Introduction

For the past two years, Uniswap has been stuck in a valuation paradox: as the leading protocol of DeFi, it has the highest trading volume and transaction fees in the industry, yet it cannot deliver even a penny of return to token holders.

However, as we enter 2025, the story of Uniswap seems to be entering the next phase. The protocol itself is changing, governance is changing, and the only thing that hasn't changed is that the market is still pricing UNI based on a '0 revenue sharing' logic.

When we attempt to answer the valuation question about UNI:

Based on the current 'favorable conditions,' what should its reasonable valuation be?

So, it is time to re-evaluate Uniswap.

1. Current status of the protocol: from a narrative of no dividends to an undervalued reality

In February 2025, Uniswap finally welcomed a turning point in its narrative— the U.S. Securities and Exchange Commission (SEC) announced that it would formally close its investigation into Uniswap Labs, and 'will not take any enforcement action.'

This not only clears years of regulatory shadows for Uniswap itself but also sends a clear signal to the entire DeFi market: the open financial infrastructure at the protocol level still has room to survive and expand within the regulatory framework.

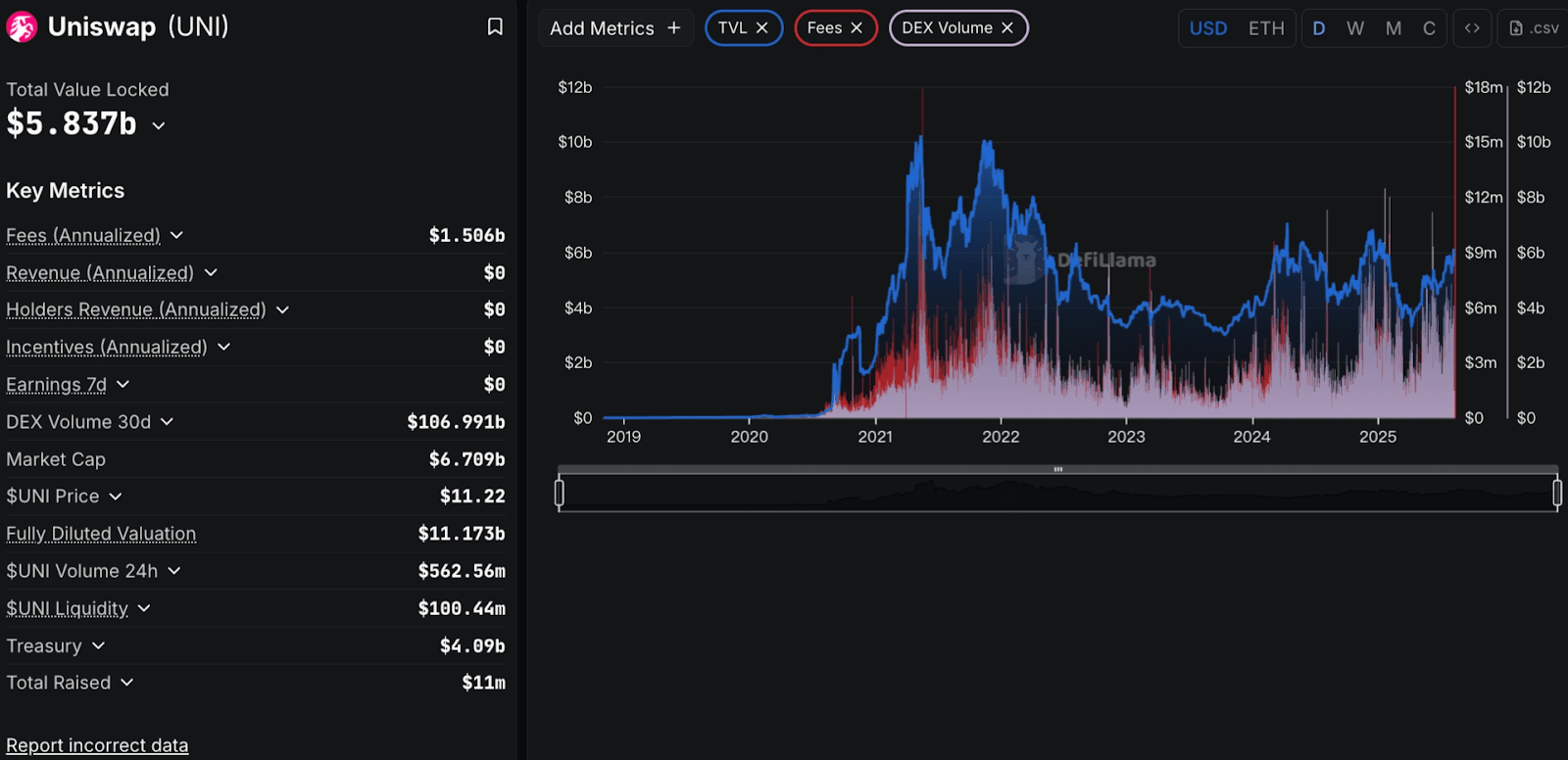

At the same time, Uniswap's product iteration has quietly completed a generational upgrade. At the beginning of 2025, v4 officially launched and completed multi-chain deployment. With the flexibility brought by the Hooks architecture, Uniswap's