Original | Odaily Planet Daily

Author | Azuma

Lido (LDO), the leader in the liquid staking space, has finally strengthened recently. According to OKX market data, as of 10:00 AM Beijing time on August 11, LDO is priced at 1.52 USDT, with a 24-hour increase of 14.21%, and a weekly increase of as much as 64.5%.

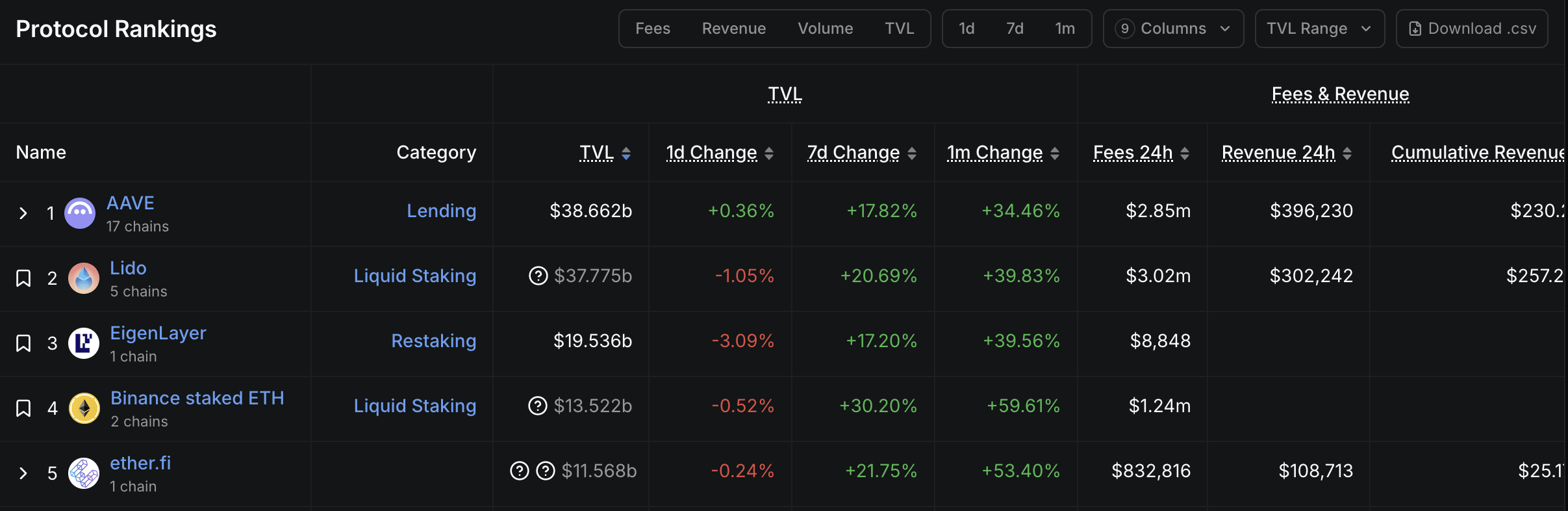

As the largest liquid staking protocol in the Ethereum ecosystem, Lido has long dominated the total locked value (TVL) ranking in the Ethereum ecosystem and even the entire on-chain ecosystem. Although it has recently been overtaken by Aave, which has rapidly grown due to the borrowing of USDe assets, Lido remains one of the protocols with the most influence in the entire Ethereum ecosystem.

The logic behind LDO's recent price surge can generally be attributed to both macro and micro levels.

Macro: Regulatory clarity on attributes, progress of staking ETFs.

First, at the macro level, on August 6, the U.S. Securities and Exchange Commission officially released a statement on certain liquid staking activities, which clearly pointed out that 'liquid staking activities' related to protocol staking do not involve the issuance and sale of securities, unless the deposited crypto assets are part of an investment contract or bound by an investment contract. Participants in liquid staking activities do not need to register transactions with the SEC under securities law, nor do they need to meet the registration exemption provisions under securities law regarding these liquid staking activities.

In June 2024, when Gary Gensler was still at the helm of the SEC, the agency accused Lido and Rocket Pool and other liquid staking projects of being securities. On that day, LDO fell more than 10% due to this negative news and remained in a downturn for a considerable period thereafter. Just a year later, the new SEC's statement clarified that its business model does not involve securities, effectively loosening regulatory constraints for the subsequent operation and development of such projects.

