Source: Bitcoin Versus The IMF

Organized & Compiled by: LenaXin, ChainCatcher

Original Link: https://www.chaincatcher.com/article/2191241

Disclaimer: This article is a reprint, and readers can obtain more information through the original link. If the author has any objections to the reprint format, please contact us, and we will modify it according to the author's request. Reprints are for information sharing only and do not constitute any investment advice, nor do they represent the views and positions of Wu Shuo.

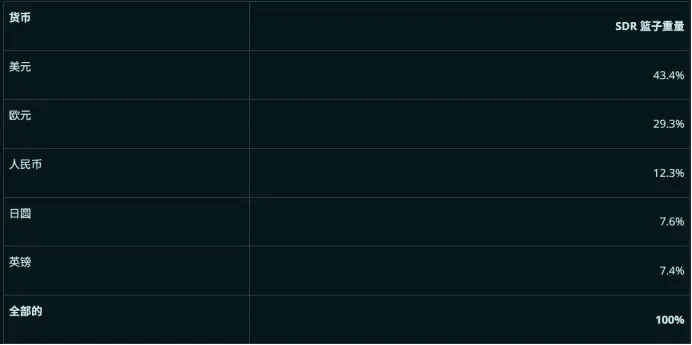

Note: The "Policies under the mid-term loan arrangement" section of the El Salvador country report published by the International Monetary Fund in March 2025, which is 111 pages long, is being generated using a word cloud generator. Years before Bitcoin's inception, in 2004, author John Perkins published the influential book (Confessions of an Economic Hit Man). This semi-autobiographical work chronicles Perkins' career as an "economic hit man"—he traveled to emerging market countries, persuading local governments to accept loans from the International Monetary Fund (IMF) and the World Bank. These loans often came with harsh conditions and were secured through highly controversial means. Perkins vividly described these economic agents as "jackals." For readers hoping to understand the economic libertarian background of Bitcoin's creation and its potential mission, this book is a must-read classic. Perkins' revealing narrative provides early Bitcoin supporters with a crucial perspective on understanding the value of this emerging monetary system. Like many members of the Bitcoin community, we are cautious about the IMF based on our understanding from such books. Overall, Bitcoin supporters not only question the central banking system, but also remain wary of transnational financial institutions such as the IMF, the World Bank, and the Bank for International Settlements. Correspondingly, it is not difficult to understand the resistance to Bitcoin from those within the IMF system. IMF's narrative control In May 2011, years after Bitcoin's emergence, then-IMF Managing Director Dominique Strauss-Kahn (DSK) was accused of sexually assaulting a hotel maid in New York. This political figure, who was originally expected to compete for the French presidency, was accused of victimizing an immigrant from Guinea. Notably, Guinea at the time still owed the IMF as much as $472 million in loans, a debt that represented a significant portion of the country's GDP (30 billion Canadian dollars). Many readers familiar with John Perkins' book, including some Bitcoin holders, immediately linked this sexual assault allegation with the IMF's financial predation on developing countries. The victim's double misfortune was that she was forced to emigrate because her home country was under economic pressure from the IMF and was then directly victimized by a powerful figure within the organization. Although the sexual assault case was widely reported that year, mainstream media generally ignored this highly ironic connection, maintaining a consistent tone of respect for the IMF in its coverage. DSK subsequently resigned and was replaced by Christine Lagarde, the current President of the European Central Bank, as the IMF Managing Director. Notably, Lagarde herself has a criminal record and has repeatedly taken a negative stance on Bitcoin. In January 2025, she intervened to prevent the Czech Republic from including Bitcoin in its official foreign exchange reserves. Lagarde said: I believe... Bitcoin will not enter the reserves of any central bank on the General Council. Lagarde's term as President of the European Central Bank will end in 2027, and there are already rumors that she may succeed Klaus Schwab as Chairman of the World Economic Forum. If true, this would be the second time Lagarde has taken over the top position in an international economic organization left vacant due to sexual assault scandals. The Invisible Game with Bitcoin Currently, the International Monetary Fund (IMF) has issued $173 billion in outstanding loans to 86 countries, most of which are relatively poor. Through its Special Drawing Rights (SDR) system, the organization has the potential to issue up to $1 trillion in loans. As a "global reserve asset," the value of the SDR is linked to a basket of national currencies, essentially a financial instrument created out of thin air through a debt mechanism. Notably, although the IMF has 191 member countries, the distribution of voting rights heavily favors European and American countries. The United States alone enjoys 16.49% of the voting rights (a proportion that effectively gives it a veto over new loan projects requiring an 85% majority vote), while the voting rights of most major European countries remain between 3% and 5%. In contrast, China's voting rights in the IMF are only 6.1%—this proportion was obtained after a reform of voting rights, before which China's voting rights were even comparable to Belgium's. The IMF has long maintained a traditional personnel arrangement where the President is European and the head of the World Bank is American. This institutional arrangement further highlights the power imbalance in the global financial governance system.

