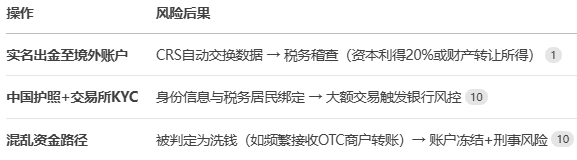

Information exchange mechanism

Banks in CRS member countries such as Hong Kong and Singapore are required to regularly report to mainland tax authorities: account balances, annual transaction records, and account holder identity information19.

Key trigger point: Single transfer > $500,000 or annual cumulative transfer > $1,000,000 (Hong Kong standard), automatically triggering data exchange7.

The chain reaction of exchange KYC

Exchanges such as Binance and OKX cooperate with FATF supervision. Large withdrawals (e.g., >100,000 USDT per day) may trigger a suspicious transaction report (STR) from a financial institution10.

Typical Cases

Zhejiang case in 2024: A user received OTC funds through a Hong Kong account and was required to pay 1.41 million yuan in taxes due to CRS exchange1.

Basic operations in the cryptocurrency world

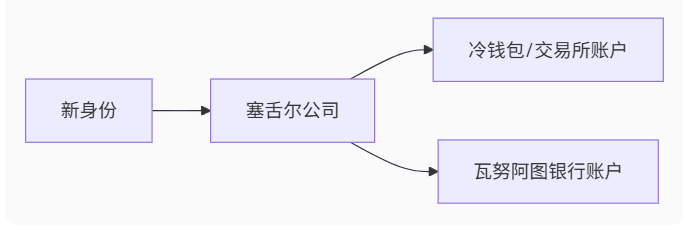

Compliance Solution (Four-Step Refactoring)

1. Identity Segregation: Non-CRS Country Identity

Preferred countries: Panama (residency for a $300,000 home purchase), Nicaragua (citizenship through a $100,000 investment)

Core function: Cut off the CRS information exchange chain and open an exchange/bank account with a new identity9.

2. Asset structure: offshore company holding

Advantages: Capital flow is shown as “company operation”, not personal income9.

3. Closed-loop design for deposits and withdrawals

Path: Withdraw from the exchange to your company wallet → Exchange to an offshore account at a licensed OTC dealer → Physical card purchase/cross-border wire transfer

Key: Avoid handling personal accounts of CRS member countries, and ensure that single transfers are less than $200,000.

4. Tax filing optimization

Offshore companies: Choose a jurisdiction with no capital gains tax (such as BVI) and only declare corporate income tax (0-5%)9.

Loss deduction: Keep complete transaction records, and losses can be offset against profits (for example, Taiwan allows deduction of property transaction losses)

Emergency Response

If you have received a tax inquiry letter:

1. Immediately freeze the associated account to prevent new transaction records from being tracked.

2. Material preparation:

Offshore company registration documents (if any)

Transaction records proving the source of funds (such as OTC orders, on-chain transfers)

3. Professional Defense:

Claim that “digital commodity transactions” are not taxable income (China currently has no clear regulations)1

Refer to the Fujian case: cooperating with the investigation can result in a 30% reduction in sentence.

Ultimate advice

Short-term: Complete non-CRS identity + offshore company registration within 3 months and transfer existing assets.

long:

Use an offshore physical card (such as Wirex) to spend cryptocurrencies directly, avoiding fiat currency conversion9.

Pay attention to the Hong Kong digital RMB pilot program, and compliance channels may become the future option10.

Remember: the essence of CRS is to "track funds," not "monitor on-chain transactions." Using a real-name account to receive OTC withdrawals is equivalent to proactively "submitting evidence" to the tax authorities. 19 Planning ahead is 90% less expensive than remediating afterward.

People are more important than anything else! If you are still confused, you might want to check out @crypto广哥 to help you snipe every wave of the bull market.