In recent months, stablecoins have undoubtedly become the hot topic in the financial and cryptocurrency circles! The US and Hong Kong have successively passed legislation supporting stablecoins, while internet giants and established financial institutions have jumped into the fray, either hoarding coins or applying for licenses, as if a spring breeze has suddenly arrived, bringing forth countless blossoms. In contrast, mainland China still appears to have no policy loosening, giving a strong feeling of waiting for fish to bite. Among this, a piece of news about the large-scale use of stablecoins in Yiwu has spread widely on the internet, mainly citing two sources: Huatai Securities' research report shows that stablecoins have become an important tool for cross-border payments in Yiwu, and the blockchain analysis company Chainalysis estimates that the on-chain stablecoin flow in the Yiwu market will exceed 10 billion USD in 2023.

Interestingly, when reporters conducted field visits and surveys, most merchants stated they had not heard of stablecoins and did not understand them. A few merchants expressed doubts about the compliance and costs of stablecoins, and only a very few merchants explicitly stated that they had used stablecoins for payments. The situation on the ground somewhat resembles an old man downstairs answering Charlotte with esoteric responses. What is the real situation? Let's dig into the two sources of the news.

Huatai Securities research report

Based on publicly available information, I have not been able to find any media providing the specific name and source of Huatai Securities' research report. However, with the help of friends, I found a macro securities research report published by Huatai Securities on June 25, titled 'How Stablecoins Will Affect the Global Monetary System'. In this 31-page report, Huatai Securities systematically elaborates on the prospects and risks of stablecoins' development globally across eight chapters. On page 8 of the report, there is a description regarding the usage scenarios of stablecoins:

"Besides direct trading of crypto assets, the proportion of stablecoins in global commodity and service transactions, as a means of value storage, and the penetration rate among residents is rapidly developing. Specifically, in Yiwu, the world’s small commodity center, stablecoins have become an important tool for cross-border payments. The blockchain analysis company Chainalysis estimates that the on-chain stablecoin flow in the Yiwu market will exceed 10 billion USD in 2023."

However, unlike other viewpoints in the report that are supported by data charts, this particular viewpoint lacks data support.

Overall, the report is quite readable, and here are some of the viewpoints I have extracted:

1. Countries represented by the United States (dollar hegemony), the European Union (single market), and China (potential market) have large monetary volumes and stronger legislative demands, and the market scale for stablecoins is enormous. Countries represented by South Korea, which have developed digital and virtual economies, and those represented by Singapore, which have a high degree of openness and strong external dependence, will have a high penetration rate for stablecoins. Countries represented by emerging market economies such as Turkey, Argentina, and Nigeria, which have low currency stability, underdeveloped banking systems, a large underground economy, and capital controls or sanctions, will also have a high penetration rate for stablecoins.

2. In response to the challenges brought about by the development of stablecoins, major economies usually adopt two countermeasures: issuing digital currencies or strengthening regulation of stablecoins. For mainland China, research on digital currencies began as early as 2014, and a pilot was launched in 2019. With the rapid development of stablecoins, especially the stablecoin legislation in Hong Kong that will take effect this August, it may mark China's shift towards a 'dual-track' development path. On June 18 this year, the head of the central bank clearly stated at the Lujiazui Forum that emerging technologies such as blockchain and distributed ledgers are driving the vigorous development of central bank digital technologies and stablecoins, which also shows that the Chinese central bank's emphasis on stablecoins has significantly increased.

3. The legislation for Hong Kong's stablecoins is expected to accelerate the development of Hong Kong dollar, offshore renminbi, and even renminbi stablecoins, with further appreciation potential for the renminbi. Expanding the 'funding pool' for Hong Kong dollar and offshore renminbi, enriching the high liquidity assets they can invest in such as interest rate bonds, vigorously developing cross-border businesses, digital economy, and virtual economy, and increasing the usage scenarios for stablecoins are key to the success of Hong Kong's stablecoins and will once again activate the internationalization process of the renminbi.

4. Stablecoins pose challenges to cross-border financial regulation and face a certain degree of redemption risk. When the value of reserve assets fluctuates, the credit of the issuer is challenged, or even if the issuer goes bankrupt, fiat stablecoins may also experience a decoupling of value. As the scale of stablecoins expands and their impact on the traditional financial system deepens, there may ultimately be a need to accept stricter regulation, or even partial nationalization, in exchange for true stability.

Data analysis from Chainalysis

Unfortunately, through my searches of online resources, I found no relevant statements or statistical support regarding Yiwu merchants' use of stablecoins in the Chainalysis reports for 2023 and 2024 (cryptocurrency geographical report).

