Original author: Animoca Brands

Reprint: Daisy, Mars Finance

● Stablecoins have obtained regulatory legitimacy in the two major economies of China (Hong Kong) and the United States, and ushered in a wave of enthusiasm. Unlike offshore stablecoins, which are mostly used for speculation and informal economies, we believe that onshore stablecoins will mainly focus on two areas: "open source digital wallets" in payments and "open clearinghouses" for inter-agency settlement.

● Digital wallets using stablecoins and blockchains have much lower thresholds than centralized digital wallets in the Web2 era, both in terms of technology and commercial promotion. Technically, stablecoin payments can be completely based on existing blockchain technology, token standards, and crypto wallets. Commercially, consumer platforms such as retailers, e-commerce, and social networks can promote stablecoin payments for their own benefit without coordination, while forming a synergy to promote stablecoins. Based on these two points, stablecoin payments can be considered "open source digital wallets".

● Based on these advantages, stablecoins may form a wave of challenges to the credit card-dominated payment system, and the issuing banks, as the main collectors of transaction fees, will undoubtedly be impacted. At the same time, bank card networks such as Visa and Mastercard and payment terminals such as Stripe will benefit from the increase in 'currency' types in the payment network, thereby consolidating their role in the payment system.

● In terms of fund transfer, stablecoins will be able to play the role of "open clearinghouse". The interbank settlement of stablecoin deposits and withdrawals and on-chain transfers is architecturally very similar to traditional interbank transfers conducted by clearing houses. At the same time, the stablecoin-based system can further improve real-time performance, scalability, and cross-regional performance. The inefficiency of cross-border settlement for a long time is precisely because of the lack of the role of international clearing houses. Therefore, stablecoins, as an open cross-regional clearing service, are crucial to solving the inefficiency of cross-border transfers.

● Existing money transfer operators, such as Wise and Airwallex, improve remittance efficiency by acting as cross-border clearing houses. Operators bridge their own ledgers and fund pools in various countries with banks in various countries, avoiding actual cross-border fund transfers. However, if banks achieve the same efficiency through stablecoin clearing, this model may face challenges. On the other hand, it should also be noted that not all blockchain companies' remittance solutions actually use the core capabilities of stablecoins. For example, cross-border transfers through centralized cryptocurrency exchanges only involve the exchange's internal ledger and do not involve blockchain transactions, so they should be regarded as money transfer operator businesses rather than stablecoin-based solutions.

Stablecoins Going Mainstream

In the past two months, stablecoins have completed relevant legislation in the world's largest economies, the United States and China (through Hong Kong). The completion of these legislations marks the transformation of stablecoins from a tool mainly used in the virtual currency community to a new financial technology innovation recognized by the mainstream economy.

In the United States, on July 18, the "GENIUS Act" was officially signed, clarifying the path for compliant use of stablecoins. In the past few months, the bill has been gradually reviewed and discussed by the Senate and the House of Representatives. As the possibility of the bill's passage continues to increase, various institutions and large enterprises have begun to participate in the issuance and use of stablecoins, such as:

● Payment service providers begin to support stablecoins: Stripe, Visa, Shopify, PayPal, etc.

● Social media and e-commerce platforms are considering adopting stablecoin payments: Meta, Amazon, Walmart, etc.

● The four major banks in the United States plan to form an alliance to issue stablecoins: including JPMorgan Chase Bank, Bank of America, Wells Fargo Bank, and Citigroup.

Hong Kong also passed the (Stablecoin Ordinance) in May 2025 and came into effect on August 1, 2025. This indicates that Hong Kong, as China's financial gateway, is open to stablecoin-related financial activities. In addition to the Hong Kong dollar, the bill also allows licensed issuers to issue stablecoins of other currencies, so the impact on international currency circulation is far greater than that of Hong Kong. Interestingly, the type of institution that responds most actively to this opportunity is very similar to that in the United States, including:

● Payment service providers: Ant Financial (including Ant International and Ant Digital Technology), LianLian International, etc.

● E-commerce platforms: JD Digits plans to launch a stablecoin, while Alibaba can do so through Ant Financial.

● Large banks: Standard Chartered Bank plans to apply for the issuance of stablecoins through a joint venture with Animoca Brands and Hong Kong Telecom.

In this context, this article aims to provide readers with a framework to understand the main scenarios in which onshore stablecoins can play a role in the economy, and explain the main purposes of the above-mentioned institutions. We will divide the discussion into two main application categories:

● Payment, that is, the consumer pays the merchant

● Transfer, that is, the remitter transfers money to the payee across banks

Strictly speaking, payment can also be a type of transfer. We discuss these two use cases separately because the existing mainstream solutions for implementing non-cash payments and transfers are different, and therefore have different pain points. The former mainly uses credit card payments supported by card networks, while the latter mainly uses bank transfers. In the following, we will discuss the main problems of existing solutions, existing alternatives, and new opportunities brought by stablecoins.

