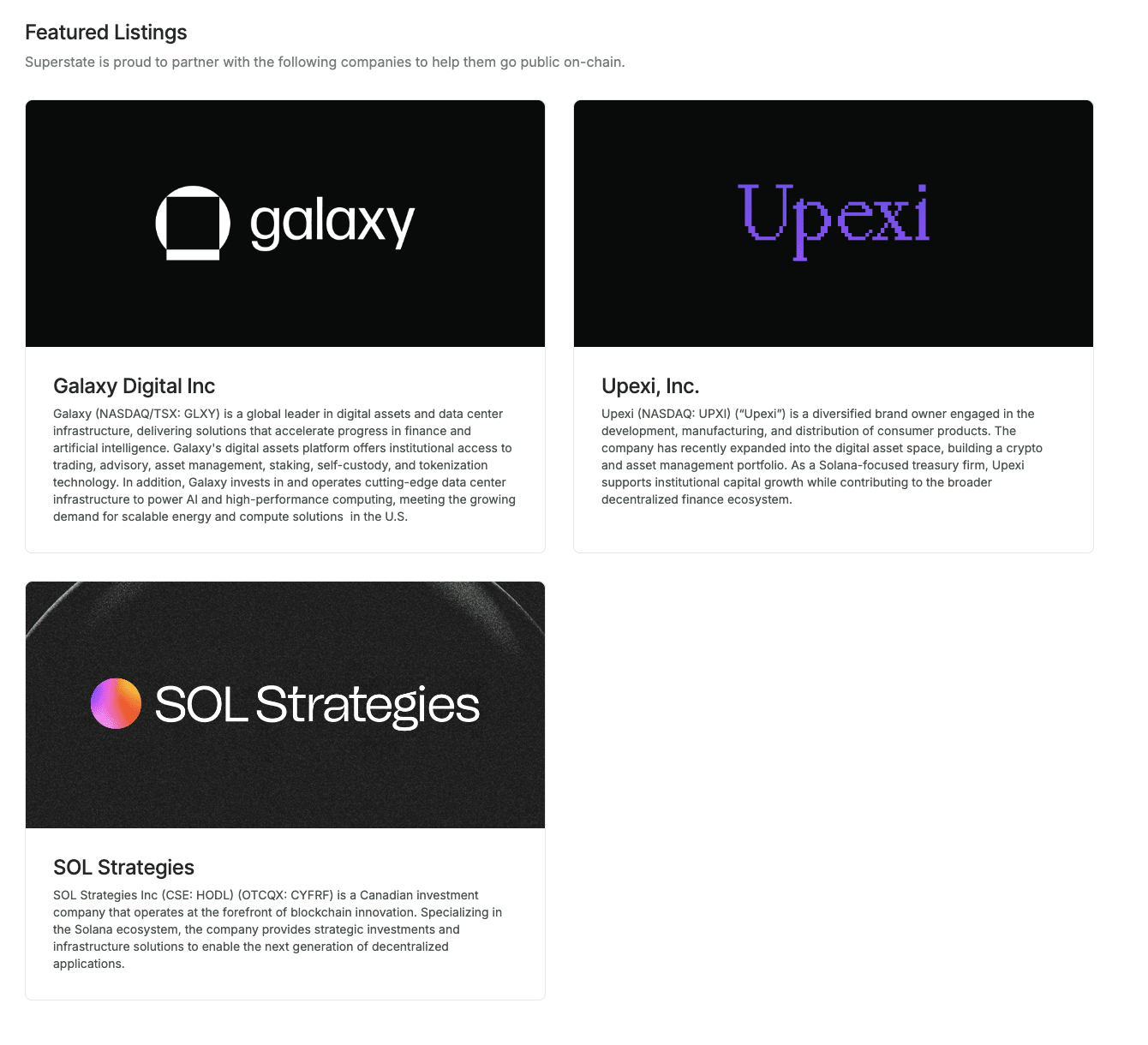

The Opening Bell platform launched by Superstate offers another pathway, allowing companies to move their stock onto the chain directly. Unlike the aforementioned projects where third parties buy shares and issue tokens, here the company itself becomes the issuer. In May 2025, Superstate (a compliance fintech company founded by Compound founder Robert Leshner and others) announced the launch of Opening Bell, enabling stocks already registered with the SEC or eligible private companies to conduct 24/7 on-chain trading via the Solana blockchain. In simple terms, public companies or private companies can issue on-chain stock tokens on the Opening Bell platform and ensure these tokens represent actual legal equity (not Mirror token synthetics).

