Huma Finance is an income-based lending protocol that enables businesses and individuals to connect with global investors. Huma provides popular credit tools such as revolving credit lines and accounts receivable factoring.

The project also introduces a decentralized signal processor and Rating Agent—essential infrastructure for integrating income sources, credit assessment, and continuous risk management.

The latest upgrade aims to better support institutional investors. New integrations include:

Structured finance: There are payment rounds, insurance, 30/360 schedules, and daily yield calculations.

Tokenization: Enables the tokenization of real assets through SPV structures.

Transparency: Displays the lifecycle of receivables on-chain, making it easier for investors to track performance.

Since launch, Huma Finance has provided loans worth $1.19 billion, of which $1.17 billion has been repaid, maintaining a default rate of 0%.

The development team has extensive experience in finance. Founders include Erbil Karaman, Richard Liu, Ji P, and Lei Du.

Erbil Karaman and Richard Liu were both Chief Product Officers (CPO) at Earnin, a financial startup. Ji P also worked at Earnin as Head of Machine Learning. Lei Du was involved in data research at News Break and Opendoor.

HUMA token information

Token name: Huma

Symbol: HUMA

Total supply: 10,000,000,000

Initial circulating supply: 17.33%

Allocation

Airdrop: 5%

Liquidity providers (LP) and ecosystem incentives: 31%

CEX Listing and Marketing: 7%

Market Makers & On-chain Liquidity: 4%

Pre-sale: 2%

Investors: 20.6%

Team & Advisors: 19.3%

Protocol treasury: 11.1%

Token utility

Governance: HUMA holders can stake their tokens to participate in the protocol governance process. The longer the staking period, the greater the voting power, encouraging long-term commitment to the protocol.

LP rewards & ecosystem: HUMA plays a crucial role in the incentive program, driving adoption and growth throughout the ecosystem.

Value accumulation mechanism: The Huma Fund is actively exploring sustainable ways to use revenue from the protocol, with transparent designs led by the community to adjust incentives and reward active participants.

Ecosystem currency: HUMA serves as a utility token for advanced protocol features. These functions will continue to evolve as the protocol grows.

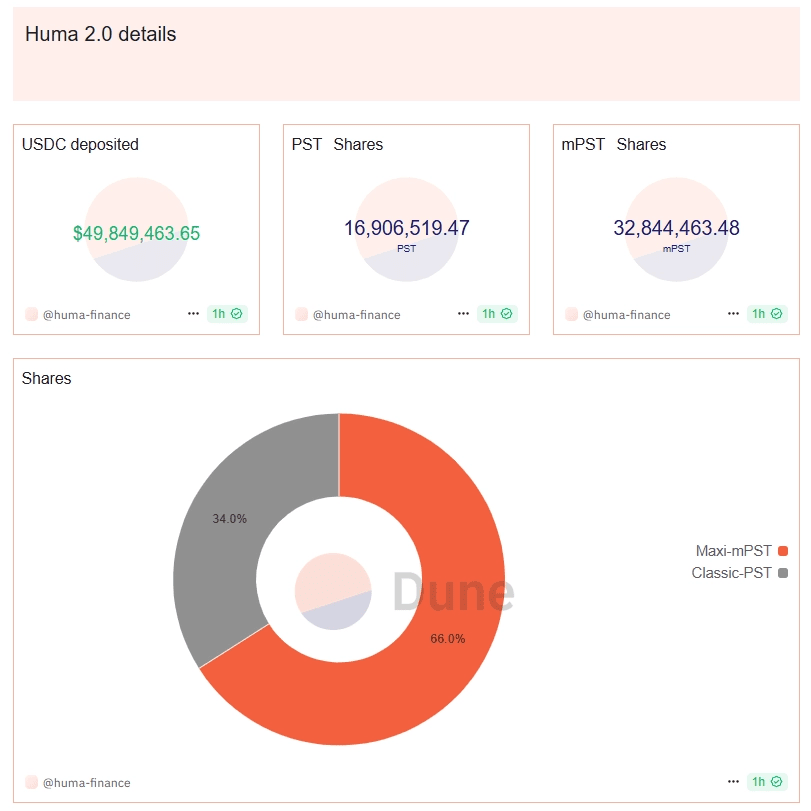

Huma 2.0 launched with groundbreaking features

Huma 2.0 has officially launched, catering to all users with significant upgrades. The new version offers two yield options:

Classic mode offers actual returns of up to double digits with an APY of 10.5% (updated monthly) along with Huma Feathers.

