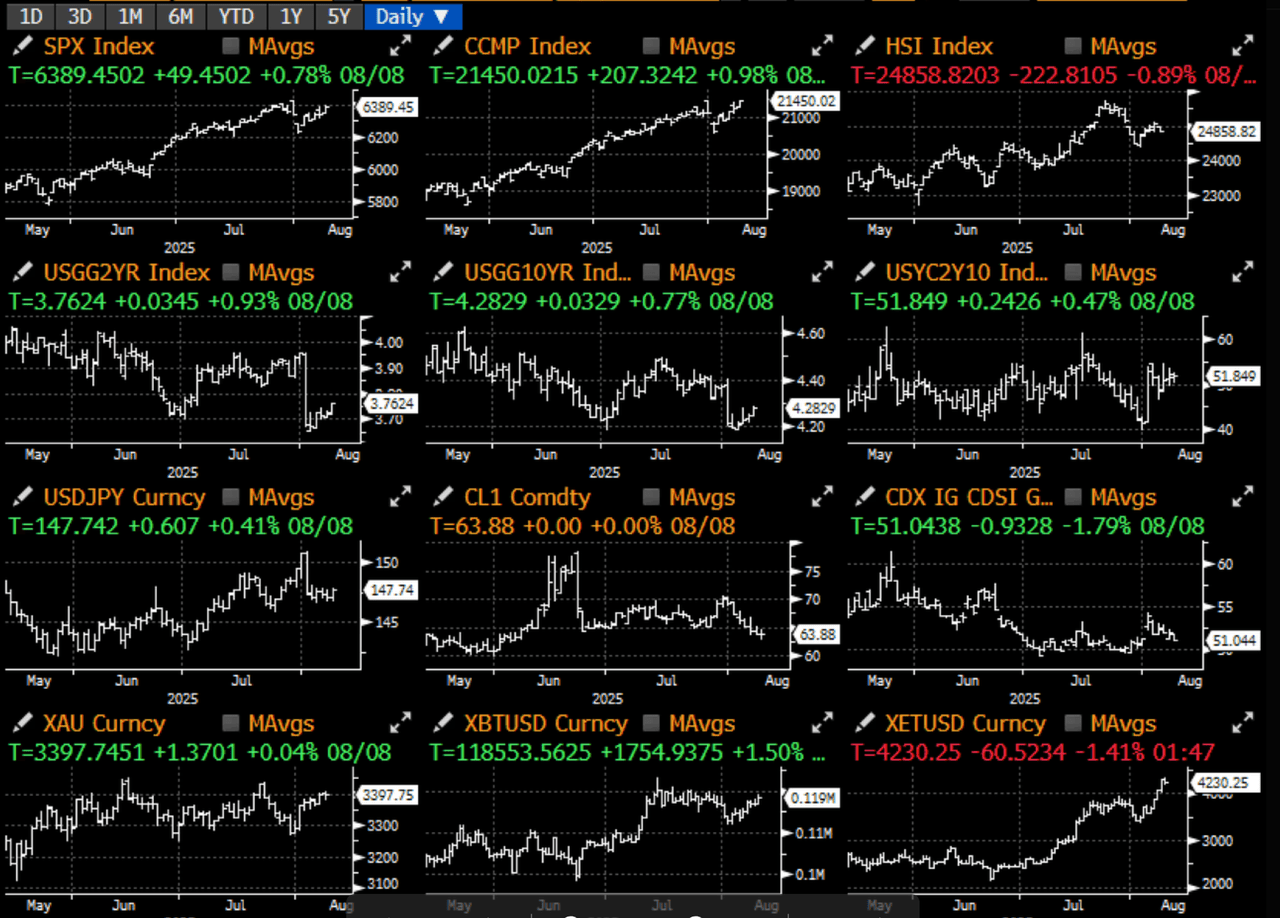

There wasn't much to report this week as the S&P 500 recovered from the post-non-farm payrolls shock and returned near its all-time high. Meanwhile, the Nasdaq benefited from strong earnings reports, hitting a new record despite the ongoing political turmoil within the Trump administration and new import tariffs.

Global risk assets also performed well, with European and Japanese stocks rising on the ongoing trade resolution, with the United States offering concessions on tariff stacking and auto tax breaks.

