Original author: Alex Liu, Foresight News

Reprinted by: Luke, Mars Finance

Recently, PENDLE's price has been strong, reaching a near 7-month high. Besides the fundamentals of Pendle V2 itself, the newly launched product Boros, which took two years to refine, is seen by the market as the next growth hotspot.

Boros allows traders to go long or short on funding rates; the author believes that besides acting as a speculative tool, it is also a potential 'hedging tool', from which third-party protocols such as Ethena and Neutrl will benefit.

In other words, Pendle's new product will be favorable for ENA. To clarify the cause and effect, we must first understand what funding rates are.

Funding Rate

Funding fees arise in perpetual contract trading to ensure that there is no significant price difference between the contract price and the spot price. When there are more long positions than short positions, the contract price is greater than the spot price, at which point the funding rate is positive, and long positions must pay funding fees to short positions at fixed intervals (usually every 1-8 hours). Conversely, when there are more short positions than long positions, short positions will pay funding fees to long positions.

Funding rates can reflect market sentiment; for example, when funding rates are negative (i.e., shorts must pay fees to longs), it reflects that the market generally expects a bearish outlook. It is worth noting that when market sentiment is neutral, funding rates are positive, as longs always outnumber shorts.

Mechanism and pain points of Ethena

The primary source of income for Ethena's synthetic dollar stablecoin is 'funding fee arbitrage'. For example, Ethena purchases ETH with part of the stablecoins deposited by users and stakes it, then opens a corresponding short position on the exchange. This way, the profits and losses of the spot and contracts offset each other, achieving risk neutrality (profit is independent of price fluctuations).

In the above example, the spot ETH position can earn an annualized staking yield of about 3%, while in a neutral or bullish sentiment, the short contract position will continuously earn funding fees paid by the longs. Relying on the combination of these two income sources, Ethena's sUSDe delivered an annual return of over 10% in the long-term slow bull of 2024, with returns being quite attractive after accounting for risks.

The problems with this model are also quite obvious; if the market turns bearish, short sellers must pay funding fees, and Ethena will have to stop the above strategy due to losses, withdrawing funds to deploy to safer but lower-yield protocols like Sky. For instance, half a month ago, the APY of sUSDe was 12%, but due to last week's market pullback, the APY dropped below 5%.

If one could short funding rates at high levels, hedging the funding rates, adding another layer of hedging to the hedging strategy, Ethena's high APY could be 'locked in', solving the pain points.

You can short funding rates; isn't that Boros?