The Maxi mode allows users to skip APY to maximize Feather accumulation with a multiplier of up to 17.5 times (limited-time promotion).

Huma Feathers, also known as Huma Points. Users can increase rewards by locking deposits for 3 or 6 months. Liquidity providers (LP) can freely switch between these two modes at any time without incurring fees.

High liquidity LP token PST deeply integrated into the Solana DeFi ecosystem:

Instantly exchange PST for USDC via Jupiter

Use PST in Kamino's liquidity pool to swap or borrow USDC (lending and looping feature not yet launched)

Share PST on RateX to participate in leveraged YT/PT strategies

Additionally, the referral system allows users to earn 10% of the Feathers generated by their referrals over the entire year.

What makes Huma Finance different

Instant liquidity: Users can access funds immediately through seamless liquidity solutions developed by the project.

Security: Huma Finance applies the highest risk management principles with a financial structure enforced by transparent smart contracts.

Compliance: The project is supported by licensed partners, comprehensive AML screening, and investor vetting.

Flexibility: Huma Finance is an open architecture with advantages in cross-layer interoperability and modular design to create customized financial solutions tailored to individual needs.

Key components of Huma Finance

Lenders

Lenders provide liquidity on Huma and earn a share of the fund's profits. Huma V2 protocol supports two types of segments for lenders: premium segment and low-tier segment. A fund can have both segments active or just the low-tier segment.

If both rounds are active, separate approval is required to participate. One group of lenders will automatically receive yield payments at the end of each period, while the other group reinvests the entire yield back into the fund. Each round can have a maximum of 100 qualified lenders eligible for automatic yield payments. The Fund Owner and Operator will decide whether the lender qualifies for automatic payment or reinvestment.

Borrowers

Borrowers are participants seeking funding from the Huma protocol. They must pay interest on time and, depending on the terms of the group, must repay a minimum principal in each payment period.

Pool Administrator

Pool administrators include Pool Owners, Pool Operators, and Rating Agents. They perform administrative tasks to ensure the pool operates efficiently. Pool administrators are rigorously vetted to protect users, and participants must complete KYC and undergo a thorough screening process to qualify.

Typically, Pool Admins are institutional financial partners like Jia, Rain, and Arf.

Core products of Huma Finance

Revolving credit line

Borrowers are approved for a fixed credit limit, allowing them to borrow, repay, and re-borrow. This product provides flexibility as long as users stay within the credit limit and make timely payments.

Credit limits secured by receivables

With this type of credit limit, borrowers must present receivables (e.g., unpaid customer invoices) for each loan. They can borrow a portion of the value of receivables to meet working capital needs, although some characteristics are restricted.

Receivables factoring

In the receivables factoring business, businesses sell receivables (unpaid invoices) to a third party (the factor) at a discount. The factor is responsible for collecting payment from customers, profiting from the spread. Through Huma Finance, borrowers can factor receivables by receiving an upfront advance based on a percentage of the invoice value.

Huma makes a mark with an impressive array of achievements

Huma had a tremendously successful 2024 with several key milestones:

Launched the first PayFi network, raising $38 million and introducing the Open PayFi Stack to accelerate global payments.

Messari's 2025 thesis identifies PayFi as an important growth area to watch.

Co-hosted the first PayFi Summit with Solana Foundation, collaborating with Circle, VISA, PayPal, and many other major entities.

Announced plans to hold five more conferences throughout 2025.

By 2025, Huma will lead the PayFi wave with:

Online transaction volume reached $4.5 billion, with annual revenue of $9.97 million.

The number of wallets surged to 55,382, increasing tenfold after the launch of Huma 2.0.

Attracted large institutional LP partners and collaborated with Jupiter to successfully conduct a token sale before TGE and swap JupDao tokens.

Ranked #1 in Mindshare across all languages on Kaito Pre-TGE Arena, topping the leaderboard in English, Chinese, and many other languages.

♡𝐥𝐢𝐤𝐞💬 ➤ @Huma Finance 🟣 #HumaFinance $HUMA