liquidity aggregation efficiency has further improved. The launch of the Unichain mainnet provides a more unified foundation and execution environment for its subsequent expansion. The actual performance also quickly provided feedback: by May 2025, Uniswap's single-month spot trading volume reached $8.88 billion, setting a new high for the year, with the total trading volume in nearly 30 days reaching as high as $109 billion.

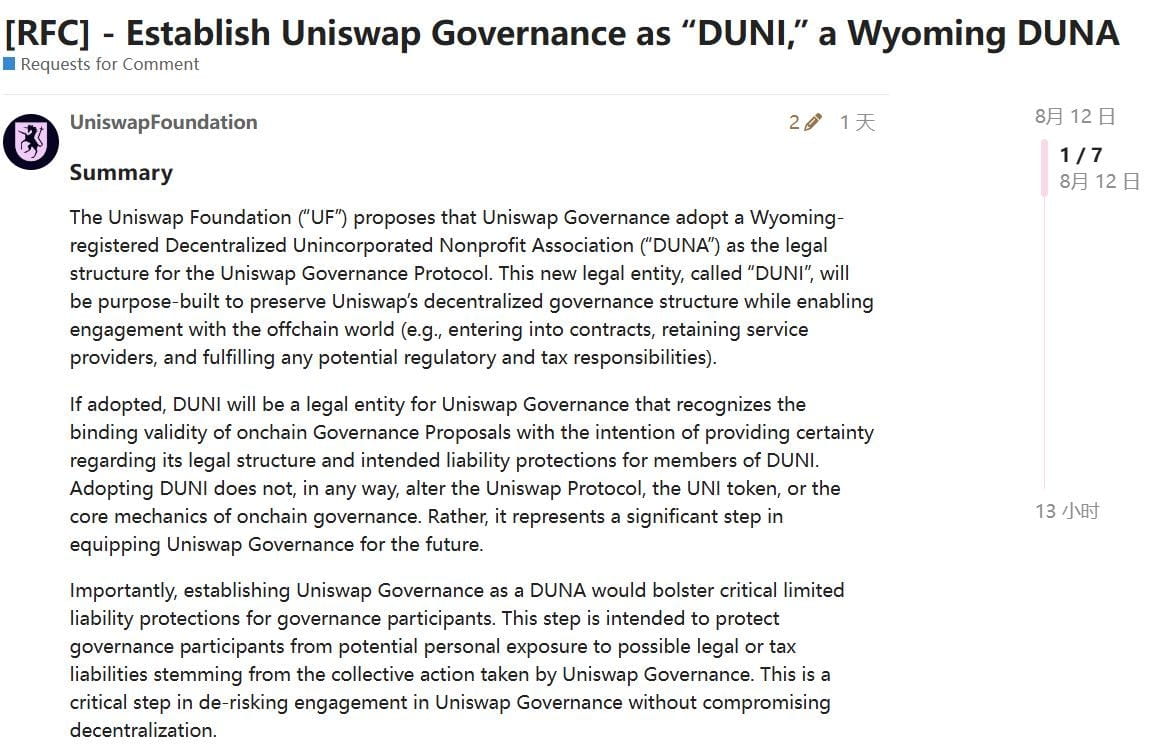

In addition to the recovery of trading volume and the launch of v4 as catalytic factors, Uniswap has also welcomed a potential key change in governance. The Uniswap Foundation (UF) proposed on August 12 to register a decentralized non-registered non-profit association (DUNA) in Wyoming and establish 'DUNI' as the legal entity for Uniswap governance based on it.

This means that in the future, the Uniswap DAO will have a legal identity, able to sign contracts off-chain, hire partners, fulfill tax compliance, while also recognizing the legal validity of on-chain governance. Most importantly, DUNI will provide limited liability protection for governance participants, significantly reducing personal legal or tax risks that may arise from protocol decisions. This structural improvement perfectly complements the final link of the dividend mechanism: the previously untouchable 'legal grey area' is being filled by the system. Once DUNI is established, the protocol's income will truly enter the DAO or UNI holders' hands, no longer just a 'vision,' but a step with actual implementation basis.

