Written by: Saurabh Deshpande, Decentralised.co

In November 2023, Blackstone acquired a pet care application called Rover. Rover initially served as a way to find dog walkers or cat sitters. The pet care industry typically consists of tens of thousands of small, often localized, offline service providers. Rover integrated these suppliers into a searchable marketplace, adding review and payment features, making it the default platform for pet care services. By the time Blackstone privatized it in 2024, Rover had become a hub for demand in the field. Pet owners think of Rover first, and service providers have no choice but to list on this platform.

ZipRecruiter did something similar in the recruitment space. It collects job information from employers, job boards, and applicant tracking systems, distributing it across multiple channels. ZipRecruiter posts job listings on social networks like Facebook. For employers, ZipRecruiter becomes a one-stop distribution channel; for job seekers, it is a unified entry point to the market. ZipRecruiter does not own companies or jobs but owns relationships with both parties. Once this relationship is solidified, it can charge for visibility and job matching, which is an introductory lesson in aggregation economics.

Aswath Damodaran calls this model 'owning the shelf': concentrating chaotic, fragmented supply, controlling how it is displayed, and charging for access. Ben Thompson refers to it as 'aggregation theory': establishing direct relationships with end users, allowing suppliers to compete for their service, and extracting value from each transaction. The core characteristics across different fields are consistent: Google with webpages, Airbnb with listings, Amazon with goods.

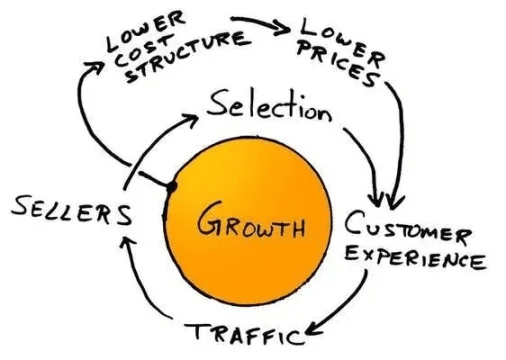

Amazon's flywheel is a classic illustration of this concept. During the downturn after the internet bubble burst, Jeff Bezos and his team adapted Jim Collins' 'flywheel' concept, sketching out a cycle that every MBA can now recite: more choices lead to better customer experiences, attracting more traffic, which in turn attracts more sellers, lowering unit costs and providing lower prices, ultimately leading to more choices. A single turn of the flywheel may have limited effects, but after turning it a thousand times, the machine starts to roar. Bezos's motto during this period was, 'Your profit is my opportunity.' The core lies in self-reinforcement: more users, more suppliers, lower costs, and ultimately higher profits.

Once this model works, it can be considered perfect. The growth rate of costs is far lower than that of revenue, and products will optimize as users increase. But this only holds under two conditions: the aggregated content must be valuable, and the supply side must be difficult to exit easily; both are essential; otherwise, the moat will become shallow. Take eBay as an example; it aggregated millions of unique niche sellers and buyers in the early 21st century. This aggregation was highly valuable, but when sellers realized they could build their own stores on Shopify or turn to Amazon, they left one after another. The flywheel does not stop overnight, but if the supply side is no longer controlled, it begins to wobble and eventually becomes ordinary.

Damodaran explains the power of platforms and aggregators in a tangible way. He mentions 'controlling the shelf', which does not refer to supermarket shelves in a literal sense, but rather to the space first encountered when customer demand arises. Controlling this space means deciding what to display, how to display it, and the costs of entry. You do not need to own the goods themselves; you only need to own the relationship with buyers, and others must go through you to reach the buyers. When analyzing Instacart, Uber, Airbnb, or Zomato, Damodaran repeatedly emphasizes: the aggregator's job is to integrate a chaotic, fragmented market into a single glass window, making that window the only one worth noticing. Once this is achieved, you can charge for 'viewing rights'.

Ben Thompson believes that aggregators are businesses that establish direct relationships with end users at internet scale, provide standardized and reliable experiences, and let suppliers compete for their service. At internet scale, you are not the biggest store in town; you are the store that covers all towns at once.

The marginal cost of serving the next customer is nearly zero, but the marginal value of owning them is enormous. Because each customer reinforces your brand, data, and network effects. As aggregators control demand, suppliers become interchangeable. This does not mean there is no quality difference, but rather that suppliers cannot take customer relationships with them when they leave. Hotels on Expedia, drivers on Uber, and sellers on Amazon all need each other more than the aggregator needs them.

Damodaran's research reminds us that flywheels do not operate the same way in all markets. For example, Uber aggregated local driver liquidity, but drivers can simultaneously open three apps and choose the first order they receive. This creates vulnerabilities in the moat. In contrast, Airbnb hosts offer unique listings, with limited alternative channels, making their cut more sustainable.

Shelves may hold value in low-margin areas, but there is limited room for extraction, and suppliers can easily push back. This is why Instacart must venture into advertising and white-label logistics to achieve growth.

The economic structure of supply is as important as the number of users focusing on the platform. If the platform has goods that are readily available everywhere, you are just a convenience store with better visibility; but if the content is scarce, differentiated, and hard to substitute, people will continue to patronize, even if you charge higher fees. Think of high-end listings on Airbnb.

