Original title: (SignalPlus Macro Analysis Special Edition: Summer Break)

Original source: SignalPlus

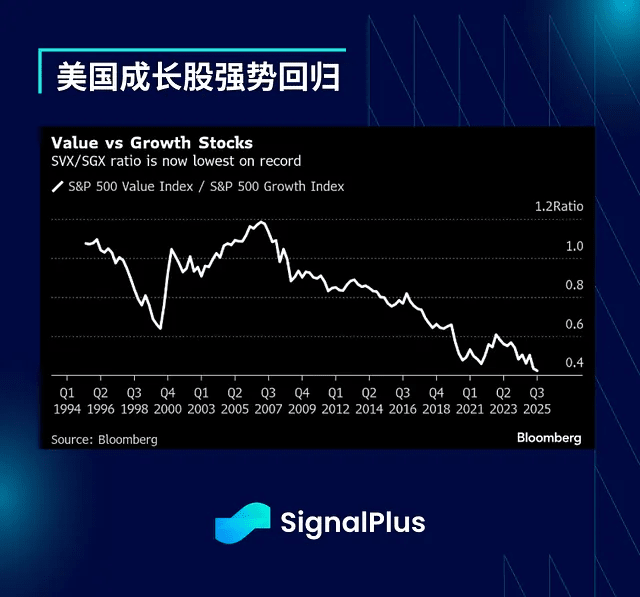

This week, there haven't been many new developments to report, as the S&P 500 index rebounded from the shock after the non-farm payroll data was released, getting close to its all-time high again. On the other hand, the Nasdaq index benefited from strong earnings reports, setting a new record while ignoring the ongoing political turmoil of the Trump administration and the new import tariff issues.

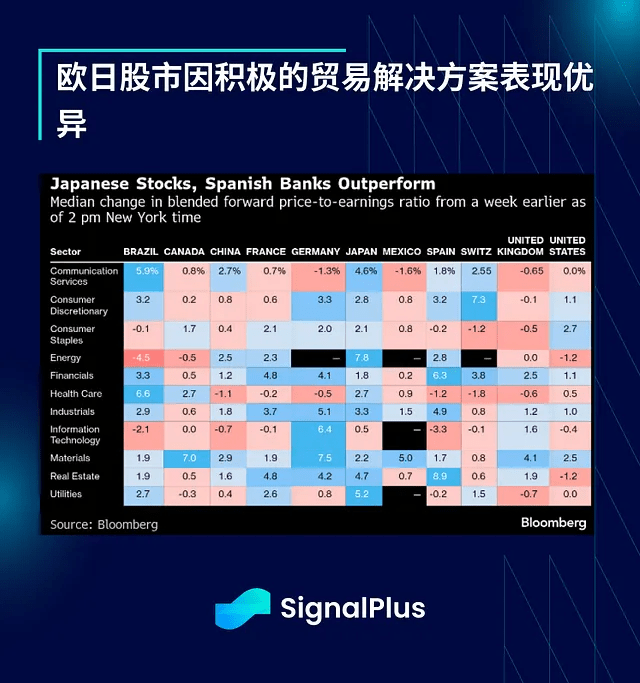

Global risk assets have also performed well, with European and Japanese stock markets rising due to ongoing trade solutions, while the U.S. has made concessions on tariffs and automotive tax reductions.

On the other hand, the U.S.-China trade truce agreement is set to expire this week, with some market participants expecting the deadline to be extended again, but others are concerned that the U.S. may impose new tariffs because of China's purchase of Russian oil—India has already been sanctioned for similar behavior.

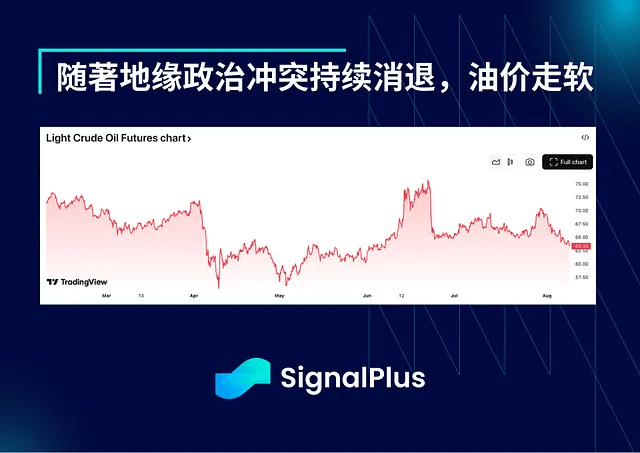

The good news is that the U.S. and Russia plan to draft a new peace agreement for Ukraine before this week's Alaska summit, providing another tailwind for risk assets and pushing down oil prices due to the continued decline of war premiums.