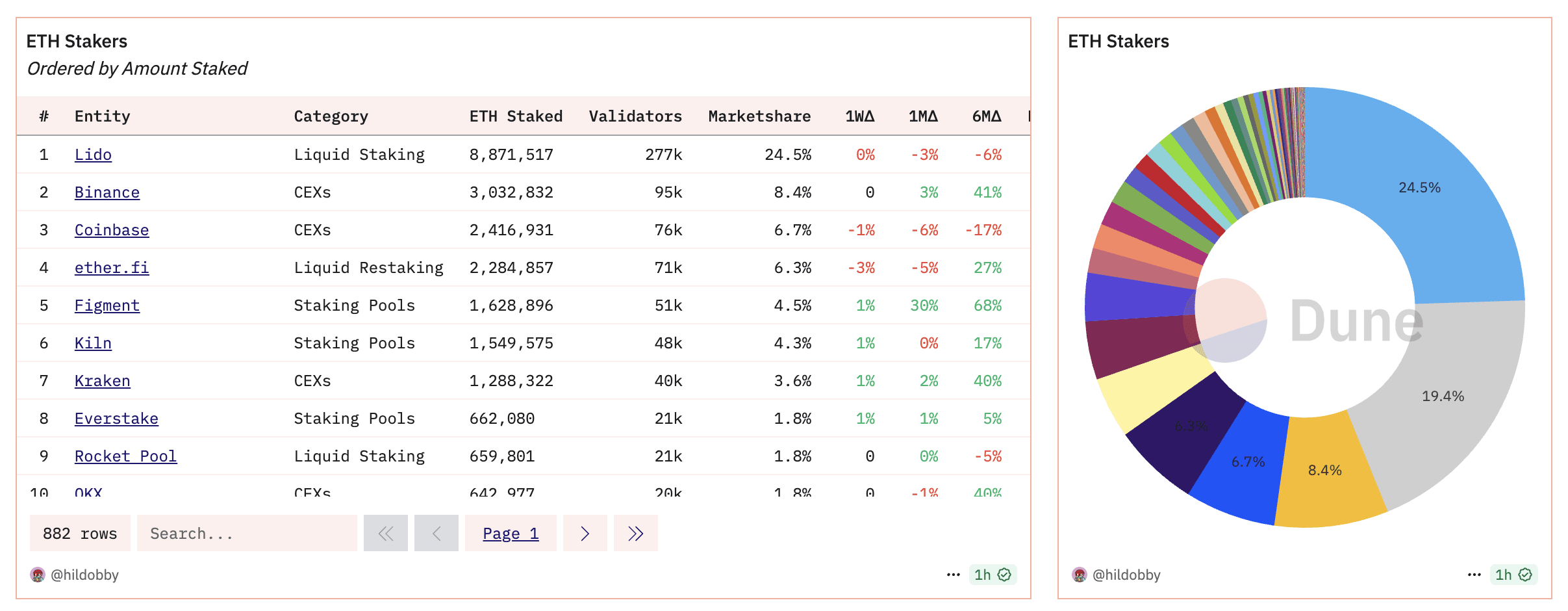

In addition to the regulatory shift, another key development in the staking space is that BlackRock has submitted an application to the SEC to introduce a staking mechanism in its spot Ethereum ETF. Although this application is still under review, given the SEC's attitude, it is expected to be approved without too much difficulty. The market generally anticipates that with the approval of the staking ETF, Lido, which currently accounts for nearly 25% of the Ethereum staking share, is likely to receive a certain boost in business and capital chasing.

Micro: The LDO repurchase plan has finally been put on the table.

Compared to the indirect impact at the macro level, the recent discussions about the LDO repurchase plan may be the direct factor influencing the price trend in the short term.