Why aggregators fail

When conditions are absent, an aggregator ceases to be a flywheel and becomes just an expensive carousel.

Quibi is a classic case of failing to control the shelf. The platform had expensive Hollywood content and a sleek application but lacked direct channels to users. Potential users had already gathered on YouTube, Instagram, and TikTok. These platforms controlled attention while Quibi locked content in a standalone app away from users, forcing it to attract users only through advertising and promotions.

Excellent aggregators start with zero marginal cost user outreach methods, such as built-in distribution, installation volume, or daily habits. Quibi had nothing and ultimately exhausted time and funds before building these.

Facebook's Instant Articles faces a similar problem. Its idea is to aggregate content from publishers, accelerate loading within Facebook, and monetize traffic. However, publishers can easily distribute content to their open networks, applications, or other social platforms. Instant Articles never became the default reading platform, merely an option in the information stream.

Both examples violate the same rule: companies failed to own user relationships in a way that creates default behavior, and the supply side does not suffer significantly once they exit.

A list of excellent aggregators is simple:

Directly connect and own user relationships;

The supply side must be either unique or interchangeable to avoid being held hostage by a single supplier;

The marginal cost of increasing supply is close to zero or sufficiently low, optimizing the business model with scale.

If these conditions are not met, you are just another easily replaceable intermediary.

How liquidity becomes a moat

In the crypto industry, projects can build moats in various ways. Some establish trust through licenses and regulations (like USDC), some rely on technology (like Starkware's proof systems or Solana's parallel execution), and others depend on community and network effects (like Farcaster's user map). But the hardest to shake is liquidity.

'Correct execution' is crucial. However, if the incentives are strong enough, liquidity can shift quickly. In 2020, Sushiswap siphoned off over $1 billion from Uniswap in just a few days through liquidity mining rewards. The lesson is simple: liquidity will only solidify when leaving is more painful than staying.

Hyperliquid understands this deeply. It not only builds the deepest order book for perpetual contract exchanges but also allows other applications and wallets to directly access its liquidity. For example, Phantom can tap into Hyperliquid's order flow, providing users with narrow spreads without needing to build their own market. In this model, aggregators need suppliers more. When traders and applications default to using your routing, you are no longer an ordinary aggregator but a core channel they cannot avoid.

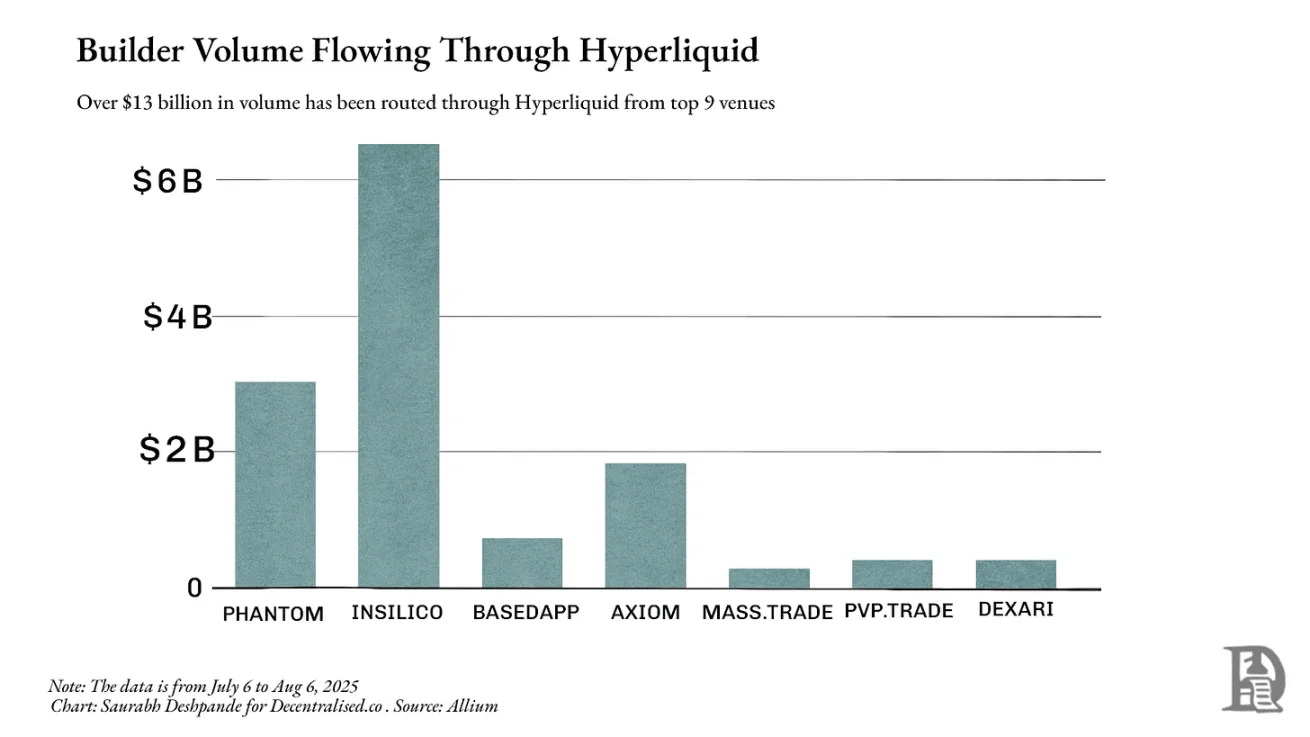

Beyond its own platform, Hyperliquid processed over $13 billion in transaction volume last month through other builders. Phantom handled $3 billion, earning over $1.5 million. This showcases Hyperliquid's current strong network effects.