On the other hand, the US-China trade truce agreement is about to expire this week. Some market participants expect the deadline to be extended again, but others are worried that the United States may impose new tariffs because of China's purchase of Russian oil - India has already been sanctioned for the same behavior.

Positive news is that the United States and Russia plan to draft a new Ukraine peace agreement before their Alaska summit this week, providing another tailwind for risky assets and pushing down oil prices as the war premium continues to fade.

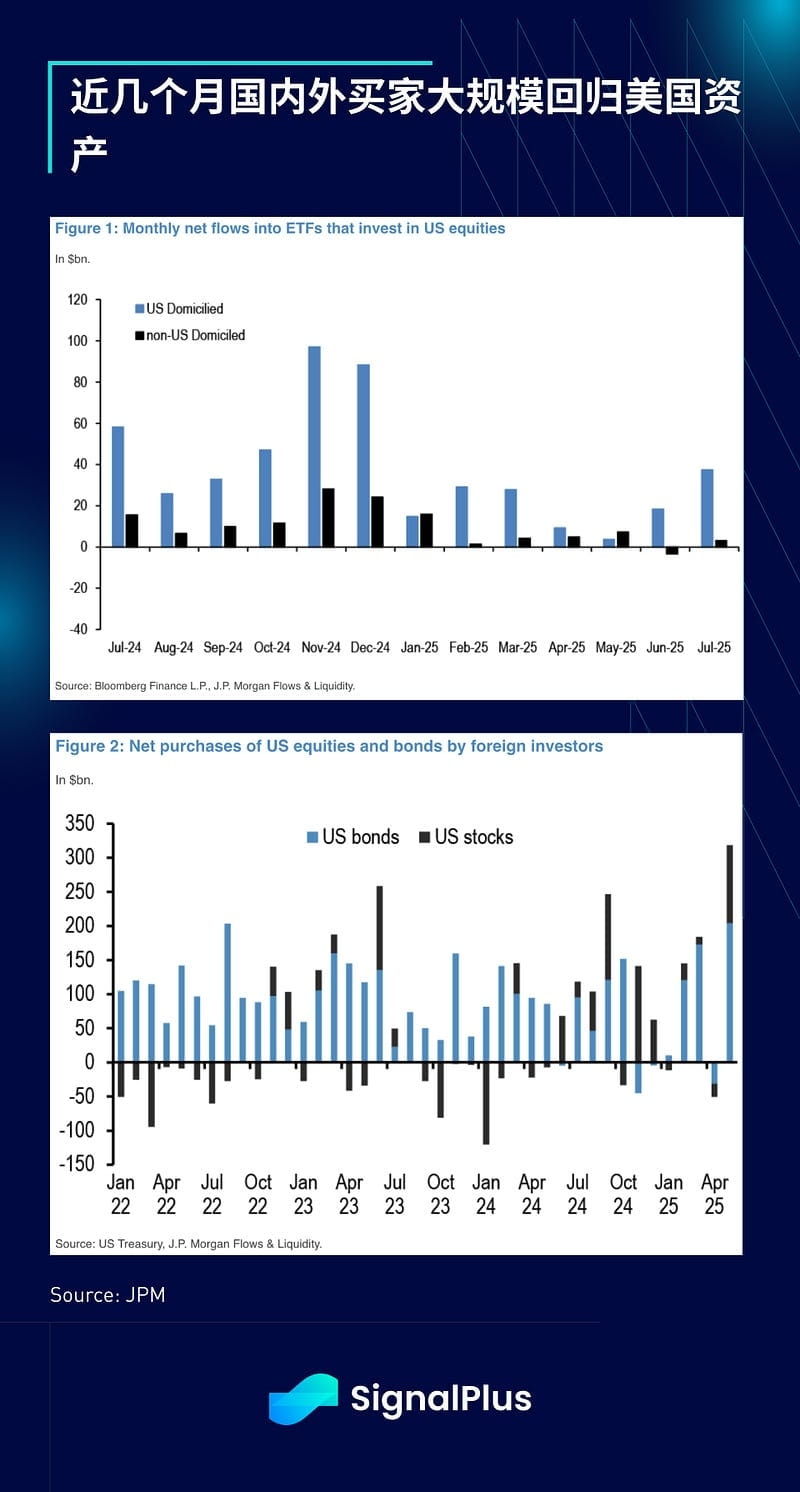

Capital flows to the United States remain strong, with domestic and foreign investors returning en masse. The latest data shows a new monthly record for net purchases and a new high for trading volume, providing positive evidence.