Payment

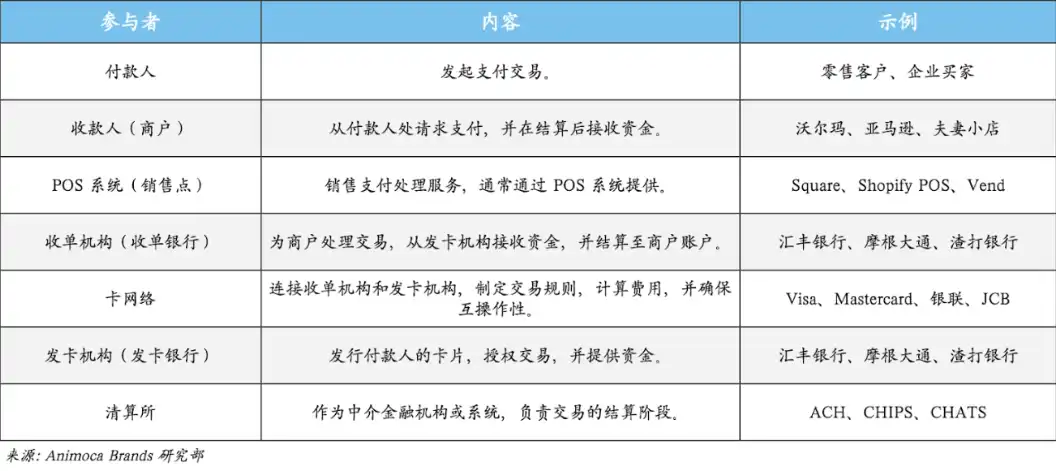

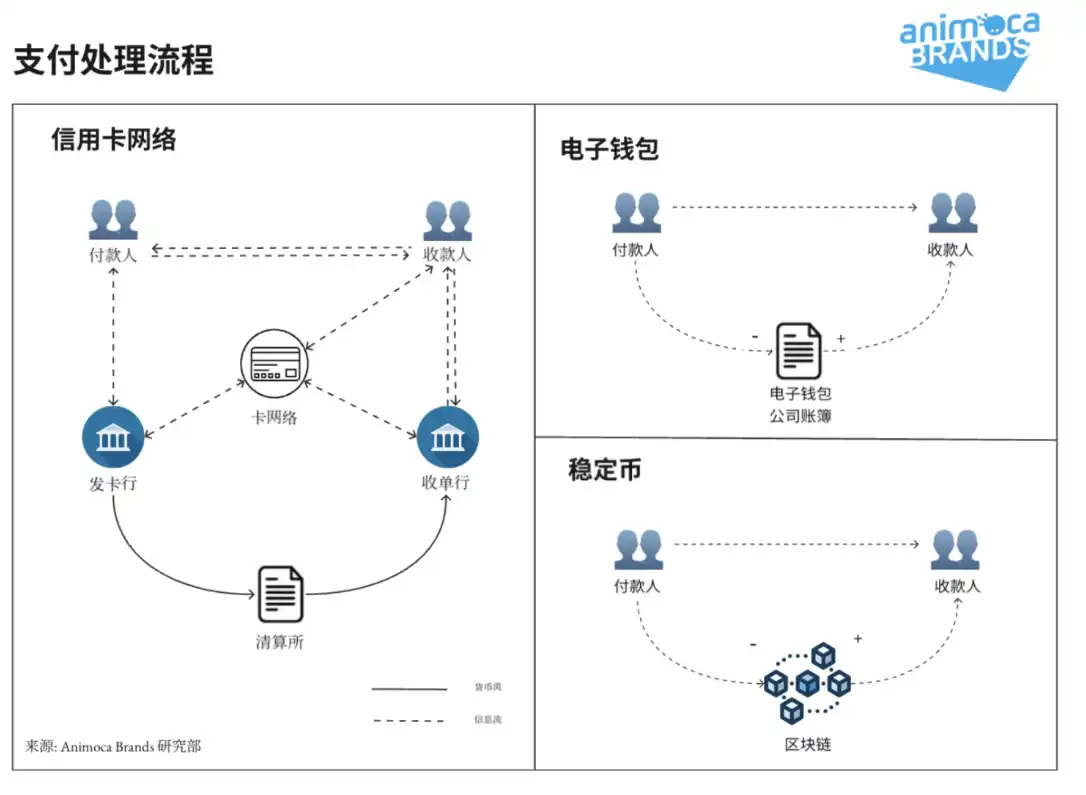

Cash and credit cards are still the most important payment methods in most regions. Among them, credit card transactions, as the main non-cash option, are processed through bank card networks such as VISA and Mastercard (hereinafter referred to as card networks). Payments implemented through card networks roughly have the following steps:

1. Merchant initiates: The merchant requests payment information from the customer through its POS terminal, and the customer provides it by swiping a card offline or filling in credit card information online.

2. Request Authorization: The POS system selects the corresponding card network based on the information provided by the customer, and sends a payment authorization request to the issuing bank through the network.

3. Approve authorization: The issuing bank approves the transaction after verifying the customer's balance or credit line. This confirmation information returns to the POS terminal through the card network, and finally returns to the customer for confirmation to complete the payment authorization.

4. Clearing and Settlement: For authorized payments, the PoS terminal initiates the clearing and settlement process with the acquiring institution (such as the bank used by the merchant). The acquiring institution sends the total amount of money to be collected in batches to the issuing institution through the card network. The issuing bank then completes the settlement through the traditional interbank transfer route.

5. Foreign exchange transactions: In the case of transactions involving foreign currencies, the issuing bank will conduct currency exchange and complete settlement through SWIFT transfers and other methods.

In this process, the card network plays the role of an information transmission layer to ensure that the financial service providers used by customers and merchants, no matter how different they are, can complete communication and clearing.