However, compared to the expansion pace of the protocol itself, the valuation pace of UNI is still on an old track—its price hovers around $10, and DefiLlama shows its holders' income is 0. The annual fees generated by the protocol are nearly several hundred billion dollars, yet not a single penny has flowed into the hands of UNI holders.

There are certainly reasons behind this. From the very beginning, Uniswap's governance set the protocol income to '0 revenue sharing,' transferring all trading fees to LPs. But now, the story is changing.

The DAO has initiated discussions for a trial to uniformly collect a 0.05% protocol fee across all v3 pools, and the 'staking + delegation → revenue sharing' UniStaker module has long been technically deployed. The removal of regulatory risks makes this distribution logic more realistically executable.

The problem is: the structure of the protocol has changed, but the market's pricing logic has not.

Uniswap is evolving from a 'non-dividend infrastructure' to a protocol 'capable of potential cash flow distribution.' However, the market's pricing for this evolutionary path still remains in the past 'only telling stories, not discussing profits' valuation system.

And this is precisely what we believe— the current Uniswap deserves to be re-evaluated.

2. Valuation approach: viewing future valuation through the lens of dividend expectations

In the current pricing logic, UNI is seen more as a mere cryptocurrency. Without dividends or fee returns, the market naturally will not value it based on the logic of 'generating cash flow.'

And once this premise of revenue sharing is established, the valuation logic of UNI will no longer be 'market sentiment × liquidity games,' but 'distributable protocol income × revenue sharing ratio × PE multiple.'

In this case, the most direct valuation method is:

Expected valuation = expected dividends of the year × PE multiple

Dividends: calculated as annual protocol income × revenue sharing ratio.

PE multiple: in most DeFi protocols, 40-60 times is a common range, but Uniswap's scale and income structure are enough to support it receiving a higher premium.