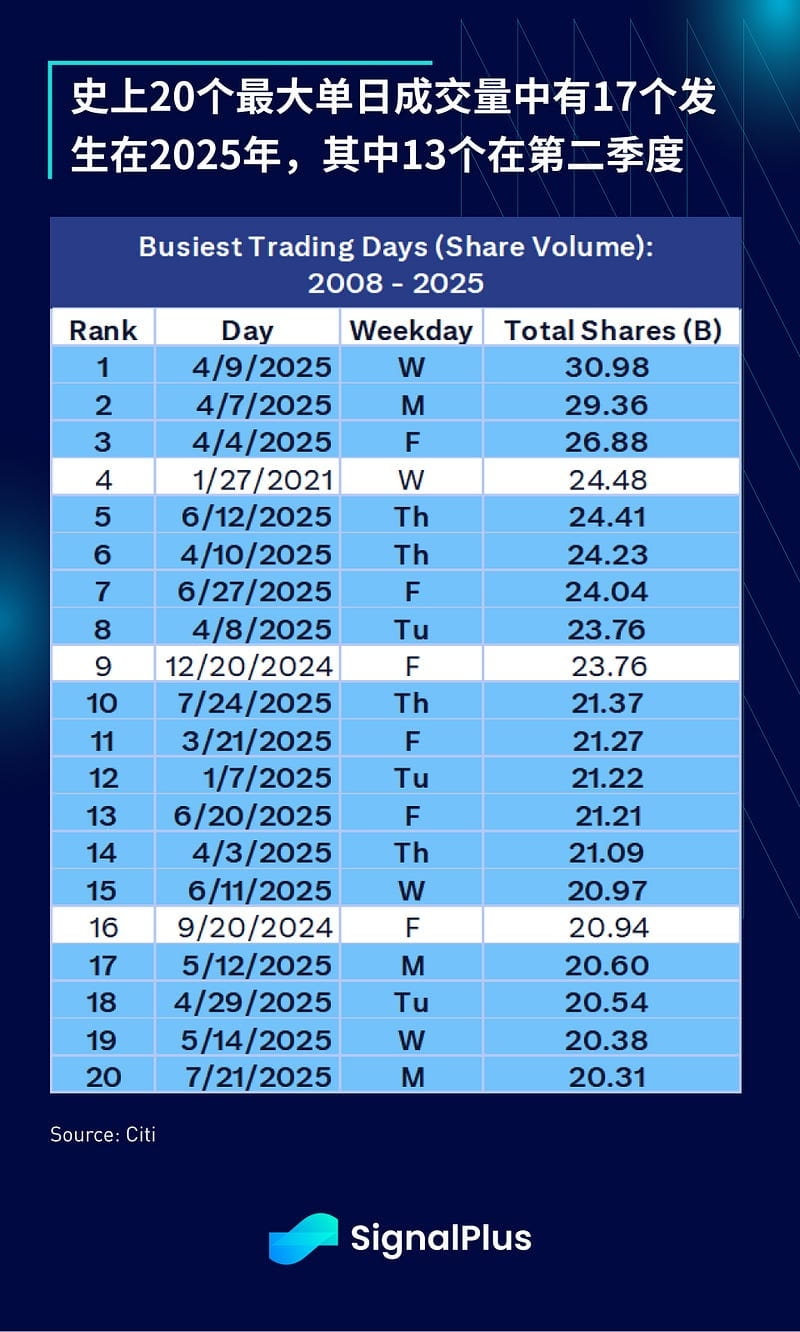

US stock market trading volume reached a record high in 2025, far exceeding previous years, primarily driven by a strong return of retail trading since the beginning of the year. According to Citi, average daily trading volume in the first half of 2025 was nearly 50% higher than the average of the previous five years and a significant 40% jump from the previous record set in 2024. This trend continued in July, with average daily trading volume reaching 18 billion shares.