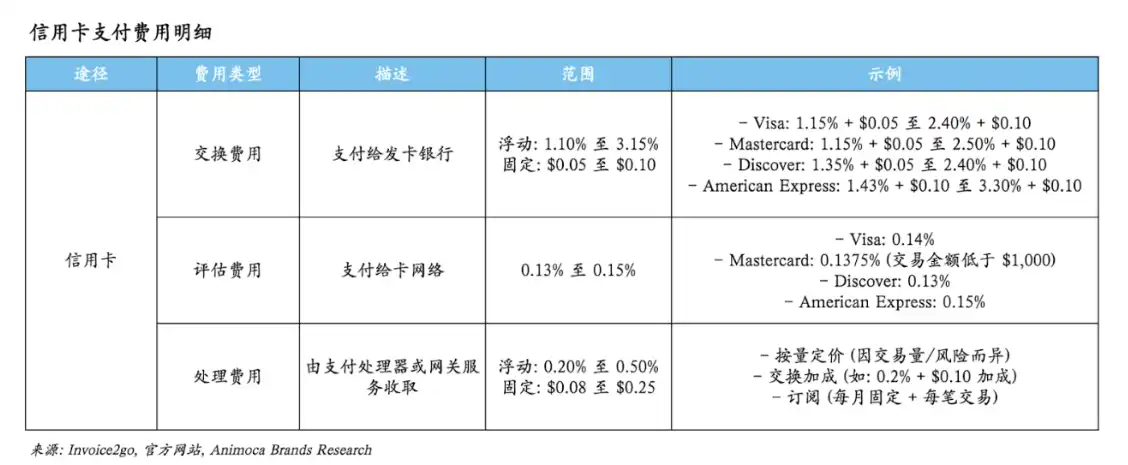

On the one hand, the existence of credit cards and card networks greatly improves the convenience of non-cash payments, but at the same time, it is often criticized for its high transaction fees. Each credit card transaction automatically deducts 2-3% or more from the amount paid by the customer as a handling fee. This fee is a heavy burden for low-profit companies.

However, upon closer inspection, the card network itself is not the main cause of high handling fees. Credit card transaction fees can be roughly divided into three parts: the 'assessment fee' paid to the bank card network, the 'processing fee' of the point of sale, and the 'interchange fee' to the issuing bank. Among these three, the card network charges the least, only 0.15% of the transaction. For example, Visa processes US$16 trillion in transactions a year, and its annual revenue only accounts for 0.2% of the total transaction volume. The bulk of the transaction fee is the interchange fee (1-3%) to the issuing bank. This fee is mainly used to cover the costs and risks of the bank providing services, such as credit default risk and consumer protection. For consumers who need to use credit, this rate is not excessive. For issuing banks, as a credit business with default risk, the 2% fee precisely shows the professionalism of bank risk management, not inefficiency.

So the key to the credit card fee problem is not that the fees are high, but that consumers use it as the default option, and they will give priority to swiping their credit cards instead of other options regardless of whether they need a credit line. The root cause of this consumer preference is the mismatch between the party choosing the payment method and the party bearing the fees: the consumer chooses the payment method, and the merchant bears the transaction fees. This mismatch gives the issuing bank room to maneuver, that is, it can use part of the fees to 'bribe' consumers with rewards and points in exchange for consumer preference. This strategy is very effective, and a large number of consumers will prefer credit cards with better cashback and point benefits over debit cards, cash, or digital wallets without points but lower transaction fees, even if they do not need credit consumption.

In addition to high transaction fees, card networks also incur high cross-border fees for cross-border payments, further increasing transaction costs. The root cause of this problem is that the settlement between the issuing bank and the acquiring bank depends on traditional interbank routes. We will discuss the topic of cross-border settlement in the transfer section.

From the above discussion, we can roughly understand the attitudes of various parties involved in the payment system towards stablecoins:

1. Merchants are the most pained in the credit card system, so they have the strongest motivation to find alternatives. Companies like Walmart, Amazon, and JD.com have shown strong interest in stablecoin payments as an alternative due to their extensive sales networks.

2. Card networks such as Visa and Mastercard themselves do not account for a high proportion of transaction fees, and can support various currencies, including stablecoins. Therefore, the card network itself is not the opposite of stablecoins. On the contrary, as more stablecoins enter daily transactions, the card network may become more important because of its bridging function. In addition, with stablecoins, the settlement process of the payment network can be simplified, allowing card networks to further participate in settlement, thereby playing a larger role in the entire payment process. Visa has already demonstrated the potential of cross-border settlement with issuers through stablecoins as early as 2021.

3. Terminal (POS) solution providers can expand their product lines by supporting new payment methods. Stablecoins will not only subvert their current role, but also allow terminal solution providers to enter services such as acquiring and deposit and withdrawal. Stripe's acquisition of Bridge and Priv (wallet services) provides a footnote to this trend.

"Open Source Digital Wallet" based on stablecoin

Digital wallets were first launched by PayPal in the United States, and after many years, they have successfully occupied a dominant position in payments in China and many developing countries in Southeast Asia and Africa. Compared with bank card payments, digital wallets have many advantages, such as:

● Registering a digital wallet is much easier than opening a bank account. Users only need to complete online registration like registering a website to start using a digital wallet. Some digital wallet services provide offline channels for recharge or withdrawal.

● As a Web2 product, digital wallets are naturally compatible with online transactions, which has made their application scenarios grow rapidly in the mobile phone era, and gradually expand to offline merchants.

● Because there are fewer participating nodes in the payment process, the cost of digital wallet transactions is cheaper than those based on card networks. For example, Alipay charges merchants 0.6%, and peer-to-peer transfers between users are free.

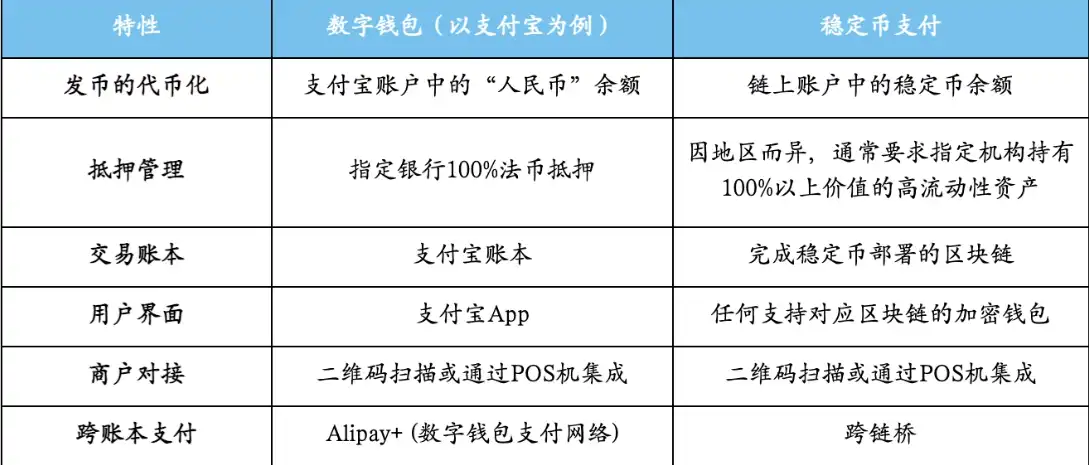

Stablecoin payments have many similarities to digital wallets, so they can be considered a new form of digital wallet service. Similarities include:

● The 'funds' in the wallet account are tokenized representations of fiat currency on the ledger, and 100% collateral must be maintained in accordance with regulatory requirements.