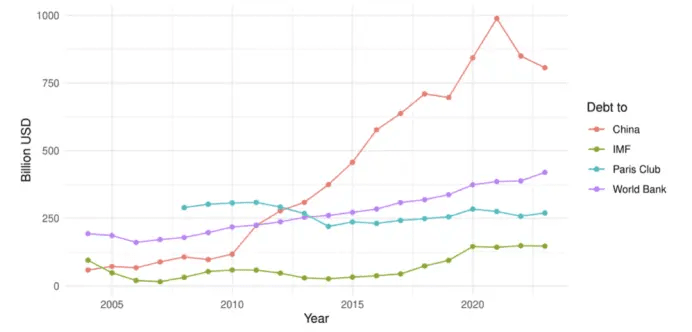

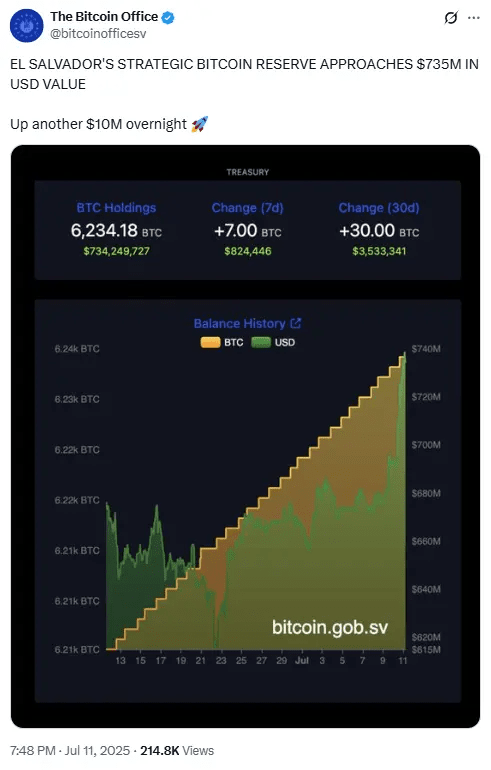

Source: International Monetary Fund (as of 2022) Over the past 15 years (since the DSK incident, we are not implying any causal relationship), the relative influence of the IMF and the World Bank has declined, with only moderate growth in their loan balances. During this period, China has emerged as the main financier of infrastructure projects in developing countries. This shift may be beneficial to smaller developing countries—enhancing their bargaining power and potentially avoiding the harsh conditions often attached to IMF loans (conditions that often require borrowing countries to cede control of key state-owned assets to foreign companies). However, the new dependency may lead these countries to shift from dependence on the IMF to excessive concessions to Chinese influence. Any form of external financial dependence may weaken the autonomy of sovereign countries, prompting some smaller economies to seek alternative solutions. Data shows that China has become the IMF's most competitive alternative, and has clearly gained the upper hand in this game in recent years. In stark contrast, the United States has invested hundreds of billions of dollars in military operations in countries such as Iraq and Afghanistan during this period, rather than economic development assistance. Source: https://cepr.org/voxeu/columns/rise-china-international-lender By modern financial standards, the balance sheet size of the International Monetary Fund (IMF) is relatively limited—currently comparable to the market capitalization of commercial entity MicroStrategy (MSTR US), and only accounts for 6% of the total market capitalization of Bitcoin. It is worth noting that since the DSK incident, Bitcoin has experienced exponential growth far exceeding the IMF's balance sheet size (although specific price charts are not shown in this article). To some extent, Bitcoin is competing with the IMF: both for the status of global reserve asset and as an alternative solution for infrastructure financing in emerging market countries. However, the Special Drawing Rights (SDR) have consistently failed to develop into a real competitor and ultimate dominator of Bitcoin, as some observers predicted in 2011. The following will focus on two distinct case study countries: El Salvador and Bhutan. It should be noted that our analysis is based on publicly available information and we have not visited these two countries in person. This kind of "armchair" research may be difficult to gain the approval of political commentators like Douglas Murray who focus on on-site investigations. El Salvador On June 5, 2021, at the Bitcoin conference held in Miami, Jack Mallers introduced El Salvador President Nayib Bukele to the attendees. Bukele announced a landmark decision at the conference: to establish Bitcoin as the country's legal tender. Since then, El Salvador has implemented a series of Bitcoin-supporting policies, including the establishment of a national strategic Bitcoin reserve. As of press time, the reserve holds 6,234.18 Bitcoins, worth approximately $735 million.

