Author:

Jessica Feng, Investment Manager of Hash Global BNB Fund;

James (KK) Shen, Founder of Hash Global.

CZ (Founder of Binance):

“I am not proficient in valuation models, but Hash Global's previous estimates have all been realized. The composition of token value should have many facets. If such a simple formula can capture all manifestations of value, that would be impressive. Market prices often deviate from fundamentals, sometimes too high and sometimes too low. Binance will continue to build and establish the fundamentals of BNB's value, while experts like Hash Global can assess the market price.”

Liang Xinjun (Co-founder of Fosun Group):

“I have been cooperating with the Hash Global team for many years. One thing I appreciate about the team is: although they may make mistakes in their investments, their decisions are always based on rational analysis and judgment, rather than blind faith. They communicated with me early about the value of the Binance ecosystem and BNB, and I participated in their node staking and BNB fund investment early on, with good returns. I have seen many institutional analysis reports on Bitcoin and Ethereum; in terms of BNB, I believe Hash Global's analysis is the earliest and best in the industry.”

Chen Long (Secretary-General of Luohan Hall, Founder of Wei Xi, former Chief Strategy Officer of Ant Financial):

“Although Web3 is increasingly becoming a new pillar of the financial system, there is a lack of consensus on how to value digital assets. Hash Global proposes a very valuable perspective based on a monetary equation analysis framework.

If the growth rate of a country's money supply synchronizes with economic growth, it will not lead to inflation, which is well-known as seigniorage. This means that economic transaction activities need the lubrication of monetary functions. With a stable velocity of money turnover, the overall value of money will synchronize with the volume of economic transactions.

Based on this reasoning, the analysis framework of the monetary equation can estimate the total value of ecological tokens around transaction volume. This method is based on many assumptions, but its logic is fundamentally sound, representing a clear advancement over most digital asset valuation logics, and is worthy of continued exploration and improvement. Returning to the first principles of value creation is a good starting point.

Wang Jingbo (Founder of Noah Wealth):

“As the largest wealth management platform serving global Chinese communities, Noah has always focused on the emergence and value of new assets. The U.S. and Hong Kong, among others, are vigorously promoting the improvement of the regulatory framework for digital assets, and we observe that digital assets are being accepted by mainstream markets. We place great importance on guiding and helping investors to learn and understand the value of digital assets at the first time. In the past two years, we have repeatedly invited the Hash Global team to share with our investors. Their research and analysis on 'value functional tokens' have brought us many refreshing perspectives and insights. Their attitudes and methods are worth everyone's attention and reference.”

Wei Zhijie (KGI International Wealth Management Director):

“I have worked in the wealth management industry for many years, helping various family offices with intergenerational inheritance and asset allocation. KGI has noticed the optimization effect on the risk-return ratio brought by digital assets to portfolio allocation, guiding clients to rationally recognize and accelerate the allocation of digital assets. We are particularly focused on functional tokens with clear economic models and real application scenarios. The innovative research work that Hash Global has done in this new asset field has inspired us greatly. We are discussing the value of such assets with them to promote traditional financial investors' understanding of their value.”

I. Introduction

In recent years, the rapid development of Web3 financial infrastructure has been reshaping the operating rules of capital markets. Its programmability and openness are also reconstructing the sources of asset value, promoting the emergence of a new class of asset forms. These new assets not only carry traditional equity value, as a value mapping of platforms, protocols, or ecosystems; they also possess clear utility value, which can be used to pay fees, obtain service discounts, unlock access rights, etc. This report collectively refers to such new assets as 'value functional tokens', representing composite asset carriers that embody both 'asset attributes' and 'utility rights'.

The emergence of new asset types is driving the evolution of the concept of 'value' itself, and the valuation methodology of value investors must also evolve accordingly, just as the internet revolution in the early 21st century brought about a new logic for valuing internet stocks. Early advocates of value investment in crypto assets, such as John Pfeffer, proposed: 'The first principle of value investing is independent thinking based on reliable valuation logic. When new asset types first emerge, there is no corresponding valuation logic; value investors should strive to discover new valuation logic.'

