Original title: (Six Pillars of On-Chain Protocols, HyperEVM Faces Off Against Ethereum)

Original source: Zuo Ye Wei Bo Shan

Ethereum returns with DeFi once again. Aave/Pendle/Ethena makes circular lending a lever amplifier. Compared to the on-chain stack based on ETH during DeFi Summer, the leverage ascent curve supported by stablecoins like USDe is more gradual.

We may be entering a warm long cycle, and the examination of on-chain protocols will be divided into two parts. The first involves more asset types, and external funding liquidity will be more abundant under the expectation of Federal Reserve rate cuts. The second examines the extreme value of leverage multiples, corresponding to the process of safely deleveraging, i.e., how individuals can exit safely and how bull markets will end.

The six crypto protocols: interaction between ecology and tokens.

There are countless on-chain protocols and assets, but under the 80/20 rule, we only need to focus on parameters such as TVL/ trading volume/token price. More specifically, we should focus on the few indispensable individuals in the on-chain ecosystem, and examine their relationships within the ecological network to consider individuals' importance, ecological connectivity, and the highest growth potential in new protocols.

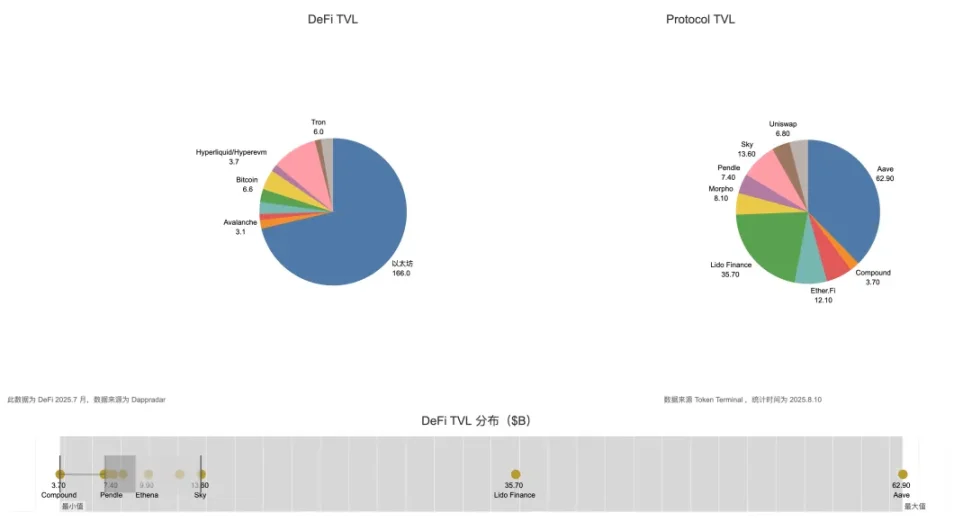

Image description: DeFi TVL Overview, image source: @zuoyeweb3

In the composition of DeFi TVL, Ethereum accounted for over 60% of DeFi TVL in July, and Aave accounted for over 60% of Ethereum's ecological TVL. This is the 20% in the 80/20 rule, meaning that the remaining protocols must have strong connections with both to be included as main active beneficiaries.

With the flywheel of the three musketeers of circular lending starting, the correlation between Ethereum, Aave, Pendle, and Ethena goes without saying. Adding Bitcoin, WBTC, ETH, and USDT/USDC are the de facto foundational assets of DeFi. However, similar to Lido, USDT/USDC only possess asset attributes and lack ecological value, while Plasma, Stablechain, etc., have just begun to compete.

To make a distinction, a protocol can possess multiple values. For instance, Bitcoin primarily has asset value; everyone needs BTC, but no one knows how to utilize the Bitcoin ecosystem. This is not to say that BTCFi is a scam (just a joke for safety).

ETH/Ethereum possesses dual value; everyone needs ETH and the Ethereum network, including EVM and its extensive DeFi stack and development facilities.

Further classification based on assets and ecological value examines the 'degree of being needed' among top protocols. Each needed asset attribute scores a point, and each needed ecological value scores a point, leading to the following summary table:

Pendle/Aave/Ethena/Ethereum/HyperEVM/Bitcoin are the six protocols with the strongest linkages. Any two can couple with each other, requiring at most one additional protocol or asset to connect.