● Payment between digital wallets is a transaction record on the ledger. However, the digital wallet transaction record is on the company's own ledger (such as Alipay), while the stablecoin payment is recorded on the decentralized blockchain ledger.

● In terms of the user interface, the user interface and interaction methods of digital wallets and digital currency wallets are basically the same, such as supporting functions such as 'scan code payment' and 'payment code'.

At the same time, stablecoin payment is a more open "open source digital wallet" than Web2 products due to its decentralized architecture, for example:

● The issuance of stablecoins, that is, providing compliance, collateral and contract deployment, can come from multiple institutions, such as Tether, Circle, etc.

● Stablecoin deposits and withdrawals are provided by independent licensed institutions, such as Transak.

● The ledgers of stablecoin transactions can use different blockchains, such as Ethereum, Solana, TON, etc.

● Users can use any wallet that supports these blockchains to pay and receive payments.

● Cross-(wallet) ledger payments can be handled through a variety of on-chain cross-chain protocols, such as LayerZero.

Therefore, in the process of popularizing stablecoin payments, on the one hand, it can learn from the successful strategies of digital wallets. At the same time, it can enter fields that digital wallets could not conquer before through its more open characteristics. such as:

● Occupy consumer scenarios: Digital wallets attract a large number of customers by targeting applications with a large user base and consumer demand. Such as Alipay (e-commerce), WeChat Pay (social), Grab Pay (ride-hailing), and public transportation payments such as Suica, EasyCard, and Octopus. Stablecoin payments are likely to follow a similar path.

● Opportunities in Developed Economies: Stablecoin payments provide developed economies such as the United States with another opportunity to challenge the dominance of credit cards. The open source nature of stablecoins allows merchants, stablecoin issuers, blockchain operators, cryptocurrency wallets, and payment service providers to work independently in the stablecoin track without coordination, and can form a joint force. This method will be much more powerful than promoting a single digital wallet service (such as PayPal). Considering that 28% of the US population already owns cryptocurrencies, once major consumer platforms start supporting stablecoins, the user base will grow rapidly.

● Financial inclusion: Digital wallets have promoted financial inclusion by realizing the conversion from cash to online payment and providing deposit and loan transfers and other services to people with insufficient banking services. As an open source digital wallet, stablecoins can further continue this trend by lowering the technical threshold. Payment service providers in various countries do not need to carry out in-depth technical development, but only need to graft the local stablecoin onto the existing blockchain infrastructure and applications.

● Advantages in marketing: Stablecoin payments will require a lot of promotion. This includes persuading merchants to accept new payment methods, upgrading point-of-sale (PoS) systems, and attracting users through incentives (such as discounts, rewards, etc.). In this regard, stablecoins, because their circulation can generate interest through collateral, provide the necessary funds for marketing activities.

● Card networks are still important: The popularity of digital wallets does not eliminate the need for intermediate networks for transactions. For example, digital wallets still rely on Alipay+ to connect merchants with different wallets; the Octopus App supports payment via UnionPay PoS, etc. Stablecoins will also need support from various payment networks. Existing payment infrastructure (such as Visa, Stripe, etc.) can expand its service scope by adding support for stablecoins. For example, Stripe has acquired a number of crypto services to support the growing needs of merchants. And Visa has also made it clear its vision to support digital currencies.

● On-chain payment network: The on-chain part of stablecoin payments will also need routing and exchange services to support payments between stablecoins of different issuers, or the same stablecoin on different blockchains. Circle's CPN (Circle Payment Network) is already able to implement cross-chain routing and settlement for its own USDC. Further development of this requirement will be a new opportunity for traditional networks and on-chain native protocols.

Transfer

Interbank transfer is one of the cornerstones of the modern economy. Even if digital wallets can handle a large number of small transfers between individuals, most fund transfers still occur through banks. Due to its importance, each country and region will establish the necessary infrastructure (such as clearing houses) to allow internal transfers to be carried out effectively. However, cross-border transfers are still relatively inefficient due to the lack of clearing houses between countries. The SWIFT message network, established in the 1970s, is still the cornerstone of cross-border interbank transfers 50 years later.