We believe that the most representative value functional token currently is the platform token of the world's largest cryptocurrency exchange, Binance Coin (BNB). BNB not only maps platform value but also possesses actual utility value within the ecosystem, making it the earliest and most mature example of such assets. Binance completed the economic design of BNB as early as 2017, taking the lead in defining the asset category of value functional tokens. In 2019, we adhered to the first principles of value investing, using BNB as a template to propose a valuation framework based on the monetary equation (MV = PQ) to evaluate the value generation logic of BNB and value functional tokens.

In the past six years, we have released five reports, receiving numerous inquiries and feedback from investors and institutions. We continuously optimize our model, which has also received preliminary validation from the market. We now整理 this method as follows, hoping to assist asset management institutions, investors, industry researchers, and project parties in their analyses and decisions regarding investment assessments, asset pricing, and token economic design for value functional tokens.

Web3 distributed ledger technology has already and will permanently change the fundamentals of capital markets. A more efficient and transparent Web3 financial system will undoubtedly become the core of future financial infrastructure. As the global regulatory system for crypto assets continues to improve, for example, the U.S. recently passed the (Digital Asset Market Structure Clarity Act) (“CLARITY Act”), and the U.S. and Hong Kong have successively introduced stablecoin legislation, we believe that we will see a large number of value functional tokens represented by BNB emerge in the future, just like Tesla issuing new 'stocks', which will be value functional tokens issued on Ethereum or Binance Chain, having not only 'equity value' but also allowing for discounts when using ecological tokens at charging stations. We expect value functional tokens to become the main asset carrier form in future capital markets!

II. Definition and Characteristics of Value Functional Tokens

The value functional tokens defined in this report refer to crypto assets that simultaneously possess the following two types of value foundations:

1. Asset Attributes/Quasi-Equity Attributes: Representing the value mapping of a platform, protocol, or ecosystem. Its value is usually driven by macro factors such as ecosystem size, user growth, and trading activity.

2. Functional Attributes/Quasi-Monetary Attributes: Play practical roles in specific usage scenarios, such as paying fees, Gas fees, staking, participating in governance, exchanging for services, or enjoying platform discounts.

For this type of asset, the report chooses to build a valuation model based on the monetary equation (MV = PQ), mainly for the following two considerations:

Firstly, although value functional tokens possess certain 'quasi-equity' characteristics, their asset attributes still differ from traditional securities. Taking BNB as an example, this token does not represent any form of equity or cash flow rights in Binance. From the perspective of ecological development, the founding team of Binance has bound the interests of all ecological participants (shareholders, management, users, and other ecological stakeholders) together since the project's inception, placing the growth of ecological value on the unique ecological token BNB, embodying the spirit of co-building and sharing that Web3 advocates. Since 2021, Binance has further adjusted BNB's burn mechanism from 'profit-linked buyback and burn' to 'automatic burn based on on-chain transaction volume', actively severing the direct link between token value and platform financial performance to avoid securities risks.

In 2025, the CLARITY Act issued in the U.S. will further clarify the distinction between 'digital commodities' and 'security tokens'. Under this regulatory direction, we believe that future value functional tokens will be designed to move towards 'digital commodities', although they may have value support from traditional equity, they will be designed to avoid the standards of 'investment contracts' and Howey tests for security tokens. Therefore, such tokens do not possess the legal characteristics of traditional equity assets; in terms of valuation methodology, they cannot be directly assessed using enterprise valuation models based on cash flow discounting.

On the other hand, the value of functional tokens primarily comes from their actual usage scenarios within the ecosystem. They serve functions such as payment, Gas, staking, participating in governance, etc., essentially functioning similarly to circulating currency within an economy. Their value is influenced by various factors such as the scale of ecological economic activity, token usage frequency, and supply adjustment mechanisms. Therefore, compared to securities valuation methods, the monetary equation is more suitable for capturing the 'quasi-monetary' attributes of such tokens and modeling multiple sources of value within a unified logical system.