Let's explain briefly:

1. Ethena <> HyperEVM: USDe has already been deployed to the HyperEVM ecosystem.

2. Pendle <> HyperEVM: $kHYPE and $hbHYPE rank first and third respectively in the trend list.

3. Aave <> HyperEVM: Hyperlend's TVL accounts for 25% of HyperEVM ($500M vs. $2B), as it is a friendly fork of Aave, promising to share 10% of profits with Aave.

4. BTC/ETH are the two cryptocurrencies with the largest trading volume on Hyperliquid, and can be deposited and withdrawn through Unit Protocol.

5. Pendle, Aave, and Ethena have already become a whole, but USDe's asset attributes are recognized, while the ecological value of $ENA is slightly inferior.

6. Pendle's new product Boros uses funding rates as the basis for trading, with BTC and ETH contracts being the top choices.

7. Aave needs WBTC and various ETH types, such as staked ETH, especially as Ethereum's ecological value as infrastructure is needed by Aave/Pendle/Ethena, serving as on-chain support for ETH prices.

8. The most special aspect here is that the Ethereum ecosystem unidirectionally needs BTC, while the Bitcoin ecosystem does not need any external assets.

9. Ethena has no relation to Bitcoin/BTC.

10. HyperEVM/Hyperliquid is the 'most proactive' external ecosystem, giving a strong impression of 'I am here to join this family.'

According to statistics, these are the six most closely linked assets. The introduction of any other ecosystem and tokens will require more assumption steps. For example, Lido, which is second in TVL, has a weak relationship with Hyperliquid and Bitcoin. After Pendle 'abandoned' LST assets to invest in YBS, Lido's ecological linkage within Ethereum will weaken.

We base on the highest BTC value of 7, dividing the six assets into three nodes based on their influence on other protocols. Please note, this is not a depiction of asset value but a ranking of their importance within the ecosystem.

BTC/ETH is the strongest infrastructure, with BTC excelling in value attributes and ETH maintaining an unshakable ecological status. If you include Solana in the calculation of linkage degree, you will find it does not compare to the linkage of Hyperliquid/HyperEVM to Ethereum. The core reason lies in the trading attributes of Hyperliquid, which align more closely with the EVM ecosystem.

· Within Ethereum, Lido/Sky and the existing six protocols have insufficient interaction.

· Outside of Ethereum, Solana/Aptos has insufficient interaction with the existing six protocols.

However, Solana needs to support its own DEX to accommodate more external assets, which naturally requires an additional assumption step. SVM compatibility with the EVM ecosystem will also be more challenging. In short, everything in Solana needs to develop independently.