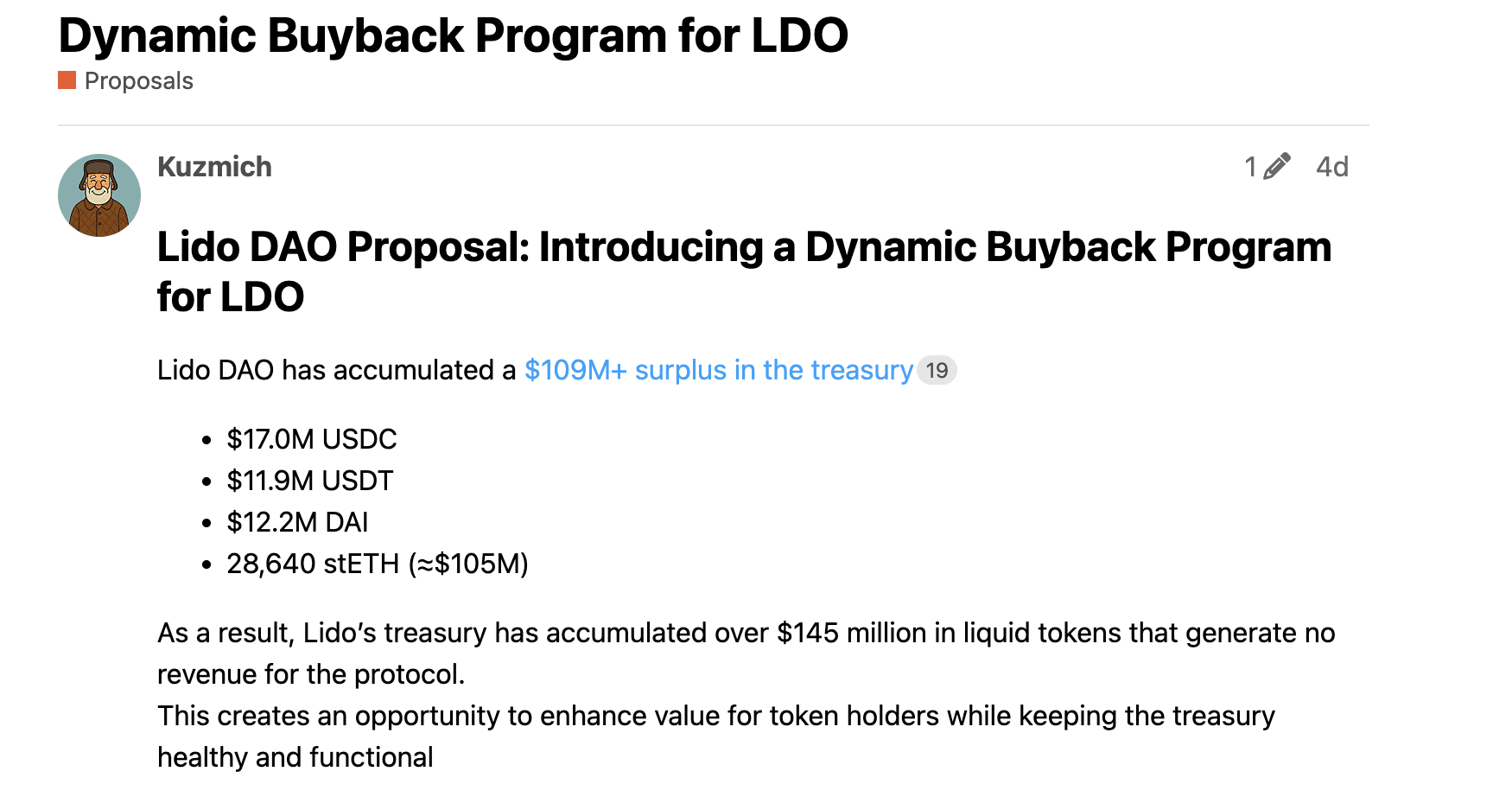

On August 7, Lido community member Kuzmich submitted a draft regarding the 'LDO repurchase plan' to the governance forum. The draft mentions that the Lido treasury currently holds liquid assets worth $145 million (17 million USDC, 11.9 million USDT, 1.22 million DAI, 28,640 stETH), but these assets have not generated any revenue for the protocol.

The draft suggests that Lido should dynamically execute LDO repurchases based on treasury balance to improve the utilization of protocol funds, boost LDO prices, and restore market confidence in LDO's value. Specifically, the draft suggests that with the current treasury reserve size, 70% of liquid assets should be used for regular LDO repurchases, and 30% should be retained in the treasury for operational and strategic needs; when treasury liquid assets decrease to between $50 million and $85 million, the ratio will be adjusted to 50% repurchase / 50% retention; when treasury liquid assets fall below $50 million, the ratio will be adjusted to 0% repurchase / 100% retention (repurchase paused until recovery to threshold).

According to the planning of the Lido governance forum, if all goes well, the draft will collect community feedback from August 7 to 14; then discuss it in the Lido token holders' conference on August 14; subsequently, revise the proposal based on feedback from August 15 to 24; and finally submit it for a Snapshot vote on August 25.

Although there is some dissent within the community forum, the majority of users, except for a small number who insist that 'repurchase is just a short-term game,' focus their doubts on the specific details of the plan, such as whether the tokens will be destroyed after repurchase is unclear, and whether the initiation and execution methods of the repurchase are still not clear enough.

Considering that the draft is still in the early stage, it is expected that further modifications will be made after the phone conference discussion. Coupled with the recent rare strong upward movement in LDO prices, there is optimism that this draft or other repurchase plans derived from the discussions will receive significant community support.

Is ETH's 'Prince' finally about to discover its value?

As one of the recognized ETH Betas, LDO's performance over a long period has been difficult to be satisfied with.

AAVE has quickly surged above $300 in the borrowing and repurchase trend; ENA is making significant progress with its borrowing flywheel and treasury plan (see more details (up nearly 50% in a week, will ENA be ETH's biggest Beta?)); PENDLE has opened up new imaginative spaces with Boros (see more details (the funding rate has finally become a tradable asset, how does Pendle's sub-platform Boros disrupt the arbitrage market?)), while LDO has remained in a relatively weak state for a long time, despite expectations for a 'staking ETF' being voiced for a long time, it has never been able to drive LDO's price performance over a relatively long period.

Under the dual stimulation of current macro and micro factors, LDO is finally showing some signs of a trend reversal. Could this be the beginning of the price discovery for this ETH 'Prince'? It's still too early to make a judgment, but there is certainly some hope.