In summary, the core advantage of using the monetary equation to value value functional tokens lies in: this model provides a clear structure, quantifiable variables, and strong adaptability, enabling it to comprehensively cover all sources of value for such tokens.

III. Building Valuation Models

This methodology constructs a systematic valuation model suitable for value functional tokens by combining the monetary equation (MV = PQ) with the Discounted Cash Flow method (DCF):

MV = PQ: A structural logical framework for building token value generation

+

DCF: Discounting the future 'monetary appreciation' brought by ecological expansion and converting it into the current theoretical price of the token

3.1 Introduction to the Monetary Equation (MV = PQ)

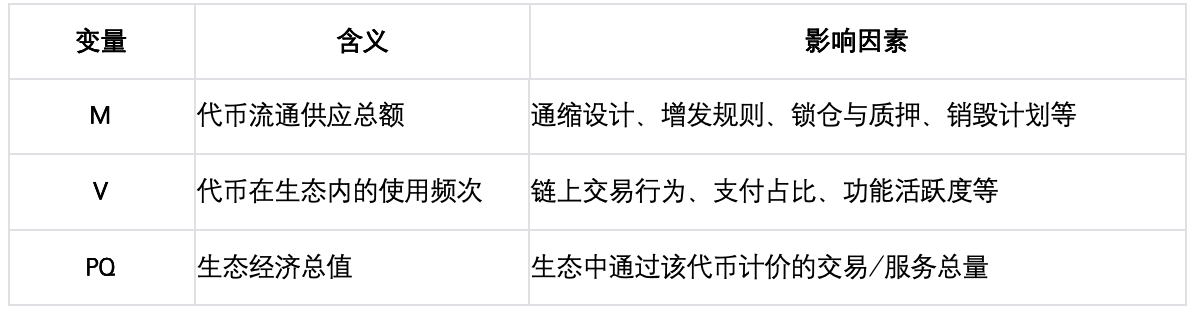

The quantity theory of money, proposed by economist Irving Fisher, is a classic theory explaining the relationship between the total amount of money and economic activity. Among them:

· M: Money Supply

· V: Velocity of Money

· P: Price Level

· Q: Total Transaction Volume or Output Value

In traditional macroeconomics, MV represents total money demand, and PQ represents nominal economic output. Both should remain consistent in a long-term equilibrium state.

We believe that for functional tokens with actual usage scenarios in the on-chain ecosystem, their economic role is highly similar to 'currency within the ecosystem'. Their value mainly comes from the expansion of ecological scale and changes in the token supply-demand structure, which aligns closely with the logic of the monetary equation. This model is particularly suitable for tokens with the following characteristics:

1. As the primary medium of payment within the ecosystem (e.g., fees, Gas, etc.);

2. Possess a transparent issuance system, deflationary design, or locking mechanism that affects the effective circulating supply;

3. Its value mainly comes from the development of ecological activities.

3.2 Structural Modeling Based on the Monetary Equation

Under the framework of MV = PQ, the theoretical value of tokens is driven by two main paths:

· PQ: Total Economic Value of the Ecosystem

· M × V: Represents token supply and its turnover rate

Any variables affecting token value (such as user numbers, transaction volume, burn mechanisms, etc.) ultimately affect token price through their impact on PQ or M × V.

Among them, V (turnover rate) is a technical difficulty in modeling. Due to the lack of directly observable data, in actual valuation, it is usually assumed that the market price in the early stage has reflected a reasonable equilibrium state, and then V is inferred using known PQ and M, assuming that this turnover rate remains stable or moderately increases or decreases in the future.