The first practitioners of this model include Nasdaq-listed company Upexi (stock code UPXI) and Canada's SOL Strategies. Galaxy Digital, which was recently in the spotlight due to its Ethereum token stock company, is also involved (however, only the SOL Strategies case has not yet been listed on Nasdaq). This requires strict legal frameworks, such as Superstate already registering a digital transfer agent in the U.S. to ensure that the on-chain shareholder registry is in sync with traditional registrations.

The emergence of Opening Bell marks a further integration of traditional finance and blockchain. Through this platform, company stocks can be traded in real-time 24/7, providing unprecedented flexibility and transparency, making stocks behave like cryptocurrencies that are 'always on.' Private companies also have the opportunity to use Opening Bell to gain liquidity in advance; some companies planning to go public or not in a hurry for an IPO can completely reach out to global investors by issuing on-chain stocks for financing or shareholder cashing out. Superstate explicitly states that Opening Bell's target clients include both publicly listed companies and 'late-stage private companies' seeking liquidity.

Of course, the advancement of this model still requires the nod of regulatory bodies. Currently, on-chain plans announced by companies like SOL Strategies have submitted SEC application documents but note that they are 'pending regulatory approval.' However, at least in terms of trends, regulatory agencies are showing a more open discussion attitude towards asset tokenization. The U.S. SEC held a specialized roundtable meeting in 2025 to discuss the tokenization of securities, and even traditional giants like Blackstone and Robinhood's CEO have publicly expressed support. Superstate itself has already gained successful experience in stablecoins (USTB) and on-chain national debt funds, now expanding into the stock sector, which is very timely.

In terms of Pre-IPO, Opening Bell offers a potential path for a disguised IPO, allowing companies to avoid the lengthy traditional IPO process and realize public trading of stocks during the private placement stage. For instance, a unicorn company can issue a portion of equity tokens on Opening Bell for trading, and when conditions are ripe, it can formally go public or directly merge. This is somewhat akin to the past OTC market, but with blockchain technology, transparency and efficiency have greatly improved.

From a certain perspective, if this model gains recognition, future IPOs may no longer require Wall Street underwriters but could be completed on-chain. Viewed from this angle, Superstate resembles 'Binance Alpha' for Nasdaq.

Further reading: (Superstate opens 'on-chain shares,' SOL reserve companies bring the token stock battlefield back on-chain)

Is the era of investment democratization upon us?

Making investment opportunities in unlisted companies more open and efficient. For ordinary investors, this is undoubtedly an exciting trend. From the perspective of wealth opportunities, it helps narrow the gap between the public and institutional investors. However, the on-chain Pre-IPO field still faces both opportunities and risks. 'Regulatory compliance' and 'the resistance of target companies' loom like the sword of Damocles over such projects.

Embracing regulation and cooperation should be the main direction for on-chain Pre-IPO trading. Increasingly, traditional financial institutions and investors are showing interest in this field. For example, the Hong Kong Stock Exchange and Nasdaq are researching tokenized securities; well-known VCs may consider collaborating with these platforms to release a portion of shares on-chain without affecting company control. This new paradigm of collaboration between LPs and GPs, if successful, is expected to significantly accelerate the popularization of private equity tokenization. Undoubtedly, on-chain trading of Pre-IPO shares is a new blue ocean filled with potential. The 'Trojan horse' of freely trading unlisted equity could ultimately open the 'city gate' to the ultimate form of capital markets; perhaps we are just a few steps away from that gate.