Liquidity allows you to convert assets without affecting prices. In finance and DeFi, deep liquidity makes trading cheaper, borrowing safer, and derivatives possible. A lack of liquidity can turn even the best protocols into ghost towns. Once successfully established, liquidity tends to persist. Traders and applications will flow to deep pools, further increasing liquidity, narrowing spreads, and attracting more trades.

This is why protocols like Aave continue to thrive. Aave has large lending pools with multiple assets, making it the first choice for borrowers and lenders seeking scale and security. As of August 6, Aave's cross-chain total locked value exceeded $24 billion. Over the past 12 months, borrowers paid $640 million in fees, and the platform generated about $110 million in revenue.

Similarly, Jupiter, based on Solana, has evolved from a routing tool to the default entry point for trading on that network. On Ethereum, Uniswap has centralized most of the spot liquidity, so aggregators like 1inch can only provide marginal improvements. On Solana, liquidity is dispersed across platforms like Orca, Raydium, and Serum. Jupiter integrates them into a single routing layer, always providing the best price. Its trading volume once accounted for nearly half of Solana's total computational usage; any delay or interruption would immediately impact execution quality across the network.

Viewing liquidity as an aggregated object makes Jupiter's product decisions easier to understand. Acquisitions, mobile applications, and expansions into new trading and lending products are all aimed at capturing more order flow, keeping liquidity routed through Jupiter, and solidifying its position.

Jupiter is worth watching because it is a clear case of evolving from a niche tool to a liquidity platform in DeFi. Starting with finding the best spot price, it gradually became the default routing for Solana liquidity, and then expanded to products that attract entirely new liquidity. Observe how it navigates through these stages and mutually reinforces them, providing a vivid case for aggregation dynamics.

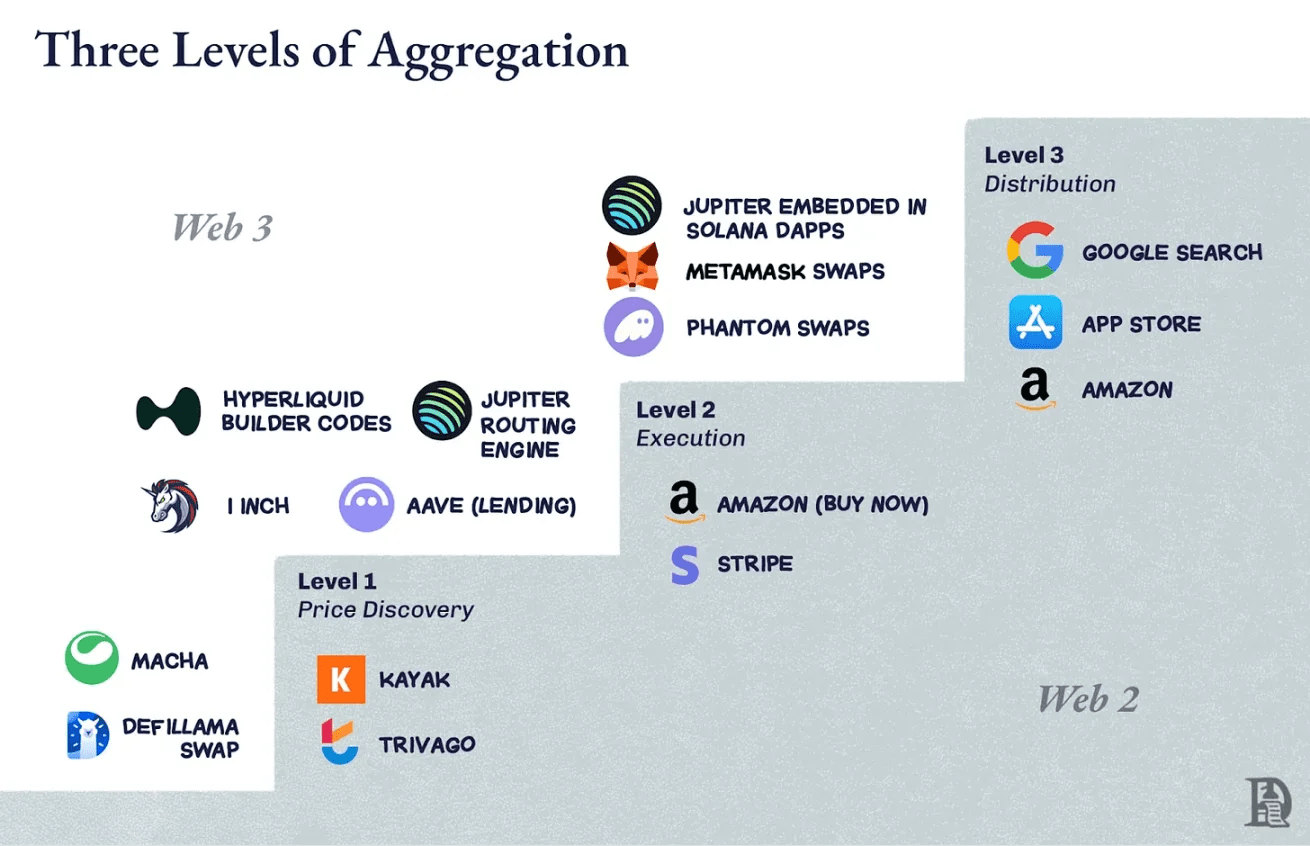

Levels of aggregation

Three questions serve as a quick checklist for identifying potential aggregators:

What is the key differentiating factor for existing businesses? Can it be digitized? In DeFi, the differentiating factor is liquidity. Deep pools can offer narrower spreads and safer loans. Liquidity has been digitized, easy to read and compare.

If the differentiating factor is digitized, does competition shift to user experience? When liquidity can be accessed arbitrarily, competition revolves around execution quality: faster settlements, better routing, fewer failed transactions. Products like BasedApp and Lootbase were born from this. The former packages DeFi primitives into a smooth mobile experience, while the latter brings Hyperliquid's deep perpetual liquidity to mobile.

If you win user experience, can you build a virtuous cycle? Traders come for better prices, attracting more liquidity, which in turn provides better prices. When liquidity is embedded in habits and integrated, it becomes sticky.

Become the default entry point of the market; if the supply side cannot bear your absence, you can charge display fees or decide the order flow in DeFi.

Note: The boundaries between different levels are often blurred. The classification is not precise but provides a mental model for aggregation levels.

First Level: Price Discovery

This is the most basic work: telling people where the best trades are. Kayak is for flights, Trivago is for hotels. In the crypto space, early DEX aggregators like 1inch or Matcha fall into this category. They check available pools, display the best rates, and provide jump-off points. Price discovery is useful but fragile, as demonstrated by DeFiLlama's exchange function.

If the underlying market is already concentrated (like Ethereum spot trading on Uniswap), routing improvements become negligible, as users can go directly to the trading venue, making your assistance non-essential.

Second Level: Execution

At this point, you are no longer directing users elsewhere; you are operating on their behalf. Amazon's 'one-click purchase' belongs to this level. In DeFi, Aave's lending functionality is at this level. When borrowing, liquidity already exists within its contracts. Execution increases stickiness, as the results are directly related to you: fast settlement and a good experience with no failed transactions.

Third Level: Distribution Control

You become the entry point. Google search is to webpages what app stores are to mobile applications. In the crypto space, the built-in exchange tag in wallets can serve as the starting and ending point for average users.

On Solana, Jupiter has reached this level. It began as a price discovery tool, transitioned into the execution layer through smart order routing, and then embedded into front ends like Phantom and Drift. A large volume of Solana transactions is actually Jupiter transactions, even if users never typed 'jup.ag'. This is distribution control; suppliers cannot bypass you to reach users.

Climbing levels in DeFi

The challenge for DeFi lies in the potential for liquidity to shift rapidly. Incentives can drain funds from pools overnight. Therefore, ascending from the first level to the third level is not only about becoming a top aggregator but also about creating enough reasons for liquidity and order flow to continue passing through your routing.

On Ethereum, 1inch primarily operates at the second level, as Uniswap has completed the aggregation work through concentrated liquidity. Routing has value for edge cases, but improvements are limited, with many traders choosing to skip it. Additionally, aggregators like CowSwap and KyberSwap also occupy a considerable share. Aave belongs to the second level, as it controls execution in a niche, but it is infrastructure rather than a starting point.

Jupiter's advantage on Solana lies in its ability to sequentially climb three levels. Liquidity is dispersed, the value at the first level is significant; the routing engine is superior to manual exchanges, naturally transitioning to the second level; through direct integration with wallets and dApps, it reaches the third level, fully controlling the distribution of Solana's liquidity. At one point, nearly half of Solana's computational usage came from Jupiter transactions, as both the demand side of traders and the supply side of liquidity pools relied on Jupiter.

Once reaching the third level, the question becomes 'What else can run through this distribution?' Amazon started with books and ended up with everything; Google started with search and ultimately controls maps, email, and cloud computing. For Jupiter, distribution is the order flow. The obvious next step is to add products like perpetual contracts, lending, and portfolio tracking, leveraging the same liquidity relationships.

A larger move is Jupnet. Solana has yet to match the throughput and execution characteristics of venues designed for financial-grade latency and certainty, like Hyperliquid. These characteristics are crucial for scaling the entire financial stack to real-world sizes. A simpler option would be to launch products on chains that already have these characteristics, but Jupiter chooses the more difficult path of building Jupnet as an application-controlled low-latency execution layer, running in parallel with Solana.

Jupnet aims to become shared infrastructure within the Solana ecosystem, supporting latency-sensitive transactions such as perpetual contracts, quote request systems, bulk auctions, and ultimately native settlement on Solana. If successful, it will provide the speed and certainty expected of vertically integrated venues while retaining user and asset retention. This is an attempt to bridge the gap between the throughput of general-purpose blockchains and the micro-latency demands of global finance, without requiring cross-chain liquidity fragmentation.