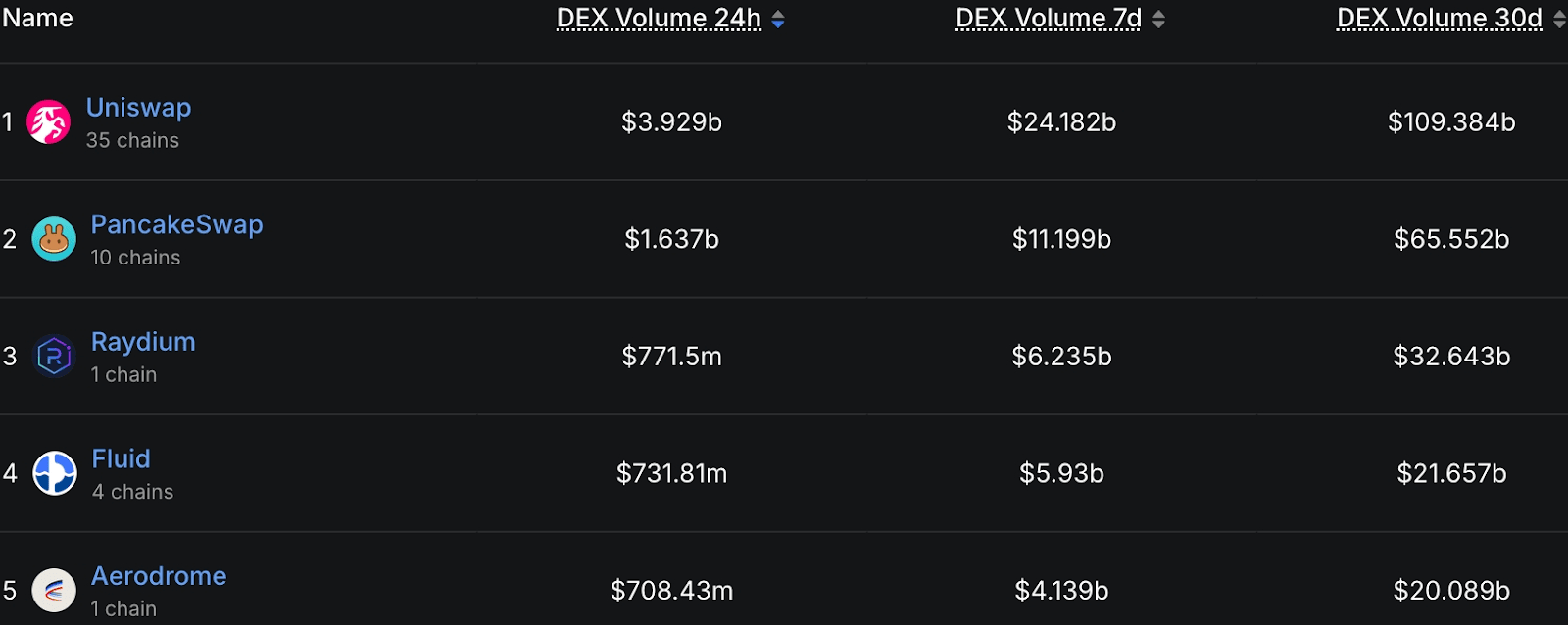

First, let's look at the scale. According to DefiLlama data, Uniswap's trading volume in the past 30 days reached $109 billion, significantly leading PancakeSwap's $65.5 billion and far surpassing Raydium's $32.6 billion. In other words, its trading volume in one month is close to the total of the top five DEXs in the market.

Compared to data from other DEXs, it is clear that Uniswap, which has already validated its cross-cycle capabilities and occupies an absolute market share in income, has long formed a 'discontinuous' leading pattern. This advantage is not just about scale; it is more reflected in the sustainability of income and breadth of distribution—it covers multiple chains including Ethereum, Polygon, Arbitrum, Optimism, etc., with strong stability in liquidity and user base. Therefore, it is reasonable to price UNI, as a leader, with a higher premium than the ordinary protocol's 40-60 times PE.

Caption

Caption

Furthermore, compared to the current P/Fees/TVL range of other DEXs, the leading valuations are generally 30%-100% higher than those of second- and third-tier projects. In the context of global regulatory narratives, the expectation of fee switch implementation, and institutions' greater inclination to allocate to top protocols, the reasonable conservative expectation for UNI's PE is calculated as:

Using the industry's relatively low average of 40 times PE as a base * (1+30%~100%) = UNI PE = 52 times - 80 times

⬇️

Taking the median PE value as 66 times

Finally, PE is not a static number; it fluctuates with changes in market interest rates, industry prosperity, and protocol competition patterns. To compare the income and valuation of other protocols, you can check the data directly on DefiLlama and see if 66 PE is overvalued; you will have an intuitive answer.

\ Four, Valuation Derivation: Uniswap, why could it be worth $26 in the future?

So if we look at Uniswap from a traditional financial perspective, the most direct valuation method is a simplified version of discounted cash flow (DCF): using the distributable cash flow for the coming year as a benchmark, multiplied by the potential price-to-earnings ratio (PE), to obtain a reasonable market value range.

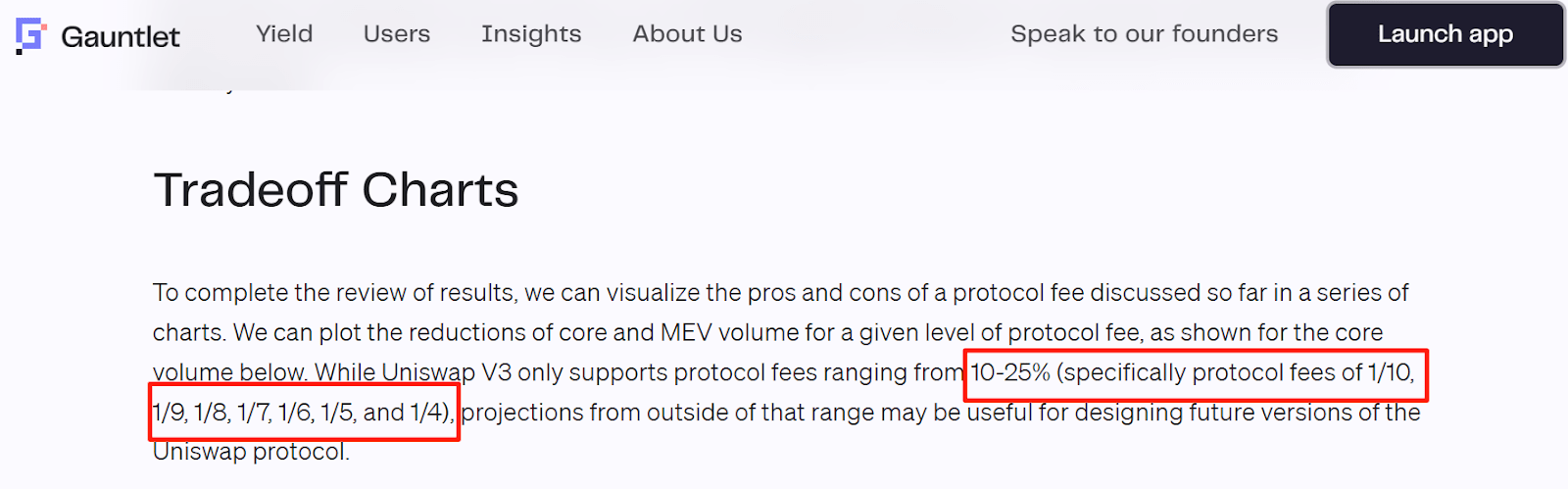

In the past 30 days, Uniswap's total trading volume was approximately $109B. Based on an average fee rate of 0.3%, the total fees generated by the protocol during this period were about $327M. Since the fee switch has not yet been activated, this income currently all flows to LPs; however, once the dividend mechanism is implemented, the protocol could distribute a certain percentage (assuming 10%-25%) to UNI holders.