In fact, 2025 was so phenomenal that 17 of the 20 largest single-day volume days in history occurred in 2025, including 13 in the second quarter alone. Absolutely incredible.

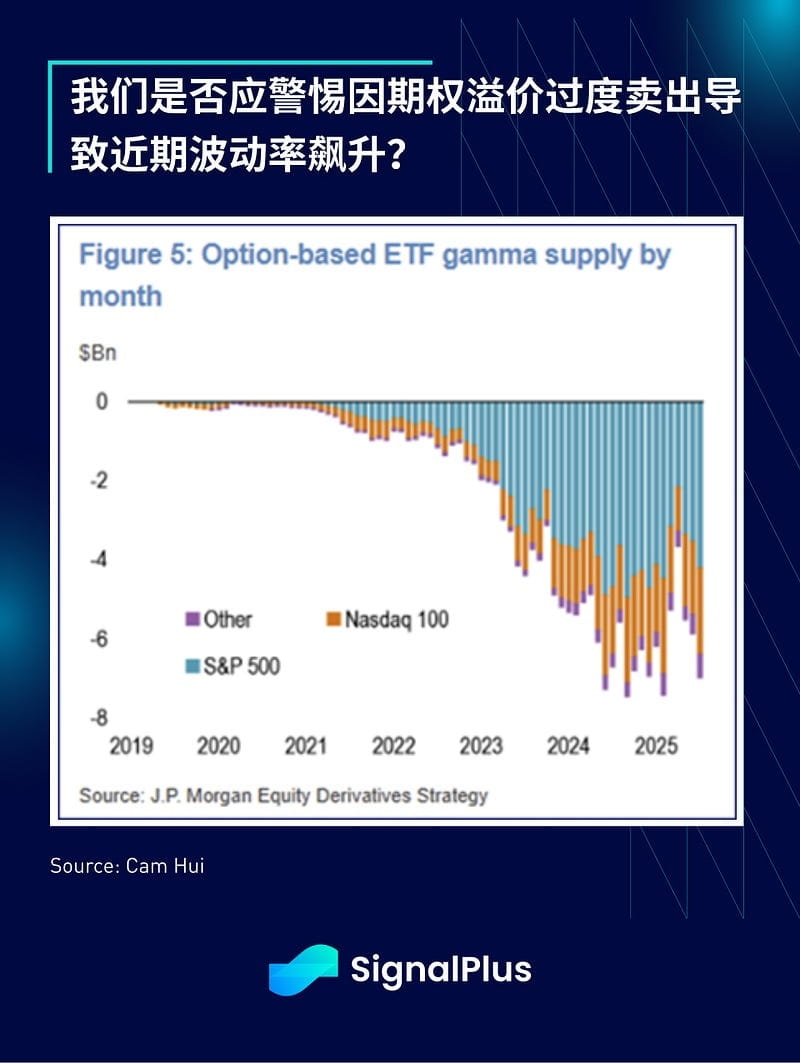

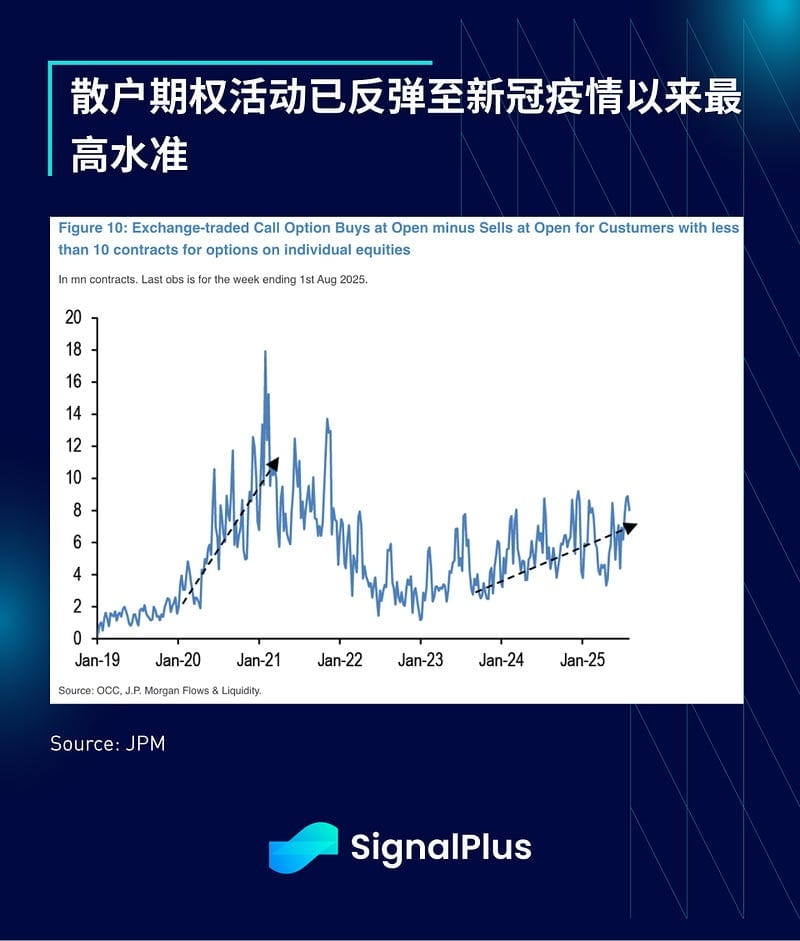

Retail participation has driven extremely high concentration of individual stocks year-to-date, with the top five stocks accounting for over 20% of total market volume on some trading days in 2025. Retail activity in call options has also rebounded sharply, reaching its highest level since the COVID-19 pandemic.

