Written by: Yue Xiaoyu

Circle's listing has ignited market attention towards stablecoins, making Circle the first stock of a compliant stablecoin, but behind the glamour also lies a crisis.

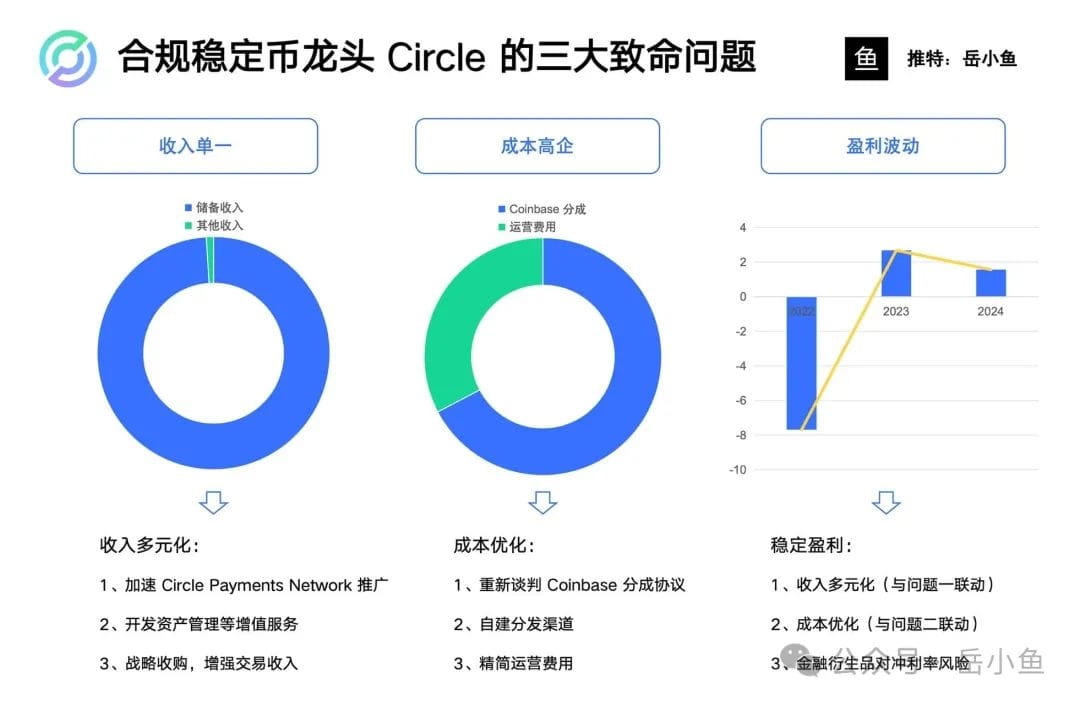

After reviewing Circle's IPO prospectus, we can actually identify three major critical issues for Circle:

Firstly, the single revenue stream, with 99% coming from reserve income and only 1% from other sources;

Secondly, high costs, with 60% of revenue going to Coinbase and a net profit margin of only 9%;

Thirdly, profit fluctuations and instability; a net loss of $770 million in 2022, a profit of $267 million in 2023, and then a drop back to $160 million in 2024.

Let's look at the causes behind these three major issues, as well as the efforts Circle is making to address them.

1. Single Revenue

99% of revenue comes from reserve income, which means Circle has no other profit points, a very obvious "valuation ceiling" for a company.

Let's first look at this core business model:

The USDC issued by Circle is a stablecoin pegged to the US dollar at a 1:1 ratio, backed by low-risk assets such as US dollars and short-term government bonds.

When users hold USDC, Circle invests these funds in US Treasuries and other assets to earn interest income, while USDC holders do not receive interest.

This model is essentially a form of "interest-free financing" where Circle invests user funds without needing to pay costs, similar to how banks absorb deposits and then lend, but with lower risk (since investments are in government bonds rather than loans).

Circle's business model can be viewed as digital dollar bond arbitrage.

Thus, Circle's profitability relies on two variables:

First, the circulation of USDC; the larger the circulation, the greater the scale of reserve assets, and the higher the interest income;

Secondly, the interest rate environment directly determines reserve income, and a high-interest environment is extremely favorable for Circle.

Although Circle has occupied the ecological niche of being the "leader of compliant stablecoins," and can eat more cake as the track grows, the Federal Reserve has now entered a rate-cutting cycle, and US Treasury yields may drop to 2% or lower, which would directly halve Circle's profits.

In addition, more and more traditional finance is entering the market, coupled with competitors (some emerging stablecoins) beginning to pay interest to holders, Circle's "interest-free financing" model will face challenges and may further lose market share of compliant stablecoins.

At this point, Circle has only reserve income as a profit point, making it impossible for Circle to support a higher market valuation.