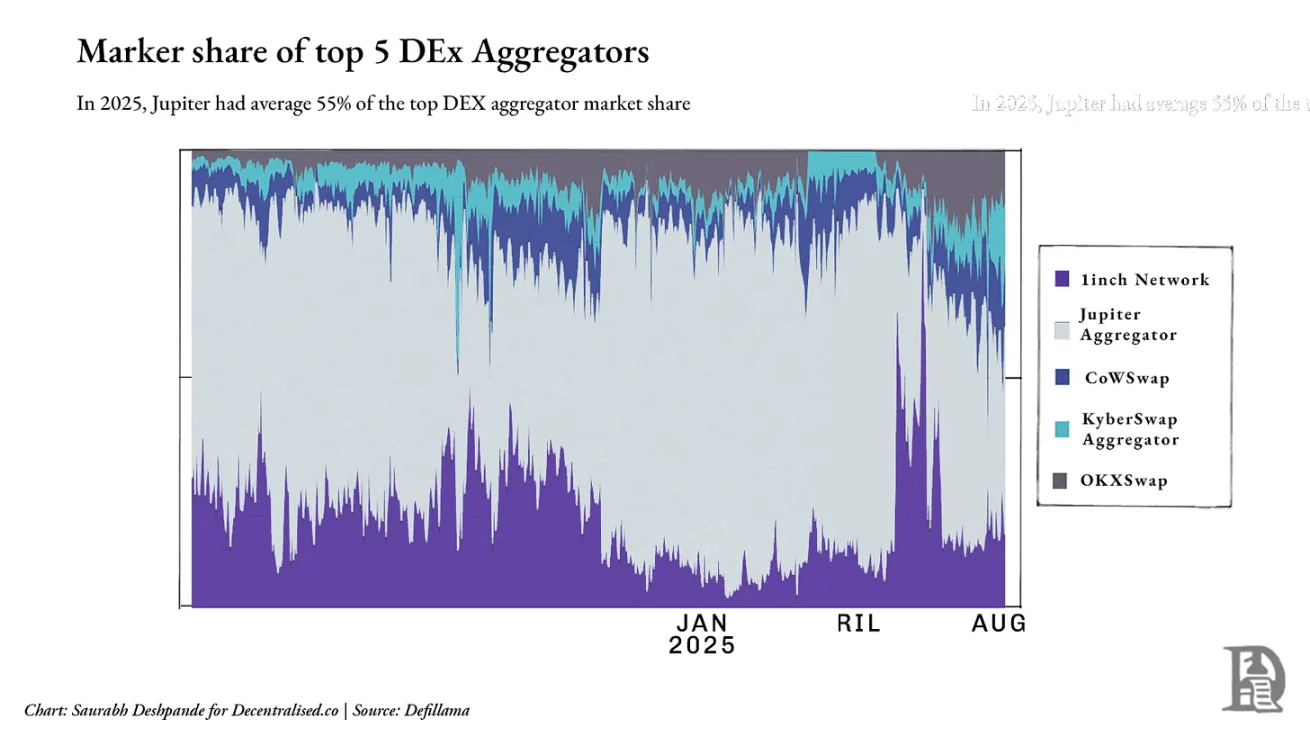

However, it should be noted that although Jupiter dominates within Solana, there is still fierce competition at the industry level. In the cross-chain space, 1inch, CoWSwap, and OKX Swap maintain significant positions. By 2025, Jupiter is expected to average around 55% of the market share among the five major DEX aggregators, but this share fluctuates with on-chain activity and integrations. The chart below shows the degree of decentralization of the aggregation layer outside Solana.

Clearly, Jupiter has become an aggregator within the Solana ecosystem. The flywheel has started: more traders bring more liquidity, more liquidity optimizes execution, and better execution attracts more traders. At this point, you are not only a liquidity aggregator but also the shelf, habits, and market entry. So, when liquidity is no longer sufficient, how do you continue to grow? Jupiter's answer is to acquire projects that have already captured new user flows.

Mergers and acquisitions as a growth engine

Previously, I wrote about two major themes of scaling businesses: the essence of compound innovation and how companies can accelerate this process through acquisitions. The former concerns building new products, functions, or capabilities based on existing advantages, while the latter involves recognizing when 'buying' is faster than 'building' to establish an advantage.

Jupiter's evolution encompasses both. Its acquisition strategy is rooted in seeking founders' teams with real appeal and integrating them into a distribution network that amplifies influence. The company seeks vertical domain expert teams to expand its coverage without dragging down its core roadmap.

This is not just about purchasing functional additions but acquiring teams that have already dominated Jupiter's targeted market segments. Once these teams integrate into Jupiter's distribution wallet interface, API, and routing, their product growth accelerates, and the traffic generated feeds back into Jupiter's core.