Domestic Transfers

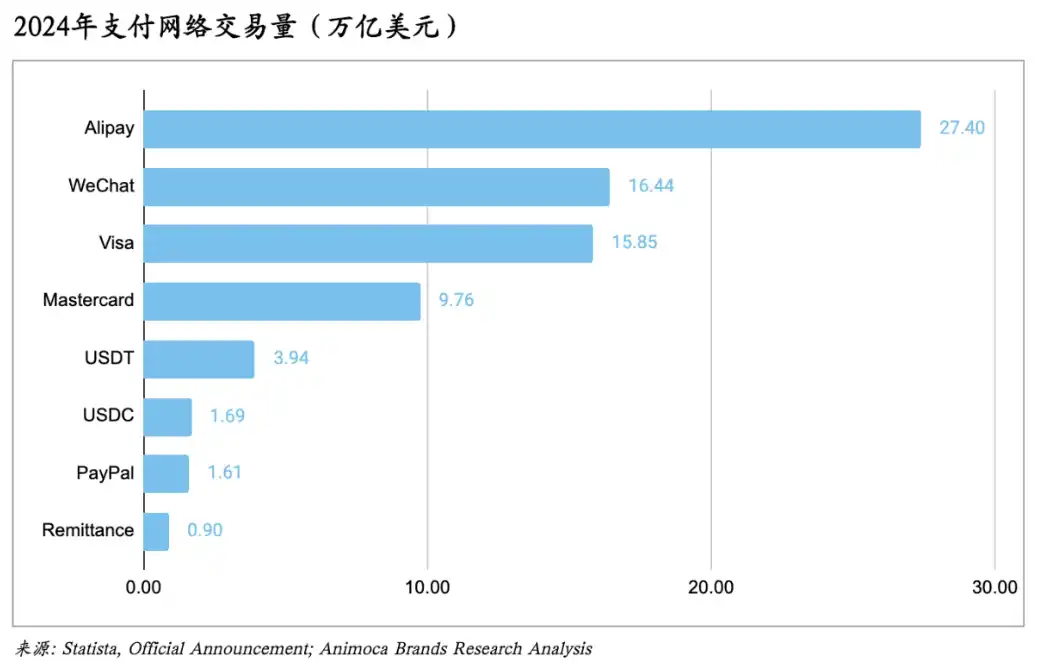

Internal transfer is the most important form of fund flow. In 2024, China's domestic payment system processed 12.45 trillion yuan (approximately 1.8 trillion US dollars) in transfers. At the same time, the amount processed domestically in the United States is also comparable.

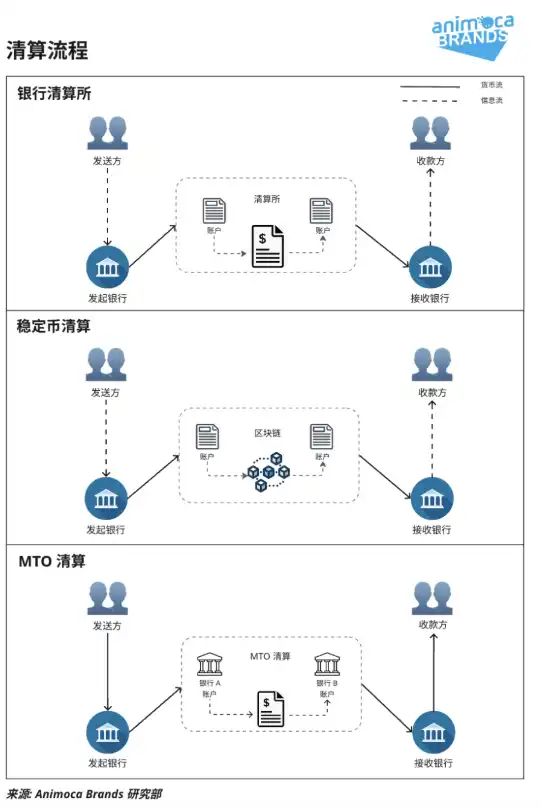

These interbank transfers are usually implemented through clearinghouse services provided by central banks or banking associations. Under the clearinghouse architecture, banks do not need to settle directly between each other, but instead participate by opening accounts in the clearinghouse, and realize the transfer through transactions on the clearinghouse ledger. In this process, there is no direct flow of funds between banks, but only deposits and withdrawals between banks and the clearinghouse. Taking the systems of the United States and China as examples:

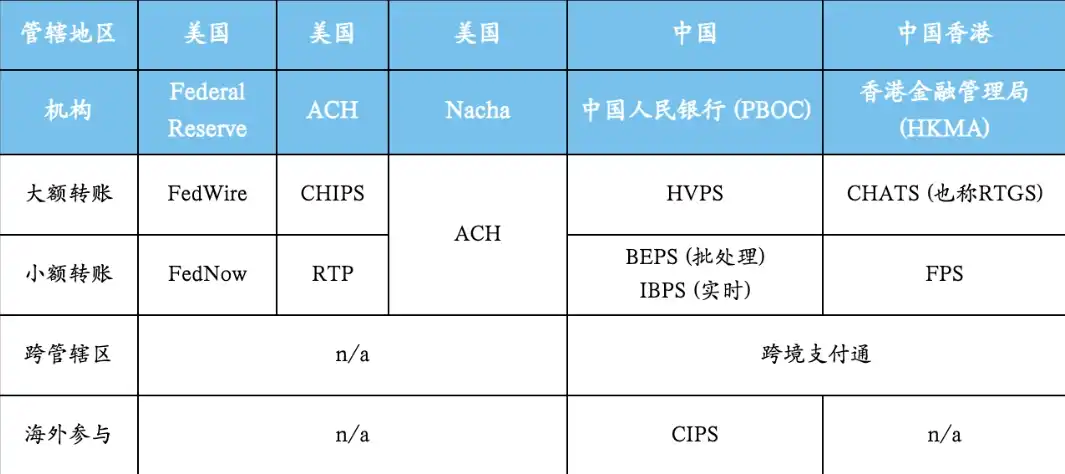

Banks in the United States use multiple clearing services. The Federal Reserve provides FedWire and FedNow for large and small transfers. The Clearing House Association provides CHIPS and RTP as parallel products. In addition, the ACH system, which has been in existence for more than 50 years and is managed by Nacha (a non-profit banking association organization), is still used by most banks in the United States due to its compatibility with old systems.

Chinese banks rely on the clearing system provided by the People's Bank of China, including HVPS, BEPS, and IBPS, to manage transfers of different sizes and time requirements. In Hong Kong, the Hong Kong Monetary Authority provides CHATS (Clearing House Automated Transfer System) for large interbank transfers, and FPS (Faster Payment System) for instant fund transfers. Just this year, "Cross-border Payment Pass" was launched, connecting the People's Bank of China IBPS and the Hong Kong Monetary Authority FPS to realize instant fund transfers between mainland China and Hong Kong, as well as the exchange between Hong Kong dollars and RMB.