Source: https://cepr.org/voxeu/columns/rise-china-international-lender By modern financial standards, the balance sheet size of the International Monetary Fund (IMF) is relatively limited—currently comparable to the market capitalization of commercial entity MicroStrategy (MSTR US), and only accounts for 6% of the total market capitalization of Bitcoin. It is worth noting that since the DSK incident, Bitcoin has experienced exponential growth far exceeding the IMF's balance sheet size (although specific price charts are not shown in this article). To some extent, Bitcoin is competing with the IMF: both for the status of global reserve asset and as an alternative solution for infrastructure financing in emerging market countries. However, the Special Drawing Rights (SDR) have consistently failed to develop into a real competitor and ultimate dominator of Bitcoin, as some observers predicted in 2011. The following will focus on two distinct case study countries: El Salvador and Bhutan. It should be noted that our analysis is based on publicly available information and we have not visited these two countries in person. This kind of "armchair" research may be difficult to gain the approval of political commentators like Douglas Murray who focus on on-site investigations. El Salvador On June 5, 2021, at the Bitcoin conference held in Miami, Jack Mallers introduced El Salvador President Nayib Bukele to the attendees. Bukele announced a landmark decision at the conference: to establish Bitcoin as the country's legal tender. Since then, El Salvador has implemented a series of Bitcoin-supporting policies, including the establishment of a national strategic Bitcoin reserve. As of press time, the reserve holds 6,234.18 Bitcoins, worth approximately $735 million. El Salvador's cooperation with the International Monetary Fund (IMF) dates back to 1959. As of April 2020, the IMF had provided the country with 23 financing packages. Before the Bitcoin policy was introduced, the last loan was a $389 million special loan for the COVID-19 pandemic approved in April 2020. In February 2025, after the Bitcoin policy was implemented, the IMF Board approved a new $1.4 billion, 40-month extended loan mechanism. As of June 27, 2025, $231 million had been disbursed under this mechanism. It is worth noting that the complete loan agreement between El Salvador and the IMF is kept confidential and the public cannot access its specific terms. This opaque practice is puzzling because intergovernmental agreements should have greater transparency. Nevertheless, the IMF has published a large number of related documents. We focused on two core documents: the 111-page report released on March 3, 2025 and the 98-page report released on March 19, 2025. The IMF report's excessive focus on Bitcoin is staggering. In these two reports totaling 209 pages, the word "Bitcoin" appears 319 times. Through word cloud analysis, we found that in the core chapters discussing credit policy, "Bitcoin" is the second most frequent word, second only to the generic word "financial". This fully demonstrates that in the IMF's assessment framework, Bitcoin has been regarded as the main source of risk related to El Salvador. The report views Bitcoin from an almost completely negative perspective—all related discussions presuppose that Bitcoin is risky and harmful, but never provide substantive arguments. The IMF completely ignores any positive impact that Bitcoin may bring, only mentioning in one place that "widespread adoption of crypto assets may threaten macroeconomic stability and increase fiscal risks." The report even regards low Bitcoin usage as a benefit, arguing that "price volatility is high and public trust is insufficient." In the IMF's logic, low adoption is equivalent to low risk. The report dedicates multiple chapters to discussing how to "prevent Bitcoin risks" and puts forward seven specific policy recommendations:

El Salvador's cooperation with the International Monetary Fund (IMF) dates back to 1959. As of April 2020, the IMF had provided the country with 23 financing packages. Before the Bitcoin policy was introduced, the last loan was a $389 million special loan for the COVID-19 pandemic approved in April 2020. In February 2025, after the Bitcoin policy was implemented, the IMF Board approved a new $1.4 billion, 40-month extended loan mechanism. As of June 27, 2025, $231 million had been disbursed under this mechanism. It is worth noting that the complete loan agreement between El Salvador and the IMF is kept confidential and the public cannot access its specific terms. This opaque practice is puzzling because intergovernmental agreements should have greater transparency. Nevertheless, the IMF has published a large number of related documents. We focused on two core documents: the 111-page report released on March 3, 2025 and the 98-page report released on March 19, 2025. The IMF report's excessive focus on Bitcoin is staggering. In these two reports totaling 209 pages, the word "Bitcoin" appears 319 times. Through word cloud analysis, we found that in the core chapters discussing credit policy, "Bitcoin" is the second most frequent word, second only to the generic word "financial". This fully demonstrates that in the IMF's assessment framework, Bitcoin has been regarded as the main source of risk related to El Salvador. The report views Bitcoin from an almost completely negative perspective—all related discussions presuppose that Bitcoin is risky and harmful, but never provide substantive arguments. The IMF completely ignores any positive impact that Bitcoin may bring, only mentioning in one place that "widespread adoption of crypto assets may threaten macroeconomic stability and increase fiscal risks." The report even regards low Bitcoin usage as a benefit, arguing that "price volatility is high and public trust is insufficient." In the IMF's logic, low adoption is equivalent to low risk. The report dedicates multiple chapters to discussing how to "prevent Bitcoin risks" and puts forward seven specific policy recommendations:

Legal Level: Abolish Bitcoin's legal tender status

Payment System: Eliminate the obligation for public and private sectors to accept Bitcoin payments

Tax System: Clearly stipulate that taxes are payable only in US dollars

Government Payments: Ensure that national debts are not settled in Bitcoin

Chivo Wallet: Publish an audit report and terminate government involvement by July 2025

Regulatory Framework: Focus on preventing money laundering risks and follow FATF recommendations

Investment Restrictions: Restrict government investment behavior in Bitcoin

Some of these loan conditions seem overly harsh. For example, allowing companies to freely choose payment methods is a reasonable request, but forcing a sovereign country to amend its laws through loan conditions (using other countries' funds) is morally questionable. However, this is precisely how the IMF has always operated. This practice of imposing ideological preferences on borrowing countries precisely confirms the power operation model revealed by John Perkins in (Confessions of an Economic Hit Man).

The government's restrictions on Bitcoin investment have attracted the most attention. Especially because the government has been buying Bitcoin and promoting it heavily. The following two paragraphs from the report most clearly explain this topic:

During the implementation of the plan, the authorities committed not to accumulate Bitcoin

In the context of the plan, the public sector will not voluntarily accumulate Bitcoin

Due to the inability to access the actual loan agreement text, we are unable to confirm the specific commitments made by the Salvadoran government. However, based on public statements, the IMF's demands are quite clear. The reality, however, presents an intriguing contradiction—the country continued to increase its Bitcoin holdings in 2024, albeit at a slower rate of one Bitcoin per day. When (Forbes) reporter Javier Bastardo inquired about this apparent inconsistency with the IMF, the response was ambiguous:

According to the plan, the government has committed not to further increase Bitcoin holdings across the public sector. We have consulted with the relevant authorities, who have assured us that the recent increase in Bitcoin holdings in the strategic Bitcoin reserve fund is in line with the agreed plan conditions.