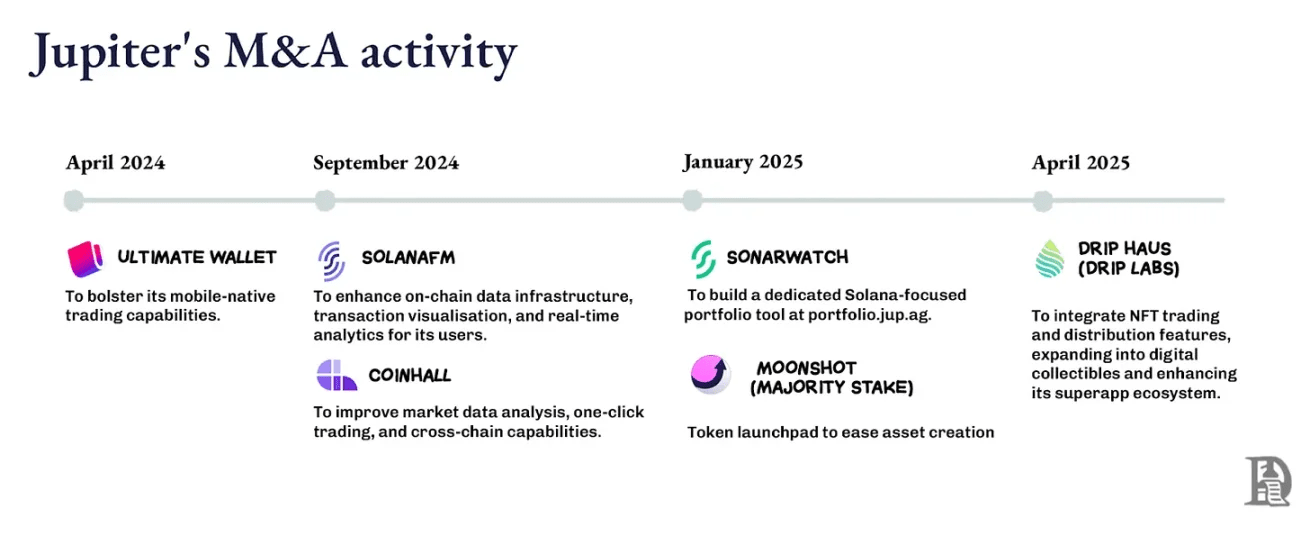

Moonshot brings a token launchpad that transforms new token creation into direct exchanges and trading activities within the Jupiter ecosystem; DRiP adds a community-driven NFT minting and distribution platform, attracting audiences away from trading interfaces and converting them into on-chain behavior; Portfolio acquisition provides position management tools for active traders. Jupiter could have built these functions internally at a lower cost, but its goal is to acquire founders, not just features.

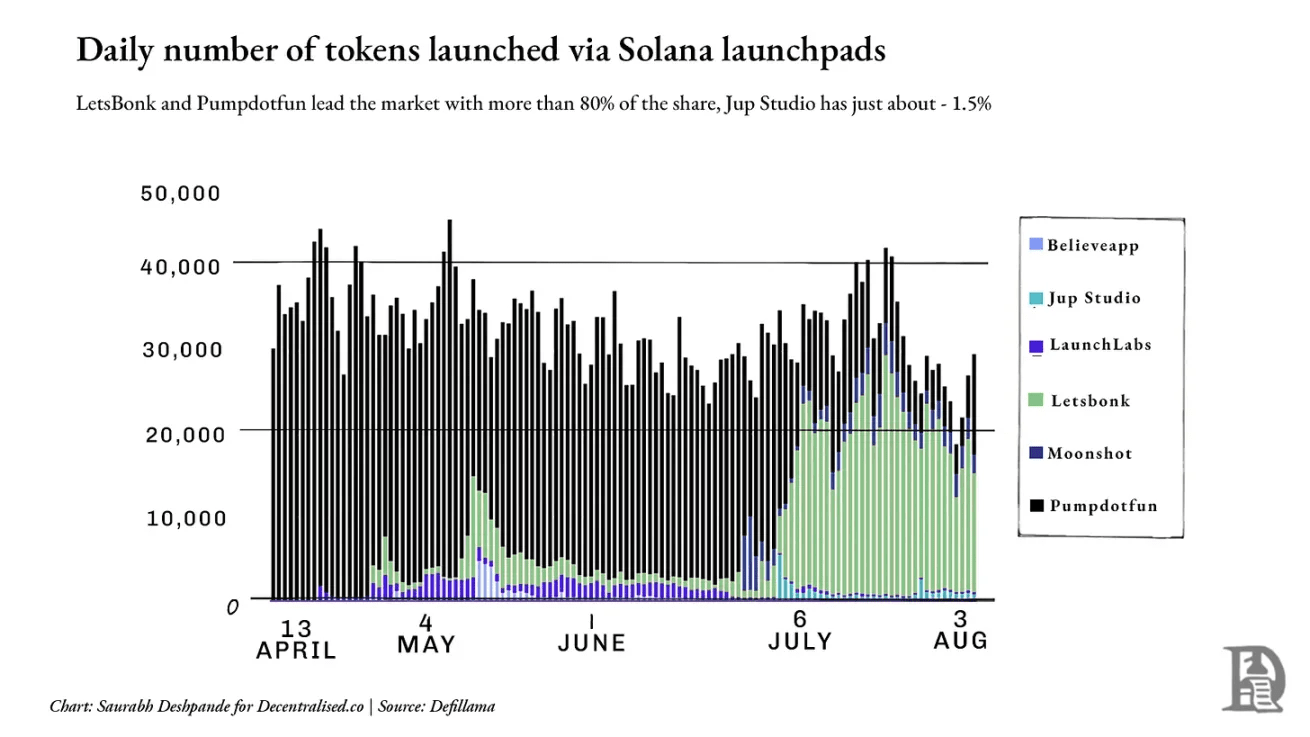

However, the growth of some indicators has yet to materialize. Taking the launchpad sector as an example, market leaders Pumpdotfun and LetsBonk control over 80% of daily token issuance, while Jup Studio and Moonshot together hold less than 10%. The chart below shows the dominance of incumbents. In this case, the default pattern may have solidified, and Jupiter may need a completely different approach to break through.