In addition, the People's Bank of China also provides CIPS (Cross-border Interbank Payment System) for offshore RMB (ie CNH) transactions. Through CIPS, overseas banks can directly transfer RMB to banks in China or other overseas CIPS participants without relying on the SWIFT system. In contrast, cross-border US dollar transfers are mainly implemented through CHIPs, which can only be cleared in New York. All cross-border US dollar transfers require each bank to first transfer US dollars to its New York branch through internal and external transfers before subsequent operations can be performed.

It can be seen from the above analysis that the existing clearing system can cover a wide range of transfer application scenarios, but it still has its limitations:

● System fragmentation: It is not easy to maintain old systems and coordinate across banks, resulting in the coexistence of multiple clearing services.

● Access threshold: Clearing houses are usually limited to banks in a country and only support local legal currencies. This is obviously not enough for currencies that need global circulation.

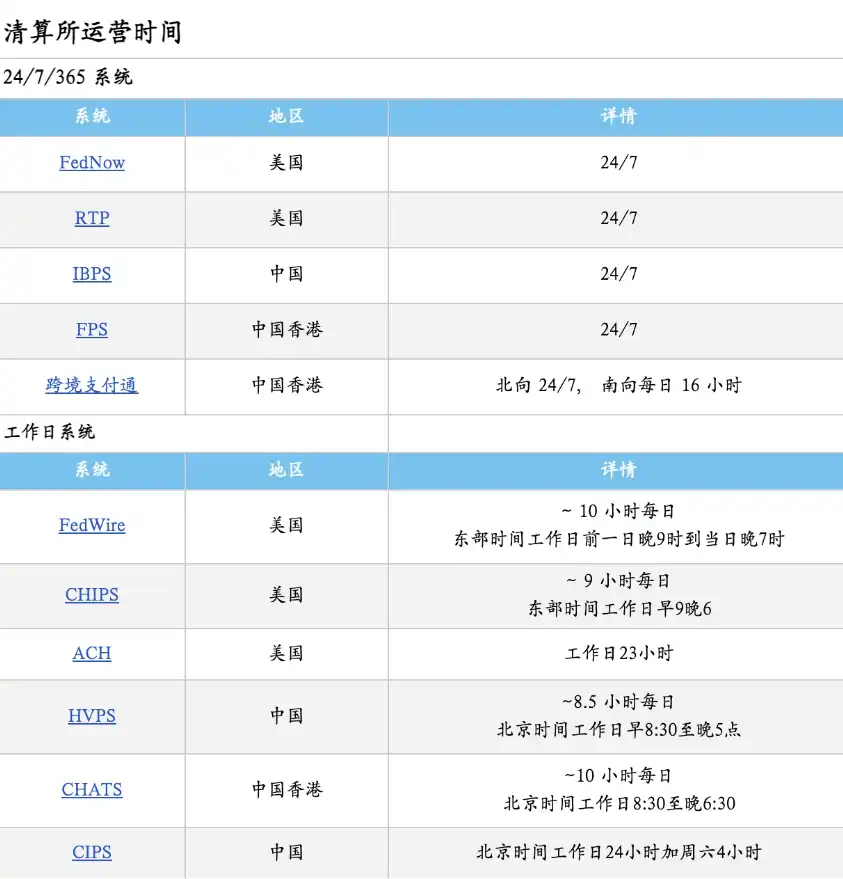

● System availability: Many clearing systems do not support 24/7/365. Services are usually closed on weekends and evenings. Even a 24/7 system still needs time for system maintenance and upgrades.

● Cost and Speed: Most clearing services are batch processing, which requires a trade-off between cost and time.

"Open Clearinghouse" based on stablecoins Stablecoins can improve transfer efficiency in two ways. One is the digital wallet transfer mentioned earlier, which is mainly for small transfers between users. The other is to provide "open clearinghouse" services in interbank transfers. Let us elaborate on the term "open clearinghouse".

Transactions via stablecoins have many similarities to clearinghouse processes. As shown in the flowchart, in a clearinghouse architecture, banks create accounts and deposit funds on the clearinghouse's books. Settlement between banks then becomes a transaction on the clearinghouse ledger. In contrast, clearing through stablecoins is equivalent to banks establishing on-chain accounts and 'depositing' into stablecoins. Bank-to-bank transfers also become transactions on the blockchain ledger. In this way, interbank payments implemented through stablecoins can be seen as a clearing service provided by blockchain and stablecoins.

At the same time, the clearing service implemented through stablecoins is more open than traditional clearinghouses. Stablecoin clearing can be implemented between banks in a self-organized manner, without being restricted by jurisdiction or the currency used. At the same time, stablecoin clearing can be connected to various DeFi functions of the blockchain to continuously expand clearing-related functions.

With a stablecoin "open clearinghouse", the interbank transfer process can be improved in many ways:

● Cost: Traditional clearing services generate high fees. For example, FedWire charges $0.2 per transaction, while FedNow charges an average of approximately $0.045 per transaction. This is not a small number under large-scale applications. In comparison, stablecoin transfer fees on most blockchains are usually less than $0.01.

● Speed: On-chain transfers are defaulted to real-time settlement, and the processing speed is only limited by the block generation time. The generation time of various blockchains is different, but it is generally 0.1 to 10 seconds. ● Availability: The main public chains are available 24/7 by default, and there is no need to shut down for maintenance.

● Access: The main public chains do not require permission, which means that clearing services are no longer restricted by country and currency. As more fiat currencies are added to the

chain, the types of currencies supported can be continuously expanded.

● Function Expansion: Traditional clearinghouses are usually managed by central banks or banking associations, and functional decisions are made in a top-down manner. This leads to new functions often prioritizing commonly used functions, and decision-making is slow. In contrast, the blockchain is naturally open to the functions required by banks, which is equivalent to adding an 'app store' to the clearing service.