Annualizing the 30-day trading data yields the annual distributable cash flow range:

Revenue sharing ratio 10%: $109B × 0.003 × 0.10 × 12 ≈ $392.4M

Revenue sharing ratio 25%: $109B × 0.003 × 0.25 × 12 ≈ $981M

(According to Gauntlet's report, Uniswap v3's fee switch mechanism supports tiered revenue sharing for LPs at 10%-25%. The DAO governance has now also opened a trial pool to uniformly collect a 0.05% protocol fee, indicating that the protocol is attempting to activate dividend possibilities without harming LPs.)

In the current market environment, the PE level we reasonably inferred in the previous section is approximately 66 times. Substituting into the calculation formula:

Low revenue sharing scenario (10%): $392.4M × 66 ≈ $25.9B

High revenue sharing scenario (25%): $981M × 66 ≈ $64.8B

Considering that the current total market value of UNI is only $10.5B, with a coin price of about $10.6 (as of 10 PM on August 8, 2025), this means that under different dividend ratios, the theoretical price range after revaluation would be:

Low revenue sharing scenario: approximately $26.2

High revenue sharing scenario: approximately $65.4

From the valuation results, even with a conservative 10% revenue sharing ratio, the corresponding reasonable price has more than 2.5 times the upward potential compared to the current level. Under more aggressive assumptions, the potential revaluation could exceed 5 times.

In other words, the market's pricing of UNI is stuck in the 'undervalued' period before the fee switch was activated. Once dividends are realized, the cash flow logic will replace mere trading volume sentiment, becoming the core force driving the valuation center upward.

Of course, a project's reasonable valuation is influenced by multiple factors, so it is not very logical for UNI to suddenly hit a valuation ceiling, so a lower estimate of around $26 is still worth looking forward to.

5. Between the reality and imagination of dividends: opportunities, paths, and risks

You might be wondering: revenue sharing sounds great, but can it really be realized?

In fact, this question has been an unresolved puzzle hanging over the leading DeFi projects for the past few years. Now, Uniswap, aside from the aforementioned regulatory, governance, and technical issues being properly addressed, is actually not the first to take the plunge in the industry:

SushiSwap has incentivized token holders with 'transaction fees' since its inception;

Protocols like GMX, dYdX, etc., have long formed a market mentality of 'staking = income rights';

The new generation of trading protocols like Ambient, Maverick, Pancake v4, have all integrated 'revenue sharing logic' from their launch stages.

But that doesn’t mean the risks have disappeared.

The fee switch has not yet officially launched, and all valuation expectations are still based on 'reasonable' assumptions;

A 2% perpetual inflation mechanism was launched this year. Before dividends are realized, each newly added UNI actually dilutes the value of existing holders;

In addition, the activation of the fee switch does not mean that everyone can 'sit back and enjoy the benefits'; dividends may require thresholds, and the actual proportion of those who can enjoy cash flow sharing is still unknown.

The most critical risk lies in—everything still depends on DAO decisions.

But this time, at least we have seen Uniswap striving forward with great ambition.

Conclusion: Beyond valuation is a bet on direction

At this point, it can be confirmed that Uniswap's valuation logic has indeed reached a turning point.

The only lagging factor is the market sentiment and pricing model.

From the current data, Uniswap's trading volume has returned to a high level, and the revenue sharing mechanism is beginning to have the possibility of implementation, while the cash flow model is reshaping the market's understanding of UNI. Compared to the vague narratives during the bubble period, today's Uniswap has a stronger foundation for 'value return.'

Of course, the valuation model can only tell us: 'If everything goes smoothly, how much can UNI be worth?'

Ultimately, UNI's value lies not just in whether it can provide dividends, but in whether it can regain its voice at the moment when the DeFi narrative is least favored.

Because the market does not always price rationally, but it will always catch up eventually. And this time, perhaps it is time to go back to class.

The data in this article is based on statistics from August 8 to August 10, 2025, and subsequent situations may vary.