Boros Gameplay

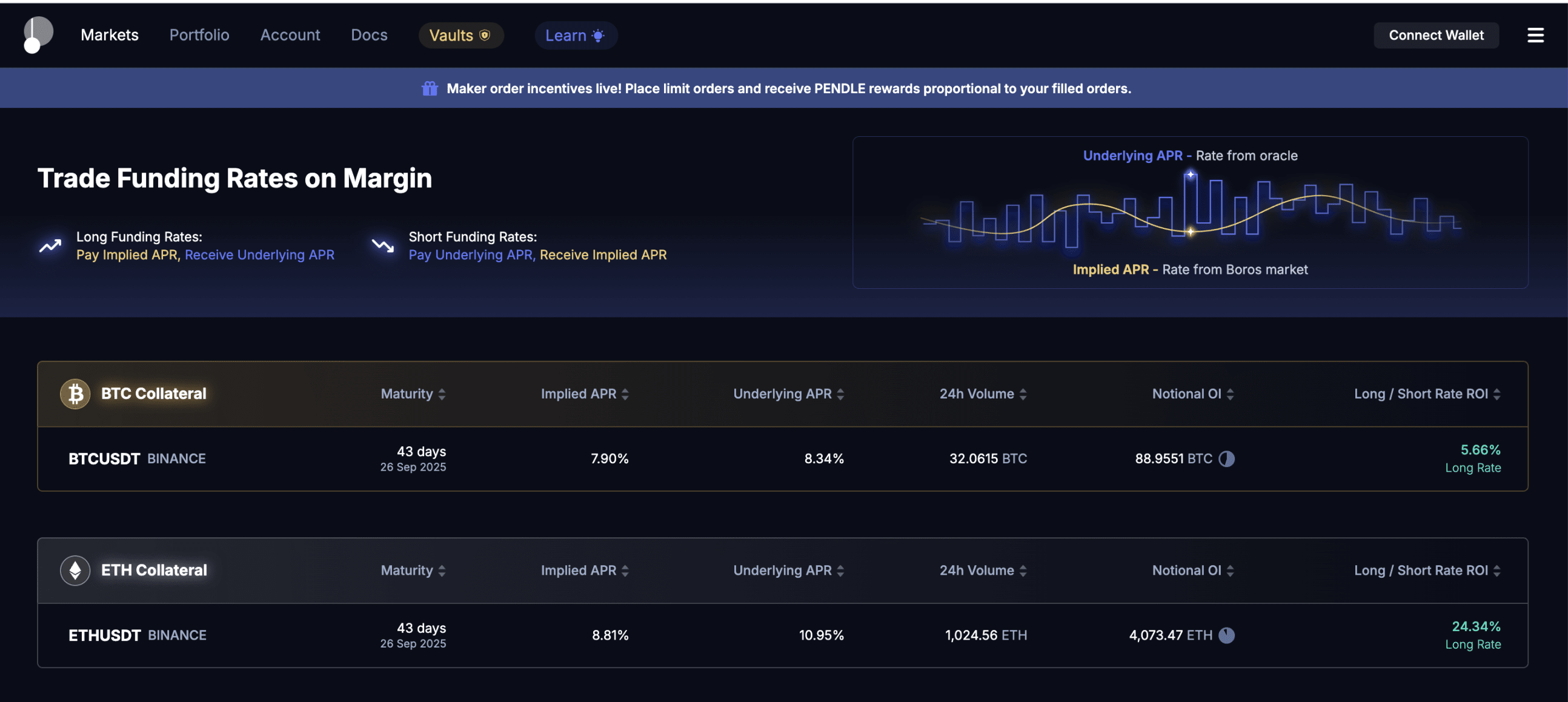

Boros abstracts the funding fees generated by a unit of underlying asset in perpetual contracts within a certain timeframe as Yield Unit (shortened as YU). Users go long on YUs if they believe funding rates will rise, and short if they believe funding rates will fall; opening positions requires depositing collateral, and the logic is very simple.

Here are a few concepts introduced. The current market pricing of the trading funding rate is referred to as Implied APR (Implied Annual Percentage Rate), while the actual annualized value of the funding rate is called Underlying APR. Therefore, going long on YUs essentially means choosing to pay the corresponding YU's fixed funding rate according to the Implied APR at the time of purchase for the next term, gaining actual funding based on the ever-changing Underlying APR, while going short on YUs is exactly the opposite.

Thus, Ethena can completely short the YUs corresponding to its strategy's short position when funding rates are at relatively high points, locking in satisfactory funding income.

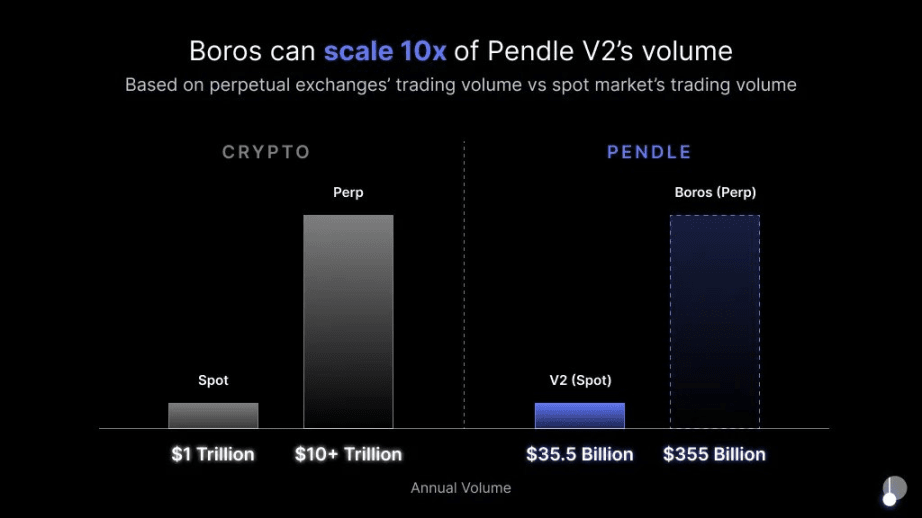

Boros has shown remarkable data post-launch, achieving $15 million in open positions on its first day and a striking nominal trading volume of $36 million. The Pendle team also holds high hopes for its development potential, believing it can achieve trading volumes ten times that of the current flagship product Pendle V2 since perpetual contract trading volumes in the crypto market are already over ten times those of spot trading, and Pendle V2 and Boros also represent the relationship between spot and contracts.

Neutrl, another client

Boros' shorting feature for funding rates makes it a 'hedging tool'; besides Ethena, which other protocols might be willing to pay for it?

Let's take another example, Neutrl. Neutrl is also a synthetic dollar stablecoin protocol currently in closed beta testing, with a total locked value exceeding $50 million. Its yield model is: purchasing the locked tokens at a discount through OTC, then shorting an equivalent amount of tokens for hedging, thus achieving OTC discount arbitrage.

One of Neutrl's biggest risks is the uncontrollable funding rates; extreme rates in extreme market conditions could lead to losses. Boros has found its PMF (Product-Market Fit) here.

Current limitations of Boros

Boros has just launched and is in the very early stages, with many limitations. Many of the theoretical use cases mentioned above are still just ideas, awaiting Boros to make continuous progress to turn these 'clients' into reality.

First is the scale issue. Ethena's shorting volume exceeds tens of billions of dollars, making it a quality potential client, but whether Boros's funding fee perpetual market can create enough liquidity to handle this business remains to be seen.

Secondly, there is the issue of the number of supported assets; Boros currently only supports funding fees for BTC and ETH. Ethena only deals with major assets, but to turn Neutrl into a client, it needs to support more 'VC' coins and ensure relatively low-profile assets have liquidity support.

Conclusion

While the newly launched Boros has many limitations, its design has already provided us with a vast imaginative space for use cases. Where there are opportunities, there will be trading volume; where there is trading volume, there will be fees.

Pendle's new product is favorable for ENA. When it synergizes with third-party protocols to bring massive trading volume, protocol fees will also flow to Pendle. Pendle's new product is seeking to become the new DeFi infrastructure, benefiting major related protocols, ultimately benefiting the PENDLE token.