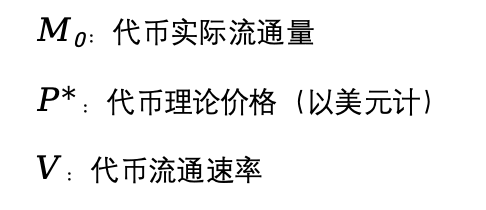

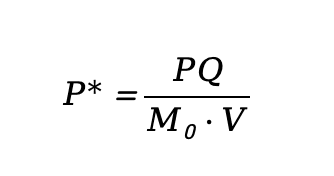

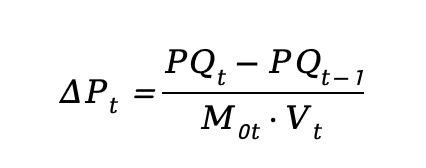

Theoretical Price Derivation:

Unlike general national fiat currencies, the price of ecological tokens is usually denominated in U.S. dollars. Therefore, in the model, the total circulating supply of the token (M) can be broken down into:

Where:

整理得:

The total economic value of the ecosystem (PQ) divided by the circulating token supply and turnover rate gives the theoretical price of the token. This formula serves as the valuation basis of this model.

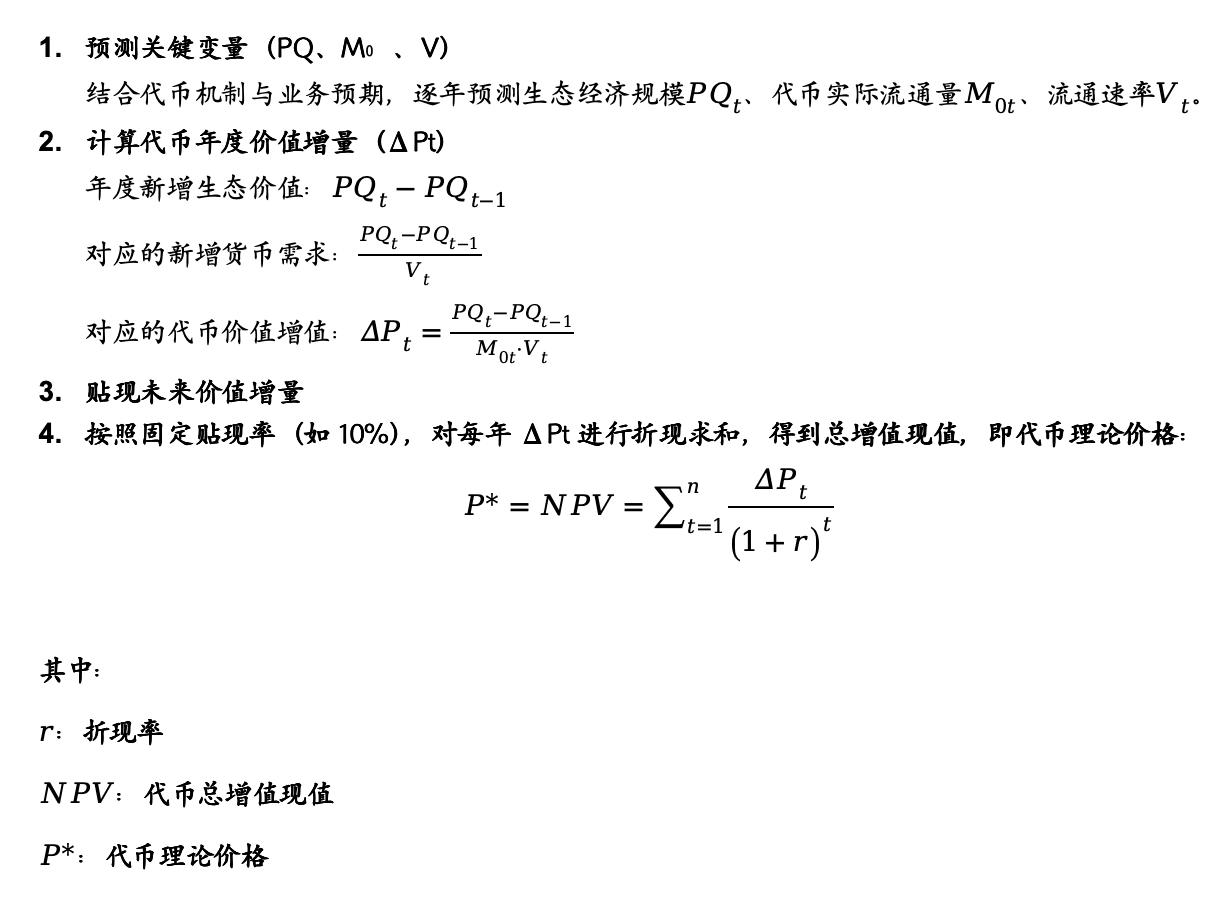

3.3 Introduce Discounted Cash Flow (DCF) for Quantitative Valuation

The monetary equation provides a logical framework for the token value generation mechanism but does not directly output price. On this basis, we further introduce the Discounted Cash Flow (DCF) method. By predicting the growth of the total ecological economy and combining changes in token supply and turnover rates, we estimate the annual increment of unit token value and discount and sum the future value to obtain theoretical valuation. This process can also be understood as calculating the present value of 'monetary appreciation'.

The specific steps are as follows:

IV. Valuation Case: Taking BNB as an Example

To demonstrate the applicability of this valuation method in practice, we take BNB as an example and apply our proposed 'MV = PQ plus DCF' model for quantitative valuation analysis.

4.1 BNB as a Value Functional Token, the Monetary Equation is the Best Valuation Model

BNB is the core value carrier of the Binance ecosystem (Binance exchange + BNB Chain), with two sources of value:

1. Asset Attributes/Quasi-Equity Attributes: BNB's economic model integrates the value creation logic of traditional finance. Just as U.S. stocks enhance shareholder equity through stock buybacks, BNB continuously reduces circulating supply through a quarterly burn mechanism, creating a long-term deflationary