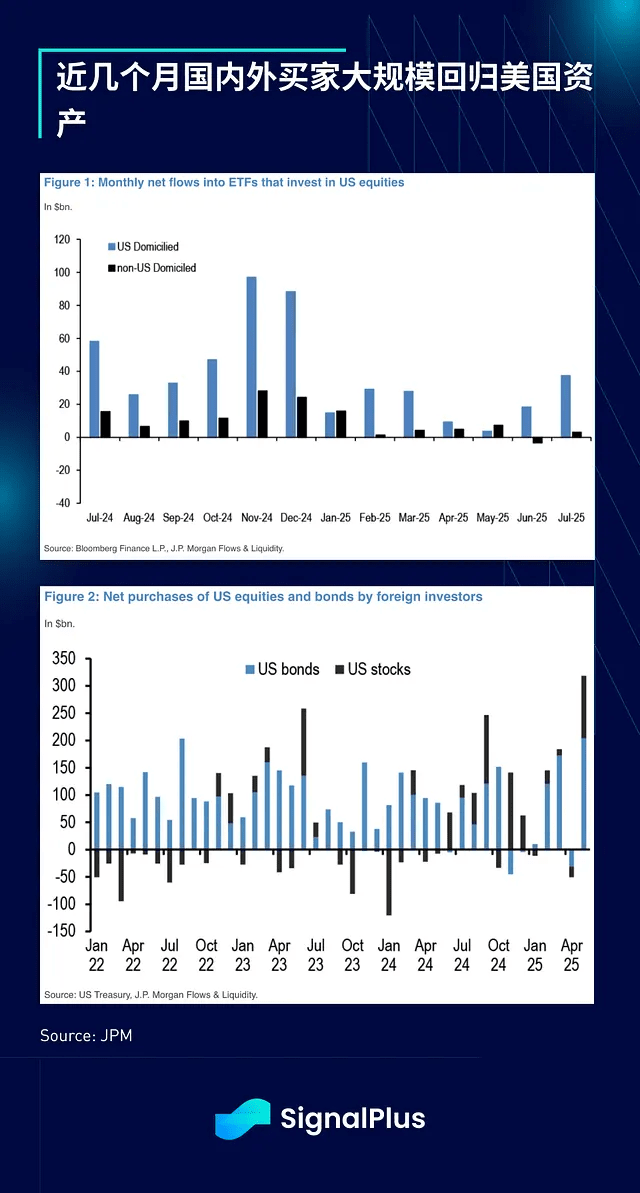

U.S. capital flows remain strong, with domestic and foreign investors returning en masse. The latest data shows that net purchases have set a new monthly inflow record, and trading volumes have also hit new highs, providing positive confirmation.

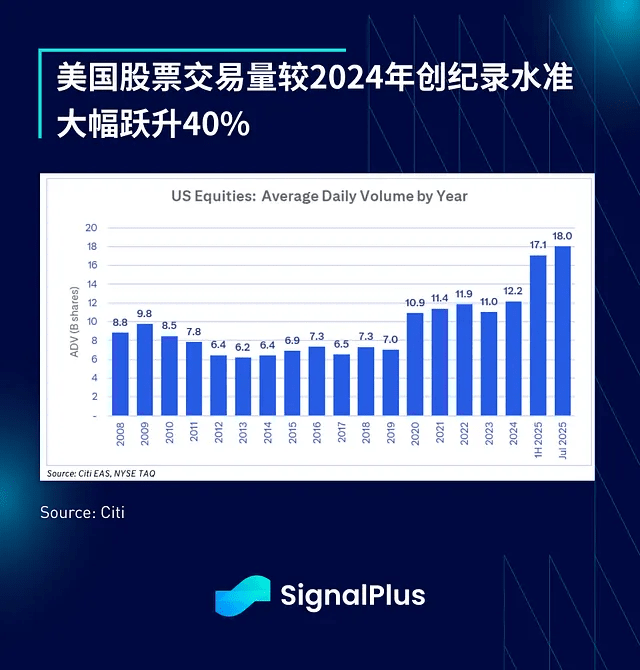

In 2025, the trading volume of the U.S. stock market hit a record high, far exceeding previous years, primarily due to a strong return of retail trading year-to-date. According to Citigroup data, the average daily trading volume in the first half of 2025 was nearly 50% higher than the average level of the previous five years, marking a significant leap of 40% compared to the previous record set in 2024. This trend continued in July, with the average daily trading volume reaching 18 billion shares.