Regarding earnings, approximately 80% of the S&P 500 companies that have reported have exceeded expectations, with year-over-year growth of 12% and a 9% margin of victory, led by the technology and financial sectors. Second-quarter 2025 earnings per share significantly exceeded expectations, despite downward revisions to expectations following tariff concerns.

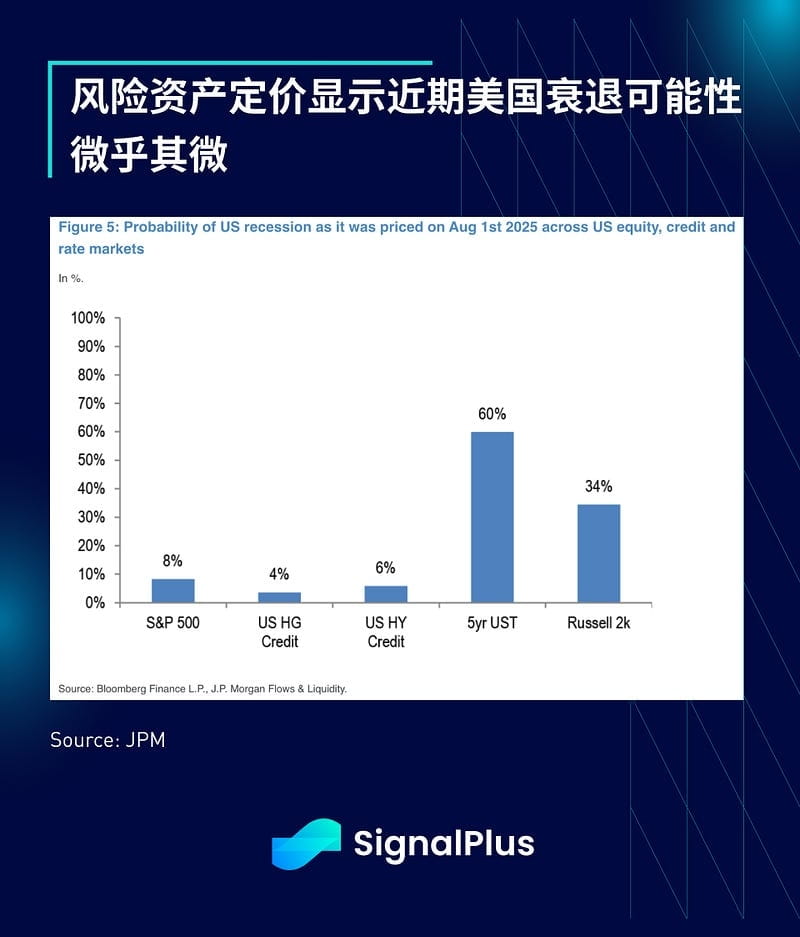

The current rally has pushed recession probabilities back into the low single digits for both equity and credit markets. The exception is (as usual) US fixed income markets, which remain the most aggressive in pricing in further Fed easing.