The solution provided by Circle is:

(1) Accelerating the promotion of Circle Payments Network: Circle launched Circle Payments Network in May 2025, aiming to provide instant, low-cost cross-border payment services using USDC, connecting banks, digital wallets, and payment service providers.

(2) Developing value-added services: developing USDC custody and asset management tools aimed at institutional clients (such as crypto funds and banks), charging management fees.

(3) Exploring non-US dollar stablecoins and emerging markets: Circle has issued EURC (Euro-pegged stablecoin) and plans to promote USDC and EURC in Asia and Latin America, where growth in these new markets has been quite fruitful.

2. High Costs

60% of Circle's revenue goes to Coinbase, primarily as distribution and promotion fees.

Among these, the revenue-sharing ratio poses a significant burden for Circle.

Why does Circle give 60% of its revenue to Coinbase?

This relates to the development history of USDC, as Circle and Coinbase are the co-founders of USDC.

Circle is responsible for issuing USDC and managing reserve assets, while Coinbase provides distribution channels, technical support, and marketing, with both parties sharing USDC reserve income (mainly from US Treasury interest) based on agreements.

When USDC was first launched in 2018, Circle's brand and distribution capabilities were weak, relying on Coinbase's exchange status and user network to rapidly expand USDC's market share, hence Coinbase dominated the partnership.

Coinbase is the leader of compliant exchanges in the US, with strong bargaining power.

Moreover, for a long time, the circulation and trading volume of USDC have been highly dependent on Coinbase's infrastructure, making it difficult for Circle to detach in the short term.

For example, in 2024, based on a total circulation of $32 billion, Coinbase contributed approximately 50%-60% of USDC's circulation, roughly $16-19.2 billion.

In the cooperation agreement between Circle and Coinbase, there is actually a rather interesting clause:

If Circle is unable to distribute this dividend to Coinbase under certain circumstances, or if there are some regulatory issues, Coinbase has the right to become the issuer of USDC itself, which means it can take USDC and become the issuer.

Although USDC is currently fully issued and operated by Circle, Coinbase still plays a relatively important role.

Circle has also recognized the long-term risks of high revenue sharing, so it has taken some measures, such as renegotiating revenue-sharing agreements and building its own distribution channels.

For the former, renegotiating revenue-sharing agreements is still challenging, as there are legal agreements in place that constrain Circle from escaping these limitations;

Meanwhile, building its own distribution channels can effectively alleviate the profit pressure from high revenue sharing.

3. Profit Fluctuations

We must admit a fact: the market capitalization of stablecoins is still strongly correlated with the cyclical fluctuations of the cryptocurrency industry.

The alternating bull and bear markets in the cryptocurrency sector directly influence the overall scale of the stablecoin market.

Circle reported a net loss of $768.8 million in 2022, largely due to the crypto bear market;

However, the profit of $267.6 million in 2023 is attributed to cost control and rising interest rates;

By 2024, it drops back to $155.7 million due to surging distribution costs.

We can review the changes in USDC issuance, which have several key points:

The first key point is the DeFi summer of 2020, when the issuance of USDC reached $55 billion;

The second key point is the UST collapse in 2022, which brought a large influx of funds into USDC, allowing it to maintain a high market cap for a long time during the crypto bear market;

The third key point is the strong rise of Solana in early 2023, which allowed USDC to grow well compared to USDT;

The fourth key point is the collapse of Silicon Valley Bank in March 2023, combined with unfavorable regulatory policies from the SEC in the US, which led to a decrease in USDC issuance by about 30%, and by the end of 2023, it had dropped by about 50%.

The fifth key point is that after Trump won the election, stablecoins began to gain traction again, with USDC growing to over $60 billion, an overall increase of 80%.

Therefore, we can see that the bull and bear markets in the cryptocurrency market are extremely important for the growth of stablecoins. Additionally, policies that focus on compliance have a significant impact on stablecoins, especially compliant stablecoins like USDC.

To mitigate profit fluctuations, what Circle needs to do is actually related to the first and second questions: on one hand, diversifying revenue to reduce dependence on interest rates, and on the other hand, optimizing costs to stabilize profit margins.

More importantly, Circle can leverage its compliance advantages to consolidate its market position and cope with fluctuations in the crypto market.

To summarize

Stablecoins can be said to be a transformation of the traditional financial system.

Stablecoins are a crucial infrastructure to replace SWIFT, bank settlements, and the foreign exchange system.

However, Circle's vision extends far beyond issuing stablecoins; Circle aims to build a new financial system, with USDC as the core of this new financial system.

However, Circle also faces many issues, especially the three critical problems mentioned above, which Circle needs to resolve.

Regardless of the outcome, Circle's listing has set a benchmark for the crypto industry, inspiring more people to pay attention to stablecoins, and we can continue to monitor this financial system transformation.