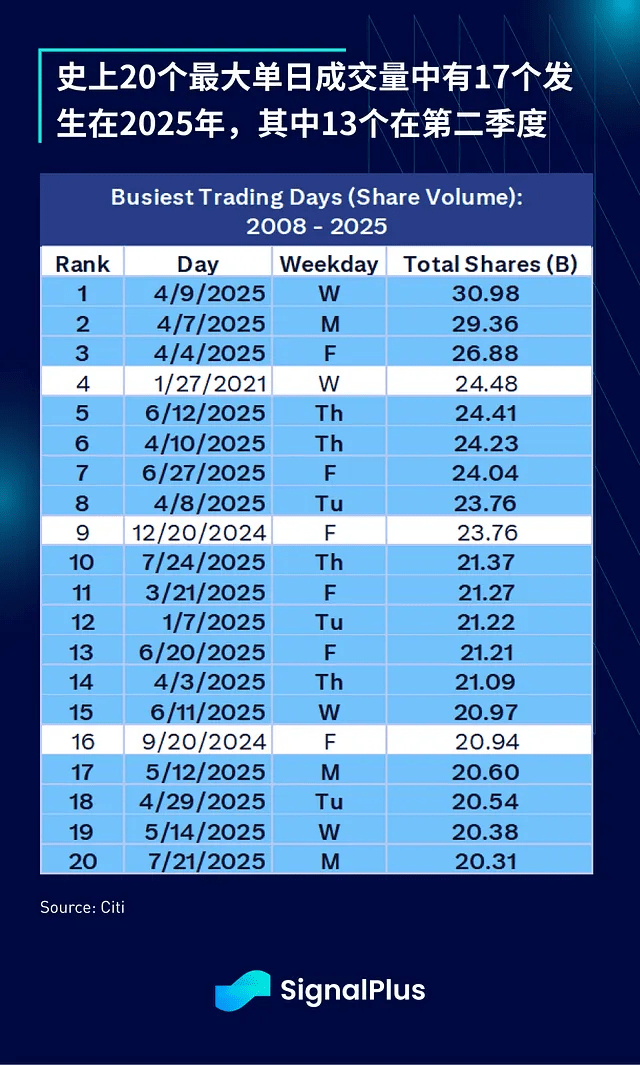

In fact, 2025 has been so remarkable that 17 of the 20 largest single-day trading volumes in history occurred in 2025, with 13 days in just the second quarter. Absolutely incredible.

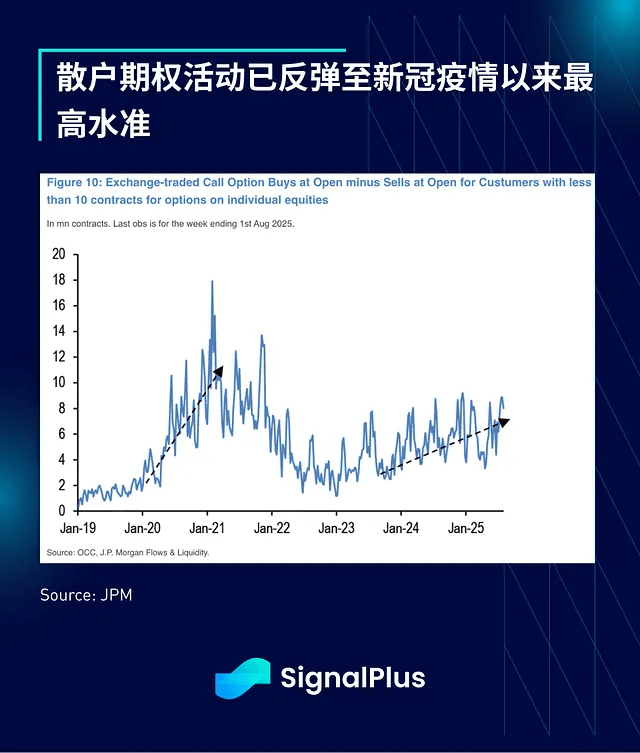

Year-to-date, retail participation has driven extremely high individual stock concentration, with the top five stocks accounting for over 20% of total market volume on certain trading days in 2025. Retail activity in call options has also rebounded significantly, reaching its highest level since the COVID-19 pandemic.