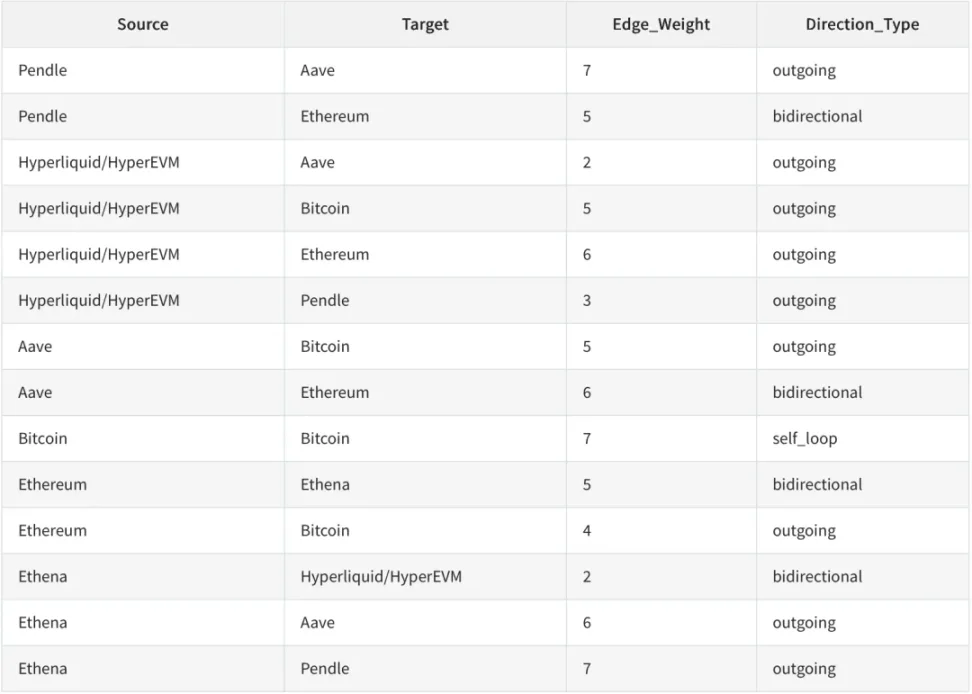

Image description: Connectionism, image source: @zuoyeweb3

However, in the network of relationships, the synergistic effect of the Ethereum ecosystem is the strongest. $1 of Ethena is hedged through ETH, then flows into Pendle and Aave for value circulation. The Gas Fees generated above become the value support for ETH.

Apart from Bitcoin naturally relying on BTC for value self-circulation and self-flow, ETH is closest to a value closed loop, but this is the result of active and proactive actions. The combination of Hyperliquid/HyperEVM is still in progress, and whether it can complete the linkage of trading (Hyperliquid) + ecology (HyperEVM) and $HYPE remains to be seen.

This is a process of increasing entropy with gradually more assumptions. BTC needs only itself, ETH needs an ecosystem and tokens, while $HYPE needs trading, tokens, and an ecosystem.

Does the expansion of DeFi have an end?

As mentioned earlier, Hyperlend needs to share profits with Aave. Aave's influence is not limited to this; in fact, Aave is the main character of the circular lending initiated by Pendle and Ethena, bearing the leverage of the entire circular system.

Aave is the closest existence to becoming the on-chain infrastructure of Ethereum, not because it has the highest TVL, but due to a comprehensive consideration of safety and capital volume. The safest way for any public chain and ecosystem to start a lending model is to fork Aave compliantly.