On the inflation front, while the Federal Reserve has indicated it is happy to overlook recent price pressures, the Institute for Supply Management (ISM) data showed a worrying rebound in prices paid, which typically leads the CPI by about a quarter and could pose a problem for the Fed's interest rate cut plans later this year. However, for now, driven by risk appetite, the market is happy to remain elevated until hard data confirms a change in the situation.

Cryptocurrencies experienced a similar rally this week, driven primarily by headlines that Trump ordered regulators to "study" the possibility of including cryptocurrencies (and private equity) in 401(k) portfolios. If such a move were to materialize, it would clearly unleash significant buying demand. However, it remains a long way from becoming law.

Even more exciting, Ethereum led the week's gains, posting a +20% weekly gain. The latest mainstream pundits/heroes have touted ETH as the latest FOMO (Fear of Missing Out) asset in the public equity space. Retail traders responded enthusiastically, driving BNMR up nearly 60% this week, demonstrating to "native gamblers" how to properly FOMO in the regulated world.

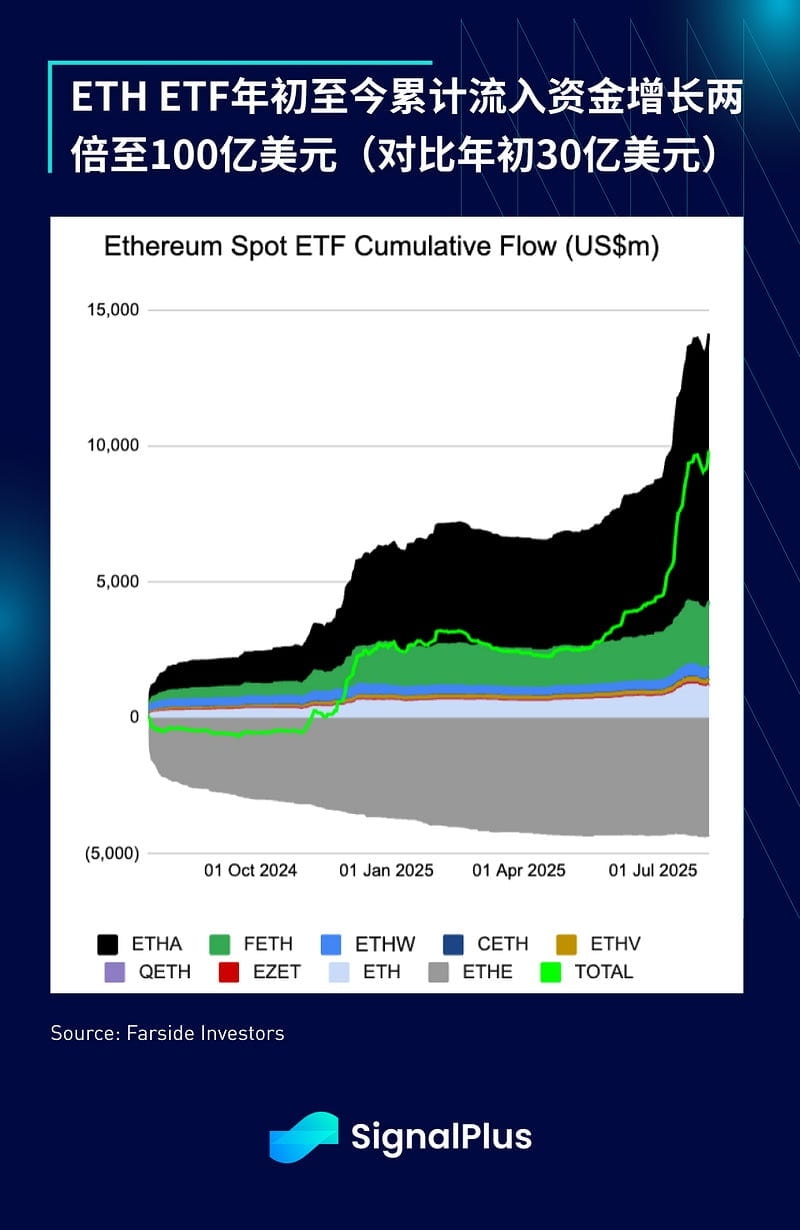

As expected, the Ethereum ETF saw an additional inflow of approximately $700 million in the last two days of the week, pushing cumulative inflows to a new record high. The cumulative assets under management have tripled to nearly $10 billion since the beginning of the year (vs $3 billion at the beginning of the year).