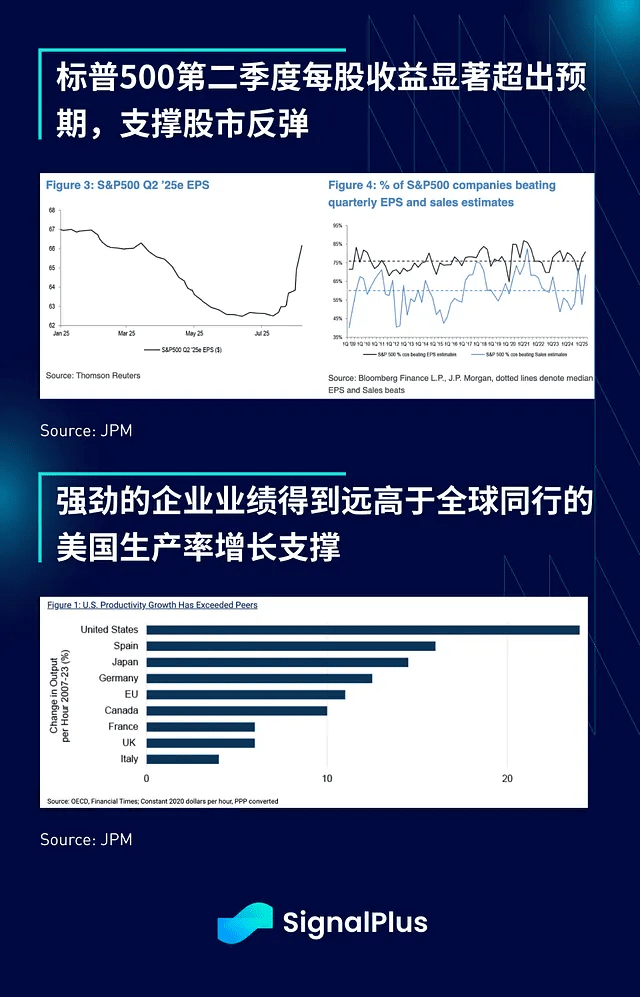

In terms of earnings reports, about 80% of the S&P 500 companies that have reported earnings exceeded expectations, with a year-on-year growth of 12%, and the surprise magnitude reaching 9%, led by the technology and financial sectors. Against a backdrop of lowered expectations due to tariff concerns, earnings per share significantly surpassed expectations for the second quarter of 2025.

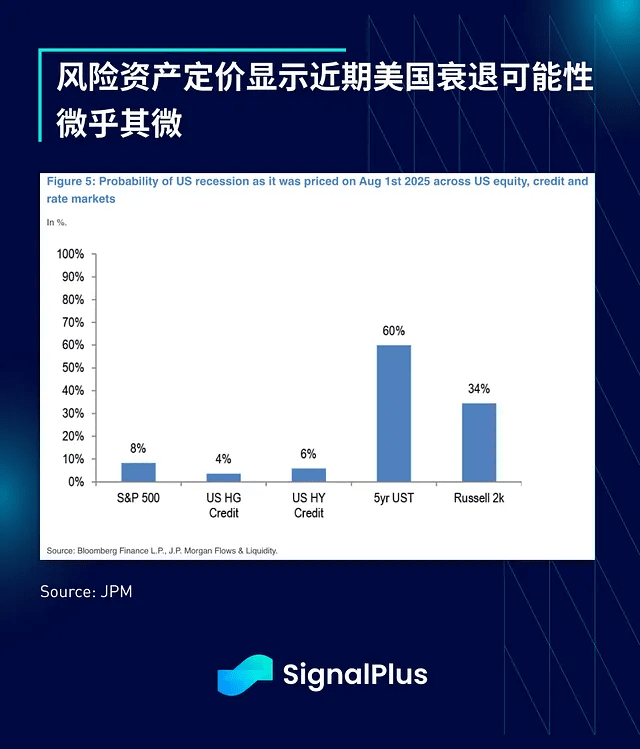

The current rebound has pushed the stock and credit markets' expectations of recession probabilities back to single-digit lows. The U.S. fixed income market, as usual, is an exception, as they remain the most aggressive in pricing further easing from the Federal Reserve.