Force multipliers: founder-led acquisitions

To expand the shelf, it is necessary to bring in operators who already control targeted market segments. Jupiter's selection criteria are: does the team bring new types of liquidity or users that reinforce the flywheel? This logic echoes Amazon's early flywheel: every new category or supplier increases 'choice', optimizing customer experience, driving more traffic, and attracting more suppliers.

For Jupiter, each acquisition is like adding a new shelf to a store, broadening choices and deepening the relationship between traders and liquidity providers.

Acquire creative founders to enable Jupiter to penetrate unfamiliar fields (such as DRiP's NFT culture or mainstream retail token issuance) without diluting core competitiveness. These founders understand niche spaces, have communities that trust them, and can act quickly. Tapping into Jupiter's distribution channels amplifies their reach overnight while Jupiter gains new user flows and liquidity.

Acquisition cases illustrate this point: Moonshot is a minting and trading platform aimed at mainstream behavior, with the tokens issued seamlessly transitioning into exchanges, funding markets, and perpetual contracts within the Jupiter ecosystem; DRiP is a creator-first distribution channel for collectibles, attracting communities that would otherwise not engage with trading interfaces.

Moonshot added over 250,000 users within three days of launching the TRUMP token, processing over $1.5 billion in trading volume; DRiP attracted over 2 million collectors, minting over 200 million collectibles, with more than 6 million secondary sales.

Integration follows a clear pattern: founders retain product direction leadership; products go live integrated with the Jupiter interface and back-end, instantly benefiting from its user base, while Jupiter gains new traffic; each acquisition adds unique liquidity primitives (such as issuance, culture, leverage) rather than duplicating existing functionalities. Core competitiveness remains unchanged, with all paths still returning to Jupiter.

In DeFi, code can fork overnight, but market share is hard to replicate. Founder-led acquisitions allow Jupiter to add market share without losing its core path, making its flywheel harder to replicate. As applications control execution and low-latency infrastructure matures, Jupiter may target teams for risk engines, matching layers, and specialized venues, integrating them into Jupnet.

Aggregator vs Supplier

In the big picture, two dominant models are emerging in DeFi: Jupiter and Hyperliquid. Both are powerful, but their strategies are entirely different.

Hyperliquid aims to control liquidity rather than directly own end-user relationships. It offers liquidity as a service. If a better user experience can be built, welcome to use Hyperliquid's order book and execution engine. Builder Codes are based on this idea, allowing others to own the front-end experience while Hyperliquid quietly supports the back-end, maintaining a supplier-first model.

Jupiter focuses on distribution; it hopes to control the interface, shelf, and market entry, aggregating dispersed liquidity by becoming the default interface and directing it to the desired places. This means controlling user relationships, not just execution paths. From perpetual contracts to portfolios, Jupiter aims to make all financial interfaces start and end within its paths.