I have also extracted some data and viewpoints regarding mainland China and Hong Kong from the two reports by Chainalysis:

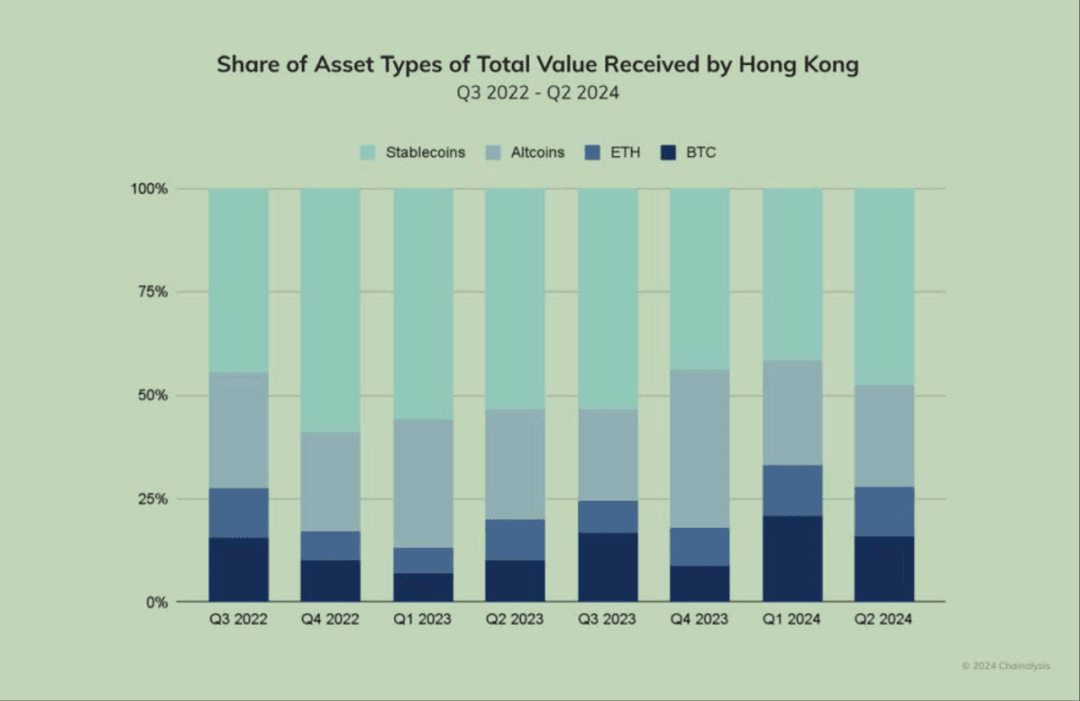

1. For a long time, the value proportion of cryptocurrency assets received by users in Hong Kong has remained above 40%, and with the stablecoin legislation in Hong Kong set to officially take effect this August, this proportion is expected to rise further.

Figure 1 The proportion of stablecoins in the cryptocurrency assets received in Hong Kong is high - Chainalysis