The role of stablecoins as an 'open clearinghouse' may be one of the main motivations for the four major banks in the United States to explore stablecoins. First movers can have a first-mover advantage in setting standards (such as choosing blockchains and stablecoin types). In addition, given the huge influence of these banks in the US dollar ecosystem, their actions will affect the direction of subsequent innovation in this system. Considering the global role of the US dollar, this dominant advantage will transcend the United States to influence the world.

Cross-border Transfers

Cross-border transfers, or cross-border remittances, are smaller in scale compared to domestic transfers, but are often criticized for their high costs (approximately 5-6% of the transaction value), long duration (approximately 5-7 business days), and unpredictable results (transfers may fail for no reason).

As mentioned earlier, the root cause of this inefficiency is the lack of cross-border clearinghouse services. This means that there is a missing link in the two key functions of fund transfer:

1. Communication, that is, the remitting bank notifies the receiving bank of the transfer information.

2. Settlement, that is, the transfer of funds from the remitting bank to the receiving bank.

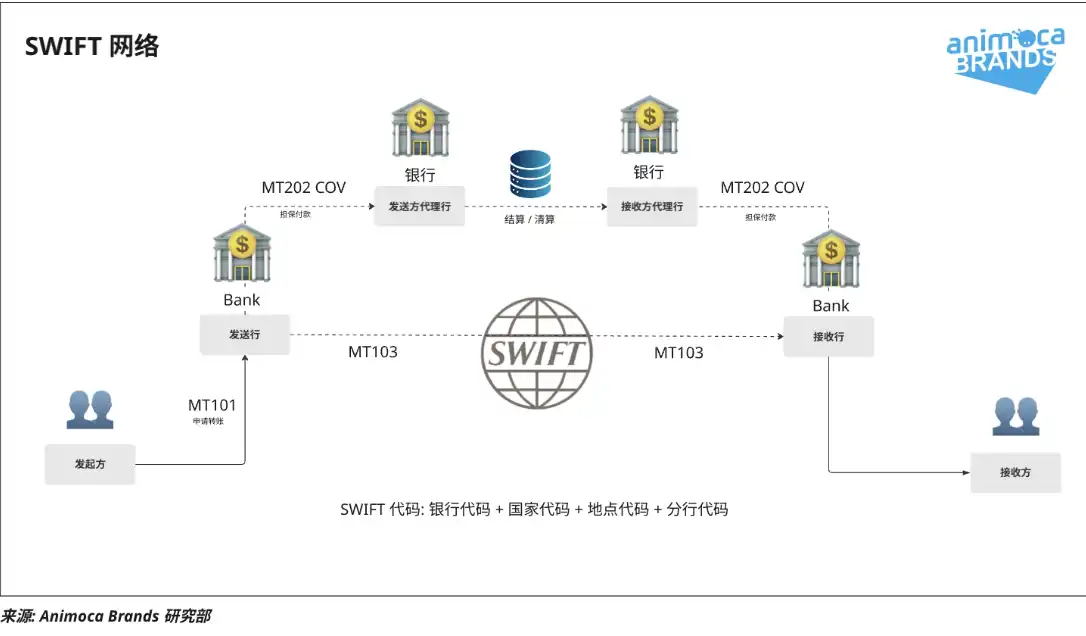

In the absence of clearing services, the existing mainstream solution is wire transfer, also called SWIFT transfer. This method implements the above two functions separately:

● Communication: SWIFT handles interbank communication, transmitting transfer requests between the remitting bank, the receiving bank, and the intermediary bank.

● Settlement: Rely on interbank transfers, which use internal bank transfers and domestic clearing services in various countries to achieve this (for example, US dollars pass through CHIPs).

Taking a US dollar transfer from Hong Kong to Brazil as an example, the general steps are:

1. Send a message: The bank in Hong Kong sends a SWIFT message to the bank in Brazil, notifying it of the transfer information.

2. Choose a route: The remitting bank in Hong Kong chooses a settlement route and sends a SWIFT message to the intermediary bank.

3. Fund settlement:

-The remitting bank transfers US dollars from its Hong Kong branch to its New York branch through internal settlement.

-The New York branch sends funds to the receiving bank's New York branch through CHIPS.

-The receiving bank transfers funds to Brazil through internal settlement.

Even in this simple case, because each step requires daily settlement and each transfer point generates handling fees, the entire process takes 3-5 business days, and the fees accumulate at each transfer point.

This transfer can become more complicated with the addition of other factors, such as:

● Use local currency: If the recipient in Brazil only accepts Brazilian Reais, and the remitter only has Hong Kong dollars, the remitter must first convert Hong Kong dollars into US dollars to use the above-mentioned fund transfer route, and then convert them into Brazilian Reais at a Brazilian bank.

● Small banks: Banks without New York branches need to transfer through a large bank with US dollar processing capabilities, which will further increase steps and costs.

烫染, In the traditional clearinghouse model, a country can also accept non-local banks to participate in the cross-border clearing of currencies by setting up overseas clearing banks (such as CIPS for RMB transfers), but these efforts are still limited by a single currency and a slow expansion process from top to bottom. For example, the vast majority (73%) of offshore RMB transfers still rely on Hong Kong (equivalent to CHIPs through New York), and they still often use SWIFT rather than relying purely on CIPS.

Money Transfer Operators: Existing cross-level payment improvement methods

Money Transfer Operators (MTOs) are one of the innovative methods to solve the inefficiency of cross-border transfers. MTOs are widely used in international e-commerce and personal remittances. Companies such as Western Union, Wise, and Airwallex are well-known brands in their respective regions and customer groups.

The role of the MTO is similar to a user-run multinational clearing house. The remitter transfers the local currency to the MTO's local bank account and notifies the MTO, thereby 'depositing' into the MTO's ledger. Next, the MTO calculates the corresponding amount of the recipient's currency, and pays the corresponding amount from the bank account in the recipient's country to the recipient's local account, completing the 'withdrawal'.