trend on the supply side to provide stable support for the token price. However, unlike traditional equity, BNB's burn mechanism is not tied to platform profitability but is anchored to its supply-demand relationship within the ecosystem. Therefore, BNB is not strictly a form of equity asset but possesses a quasi-equity attribute—building a value mapping relationship between BNB and the Binance ecosystem by reducing the actual circulating amount of BNB through burns.

2. Functional Attributes/Quasi-Monetary Attributes: BNB has multiple uses within the Binance exchange and public chain ecosystem, including paying fees within the exchange, participating in new projects, serving as Gas Fee, participating in governance, etc. BNB has essentially become the 'circulating currency' of the entire ecosystem, with its value depending on changes in the scale of the ecological economy and the supply-demand relationship of the token within the ecosystem.

In summary, as an ecological circulating currency, the value of BNB mainly depends on the supply-demand relationship (MV) and the economic value of the ecosystem (PQ). Therefore, the monetary equation can comprehensively capture the core value drivers of BNB, making it the best valuation model.

4.2 Valuation Calculation of BNB

The analysis will unfold around the following three core steps:

1. Define and predict key variables PQ, M₀, V

2. Calculate the annual value increment ΔPt

3. Use the Discounted Cash Flow method to discount and sum future incremental values

1. Define and predict key variables: PQ, M₀, V

Total Economic Value of the Ecosystem PQ

The Binance ecosystem mainly includes the Binance exchange and the Binance Chain (BNB Chain). Therefore, PQ is the total economic activity value driven by BNB in these two parts, mainly including:

1. In the trading fee income of Binance centralized exchange (CEX) for spot and derivatives trading, the portion paid in BNB (trading volume × fee rate × proportion paid in BNB (assumed 50%));