This flexibility in policy implementation has sparked much speculation: perhaps the agreement limits the proportion of Bitcoin investment to GDP, and the purchase quota increases accordingly as the economy grows; or perhaps El Salvador has, through some institutional design, classified Bitcoin assets as a special category outside the "public sector". In any case, one obvious fact is that although the IMF has shown a strong anti-Bitcoin stance, the Salvadoran government is clearly seeking a balance—hoping to maintain a cooperative relationship with the IMF and formally limit the scope of Bitcoin policies while also insisting on exploring greater economic sovereignty and independence through Bitcoin. This "tightrope walking" strategy precisely reflects the real difficulties and wisdom of small countries in the global financial system.

Bhutan

Bhutan, Paraguay, and Laos together constitute a unique group of countries—these countries possess inherent hydropower resources, with electricity generation often far exceeding domestic grid demand. This energy endowment presents a dual opportunity: traditionally, surplus electricity is exported through cross-border transactions (Bhutan to India, Paraguay to Brazil, Laos to Thailand and Vietnam), but this trade model grants excessive bargaining power to electricity importing countries because they are the only realistic channels for absorbing the surplus electricity.

However, Bitcoin mining provides a breakthrough option for these countries. Bhutan has taken the lead in exploring this path, maximizing the value of natural resources by converting surplus electricity into digital currencies. In theory, this innovative model may make Bhutan, Paraguay, and Laos potential winners in the Bitcoin economy, while the relative advantage of traditional electricity importing countries may be weakened.

Located in the Himalayas, Bhutan is famous for its unique natural landscapes and spiritual pursuits. This country, with a GDP of approximately $3.3 billion, places Gross National Happiness (GNH) and sustainable development above traditional economic growth indicators. Tourism (accounting for 15% of GDP) is one of its economic pillars—although this industry was not open to the outside world until 1974. It is precisely this special economic structure that has caused Bhutan to suffer particularly severe impacts during the COVID-19 pandemic, which has also prompted the country to more actively seek innovative economic solutions such as Bitcoin.

Bhutan also faces the challenge of talent outflow. To address this issue, the government announced in 2023 that it would increase public sector salaries by 50% overall. Unlike El Salvador, Bhutan does not purchase Bitcoin in the open market, but makes full use of its surplus hydropower resources for Bitcoin mining. To date, the country has accumulated 11,611 Bitcoins (worth approximately $1.4 billion), equivalent to 42% of its GDP. This strategic move has significantly enhanced Bhutan's economic autonomy—not only reducing its reliance on external funding such as the IMF, but also providing funding for domestic infrastructure construction and public sector development.

Although Bhutan has not borrowed from the IMF, it still receives some support from the World Bank. In the World Bank's latest 125-page country partnership report, Bitcoin is only briefly mentioned three times, far less obsessive than in the IMF report. However, the World Bank still criticized Bhutan's lack of transparency in its Bitcoin mining operations. It is foreseeable that without the economic buffer brought by Bitcoin, Bhutan would likely be forced to seek loan support from the IMF. This alternative financial path allows the Himalayan country to maintain its unique Gross National Happiness development philosophy while gaining more policy autonomy.

Bhutan recently announced a very forward-looking "Mindfulness City" plan, a special zone that will adopt a special legal framework different from other parts of the country (see video for details). Although the global economic zone model is not uncommon, Bhutan's vision is unique: focusing on sustainable development, using natural engineering methods to address flood risks, designing important cultural facilities as bridges across rivers, and even integrating temples into colorful hydropower station buildings.

This Buddhist-wisdom-filled city project is likely partially dependent on Bitcoin mining revenue as a source of funding. In fact, Bhutan has already become a successful example of the Bitcoin economy—by converting surplus hydropower into digital assets, the country not only promotes infrastructure construction in a unique, eco-friendly way, but also achieves a substantial increase in public sector salaries. Even more valuable is that these achievements are made while maintaining national independence and staying away from the intervention of so-called "economic jackals".

Looking ahead, if Bitcoin's value continues to grow, coupled with prudent governance and political wisdom on the part of the Bhutanese government, this "Land of the Thunder Dragon" and its people are poised to become the most successful strategic beneficiaries of the digital currency era. Perhaps in the near future, we will witness Bhutan becoming the first classic case of a sovereign nation empowered by Bitcoin.