This method can improve efficiency because it actually avoids real cross-border funds. The 'cross-border' part of each transaction is only recorded on the MTO's ledger, and then operated through the MTO's accounts in the remitter and payee countries. Therefore, the main cost of MTO is not related to cross-border, but mainly to maintaining its service area's fund pool. For regions with balanced fund flows (for example, between Singapore and Hong Kong), the liquidity pool is basically balanced and does not require much maintenance. When the liquidity pool is unbalanced (for example, from the United States to Mexico), MTO reduces the cost of transferring per amount through bulk transfers and currency exchanges.

However, despite their high efficiency, MTOs still only handle a small fraction of the total cross-border transfer volume. Leading MTOs such as Wise or Airwallex process less than $200 billion in transactions annually, generating approximately $1 billion in revenue. It is also reported that the entire MTO industry has annual revenue of $42 billion, so we estimate that MTO transfers account for approximately 3-5% of total cross-border remittances.

Several factors may have contributed to MTOs not dominating the cross-border transfer market:

● Large organizations usually prefer bank transfers for security reasons.

● Traditional wire transfer networks provide broader coverage, while MTOs typically only support popular destinations and currencies.

● Limited liquidity pool size may limit MTOs from processing large transfers.

In addition, MTOs also incur additional operating costs, such as maintaining retail stores or public sales teams, which banks can amortize in their broader service offerings.

It is worth noting that cross-border transfers through cryptocurrency exchanges (such as Bitso) are more based on the MTO model, that is, the core transfer occurs on the exchange's own ledger, rather than using the blockchain transfer capabilities of cryptocurrencies. The remitter deposits US dollars into the cryptocurrency exchange account, sends stablecoins to the recipient's exchange account, and then withdraws them to the recipient's local bank account. In this process, the cryptocurrency exchange only updates its centralized ledger and manages deposits and withdrawals with local bank accounts. The existence of cryptocurrencies is mainly to provide an alternative way to fund accounts, rather than as part of the underlying transfer mechanism.

Stablecoins for Cross-Border Transfers: A New Way to Integrate MTOs and Banks

Stablecoins can integrate the MTO model into bank cross-border transfers. As mentioned earlier, stablecoins support the establishment of an 'open clearinghouse' that transcends geographical restrictions and enables direct single-currency transfers between any bank. For example, a US dollar transfer from Hong Kong to Brazil requires a three-stage relay by wire transfer, but can now be achieved through a direct on-chain stablecoin transfer between two banks, taking only a few seconds and costing less than US$1.

For transfers that require currency exchange (for example, Hong Kong dollars to Brazilian Reais), a simple solution is to first exchange Hong Kong dollars to US dollars or RMB for stablecoin cross-border settlement. Then convert to Reais after local withdrawal. This model is already a significant improvement compared to wire transfers. A better cross-border transfer method is to integrate currency exchange into the 'open clearinghouse'. Once Hong Kong dollars and Brazilian Reais have their own stablecoins, banks only need to deposit and withdraw blockchain funds in local currency, and the exchange between Hong Kong dollars and Brazilian Reais can be exchanged through on-chain transaction fund pools. In this way, banks do not need to have currency exchange capabilities to participate in cross-border transfers, thereby expanding the range of participating banks. Of course, this model requires all participating currencies to be compliant stablecoins accepted by various countries, and the arrival of this day remains to be seen.

It is worth noting that SWIFT, as the most widely accepted communication platform among global banks, will still be able to play a key role in cross-border transfers. Although stablecoins can greatly improve the settlement process, transaction initiation still requires a shared platform to communicate transfer details. Just as card networks will continue to exist and stabilize coin payments, SWIFT can still play its role in interbank communication in the stablecoin world.

What will happen to banks after stablecoins?

The "open source digital wallet" implemented through stablecoins may take away some of the retail business of banks. For the credit card market mainly issued by banks, a shift in market preference to stablecoin payments may reduce the use of credit cards, thereby reducing the income banks obtain through issuing cards. This may prompt banks to shift from issuing credit cards to providing consumer credit and consumer protection services by integrating with retailers or wallet applications. In addition, personal deposits may appear on the chain more in the form of stablecoins rather than bank account balances, which will prompt banks to find other new ways to attract deposits, such as on-chain custody or RWA.

At the same time, bank infrastructure still has its advantages. For example, central bank-backed clearing houses provide ample liquidity for large instant settlements. In contrast, stablecoin transfers require pre-funding on-chain accounts, so traditional clearing houses may still have an advantage in terms of capital efficiency for large transfers. In addition, key bank capabilities, such as lending, combined with their strong risk control capabilities, are still indispensable for the modern economy. Finally, banks can still be the gateway for users to obtain more financial and property services.

A possible change is that banks will gradually move their capabilities on-chain, whether through the transformation of the banks themselves or the emergence of new banks, just as banks transferred their businesses from branches to online banking in the Internet era. Users' bank accounts may evolve into on-chain IDs, and banks will only act as on-chain asset custodians. The wealth management products recommended by banks can also be transformed from funds and wealth management to tokenized real-world assets (RWA). Similarly, lending services may be integrated into on-chain DeFi and add bank risk control and compliance capabilities.

In the end, the modern financial system is built around banks. The central bank is responsible for creating money, and commercial banks distribute money under supervision and amplify the money supply. Stablecoins bring new possibilities for carrying out banking services, forcing banks to adapt to new business models. Banks that cannot keep up with the trend may be eliminated, but the banking industry as a whole will still play an important role in the world.

Conclusion

This article mainly focuses on the main scenarios and potential of onshore use of stablecoins when regulatory regulations have been established in major economies. There are many other topics about stablecoins, such as on-chain native stablecoins, interest-bearing stablecoins, other competitors of stablecoins (such as central bank digital currencies CBDC or tokenized deposits), and the political appeals behind promoting stablecoins. We will discuss these topics in future articles.