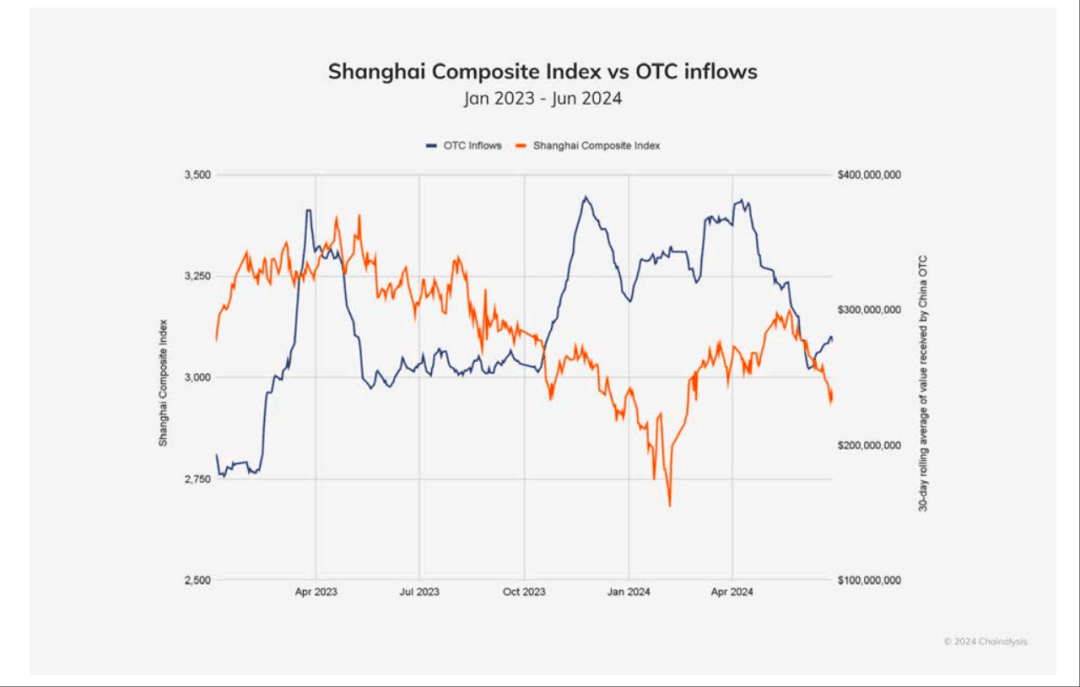

2. Data indicates that Chinese users are utilizing crypto assets to preserve and increase their wealth.

Figure 2 Comparison of the Shanghai Composite Index and OTC inflow from January 2023 to June 2024 - Chainalysis

In my view, while there may be a lack of accurate data to confirm whether stablecoins will be widely used in Yiwu, the combination of foreign trade and stablecoins indeed possesses inherent advantages. The characteristics of stablecoin payments, such as instant settlement, value stability, and low fees, address many pain points for small and medium-sized foreign trade merchants.

However, on the other hand, considering the regulatory policies in mainland China regarding stablecoins and other crypto-assets, mainland foreign trade merchants may face serious compliance issues if they directly use stablecoins in transactions, and there may even be potential criminal risks.

Moreover, considering that the current implementation of our country's export tax rebate policy often requires the provision of the bank's foreign exchange settlement slip, using stablecoins would mean that this certificate cannot be provided, thus enjoying no export tax rebate, which is fatal for the merchants' profits. On the other hand, qualifications for participating in exhibitions such as the Canton Fair typically use the bank transaction records of export companies as an important reference standard, and commercial banks' lending review standards also place importance on the bank transaction records of export companies. These factors determine that currently, the scale of stablecoin usage by exporters in Yiwu will not be too large.

So how can mainland foreign trade merchants compliantly utilize stablecoins to reduce costs and increase efficiency? Currently, a relatively compliant way is to leverage the linkage between Hong Kong companies and mainland companies, using Hong Kong's trade facilitation and open policies towards crypto assets to achieve compliant integration of traditional foreign trade and crypto payments.

Hong Kong dollar stablecoins and feasible compliant foreign trade models using stablecoins

On August 1, the Hong Kong (Stablecoin Ordinance) will officially take effect, and the Hong Kong government will begin processing license applications for issuing stablecoins in Hong Kong. This means that stablecoins recognized by the Hong Kong authorities will officially go live, with Hong Kong dollar stablecoins regarded as legal means of payment, and the exchange between Hong Kong dollar stablecoins and fiat currency will become more convenient and compliant.

1. A rigid requirement for 100% redemption of Hong Kong dollar stablecoins

The Hong Kong (Stablecoin Ordinance) stipulates that issuers of stablecoins must ensure that the stablecoins they issue are backed by sufficient reserve assets, ensuring that the market value of the reserve assets is not less than the nominal value of the issued circulating stablecoins.

Stablecoin issuers should guarantee the right of stablecoin holders to redeem their stablecoins and must not obstruct or restrict the redemption of stablecoins. No fees other than reasonable handling fees should be charged during the redemption of stablecoins.

2. Hong Kong dollar stablecoins meet anti-money laundering, anti-terrorist financing, and other compliance requirements

The Hong Kong (Stablecoin Ordinance) stipulates that issuers of Hong Kong dollar stablecoins must comply with strict anti-money laundering and counter-terrorist financing requirements.

In a consultation document released by the Hong Kong Monetary Authority on May 26, the authority outlined the relevant anti-money laundering and counter-terrorist financing requirements, with core requirements including:

Customer due diligence. For purchases or redemptions that reach or exceed a baseline of 8,000 Hong Kong dollars, customer due diligence must be conducted, including verifying wallet ownership;

Strict regulation of non-custodial wallets. Implement strict monitoring and transaction limits on non-custodial wallet transactions to reduce the risk of wallets being exploited by criminals;

Continuous monitoring. Utilize blockchain analysis to track transaction history and detect illegal activities, reporting suspicious transactions;

Conduct due diligence on custodial wallet providers;

Blacklist illegal wallet addresses.

3. Key points for mainland foreign trade merchants to comply with the use of Hong Kong dollar stablecoins

Considering the current policy differences between the mainland and Hong Kong regarding stablecoins, I believe that mainland foreign trade merchants can avoid most compliance risks by grasping the following three key points when using Hong Kong dollar stablecoins:

Using Hong Kong or other overseas company entities to receive and pay stablecoins;

The compliant exchange of stablecoins with fiat currency is completed in Hong Kong;

Compliant foreign exchange settlement back to the mainland parent company;