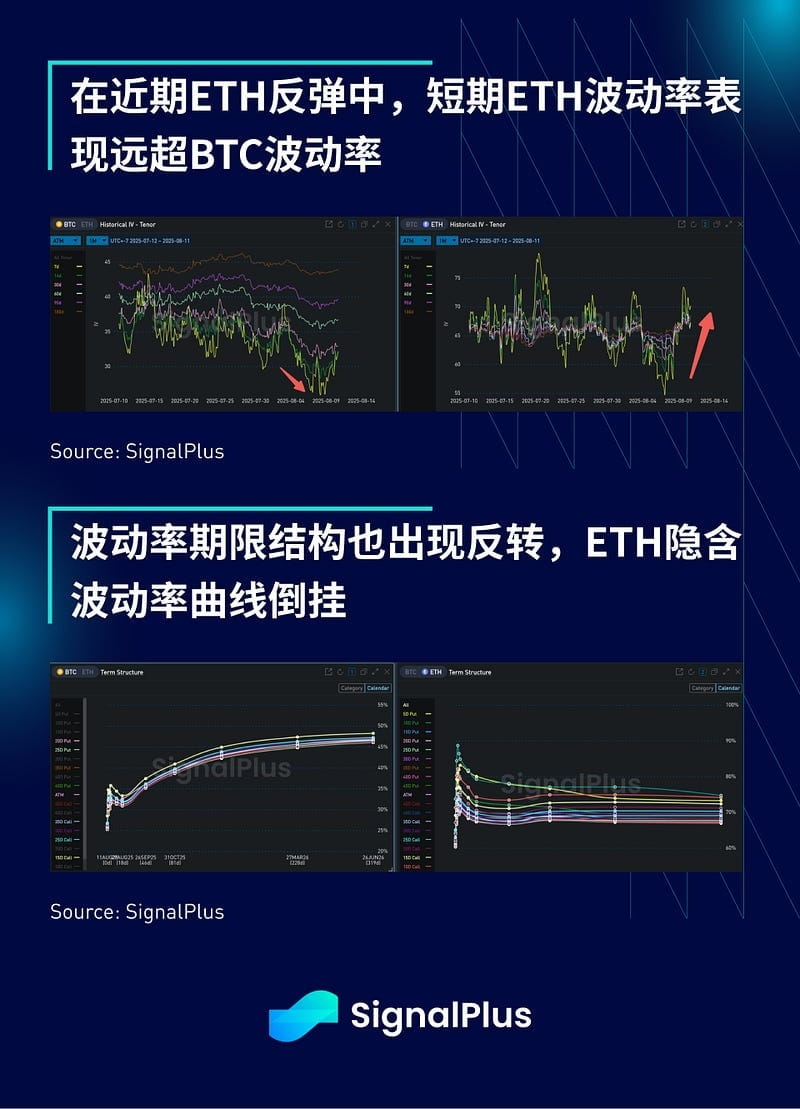

ETH's recent rebound has also led to a divergence in short-term volatility. While Bitcoin's implied volatility remains near historical lows, ETH's volatility has surged significantly. ETH's term structure is also currently inverted, with long-term volatility expected to fall back to the ~70% range. Meanwhile, BTC's IV curve shows the opposite trend, with short-term volatility severely compressed, with the spot market hovering around $120,000.

For comparison, a month ago, market pricing only implied a 5% probability that ETH would hit $4,500 in August, but the actual trend of the spot market far exceeded the implied path, catching many participants off guard.

Looking ahead, we don't see a compelling reason to chase the market higher at this point, as we anticipate a period of two-way volatility in market assets over the next month or so. Be wary of potential downside catalysts such as a sharp reversal in the US dollar index or an unexpected rise in inflation. Traders, please remain vigilant and wish you the best of luck!