The decentralized yield protocol Pendle announces the launch of a new product, Boros, creating a tradable and hedgeable on-chain market for funding rates. This product will allow users to directly participate in the changes of funding rates for assets like BTC and ETH through a simple Long/Short operation model, providing unprecedented interest rate strategy tools for DeFi traders and protocols.

Funding Rate Trading Market - Boros

As a pioneer in on-chain yield trading, Pendle has long been committed to productizing and structuring various cryptocurrency yield products. Following the establishment of PT (fixed yield) and YT (floating yield) markets in V2, the launch of Boros further opens up a brand new yield product - funding rate.

During the trading process between spot and perpetual contracts, the funding rate plays a key role as an incentive mechanism; however, it has long been ineffectively productized or incorporated into on-chain yield strategies. The emergence of Boros is meant to fill this gap.

The YU asset model turns funding rates into tradable commodities

Boros introduces a new asset type called Yield Units (YU), where each unit of YU represents the funding rate yield of the corresponding underlying (such as BTC, ETH) over a fixed period. Users can bet on future changes in funding rates and profit through the following two operations:

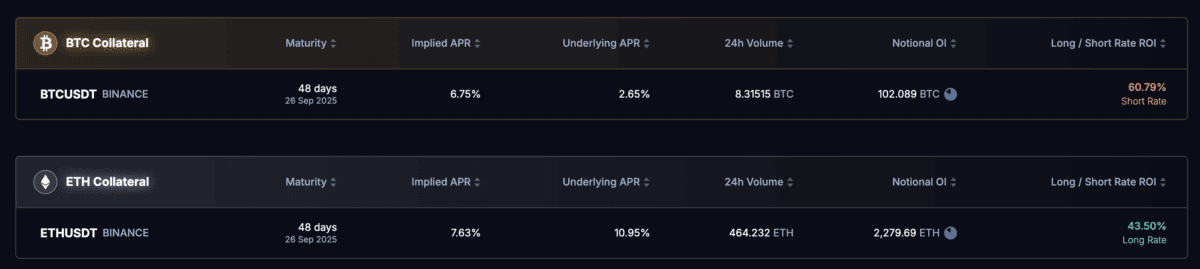

Long YU: Pay a fixed interest rate (Implied APR, priced by the Boros market) and receive the funding rate (Underlying APR, the actual funding rate on the exchange).

Short YU: Receive a fixed interest rate (Implied APR, priced by the Boros market) and pay the funding rate (Underlying APR, the actual funding rate on the exchange).

This design allows users to conduct spread trading or hedging operations based on market expectations. For example, when expecting future funding rates to be higher than the market consensus fixed rate, one can go long on YU to capture the intermediate spread. Currently, the funding rate for Binance's perpetual contracts supporting BTC and ETH is online, with plans to expand to SOL, BNB, and integrate with trading platforms like Hyperliquid and Bybit.

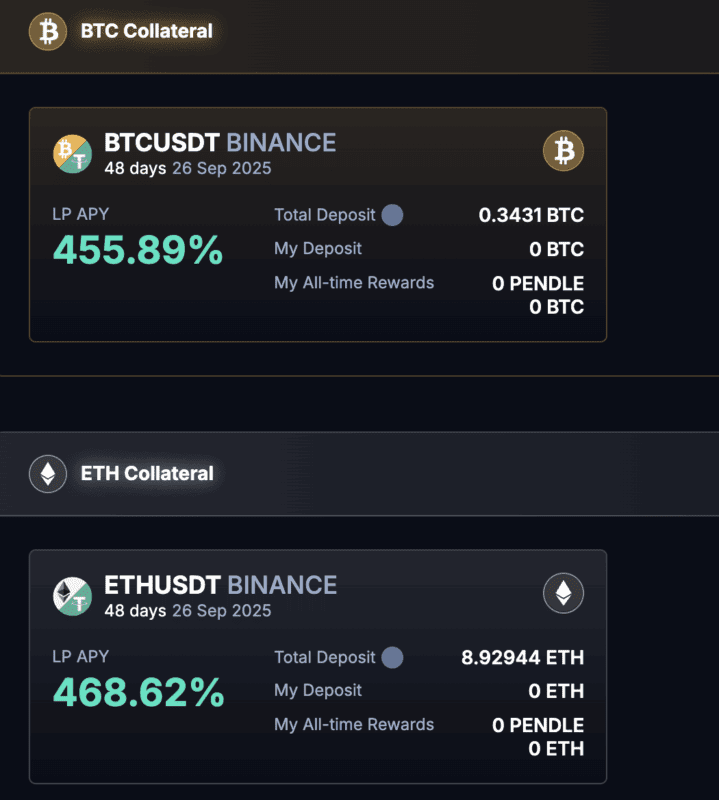

In terms of mechanism design, Boros adopts an order book matching structure and combines it with a vault mechanism to provide initial liquidity, allowing liquidity providers (LPs) to earn fees and PENDLE rewards, but the current vaults are almost at their limits, and subsequent releases will gradually depend on YU trading volume.

Addressing hedging pain points at the protocol level

Addressing hedging pain points at the protocol level

Boros not only provides new tools for retail traders but will also play an important role at the protocol level. Taking the stablecoin protocol Ethena as an example, its TVL has exceeded $9.7 billion, using a delta-neutral strategy to maintain the price of the stablecoin USDe. This strategy requires holding both spot and short perpetual positions simultaneously, and although the price difference has been hedged, it is still exposed to the risk of funding rate fluctuations.

The funding rate hedging tool provided by Boros will enable Ethena to effectively resist the erosion of returns caused by negative funding rates during market downturns.

Pendle's yield sources are expected to expand

If the PT/YT market leans towards savings and allocation-type assets, Boros is a rate product oriented towards trading and hedging. As the source of perpetual contract rates, which has a global daily trading volume exceeding $150 billion, on-chain open trading of funding rates is expected to significantly expand Pendle's use cases and yield sources.

Source