Ripple is causing controversy by applying to establish Ripple National Trust Bank (RNTB) to issue and manage the RLUSD stablecoin.

The American Community Bankers Association (ICBA), representing about 5,000 local banks, has officially opposed, claiming that Ripple is intentionally acting as a deposit-taking bank, which is prohibited for trust banks.

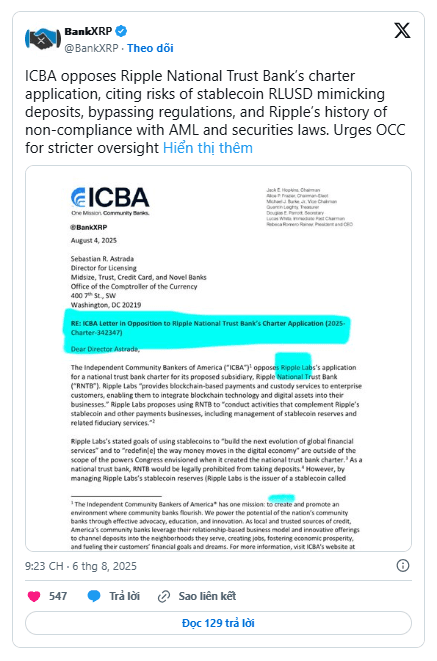

The ICBA warns:

"Ripple and RNTB appear to be recreating deposit-taking functions without having a full banking license."

Legal Risks and Threats to the Financial System

The ICBA criticizes Ripple for exploiting trust bank licenses to evade the strict regulations applicable to traditional banks, especially when the RLUSD stablecoin can be converted to dollars, facilitate payments and transactions, similar to deposits. The ICBA emphasizes:

"The OCC should not allow stablecoin issuers like Ripple to enjoy full banking powers without corresponding obligations."

Additionally, the ICBA believes that the OCC violated rulemaking procedures when it expanded trust bank authority to include stablecoin issuance, which is not part of traditional fiduciary roles.

History of Risks and Hidden Consequences

In addition to legal concerns, the ICBA also highlighted risks related to digital assets such as fraud, money laundering, and cybercrime – particularly dangerous as RNTB takes on the role of custodianship of digital assets.

The organization reiterated that Ripple was previously fined $125 million for securities violations and has a history of violating anti-money laundering regulations. The ICBA warns:

"Licensing RNTB would undermine financial stability by allowing a non-traditional organization to provide deposit-like services without full oversight."

Although Ripple claims it wants to modernize the financial industry, the ICBA believes that the potential benefits are not enough to offset the risks if strict oversight is lacking.