2. BNB Chain Gas fees (total Gas income on-chain).

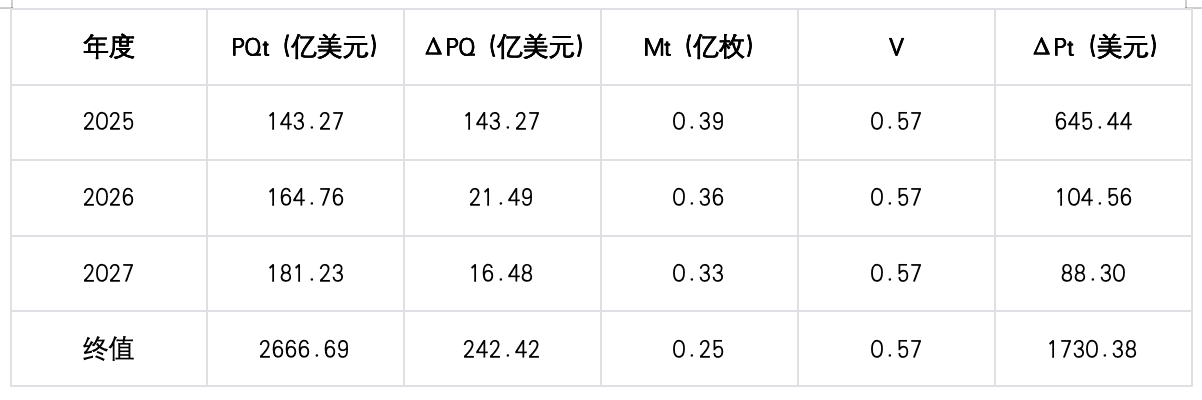

In the calculations, we assume the annual growth rate of the ecological economy to be the following values, summarizing to obtain the future annual nominal economic value PQt.

· 2025–2027: 25%, 15%, 10% respectively;

· 2028 and beyond: Long-term stable growth rate of 3%.

Total Circulating Token Supply M₀

According to the Binance white paper and on-chain data, the initial total supply of BNB was 200 million tokens. After deducting team locked holdings (approximately 80 million tokens) and historical cumulative burn amounts (approximately 11.65 million tokens), the current theoretical circulating supply is about 108 million tokens. Combining Binance's current burn mechanism and future burn predictions, it is expected that the circulating supply will remain at this level between 2025 and 2027 and gradually transition to a stable 100 million tokens in the long term. This is the maximum supply available for trading in the secondary market without ecological usage.

On this basis, further eliminate the four major ecological locking scenarios (fee payment, node staking, financial products, long-term value holding) to obtain the actual circulating supply M₀t.

Turnover Rate V

The turnover rate of BNB is difficult to directly measure. We employ a reverse deduction method: through the actual market price in 2024, PQ, and M₀, we deduce the benchmark value of V to be 0.57. For future years, a ±10% range can be set, and its impact on valuation will be verified in subsequent sensitivity analyses.

2. Calculate Annual Value Increment ΔPt

According to the formula from the previous section:

We calculate the incremental value added to the ecosystem year by year and divide it by the actual circulating scale and turnover rate of BNB for that year to obtain the theoretical value increment of each unit token annually.

Based on actual data from 2024, assuming growth rates of 25%, 15%, 10% for the next three years, and a long-term rate of 3%:

3. Value Discount Summation: Calculate Theoretical Valuation

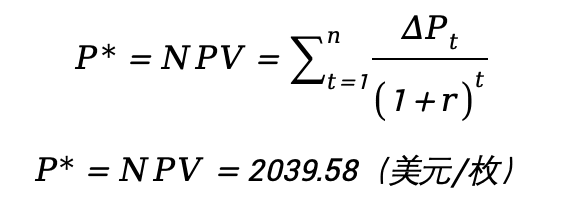

Using a 10% discount rate, discount each year's value increment ΔPt to obtain the total present value of all future 'monetary appreciation':