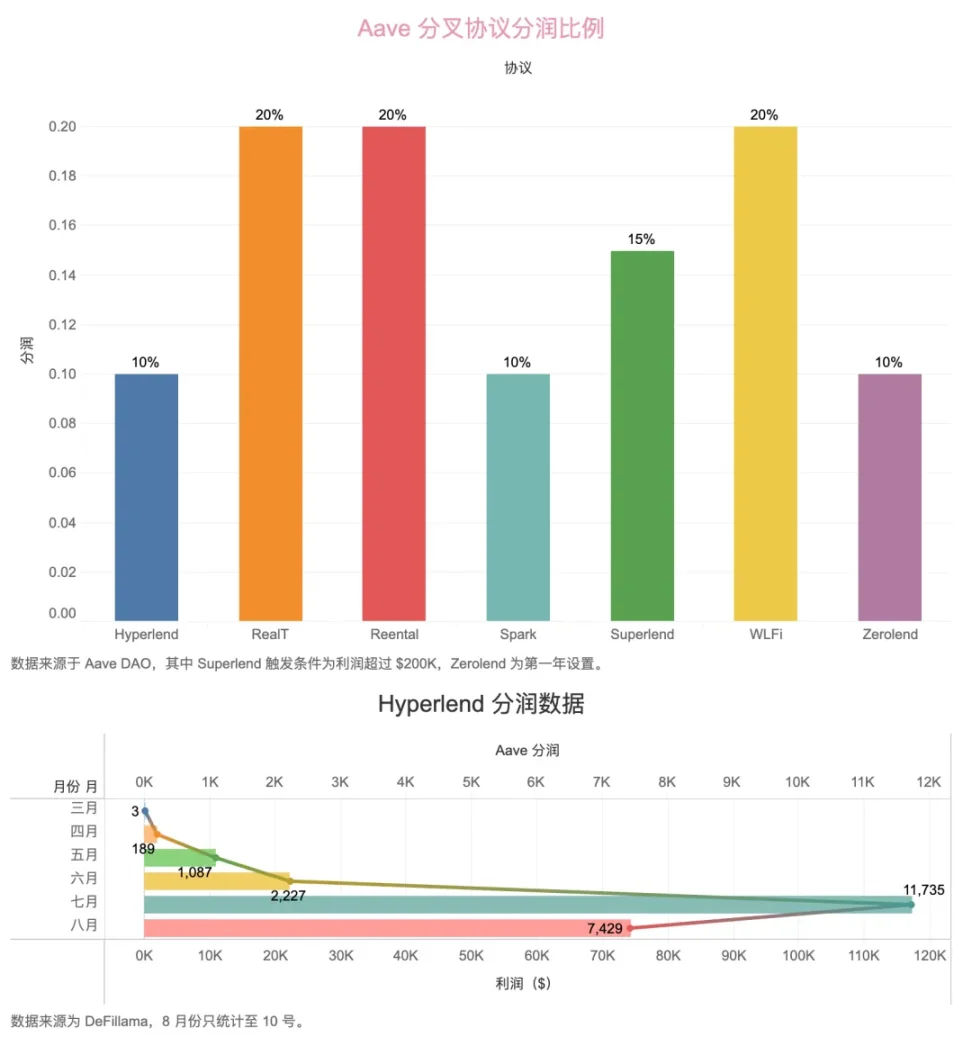

Image description: Aave and Hyperlend profit-sharing setup, image source: @zuoyeweb3

In the forking model of Hyperlend, a 10% profit share is fundamental. Additionally, 3.5% of its own tokens are allocated to Aave DAO and 1% to stAave holders. This means Aave is selling itself as a service to various ecosystems, which connects its ecological value and token value.

However, it is not without competitors. Maple has expanded to HyperEVM, and new forms of lending agreements like Fluid and Morpho are also competing fiercely with new assets like YBS. As the strongest competitor in the Ethereum EVM ecosystem, HyperEVM may not maintain peace indefinitely.

In terms of proactivity, Bitcoin and HyperEVM are absolute extremes. HyperEVM is siphoning traditional trading types onto the chain through HIP3, connecting the liquidity of HyperCore and HyperEVM via CoreWriter, and supporting its front-end agents through Builder Code.

In addition, it leverages Unit Protocol and Phantom to connect funding in the Solana ecosystem, siphoning all on-chain liquidity, which is also a way to expand infrastructure.

To summarize:

· Pendle targets all types of assets that can be split, expanding the derivatives market beyond perpetual contracts, in the broad sense of the interest rate swap market.

· Ethena leverages the DeFi circular lending model and treasury strategy to create a stablecoin third pole starting from $ENA and $USDe, $USDtb. The basic use of USDT/USDC remains trading and payment, while USDe aims to become a risk-free asset in the DeFi space.

· Aave has already become the de facto lending infrastructure, its status tightly bound to Ethereum.

· Bitcoin and Ethereum represent the limits of the blockchain economic system. The extent of their expansion is the basis for DeFi growth, specifically how much BTC can be migrated to DeFi and how large the growth interval for DeFi is.

· Hyperliquid/HyperEVM has already tightly bound existing DeFi giants in the ecosystem. Although its TVL is far less than Solana's, its growth prospects are greater. Solana's narrative is about defeating the EVM system from the public chain perspective.

Conclusion

The six crypto protocols examine the degree of interlinkage among themselves. This does not mean that other protocols lack value; rather, high cooperation density will exponentially increase the freedom and utilization of funds, leading to mutual benefits.

Of course, one loss will lead to another, which requires examining the subsequent development of DeFi re-anchoring—from switching from ETH to YBS. As a high-value asset, ETH is more aggressive in leverage, while YBS, like USDe, is naturally more price-stable (not value-stable). This makes DeFi Legos based on it more solid, theoretically allowing for a gentler curve for both leveraging and deleveraging, except in extreme decoupling situations.

There are limited seats in the crypto pantheon. New electors can only strive to move forward, connect with existing deities, and build the strongest protocol network to earn their place.

Original link