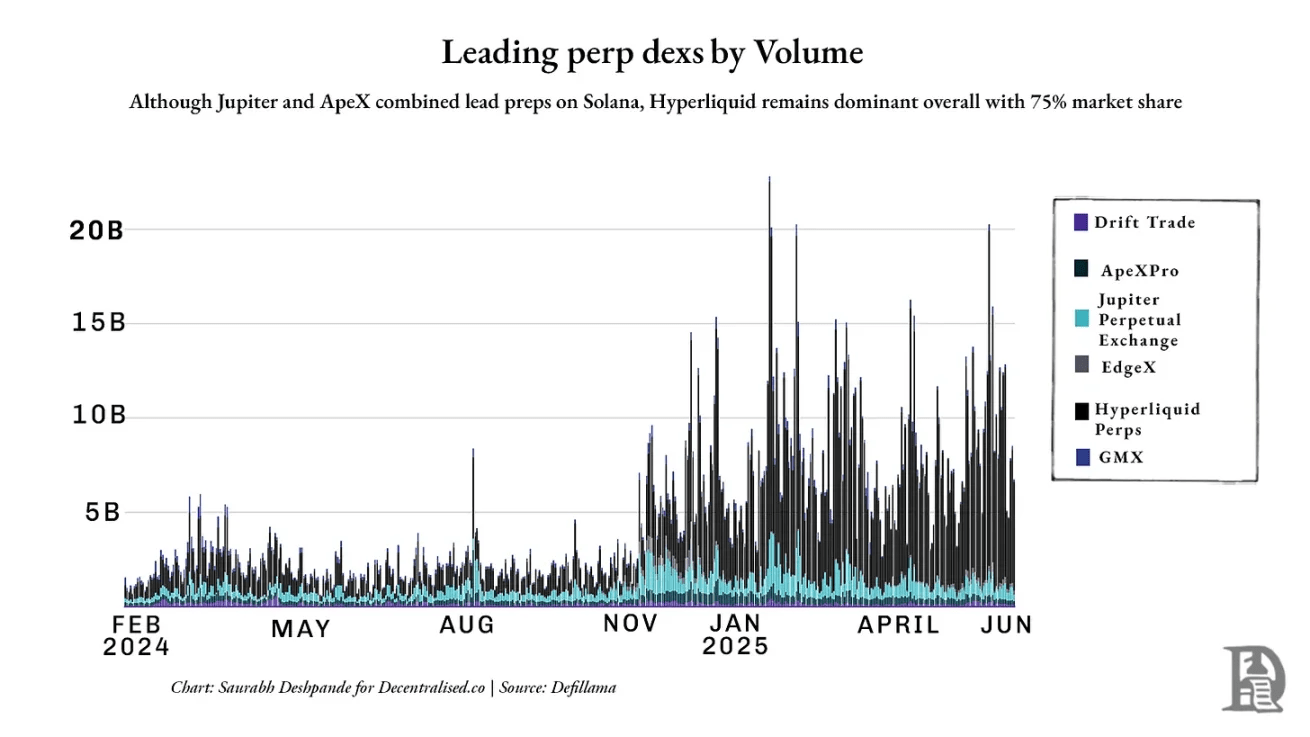

However, perpetual contracts may expose the current limitations of this strategy. Jupiter has made progress on Solana, but Hyperliquid still dominates the market with about 75% of the perpetual DEX market share. The chart below shows the leading margin of Hyperliquid in raw trading volume:

Both models bet on scale, but their starting points are opposite. Jupiter believes liquidity follows the user interface; Hyperliquid believes liquidity is the interface. Jupiter builds entry points, while Hyperliquid builds endpoints.

In practice, we witness differentiation: if you need broad interfaces and user aggregation, choose Jupiter; if you need depth, certainty, and composability, choose Hyperliquid. One converts liquidity into a dependency network, while the other becomes the underlying structure built by the crowd.

Winners are not only those who arrive first, but also those who others cannot abandon.

This is precisely what makes DeFi exciting right now. We are witnessing a philosophical showdown for the first time: one side believes distribution is the moat, while the other firmly believes liquidity is.

Applications are the new platforms

When Ethereum Layer 2 first appeared, there was hope it would become a new platform: a neutral ground where applications could be composable, competitive, and scalable. However, it turned out that L2s did not become platforms as imagined but mostly stayed at the infrastructure level: providing the technical basis for speed, security, and scalability without controlling user relationships.

Platforms are the interface at the starting point of the user journey, where demand aggregates, habits form, and distribution survives. Few L2s cross this line; most are pipes rather than shelves, rarely constructing meaningful distribution, and even less likely to become the default entry point for users.

In contrast, applications like Jupiter and Hyperliquid are gradually revealing platform characteristics. They have user relationships, embed into daily habits, and strengthen their position through acquisitions or integrations with other applications. In fact, they are beginning to closely resemble Web2.

Google transcended its search engine roots by acquiring YouTube, turning its search advantage into video dominance; Facebook expanded its control of attention by acquiring Instagram and WhatsApp. They targeted adjacent fields where they were absent but where users had already gathered, and crucially, they acquired the core players in those fields. Once acquired, these applications could immediately tap into the existing distribution flywheel of Google and Facebook, resulting in the capture of multi-channel user attention.

Jupiter is executing a similar strategy. Launchpads, NFT minting tools, portfolio managers, and now Jupnet all serve the same purpose: to expand coverage, capture more user behavior, and route more liquidity to itself. Its strategy is to become the shelf, the default choice, and the starting point for financial interactions.

However, aggregation is not a surefire strategy. History is filled with failed platform acquisitions and aggregation attempts, often due to a failure to own user relationships or a misunderstanding of how habits form.

Take Microsoft's acquisition of Nokia as an example. This was a bet on controlling mobile distribution, but users have shifted to the iOS and Android ecosystems. Microsoft owns hardware and software, but its mobile devices and operating systems are either too similar to existing products or not compelling enough to prompt user transition. It did not control the application layer, did not win developer loyalty, and did not provide reasons for behavior change. A lack of control over supply or clear differentiation leaves the shelves unvisited.

These cases reflect a core truth: acquisition alone does not create a flywheel. Without a starting point, habits, or interfaces, no matter how many functions are bundled, users will not follow.

This makes the current moment in DeFi particularly interesting. Jupiter acquires front ends, distribution channels, and liquidity primitives, attempting to become the default entry point for the Solana financial stack; Hyperliquid, in contrast, builds depth rather than breadth, allowing others to center around its composition.

In a sense, we are witnessing a true platform war unfolding among applications rather than between public chains as many had anticipated. This raises bigger questions: if L2s do not control distribution, where will value flow when applications on them do? What about fat protocols?

We conclude with unresolved questions, as there are no definitive answers yet. In the future, we will bring sharper insights, new data points, and more stories and analogies to clarify the direction of all this.