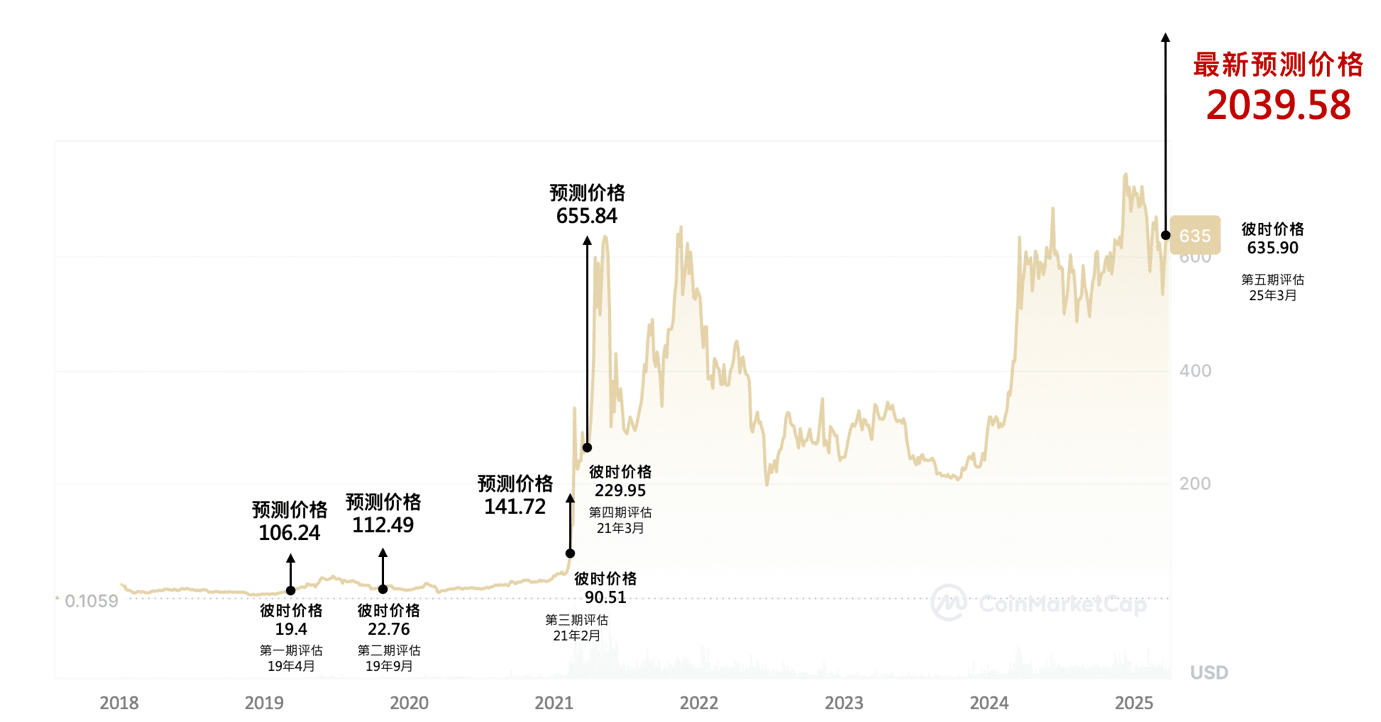

4.3 Hash Global Past Four Period Reports - BNB Target Price Achievement Timeline

V. Conclusion

This report takes BNB as a case study, proposing the concept of 'value functional tokens' as an asset category and building a systematic valuation framework based on the monetary equation. We hope this framework can provide reference and inspiration for project parties' token economic design, investors' value judgments, and researchers' model assessments.

As the Web3 industry is still in a stage of rapid evolution, we will continue to update the model and research results. We welcome investment institutions, researchers, and developers to discuss and provide feedback on the report's content.

For report updates, model details, or further discussions, please visit our official website or contact team members. We look forward to your feedback and suggestions:

• Official Website: www.hashglobal.io

• Author Twitter: @longwinsk, @Jf4172

• Contact Email: [email protected]

Disclaimer

This report aims to share information and does not constitute any investment advice, nor should it be seen as a guarantee of future market performance. This report is based on Hash Global's independent research and publicly available information, and we have made every effort to ensure the accuracy and completeness of the data and analysis. However, we make no commitments or guarantees regarding the applicability of the final results or opinions. Investing in crypto assets carries high uncertainty and volatility. Readers should fully understand the relevant risks and assume all responsibilities before making any investment decisions. Hash Global and its related parties are not responsible for any direct or indirect losses caused by the use of this report's content.

As of the date of this report's release, Hash Global and the funds it manages hold some BNB assets, and relevant analyses and opinions may be influenced by these holdings. We will continue to monitor the relevant assets according to market dynamics and update research content as necessary.