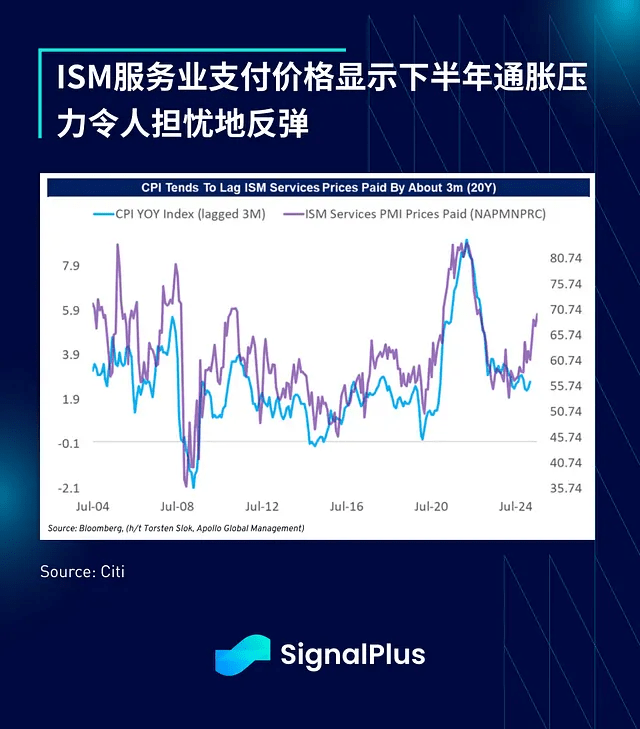

Regarding inflation, although the Federal Reserve has expressed a willingness to overlook recent price pressures, the ISM (Institute for Supply Management) sub-index data shows a concerning rebound in payment prices, which often leads CPI by about a quarter and could complicate the Fed's plans for rate cuts later this year. However, for now, the market is happy to maintain high levels under the dominance of risk appetite until hard data proves otherwise.

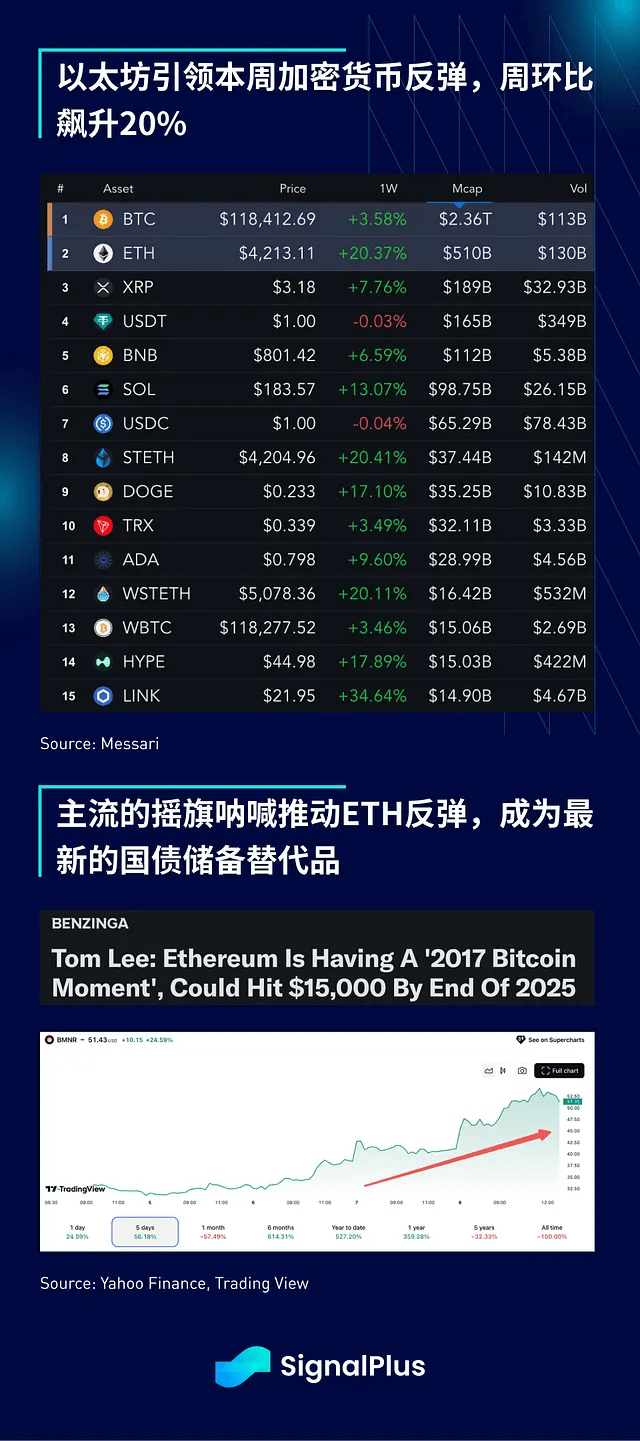

Cryptocurrency also experienced a similar rebound this week, primarily driven by Trump's order for regulators to 'study' the possibility of including cryptocurrencies (and private equity) in 401k portfolios. If this comes to fruition, it would clearly open up huge buying demand. However, there is still a long way to go before it could become law.

Excitingly, Ethereum led the rise this week with a weekly increase of +20%. The latest mainstream experts/followers have touted ETH as the latest FOMO (Fear of Missing Out) asset in the public equity space. Retail traders responded actively, propelling BNMR to nearly a 60% increase this week, showing 'native gamblers' how to properly engage in FOMO in a regulated world.

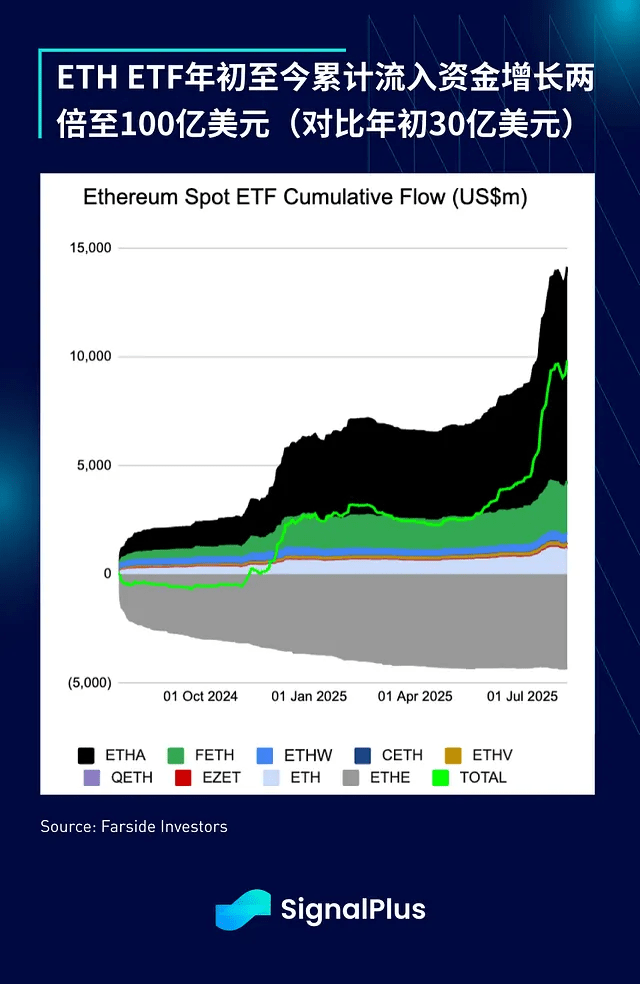

As expected, Ethereum ETFs saw about $700 million in new inflows in the last two days of this week, pushing cumulative inflows to a new historical high, with assets under management doubling year-to-date to nearly $10 billion (vs. $3 billion at the beginning of the year).

The recent rebound of ETH has also led to a divergence in short-term volatility, with Bitcoin's implied volatility still hovering around historical lows, while ETH's volatility has surged significantly. The term structure of ETH is currently inverted, with long-term volatility expected to fall back to around 70%, while BTC's IV curve is the opposite, with short-term volatility severely compressed, and the spot market hovering around $120,000.

For comparison, a month ago, the market priced in only a 5% likelihood of ETH reaching $4,500 in August, while the actual performance in the spot market far exceeded the implied path, catching many participants off guard.

Looking ahead, at this current juncture, we believe there is no strong necessity to chase the market higher, as we expect assets to experience bidirectional volatility over the next month or so. Be wary of potential downturn catalysts such as a significant reversal in the dollar index or unexpected inflation spikes. Traders should remain vigilant and wish you successful trading!

Original link